The CalPERS Packet Arrived. 47 Pages. Three Different Survivorship Options. A 45-Day Processing Window That Starts When They Receive Your Completed Application --- Not When Your Spouse Died. And Nobody Told You That Your Registered Domestic Partnership Means Nothing to Social Security.

Someone you love just died in California. You called CalPERS because your spouse was a retired state employee. The representative said a survivor benefit packet was on the way. It arrived eleven days later: 47 pages, three survivorship options with different payout structures, an irrevocable election form, and a list of supporting documents including a certified death certificate, a marriage certificate, and a notarized affidavit. You called back to ask which option to choose. The representative said they "cannot provide financial advice" and suggested you consult a financial planner. The processing window is 45 days from the date they receive your completed application. If you submit it incomplete, the clock resets.

Then the health insurance question hit. Your spouse's employer-sponsored plan covered the family. The plan administrator said COBRA continuation is available for 36 months --- at $3,400 per month, the full unsubsidized premium. You have heard of Covered California but do not know if you qualify for subsidies, what the 60-day special enrollment window means, or whether Medi-Cal is an option. The 60-day window started the day your spouse died. Not the day you found out about it. Not the day you got around to looking into it. The day they died.

You went online. The Social Security Administration website says you may be eligible for a $255 lump-sum death payment and monthly survivor benefits. You started the application. Then you discovered that your 12-year registered domestic partnership --- recognized by every California state agency, every county office, and every employer in the state --- does not exist as far as federal Social Security is concerned. The $255 payment, the monthly survivor benefits, the Medicare eligibility: none of it applies to you. California gave you every right a married spouse has. The federal government did not.

Meanwhile, the county assessor sent a Proposition 19 notice about the house. A workers' compensation representative left a voicemail about a death benefits claim you did not know existed. The Department of Veterans Affairs sent a form about burial allowances. The California Victim Compensation Board has a program you have never heard of. And each of these agencies operates on its own timeline, its own forms, its own deadlines --- none of which reference each other, none of which tell you the order, and none of which warn you what you lose if you miss their window.

Here is the reality: California survivors are entitled to more benefits than survivors in almost any other state --- Social Security, CalPERS, CalSTRS, workers' compensation death benefits up to $320,000, Proposition 19 property tax protection, VA survivor benefits, Cal-COBRA and Covered California health insurance options, county indigent burial programs, and victim compensation funds. But the benefits are administered by 20+ separate agencies with different forms, different deadlines, and zero cross-referencing. No single government office will tell you what you are entitled to. No single website lists everything. And the deadlines for some of the largest benefits --- 60 days for health insurance, 240 weeks for workers' compensation, one year for Proposition 19 --- run silently from the date of death whether you know about them or not.

The California Survivor Benefits Navigator is the complete benefits recovery system --- the step-by-step operational roadmap that identifies every benefit available to California survivors, sequences every application in deadline order, and walks you through the specific forms, documentation, and follow-up procedures for each agency. Not a generic "benefits after death" overview with California in the title. Not a list of phone numbers. A 15-chapter, California-specific manual that covers Social Security survivor benefits (and the federal gap for domestic partners), CalPERS and CalSTRS pension survivorship elections, county pension systems like LACERA and SDCERA, workers' compensation death benefits under Labor Code 5406, Proposition 19 property tax protection, health insurance continuation, VA survivor benefits, victim compensation, indigent burial programs, and the master timeline that puts every deadline on one calendar so nothing falls through the cracks.

What's Inside the California Survivor Benefits Navigator

A 15-chapter guide and the Survivor Benefits Checklist --- covering every benefit, every agency, and every deadline available to California survivors, organized chronologically from the first week through ongoing claims, built specifically for California statutes, state pension systems, and the federal-state gaps that make claiming benefits here unlike any other state:

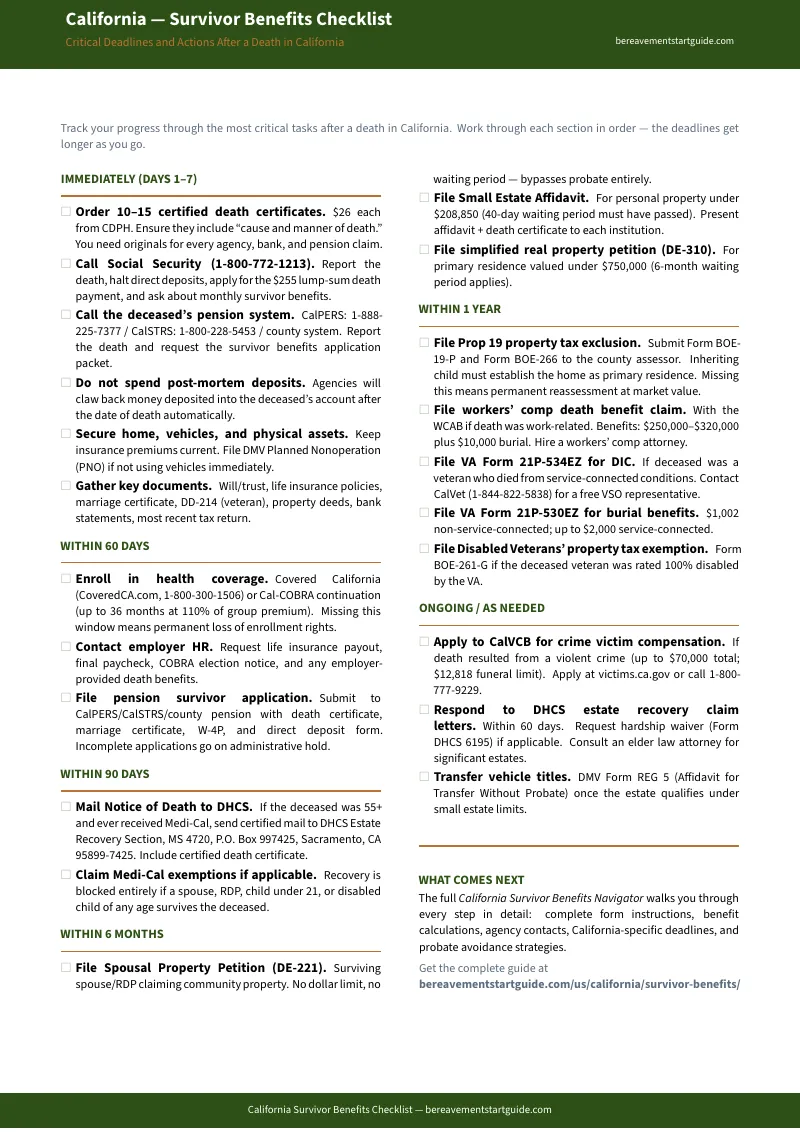

Chapter 1: The First Week --- Immediate Triage

Before you can claim any benefit, you need the documentation that every agency requires. This chapter covers ordering certified death certificates (10-15 authorized copies --- not informational copies, which no agency will accept), halting the deceased's own benefit payments before overpayments create recovery demands, and securing assets that agencies will ask about on their applications. It also covers the calls you need to make in the first 72 hours: Social Security, the deceased's employer, CalPERS or CalSTRS if they were a public employee, and the VA if they were a veteran. Each call triggers a different process with a different timeline, and this chapter tells you what to say on each call and what to request.

Chapter 2: The First Month --- Health Insurance and State Notifications

This is the chapter that saves families from financial catastrophe. When employer-sponsored health insurance ends, California survivors face a brutal choice: Cal-COBRA continuation at $3,400 or more per month for the full unsubsidized premium, or Covered California marketplace plans with potential subsidies that can drop that to $200 to $400 per month. The difference is tens of thousands of dollars per year --- but the special enrollment window is 60 days from the qualifying event. Miss it and you wait until open enrollment or go uninsured. This chapter also covers the 90-day Medi-Cal notification deadline, the DHCS 9060 form, and the specific state agencies that need to be notified within 30 days.

Chapter 3: Social Security Survivor Benefits

The federal $255 lump-sum death payment. Monthly survivor benefits for widows and widowers (up to 100% of the deceased's benefit amount at full retirement age). Benefits for dependent children under 18. The earnings test that reduces benefits if you are still working. Why the Government Pension Offset no longer reduces Social Security survivor benefits for CalPERS and CalSTRS families who did not pay into Social Security — it was repealed for benefits payable January 2024 onward, so the pension and the full survivor benefit can finally be drawn together — plus how to check the SSA paid the retroactive catch-up it owes you, and why the teachers' families who never applied because the GPO would have wiped the benefit out must file now rather than wait to be found. And the "Federal Gap" --- the chapter that no other guide covers: registered domestic partners in California have full state-level spousal rights but zero federal Social Security survivor benefits. No $255 payment. No monthly benefits. No Medicare based on the deceased partner's record. This chapter explains what the gap means, which state benefits partially compensate, and the specific financial planning implications for surviving domestic partners.

Chapter 4: California Public Pension Survivor Benefits

CalPERS, CalSTRS, and county pension systems are the largest source of ongoing income for many California survivors --- and the most complex to navigate. CalPERS offers multiple survivorship options with different payout structures, and the election you make is irrevocable. CalSTRS has two completely different benefit structures: Coverage A (members hired before 2013) and Coverage B (members hired after), with different survivorship rules, different calculation methods, and different application forms. County systems like LACERA (Los Angeles), SDCERA (San Diego), and UCRP (University of California) have their own rules, their own forms, and their own processing timelines. This chapter walks through each system, explains the survivorship options in plain language, identifies the irrevocable decisions you cannot undo, and tells you exactly what documentation each system requires.

Chapter 5: Probate Bypass Strategies

Before you spend months in probate court, this chapter identifies the transfer mechanisms that bypass it entirely. The Small Estate Affidavit for estates under $208,850 in personal property --- no court filing, just a sworn declaration after a 40-day waiting period. The Spousal Property Petition (Form DE-221) for surviving spouses --- no dollar limit, typically processed in 30 to 60 days. Community property with right of survivorship that transfers automatically by operation of law. This chapter covers which assets qualify for each pathway and how to use them in combination --- the DE-221 for the house, the affidavit for the bank accounts, and the TOD registration for brokerage accounts, all simultaneously.

Chapter 6: Property Tax Protection

Proposition 19 changed everything for inherited homes in California. A home your parent bought for $180,000 in 1987 --- now assessed at $900,000 --- will be reassessed to current market value unless the inheriting child moves in within one year and claims the homeowners' exemption. That means property taxes jumping from $3,200 to over $15,000 per year, permanently. But the exclusion exists: if you file the BOE-19-P form within the deadline, move in, and claim the exemption, you can preserve the parent's tax base on the first $1,044,586 of assessed value above the original base. This chapter covers the BOE-19-P filing sequence, the disabled veteran exemption that provides additional property tax relief for qualifying survivors, and the California Property Tax Postponement Program for seniors and disabled persons who inherited a home they cannot afford to keep without tax relief.

Chapter 7: Workers' Compensation Death Benefits

If the deceased died from a work-related injury or illness, the surviving dependents are entitled to workers' compensation death benefits of $250,000 to $320,000 depending on the number of dependents, plus a $10,000 burial allowance. These are among the largest single benefits available to California survivors --- and among the least known. The statute of limitations under Labor Code Section 5406 is 240 weeks (approximately 4.6 years) from the date of death, but the earlier you file, the sooner payments begin. This chapter covers who qualifies as a dependent, how to file the claim with the Workers' Compensation Appeals Board, what documentation is required, and how the benefit is calculated and distributed among multiple dependents.

Chapter 8: Veterans Affairs Survivor Benefits

If the deceased was a veteran, the surviving spouse and dependents may be entitled to Dependency and Indemnity Compensation (DIC) --- a monthly tax-free benefit for survivors of veterans who died from service-connected conditions or who were rated 100% disabled for at least 10 years. The VA burial allowance starts at $1,002 for non-service-connected deaths and goes higher for service-connected deaths. The Presidential Memorial Certificate, the burial flag, and the headstone or marker are available to all eligible veterans. This chapter covers VA Form 21P-530EZ for burial benefits, the DIC application process, the Aid and Attendance benefit for surviving spouses, and the specific documentation the VA requires --- including the DD Form 214 that many families cannot locate and the process for requesting it from the National Personnel Records Center.

Chapter 9: California Victim Compensation Board

If the death resulted from a crime --- including vehicular manslaughter, homicide, or domestic violence --- the California Victim Compensation Board (CalVCB) provides funeral and burial reimbursement, mental health counseling for survivors, income loss replacement, and relocation assistance. Most families do not know this program exists. It covers funeral costs up to the statutory maximum, provides ongoing support services, and does not require a criminal conviction --- only a police report and a reasonable belief that a qualifying crime occurred. This chapter covers the application process, the documentation requirements, the timeline for reimbursement, and how CalVCB coordinates with other benefit programs.

Chapter 10: Indigent Burial and Emergency Assistance

When there is no money for a funeral and no life insurance, California counties are required to provide for the disposition of remains. Each county has its own program with different procedures, different contact points, and different levels of service. This chapter also covers FEMA funeral assistance for deaths related to federally declared disasters, charitable burial funds, and the specific county programs in Los Angeles, San Francisco, San Diego, Sacramento, and other major California counties. It explains who qualifies, what the county provides, what the family is expected to contribute, and how to apply before the funeral home begins charging storage fees.

Chapter 11: The Document Vault --- What to Gather in Week One

Every agency, every insurer, and every pension system is going to ask for the same core documents --- and several will ask for documents you did not know existed. This chapter provides the complete document gathering list organized by category: identification documents, financial records, insurance policies, property records, military service records, employment records, and government benefit statements. It tells you where to find documents the deceased may not have kept at home --- including the process for requesting records from the California Secretary of State, the county recorder, the National Personnel Records Center, and the Social Security Administration. Gathering everything in week one prevents the delays that add weeks to every subsequent application.

Chapter 12: The Master Forms Reference

Every form number, every agency, and exactly where to get each one. Social Security Form SSA-10 and the online application at ssa.gov. CalPERS Form 1932 and the member services portal. CalSTRS survivor benefit application and the regional office contacts. VA Form 21P-530EZ and the eBenefits portal. Workers' compensation DWC-1 claim form. BOE-19-P for Proposition 19. CalVCB application. DHCS 9060 Medi-Cal notification. Covered California special enrollment application. DE-221 Spousal Property Petition. The Small Estate Affidavit (no official form --- you draft it yourself under Probate Code 13100-13106). Each entry includes the form number, the agency that processes it, the filing method (online, mail, in-person), and the typical processing time.

Chapter 13: The Master Timeline

Every deadline from Day 1 through Month 24+ on one sequential calendar. The health insurance 60-day special enrollment window. The 90-day Medi-Cal estate recovery notification. The one-year Proposition 19 filing deadline. The 240-week workers' compensation statute of limitations. The Social Security application window. The CalPERS and CalSTRS processing timelines. The VA burial benefit application deadline. Each deadline includes the statutory citation, the consequence of missing it, and whether any extensions or hardship exceptions exist. Print this chapter, mark the actual dates for your situation, and pin it where you can see it every day.

Chapter 14: When to Hire a Professional

The decision tree for when you need a lawyer, a financial planner, or a benefits counselor --- and when you are wasting money hiring one. Straightforward survivor benefit claims with clear documentation do not require an attorney. Disputed pension elections, contested workers' compensation claims, complex VA appeals, and cases where SSA has not correctly applied the Government Pension Offset / Windfall Elimination Provision repeal to your benefit do. This chapter provides the questions to ask before retaining anyone, the fee structures you should expect, and the red flags that indicate a professional is creating complexity to justify their fees rather than resolving your situation.

Chapter 15: Agency Contact Directory

Every agency referenced in the guide with current phone numbers, websites, mailing addresses, and office hours. Social Security Administration (national and California field offices). CalPERS member services. CalSTRS regional offices. County pension systems (LACERA, SDCERA, UCRP, and others). The Workers' Compensation Appeals Board (district offices). Department of Veterans Affairs (regional office and national hotline). California Victim Compensation Board. Department of Health Care Services. Covered California. County social services offices for indigent burial programs. Each entry includes the best time to call, the average hold time, and whether online submission is available.

Who This Guide Is For

- The surviving spouse whose partner was a CalPERS or CalSTRS retiree --- the 47-page packet arrived, you have three survivorship options, the election is irrevocable, and the representative said they "cannot provide financial advice." You need to understand the difference between Option 1 (unmodified allowance), Option 2 (100% continuance), and the modified options --- and what the repeal of the Government Pension Offset changes about your Social Security — a CalPERS or CalSTRS pension no longer reduces it — before you sign anything you cannot undo.

- The adult child trying to claim benefits for a surviving parent who cannot navigate the bureaucracy --- your mother lost her husband, she is 73, she has never handled the finances, and she does not know what CalPERS is, what the $255 Social Security payment is, or that she has 60 days to enroll in a new health insurance plan. You need the complete list of everything she is entitled to and the order in which to file.

- The registered domestic partner who just learned that federal benefits do not apply --- California recognizes your partnership for every state purpose. The federal government does not. You are not eligible for Social Security survivor benefits, the $255 lump-sum payment, or Medicare based on your partner's work record. This guide identifies which state and local benefits partially compensate for the federal gap and what financial planning steps to take immediately.

- The family of a worker who died from a job-related injury or occupational illness --- the employer's workers' compensation insurer is not volunteering that you are entitled to $250,000 to $320,000 in death benefits plus $10,000 for burial. The 240-week statute of limitations sounds generous until you realize that delayed filing means delayed payments, and the insurer has every incentive to wait you out. This guide walks you through the claim from filing to payment.

- The surviving spouse about to lose health insurance --- COBRA continuation costs $3,400 per month. Covered California might cost $200 to $400 per month with subsidies. The 60-day enrollment window started the day your spouse died. You need to know the numbers, the enrollment process, and the Medi-Cal income thresholds before the window closes.

- The family inheriting a home who does not understand Proposition 19 --- the county assessor is about to reassess the property to current market value, quadrupling the taxes permanently. The BOE-19-P form exists. The one-year deadline exists. The $1,044,586 exclusion cap exists. But none of these facts are explained on the assessor's notice. This guide covers the complete filing sequence.

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across 20+ government websites, each covering their own slice, none referencing each other. Here is what actually happens when California families try to claim survivor benefits using free resources alone:

- Social Security's website covers Social Security. It does not mention CalPERS, CalSTRS, workers' compensation, Proposition 19, or Covered California. You can apply for the $255 lump-sum payment and monthly survivor benefits online. What SSA does not tell you is that the Government Pension Offset — the rule that used to gut Social Security survivor benefits for CalPERS and CalSTRS families — was repealed for benefits payable January 2024 onward, so you may be owed a higher monthly benefit plus retroactive back pay, or be eligible for a benefit someone once told you not to bother claiming. Nobody phones to tell you that, and nobody phones before you make your irrevocable CalPERS survivorship election either.

- CalPERS and CalSTRS send detailed packets but refuse to advise you on which option to choose. The representative will explain the math. They will not tell you which option is better for your situation, or how the choice interacts with your Social Security benefits now that the repeal of the Government Pension Offset lets you keep both the pension and your full survivor benefit. They are prohibited from giving financial advice. You are expected to make an irrevocable decision that determines your income for the rest of your life based on a 47-page packet and a phone call.

- The California Department of Industrial Relations website explains workers' compensation death benefits but does not connect them to the other benefits you are entitled to. The $250,000 to $320,000 death benefit and $10,000 burial allowance exist on the DIR website. What the website does not tell you is how workers' comp death benefits interact with Social Security survivor benefits, whether accepting one affects the other, or that the statute of limitations is 240 weeks --- long enough that many families forget to file.

- County assessor websites explain Proposition 19 reassessment but not the exemption filing sequence. The notice says the property will be reassessed. It does not explain the BOE-19-P form, the one-year deadline, the move-in requirement, the $1,044,586 indexed cap, or the homeowners' exemption that must be filed separately. Families who read only the notice assume reassessment is inevitable.

- Attorney and financial planner blogs explain how complex these decisions are --- because they charge hourly rates to help you make them. California probate attorneys charge $375 to $422 per hour. Financial planners charge $200 to $400 per hour for benefits analysis. Their blog posts are accurate and detailed. They are also designed to convince you that navigating survivor benefits alone is dangerous. For contested claims and complex pension elections, professional help is essential. For a surviving spouse who needs to claim Social Security, elect a CalPERS survivorship option, enroll in Covered California, and file a BOE-19-P, the process is sequential, documented, and achievable without paying hourly rates.

Free resources give you one agency at a time, in isolation, with no sequencing and no cross-referencing. The California Survivor Benefits Navigator gives you every benefit, every form, every deadline, and every agency interaction in one chronological system --- so you claim everything you are entitled to, in the order that protects the deadlines, without missing the benefits that nobody volunteers to tell you about.

--- Less Than Four Minutes With a California Probate Attorney

A single consultation with a California probate attorney costs $375 to $422 per hour. A financial planner's benefits analysis runs $200 to $400 per hour. A benefits counselor who specializes in survivor claims charges $150 to $250 per session. Workers' compensation attorneys take 15% of the death benefit award. This guide costs less than four minutes of professional legal time and gives you the complete California-specific benefits roadmap --- every agency, every form, every deadline, every pension survivorship option, and the decision framework that tells you whether you need a professional at all or whether you are paying someone to fill out forms you can handle yourself.

Your download includes 8 PDFs --- the complete 15-chapter guide, the California Survivor Benefits Checklist (20 actionable items organized by deadline), plus 6 standalone printable tools: the Master Timeline Calendar (every deadline on one page with a write-in column for your actual dates), the Document Vault Checklist (every document you need to gather in week one), the Health Insurance Decision Framework (Cal-COBRA vs. Covered California vs. Medi-Cal side-by-side), the Probate Bypass Decision Tree (which transfer mechanism applies to your situation), the Forms Reference Card (every form number and agency on one page), and the Agency Contact Directory (phone numbers, websites, and hours for every agency). Print what you need, keep the rest on your computer. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on which benefits you are entitled to and confidence that you are claiming them in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free California --- Survivor Benefits Checklist --- covering the 20 most critical actions organized by deadline, from ordering death certificates and halting benefit payments in the first week through the one-year Proposition 19 filing. It is enough to make sure you do not miss anything in the first 60 days.

You did not ask to become the person who navigates this. But the pension packet is on the table. The health insurance clock is ticking. The benefits exist --- Social Security, CalPERS, workers' comp, property tax protection, VA benefits, victim compensation --- and every one of them requires a separate application to a separate agency with a separate deadline. This guide puts all of it into one sequence so you can stop searching twenty different government websites and start claiming what your family is owed.

This guide provides educational information about California survivor benefits and claims procedures. It is not legal, financial, or tax advice and does not create an attorney-client or fiduciary relationship. For contested pension elections, complex workers' compensation claims, VA appeals, or a benefit SSA has not correctly recalculated under the Government Pension Offset / Windfall Elimination Provision repeal, consult a licensed California attorney or certified financial planner. The guide includes a chapter on when professional help is necessary and how to evaluate whether the fees you are quoted are justified.