The Fiduciary Compliance System for California Estates

California has no estate tax. California has no inheritance tax. And that single fact has destroyed more middle-class estates than any tax bill ever could.

Because families hear "no estate tax" and assume they are done. They are not done. They have not even started. The Franchise Tax Board requires a fiduciary income tax return (Form 541) the moment an estate earns $10,000 in gross income — or a trust earns just $100 in net income. The county assessor will reassess the family home at full market value under Proposition 19 unless the heir moves in within exactly one year. The Department of Health Care Services will pursue Medi-Cal estate recovery against the probate estate. And the title company will withhold 3.33% of the gross sale price at closing unless Form 593 is completed correctly — which even FTB representatives cannot agree on how to do.

Meanwhile, a California CPA charges an average of $175 per hour, with flat fees for a single Form 1041 starting at $600 and scaling past $950 for trust specialists. A probate attorney's statutory fees under Probate Code Sections 10800 and 10810 consume 4% of the first $100,000, 3% of the next $100,000, and 2% of the next $800,000 — a standard $500,000 estate yields $13,000 in attorney fees before a single dollar reaches the heirs.

The California Final Tax & Estate Tax Guide is the plain-English operational manual that sits between free-but-incomprehensible government forms and a $4,000 CPA retainer. Seventeen chapters. Every form number. Every deadline. Every calculation. Written for the executor, trustee, surviving spouse, and beneficiary who needs to act now — not schedule a consultation.

What You Get

The Proposition 19 Defense Protocol

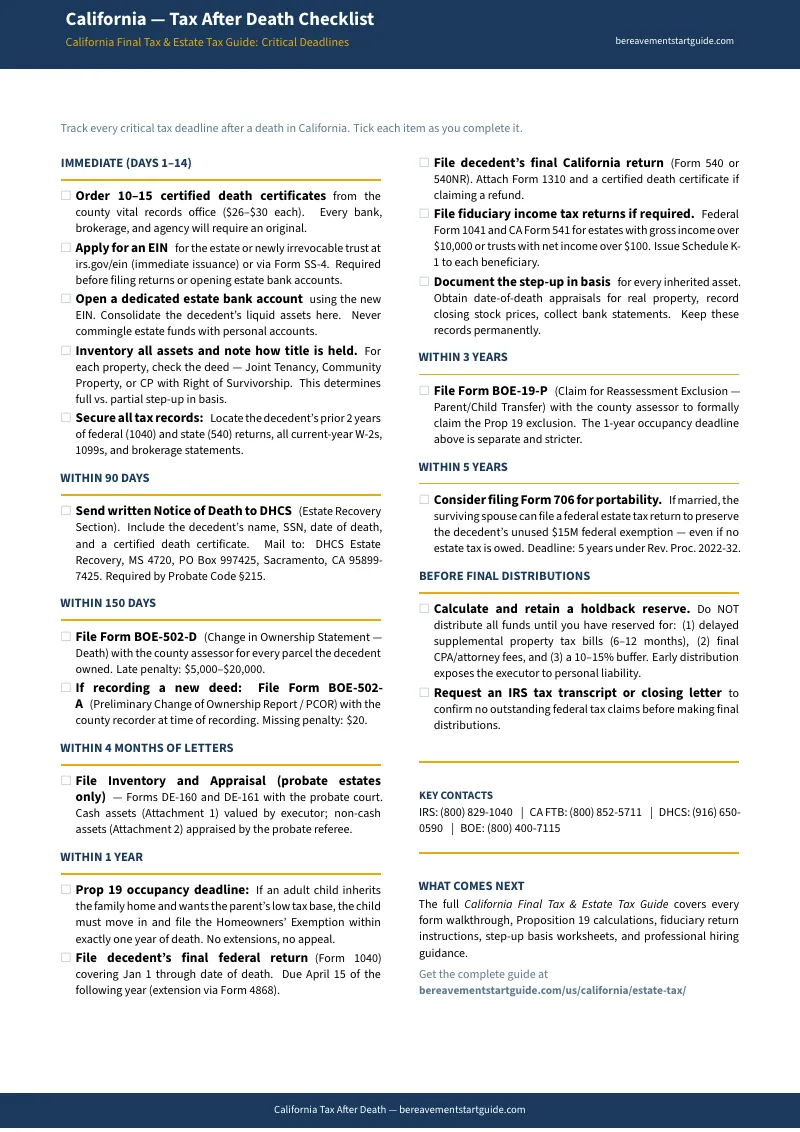

The single most dangerous trap in California estate administration. Your parent's home was assessed at $180,000 in 1987. Today it is worth $1.1 million. Under Proposition 19, you have exactly one year from the date of death to establish primary residency and file the Homeowners' Exemption — or the county assessor reassesses the property at current market value, increasing the annual tax bill from $2,200 to over $14,000. The guide walks you through the 2026 inflation-adjusted exclusion cap of $1,044,586, the Factored Base Year Value calculation, and the exact steps for filing Form BOE-19-P. No extensions. No appeals. No second chances.

The Form 593 Escrow Cheat Sheet

When you sell an inherited home in California, the title company hands you FTB Form 593 and demands you certify an exemption under penalty of perjury — or the state withholds 3.33% of the gross sale price. On a $900,000 home, that is $29,970 locked in escrow. The guide explains exactly which exemption box applies to inherited property versus a principal residence, how the step-up in basis often means zero capital gains on the sale, and how to work with the title company to clear escrow without losing tens of thousands of dollars.

The Fiduciary Income Tax Roadmap

Most executors have no idea they are required to file California Form 541 — or that the threshold is a mere $10,000 in gross income. A single inherited brokerage account paying standard dividends can trigger this filing. The guide covers the complete Form 541 workflow: when to file, how to issue Schedule K-1 to beneficiaries, the 65-day distribution rule for Form 541-T, estimated tax safe harbors for Form 541-ES, and what out-of-state beneficiaries actually owe California.

The Community Property Double Step-Up

In California, when one spouse dies, the entire value of community property — not just the decedent's half — is stepped up to fair market value at death. This can eliminate decades of accumulated capital gains liability. But only if the property is titled correctly. Joint Tenancy gives you a 50% step-up. Community Property with Right of Survivorship gives you 100%. The guide includes a title vesting comparison table and shows you how to use the Spousal Property Petition (Form DE-221) to confirm community property status and secure the full benefit.

The Complete California Tax Calendar

Every deadline mapped chronologically — from ordering death certificates on day one through the portability election five years later. The 90-day DHCS notification under Probate Code Section 215. The 150-day Form BOE-502-D filing with the county assessor. The one-year Proposition 19 occupancy deadline. The two-year estimated tax trigger. The five-year portability window for Form 706. Miss one deadline and the financial consequences are permanent.

The Holdback Reserve Worksheet

Supplemental property tax bills arrive six to twelve months after a home transfers. If you distribute all estate funds to beneficiaries before those bills arrive, the executor becomes personally liable. The worksheet calculates exactly how much cash to retain in the estate account based on appraised property value, current tax rates, and estimated professional fees.

The CPA Handoff Packet

If your estate is complex enough to need a CPA, the guide ensures you walk in organized. A checklist of every document to gather before the first meeting — Form 1310s, EIN confirmation letters, prior-year returns, PCORs, probate referee appraisals — so you pay for one hour of targeted execution instead of five hours of document organization at $175 per hour.

Who This Is For

- Executors and administrators who need to know exactly which federal and state forms to file, in what order, by when — without paying a CPA to explain the basics

- Surviving spouses who need to secure the community property double step-up, understand portability, and protect assets from Medi-Cal recovery

- Adult children inheriting a home who are facing a Proposition 19 reassessment and need to decide whether to move in, rent, or sell — with exact calculations, not general advice

- Successor trustees whose parent's revocable living trust just became irrevocable and who must file Form 541 and issue K-1s without probate

- Out-of-state beneficiaries who received a K-1 from a California trust and need to know if they owe California tax

- Families selling an inherited home who need Form 593 completed correctly before escrow closes

Why Free Resources Are Not Enough

The IRS publishes forms. The FTB publishes instructions. The Board of Equalization publishes Proposition 19 guidelines. And they are all scattered across different websites, written in statutory language, and deliberately designed to present the raw data without strategic guidance.

To resolve a single inheritance issue, you must cross-reference the IRS site for the $15 million federal threshold, navigate the FTB site for Form 541 filing rules, decipher BOE publications for Proposition 19 caps, and locate your specific county assessor's website for BOE-19-P filing procedures. No agency connects these dots for you. No agency tells you that checking the wrong box on Form 593 locks up 3.33% of your home sale. No agency warns you that the Proposition 19 deadline has no extension and no appeal.

Law firm blogs come closer — but they are lead-generation funnels. The article explains the problem beautifully, then stops short of the step-by-step solution: "Contact us for a free consultation." You leave knowing what you should be afraid of, but not what to do about it.

TurboTax and H&R Block handle personal returns well. They fail badly on fiduciary returns. Form 1310 for deceased taxpayer refunds frequently errors out, forcing manual paper filing. Schedule K-1 generation for trusts is notoriously unreliable. The software assumes you know what numbers to enter — it does not teach you which numbers are legally correct.

This guide fills the gap. Every form, every box, every calculation, every deadline — in chronological order, in plain English, with no consultation upsell at the end.

Your Files

- California Final Tax & Estate Tax Guide — 17 chapters covering Form 541, Form 593, Proposition 19, step-up in basis, Medi-Cal recovery, probate fees, inherited IRAs, portability elections, and the complete tax calendar. Plus agency directory, forms reference, and glossary.

- Quick-Start Checklist — one-page summary of the 18 most critical steps, organized by deadline

- Proposition 19 Calculation Worksheet — fillable FBYV + exclusion cap math, with spaces for your property's specific numbers

- Form 593 Escrow Guide — quick reference for which exemption box to check so the title company does not withhold 3.33% of your home sale

- Tax Deadline Calendar — 15 chronological deadlines from day one through year five on a single page

- Title Vesting Comparison — Joint Tenancy vs. Community Property vs. CPWROS step-up comparison at a glance

- Holdback Reserve Worksheet — calculates how much cash to retain before distributing to beneficiaries

- CPA Handoff Checklist — 14-item document checklist to bring to your first professional meeting

— Less Than Fifteen Minutes of a CPA's Time

A California CPA charges an average of $175 per hour for estate work. The statutory probate attorney fee on a $500,000 estate is $13,000. A single missed Proposition 19 deadline can increase your property taxes by $12,000 per year, permanently. This guide costs less than a quarter-hour of professional time — and it may save you from ever needing to buy that quarter-hour.

The Clarity Guarantee

If this guide does not save you at least two hours of frustrating bureaucratic research, or prevent at least one expensive filing mistake, email us within 30 days for a full, no-questions-asked refund.

This guide provides comprehensive educational information and operational checklists. It does not constitute individualized legal, accounting, or tax advice. Every estate is unique, and laws are subject to legislative change. Use this guide to understand your fiduciary obligations, organize your mandatory state filings, and know exactly what strategic questions to ask if you choose to hire a licensed California CPA or probate attorney.