The Bank Told You the Account Is Frozen Until You Produce "Letters of Personal Representative." The County Court Clerk Handed You a Stack of Forms and Said She Cannot Tell You How to Fill Them Out. You Are Standing in the Gap Between a Will That Apparently Means Nothing and a Legal System That Assumes You Already Know the Rules.

You expected the death certificate would be enough. You walked into the bank with the will, the death certificate, and your ID, and the teller said the account is frozen until you present Letters of Personal Representative issued by the county court. You had never heard that phrase before this week. You drove to the county courthouse, and the clerk handed you an Application for Informal Probate and told you — politely, firmly — that she is not permitted to tell you how to complete it, which boxes to check, or what documents to attach. That is Nebraska law. Court staff across all 93 counties are prohibited from providing legal guidance on the forms they distribute.

So now you are home with a blank application, a frozen bank account, a will that everyone keeps telling you "needs to go through probate," and a growing suspicion that one wrong box on one wrong form will cost you weeks or months of delay. Maybe you will file for informal probate when the estate qualifies for a small estate affidavit and waste thousands of dollars on a process you could have avoided entirely. Maybe you will attempt the small estate affidavit before the mandatory 30-day waiting period has elapsed and have the whole thing rejected. Maybe you will miss the 90-day inventory deadline under Section 30-2467 and give the court grounds to remove you. Maybe you will distribute assets before the two-month creditor claim window closes and discover — after the money is gone — that you are personally liable for debts the estate should have paid. Or maybe the decedent owned a small farm, and you will learn too late that the growing crops on that land do not pass to the Transfer on Death deed beneficiary unless the deed explicitly says so — they revert to the formal estate, and now you have an entirely separate legal problem.

The Nebraska Probate Process Guide is a County Court Command Manual for every filing, deadline, tax determination, and decision in a Nebraska probate case — from the initial application through final closing and discharge. Not a generic overview written for all 50 states. Not a blog post designed to funnel you toward an $8,000 legal retainer. A plain-English, Nebraska-specific manual that tells you exactly what the county court clerk cannot: which forms to file, when to file them, what to attach, what the statutory deadlines actually mean, and which mistakes will cost you money or expose you to personal liability.

What's Inside the County Court Command Manual

A step-by-step guide, a filing-readiness checklist, and standalone reference sheets — covering every phase of probate in Nebraska from determining whether you even need to file through final estate closing, built on the Nebraska Revised Statutes and the specific county-level filing rules that make this process different from any other state:

Before You File: Does the Estate Actually Need Probate?

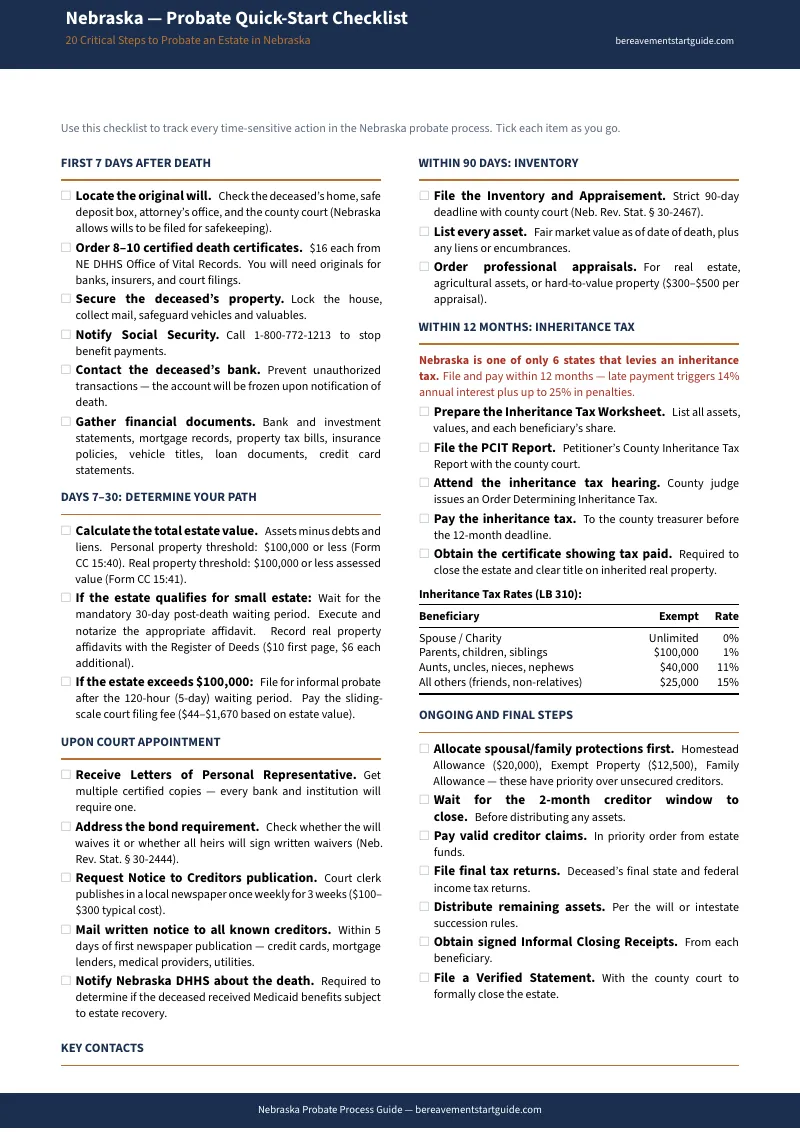

This is the question that determines whether you spend six to twelve months in county court or handle the entire transfer with a notarized affidavit. Following the July 2024 legislative amendment, Nebraska Revised Statutes Section 30-24,129 raised the real property threshold for small estate affidavits from $50,000 to $100,000. Personal property up to $100,000 can be transferred via affidavit under Section 30-24,125. But there are hard requirements that trip people up. You must wait at least 30 days after the date of death before either affidavit can be legally executed. Real estate affidavits must be recorded with the local Register of Deeds alongside a certified death certificate. And here is the part that catches nearly everyone off guard: even if the estate bypasses probate entirely through affidavits or a living trust, you may still owe the Nebraska Inheritance Tax — and settling it requires an independent court proceeding. The guide includes a decision tree that walks you through the exact criteria so you do not open a probate case you could have avoided, and you do not skip a tax proceeding you cannot legally ignore.

Informal vs. Formal Probate: Two Processes With Different Requirements

Nebraska's Uniform Probate Code creates two distinct paths. Informal probate is an administrative process handled by a court registrar — no hearing required, no prior notice to interested parties, and the fastest route for uncontested wills and agreeable families. Formal testacy under Section 30-2425 is actual litigation before a county judge, used when heirs contest the will, when creditors dispute claims, or when the estate requires judicial oversight. The forms are different. The notice requirements are different. The timeline is different. The guide covers both paths from start to finish, including the specific circumstances that force you from the informal track into formal proceedings — because discovering that mid-process, without preparation, is where the real damage happens.

Filing the Application: What the Court Needs and What Triggers a Rejection

The application to open probate is a package, not a single form. You need the original will (if one exists), a certified death certificate, personal information for the proposed personal representative, a list of known heirs and beneficiaries with addresses, and the estimated gross value of the estate. If the will is "self-proved" — meaning it includes a notarized self-proving affidavit — the registrar can process the application without examining witnesses. If it is not self-proved, you may need witness testimony. If only a copy of the will exists, you face an entirely different set of evidentiary requirements. The guide walks through each scenario and the specific documentation that prevents rejections and delays.

Letters of Personal Representative: What They Are and What They Unlock

These are not forms you download. They are judicial documents issued by the court after it approves your application, validates the will (or confirms your appointment as administrator in intestate cases), and is satisfied that bond requirements have been met or waived. Without them, no bank will release funds, no insurance company will pay a claim, no title company will transfer property, and no brokerage will liquidate securities. The guide explains the prerequisites, the timeline between filing and issuance, what delays them, and what to do if the court requires a hearing before granting them.

The 90-Day Inventory: The Deadline Most Executors Learn About Too Late

Within 90 days of your formal appointment, Nebraska Revised Statutes Section 30-2467 requires you to prepare and file a detailed inventory listing every asset the decedent owned at death — with "reasonable detail," fair market value, and the type and amount of any liens or encumbrances. Miss the 90-day deadline, and the court has grounds to remove you as personal representative. Professional appraisals can run $300 to $500 per asset. The guide includes a pre-formatted inventory worksheet designed to meet the court's reporting requirements, so you organize everything systematically instead of scrambling to assemble it as the deadline approaches.

Notice to Creditors: The Two-Month Window That Protects You

After your appointment, you must publish a notice of death in a local newspaper. Once published, creditors have exactly two months from the date of first publication to file a claim under Section 30-2485. If you never publish the notice, creditors retain a three-year window to bring claims against the estate. That is not a theoretical risk — it is a liability that follows you for years. The guide maps the publication requirements, the mechanics of direct notice to known creditors, and the exact sequence that starts and closes the creditor window.

The Nebraska Inheritance Tax: The Shadow Proceeding That Surprises Everyone

This is where Nebraska diverges sharply from most states. The Nebraska Inheritance Tax operates on a tiered system based on the beneficiary's relationship to the decedent. Surviving spouses and individuals under 22 are exempt. Parents, siblings, children, and grandparents pay 1% on amounts above $100,000. Aunts, uncles, nieces, and nephews pay 11% above $40,000. Everyone else — friends, neighbors, charitable organizations not otherwise exempt — pays 15% above $25,000. The critical detail: this tax requires an independent county court proceeding even if the estate avoided probate entirely through trusts, TOD deeds, or small estate affidavits. You must file a Petitioner's County Inheritance Tax Report (Form PCIT) and secure either a waiver or an agreement from the county attorney before the title to any real estate can be cleared. The guide breaks down every tax tier, walks through the PCIT filing process, and explains how to handle the county attorney interaction that stands between you and a clean title transfer.

Medicaid Estate Recovery: The Claim That Reaches Beyond Probate

Under LB 268, the Nebraska Department of Health and Human Services is authorized to recover Medicaid costs from non-probate assets — including joint tenancies, transfer on death deeds, and living trusts. This means that even if you successfully bypass probate, DHHS can pursue the estate for Medicaid reimbursement. The guide explains the formal DHHS notification process, the timeline for responses, how to identify exempt funeral and burial trust accounts, and the steps that protect beneficiaries from unexpected state clawback actions after assets have already been distributed.

Agricultural Land and Farm Assets: The Rules That Do Not Exist in Other States

Nebraska is an agricultural state, and farm property transfers carry rules you will not find in any generic probate guide. If a Transfer on Death deed for agricultural land does not explicitly address the disposition of growing crops, those crops revert to the formal estate — not the deed beneficiary. This catches rural families off guard at the worst possible time. The guide covers agricultural property transfers, county-level variations in filing procedures, and the intersection of farm asset valuations with inheritance tax obligations.

Closing the Estate: Final Accounting and Discharge

Probate does not end when you distribute assets. You must file a Verified Statement with the county court confirming that all creditor claim periods have expired, all legitimate debts and inheritance taxes have been paid, and all remaining assets have been distributed to the rightful heirs. You must obtain a "Certificate showing tax paid" from the separate inheritance tax proceeding before the estate can be formally closed. If you skip this step, your personal liability as personal representative never technically ends. The guide covers the closing mechanics, the Verified Statement requirements, and how to petition for formal discharge.

Who This Guide Is For

- The executor who just found the will and has no idea what happens next — who needs to understand that a will is legally inactive until processed through the Nebraska county court system, and that the path between "holding the will" and "having legal authority" involves specific applications, potential bond requirements, and a court-issued document that unlocks every frozen account

- The surviving spouse or child whose bank accounts were frozen this week — who needs Letters of Personal Representative to regain access and cannot afford months of delay because the application was incomplete or the wrong process was selected

- The family with no will navigating intestate succession — who needs to understand that Nebraska's intestate distribution rules are fixed by statute, that the court will appoint an administrator based on statutory priority, and that the bond requirements and distribution formulas are different from testate cases

- The heir managing a modest estate who wants to avoid probate entirely — who needs the decision tree that maps the $100,000 small estate affidavit thresholds, the mandatory 30-day waiting period, the Register of Deeds recording requirement, and the inheritance tax proceeding that may still be required even after bypassing probate

- The out-of-state executor managing Nebraska property from a distance — who has been named to handle an estate that owns real property in a Nebraska county, has never dealt with the Nebraska Probate Code, and needs every form, deadline, and county-specific filing requirement in one document instead of calling the county clerk repeatedly

- The rural family transferring agricultural land and farm assets — who needs to understand how TOD deed crop provisions, county-level filing variations, and inheritance tax obligations interact for Nebraska farm property in ways that no generic guide covers

Why Free Resources Will Not Get You Through This

Nebraska probate information exists. It is scattered across 93 county court websites, a state self-help center that explicitly warns it "cannot provide forms for all possible situations," attorney blog posts designed to generate retainer clients, and national platforms that treat Nebraska's inheritance tax and Medicaid recovery rules as footnotes. Here is what you actually encounter when you try to navigate probate using free sources:

- The Nebraska Judicial Branch self-help center provides a handful of forms — and explicitly tells you the rest is on you. The state offers small estate affidavit forms (CC 15:40 and CC 15:41) and a limited selection of probate templates. But the website warns that "completion of the Inheritance tax form and Probate Inventory Worksheet can be difficult" and that "this Self-Help Center cannot provide forms for all possible situations." The forms arrive without instructions, without sequencing, and without any guidance on the strategic decisions that determine whether you spend six months in court or six weeks with an affidavit.

- Court clerks across all 93 counties are prohibited from helping you fill out the forms. They will hand you the paperwork and direct you to retain counsel. If the estate is $80,000 and the attorney quotes $4,000 to $6,000, that is 5% to 8% of the entire estate consumed by legal fees — and the court offers no alternative.

- National platforms like SwiftProbate and EstateExec charge more and know less about Nebraska. SwiftProbate charges $39 for a "complete plan" built around generic county guides and an AI assistant. EstateExec charges $199 per estate for accounting software. Neither one explains the LB 310 inheritance tax tiers, the LB 268 Medicaid recovery expansion, the July 2024 small estate threshold changes, or the agricultural TOD deed crop provisions that are unique to Nebraska. They treat all 50 states identically because their business model requires it.

- Attorney-referral platforms like Atticus offer free forms — as a front door to $150-to-$650-per-hour legal representation. The probate content is accurate, emotionally resonant, and designed to make the process look so dangerous that hiring a lawyer feels inevitable. For contested wills and insolvent estates, it might be. For the straightforward estate where the family agrees and the assets are modest, the article never quite tells you that you can do this yourself.

- Local attorney blog posts are detailed, accurate, and written to sell retainers. Every probate firm in Omaha and Lincoln publishes content explaining how complex Nebraska probate is. Their articles end with "schedule a consultation." They never end with "here is how to do it without us."

Free resources give you isolated forms from a state website that refuses to explain them, scattered across 93 counties with 93 sets of local filing rules. The County Court Command Manual puts every Nebraska probate statute, form, deadline, tax determination, and county requirement into one document, in the order you actually need them.

— Less Than Ten Minutes With a Nebraska Probate Attorney

A consultation with a Nebraska probate attorney runs $200 to $400 per hour. Full probate representation for a standard estate costs $6,000 to $12,000. National estate platforms charge $39 to $199 per estate in software fees. This guide costs less than ten minutes of professional legal time and gives you the complete Nebraska-specific probate roadmap — every filing requirement, every statutory deadline, every inheritance tax tier, the Medicaid recovery rules, the small estate affidavit thresholds, and the decision tree that tells you whether you need formal probate at all.

Your download includes the complete step-by-step guide covering informal and formal probate, testate and intestate processes, the standalone Nebraska Probate Filing-Readiness Checklist, and printable reference sheets: the Probate vs. Small Estate Affidavit Decision Tree, Executor Duties Timeline (every statutory deadline from Day 1 through Month 12), Notice to Creditors Compliance Guide, Nebraska Inheritance Tax Quick Reference, Inventory Preparation Worksheet, and Medicaid Estate Recovery Notification Guide. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on what to file, when to file it, and what happens next in your Nebraska county court — email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Nebraska Probate Quick-Start Checklist — an overview of the probate process and the key deadlines, decisions, and documents you need before you walk into the county courthouse. Enough to understand what you are facing and whether you need the full guide.

Probate is not something you were trained for. But it is something you can get through with the right instructions. The guide gives you those instructions, one filing at a time.