The IRS Wants the Final Return. ADOR Wants the Fiduciary Return. The County Recorder Wants a $30 Affidavit. Your Brother in Ohio Just Triggered a Tax Clearance Requirement You Have Never Heard Of. And You Are Supposed to Figure All of This Out While Grieving.

Your spouse — or your parent — died in Arizona. Within weeks, the tax obligations started materializing. The final federal Form 1040 is due. The final Arizona Form 140 is due. If the estate earned any income after the date of death — dividends, interest, a pension payment that arrived two days late — you now owe a separate fiduciary return: federal Form 1041 and Arizona Form 141AZ. If there is a refund owed to the deceased, you need federal Form 1310 and Arizona Form 131 to claim it. Nobody at the IRS is going to tell you about the Arizona forms. Nobody at ADOR is going to tell you about the IRS forms.

You searched online for guidance. The IRS website explains Form 1040 but not Form 140. The Arizona Department of Revenue website explains Form 141AZ but assumes you already know what Distributable Net Income means. A CPA blog in Scottsdale offered a free consultation — which turned into a quote for $2,500 to prepare two returns. TurboTax says it can handle the final return, but it cannot tell you that the number you are about to enter as the property's cost basis is wrong — and that mistake alone could generate a capital gains bill tens of thousands of dollars larger than it should be.

Meanwhile, you just learned that Arizona's community property rules give surviving spouses a "double step-up in basis" that could erase decades of capital gains on the family home. But only if you document it correctly, with the right appraisal, filed the right way. If you use the County Assessor's value instead of a professional date-of-death appraisal, the IRS will not accept it. And nobody volunteered this information — you found it buried in a paragraph on a law firm's blog between the firm's biography and a prompt to schedule a retainer consultation.

The Arizona Estate Tax Compliance Sequencer

The Arizona Final Tax & Estate Tax Guide is The Arizona Estate Tax Compliance Sequencer — a plain-English guide that maps every federal and state tax filing obligation after a death in Arizona, puts them in the exact order you need to complete them, and explains the specific strategies, thresholds, and traps that determine whether you close the estate correctly or create liabilities that follow you for years.

Not a national overview that mentions Arizona in a footnote. Not a TurboTax help article that stops at "consult a tax professional." Not a CPA blog designed to generate $300-per-hour retainer clients. A structured, Arizona-specific operational manual built on the Internal Revenue Code, Arizona Revised Statutes Title 43, and current 2026 IRS and ADOR thresholds — covering every form, every deadline, every basis calculation, and every compliance trap from the week of death through estate closure.

What's Inside The Arizona Estate Tax Compliance Sequencer

A 12-chapter guide plus a Tax After Death Checklist — sequencing every tax obligation from Day 1 through estate closure, with exact 2026 statutory thresholds and form-by-form instructions:

Arizona's Tax Position: What You Owe and What You Don't

Arizona has no state estate tax and no state inheritance tax. When an Arizona resident dies, not a single dollar is owed to the state simply for transferring wealth to heirs. But Arizona does tax income at a flat 2.5% rate (transitioning to 2.47% in 2026), and every dollar the deceased earned or the estate generates after death is fully taxable. The guide clears up the four misconceptions that cost Arizona families the most money: confusing probate avoidance with tax avoidance, using the original purchase price instead of the stepped-up basis, assuming small estates have no filing obligations, and relying on tax software to catch strategic errors it was never designed to detect.

First 30 Days: The Tax Foundation You Cannot Skip

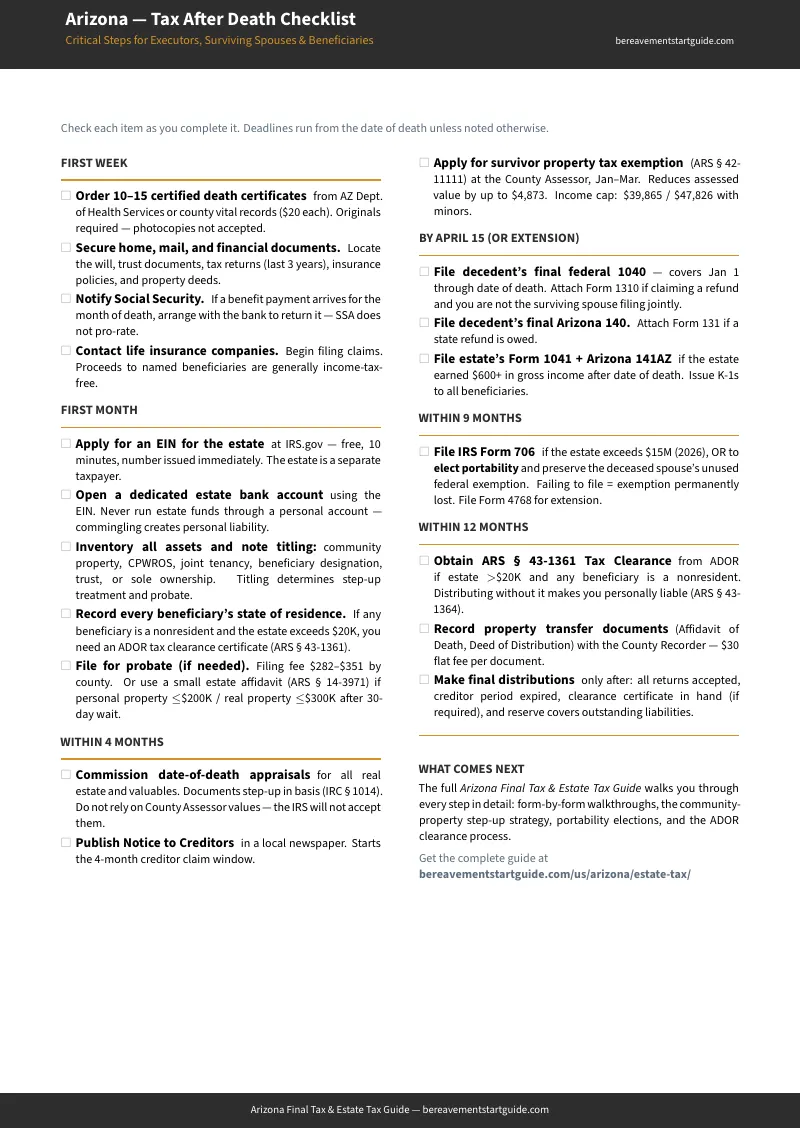

How to apply for an EIN for the estate at IRS.gov — free, takes 10 minutes, produces the number immediately. Opening a dedicated estate bank account (never run estate funds through a personal account — commingling creates personal liability). Ordering 10 to 15 certified death certificates at $20 each. Building the asset inventory that determines everything downstream: community property, CPWROS, joint tenancy, beneficiary deed, trust, or sole ownership — because titling determines step-up treatment, probate requirements, and filing obligations. Identifying every beneficiary's state of residence — if any beneficiary lives outside Arizona and the estate exceeds $20,000, the ARS 43-1361 tax clearance trap activates.

The Decedent's Final Income Tax Returns: Form 1040 and Form 140

Step-by-step instructions for filing the final federal Form 1040 and Arizona Form 140 for the period January 1 through the date of death. When a surviving spouse can — and should — file jointly for the year of death. How to handle income that arrived after the date of death (pension payments, Social Security, final paychecks). Part-year and nonresident forms (Form 140PY and Form 140NR) when the decedent lived in or earned income from multiple states. Deadlines, extensions, and the specific errors that generate ADOR and IRS notices.

Claiming Refunds: The Form 1310 and Form 131 Workflow

If the deceased overpaid taxes, the estate is owed a refund. But neither the IRS nor ADOR will release it without proof of your legal authority to claim it. The guide walks through federal Form 1310 and Arizona Form 131 line by line: who qualifies to file, what supporting documents to attach, what to do when no personal representative was formally appointed by the probate court, and the specific clerical errors — wrong checkbox, missing attachment, name mismatch — that cause administrative rejections and delay refunds by months.

Estate Fiduciary Income Tax: Form 1041 and Form 141AZ

After the date of death, the estate itself becomes a taxpayer. Any income generated by the decedent's assets — dividends, interest, rental income, capital gains from asset sales — belongs to the estate and must be reported on federal Form 1041 and Arizona Form 141AZ when gross income exceeds $600. The guide explains the Distributable Net Income pass-through mechanism that shifts tax liability from the estate to beneficiaries, how to issue Schedule K-1s, the 5.5-month automatic extension available for Form 141AZ, estimated tax payments via Form 141AZ ES, and the special apportionment rules for nonresident beneficiaries who are only taxable on Arizona-source income.

The Double Step-Up in Basis: Arizona's Most Powerful Tax Strategy

Under IRC § 1014, inherited assets receive a step-up in cost basis to their fair market value at the date of death. But in Arizona — a community property state — married couples who hold assets as Community Property with Right of Survivorship (CPWROS) receive a double step-up: both the decedent's half and the surviving spouse's half are reset to current market value under IRC § 1014(b)(6). A home purchased for $200,000 and worth $800,000 at death? The surviving spouse's new basis is $800,000. Selling immediately produces zero capital gains. The guide explains exactly how to document this with a professional date-of-death appraisal (not the County Assessor's value — the IRS will reject it), how to distinguish community property from separate property, and how to defend the double step-up in an audit.

Selling Inherited Property: Capital Gains, 1099-S, and Beneficiary Deeds

When heirs sell an inherited house, the transaction must be reported to both the IRS and ADOR. The guide explains capital gains calculation using the stepped-up basis, how to report 1099-S proceeds on Schedule D, the $250,000 and $500,000 home sale exclusion for primary residences, and the critical difference between selling shortly after death (minimal gains) versus holding for years (new gains accumulate above the stepped-up basis). For beneficiary deed transfers: recording an Affidavit of Death at the County Recorder ($30 per document under ARS § 11-475), the Affidavit of Property Value exemption, and why avoiding probate through a beneficiary deed does not avoid any of these tax obligations.

The ARS 43-1361 Tax Clearance Trap

The most frequently overlooked compliance requirement in Arizona estate administration. If the gross value of the estate exceeds $20,000 and any beneficiary lives outside Arizona, the probate court is legally barred from closing the estate until the executor obtains a Certificate of Payment of Taxes from the Arizona Department of Revenue. This is a separate application from the Form 141AZ tax return — filed with ADOR's Collections Administrative Support division. Under ARS § 43-1364, an executor who distributes assets to nonresident beneficiaries without this certificate becomes personally liable for any unpaid state taxes. Not the estate's money — the executor's money. The guide explains when the certificate is required, how to apply, expected processing time, and how to structure distributions to avoid triggering personal liability.

Federal Estate Tax and the Portability Election

The OBBBA permanently set the federal estate tax exemption at $15 million per individual ($30 million for married couples) in 2026. The vast majority of Arizona families will never owe federal estate tax. But for married couples, the executor must file IRS Form 706 within 9 months of the first spouse's death to elect portability — formally preserving the deceased spouse's unused $15 million exemption for the surviving spouse's eventual estate. If the executor does not file, $15 million in exemption is permanently and irrevocably lost. The guide explains exactly when Form 706 is legally required, when it is merely strategic, and why filing a protective Form 706 is a fundamental fiduciary duty for married estates even when no tax is currently owed.

Small Estate Shortcuts and the Probate-Tax Distinction

Arizona expanded its small estate affidavit thresholds in 2025 under ARS § 14-3971: $200,000 for personal property and $300,000 for real property. Estates below these limits can skip formal probate entirely. But this legislative convenience has created an explosion of "orphan executors" — families who successfully bypass the court system and then assume the tax system was bypassed too. It was not. The final returns, fiduciary returns, capital gains obligations, and tax clearance requirements remain in full force. The guide explains the affidavit process (30-day waiting period for personal property, 6-month waiting period for real property), what qualifies, what does not, and exactly which tax obligations survive even when probate does not.

When to Hire a CPA or Attorney

For straightforward estates — single state, no business interests, assets well below the $15 million federal threshold — this guide handles what you need. But certain situations require professional help, and pretending otherwise would be irresponsible. The guide includes a diagnostic checklist identifying the specific red flags: business ownership, multi-state real estate, closely held entities, prior-year unfiled returns, estates approaching the federal exemption, irrevocable trusts generating their own income. It also explains what to organize before the first CPA appointment to reduce billable hours — because showing up with sorted documents instead of a shoebox can cut a $2,500 engagement in half.

Complete Timeline and Deadline Calendar

A month-by-month roadmap from the week of death through estate closure. When to get the EIN. When Form 140 and Form 1040 are due. When Form 1041 and Form 141AZ are due. When to file Form 706 for portability. When to apply for tax clearance. When to make final distributions. Each deadline includes the consequence of missing it — penalties, interest, personal liability, or permanent forfeiture of exemptions.

Who This Guide Is For

- The surviving spouse who just discovered the "double step-up in basis" — Your spouse handled the taxes for decades. Now you are staring at forms you have never seen — Form 140, Form 131, Form 141AZ — and someone mentioned that Arizona's community property rules could save you tens of thousands in capital gains when you sell the house. But nobody explained how to document it, and TurboTax will not do it for you. The guide walks you through the entire basis documentation process in order.

- The executor who has never done this before — You were named personal representative in your parent's will. You have a fiduciary duty to the beneficiaries, a legal obligation to file every required return, and personal liability if you distribute assets before clearing tax obligations. You need to know which forms to file, in what order, by when — and what happens if you miss a deadline. The guide gives you the operational checklist.

- The out-of-state heir inheriting Arizona property — Your parent died in Arizona and left you a house, a bank account, or both. You live in Ohio. You searched "Arizona inheritance tax" and got conflicting results. You want to know: do you owe Arizona taxes on your inheritance? What happens when you sell the property? Will the executor need a tax clearance certificate because you are out of state? The guide answers every question and explains what your non-residency triggers for the estate.

- The family relying on a beneficiary deed and assuming taxes are handled — Your parent set up a beneficiary deed years ago. The family believes the house "just transfers" and taxes do not apply. That is dangerously incomplete. The deed avoids probate — it does not avoid income tax, capital gains tax, or federal estate tax. The guide explains exactly what tax obligations survive a beneficiary deed transfer and how to handle them.

Why Not Just Google It?

You can find every individual piece of information in this guide on the internet. The IRS publishes Form 1040 instructions. ADOR publishes Form 141AZ instructions. Legal blogs explain the step-up in basis. County Recorder websites list recording fees.

The problem is not access to information. The problem is that no single source connects the pieces. The IRS will not tell you about Form 141AZ. ADOR will not tell you about IRC § 1014(b)(6). The CPA blog explaining the step-up in basis does not mention the ARS 43-1361 tax clearance certificate. The county website explaining beneficiary deed recording does not warn you about the capital gains reporting that follows. You end up reading twenty different sources across five different agencies and still missing the interaction between them that creates the actual liability.

This guide exists because scattered accurate information is functionally the same as no information when a single missed connection costs you thousands of dollars or creates personal liability.

Why Not Just Hire a CPA?

For complex estates — business ownership, multi-state holdings, assets near the $15 million federal threshold — you absolutely should hire a CPA. The guide tells you when.

But for the majority of Arizona estates, the first CPA consultation reveals a straightforward process wrapped in a $2,500 minimum retainer. The CPA will ask you to gather documents, organize asset records, determine titling, and compile income statements — the exact same work this guide walks you through. The difference: you can do that organizational work yourself for a fraction of a single billable hour, bring the CPA a sorted file instead of a shoebox, and either complete the filings yourself or cut the professional engagement in half.

The guide is not a replacement for professional advice on complex estates. It is a replacement for paying $300 an hour for someone to explain what Form 141AZ is, when you need an EIN, and how the step-up in basis works. Those are not $300-per-hour questions. They are questions this guide answers in plain English.

Satisfaction Guarantee

If this guide does not save you at least its cost in CPA consulting time, tax preparation clarity, or capital gains documentation — email [email protected] within 30 days for a full refund. No forms. No questions. No hassle.

— Less Than 6 Minutes of a CPA's Billing Clock

Estate CPAs in Arizona charge $250 to $400 per hour. An initial consultation runs $500 to $1,000 — and you leave with a list of forms to figure out yourself. The guide costs — once, no subscription, no hourly meter.

You receive the complete 12-chapter guide plus the printable Tax After Death Checklist. Every form, every deadline, every strategy — sequenced from the week of death through estate closure so you spend your time executing, not searching.

Not ready for the full guide? Download the free Arizona Tax After Death Checklist — the 19 most critical actions organized by timeframe. It covers the essentials while you decide whether the complete guide is right for your situation.

The IRS will not sequence your filings for you. ADOR will not warn you about the tax clearance trap. TurboTax will not tell you to use the stepped-up basis instead of the original purchase price. This guide does all three.