Connecticut Owes You Nothing — Not Even an Explanation of the Paperwork It Demands

Your loved one's estate owes zero estate tax. The exemption is $15 million. You assumed that meant no paperwork. Then the Probate Court informed you that Connecticut requires Form CT-706 NT — a full estate tax return — even when no tax is owed. Without it, the state places an automatic lien on every piece of real property the deceased owned. No lien release, no home sale. No home sale, no distribution. And the Probate Court will not help you fill out the form. Families report having it sent back "several times" with highlighted fields and no explanation of what went wrong.

Meanwhile, the probate fee invoice arrives — calculated not just on probate assets, but on the living trust, the joint bank accounts, and the life insurance proceeds. Assets your family specifically structured to avoid probate. Connecticut charges probate fees on all of them. The fee scales up to $40,000 depending on the gross estate value, and if you miss the six-month filing deadline, interest accrues at 0.5% per month.

Free resources make this worse, not better. The DRS website provides the blank CT-706 NT form with dense instructions written for tax attorneys. CTLawHelp covers small estates but says nothing about the inchoate lien or the probate fee calculation for mid-size estates. Attorney blogs explain the problem in just enough detail to justify an $8,000 retainer. Reddit threads cite laws from other states. No single source connects the CT-706 NT to the lien release to the probate fee calculation to the income tax returns — because these responsibilities are split across three separate agencies that do not coordinate with each other.

The Connecticut Tax Sequencer — One Guide Through Three Agencies

The Connecticut Final Tax & Estate Tax Guide takes the scattered requirements of the Probate Court, the Department of Revenue Services, and the local Town Clerk and organizes them into one chronological action plan. It translates legalese into plain English and tells you exactly which forms to file, to which office, in what order, with which documents attached.

What You Get

The Complete Tax & Estate Tax Guide

A comprehensive guide covering every tax obligation after a death in Connecticut — organized by timeline, not by agency. Written for executors and families, not CPAs.

- CT-706 NT Field-by-Field Decoder — The form the Probate Court requires but refuses to help you complete. Every line explained in plain English: which assets to include, which qualify for the spousal exclusion, and exactly how to calculate the gross estate value that determines your probate fee. Stop getting your filing rejected and resubmitted.

- The Inchoate Lien Clearance Sequence — Connecticut places an automatic, unrecorded lien on every deceased resident's real property. Buyers' attorneys flag it during the title search and the closing stops dead. The guide walks you through the exact steps to obtain the Certificate Releasing the Connecticut Estate Tax Lien and record it with the Town Clerk so the sale can proceed.

- Probate Fee Demystifier — Connecticut's probate fee functions as a hidden tax on the gross estate, scaling by tier up to $40,000. The guide explains the complete fee schedule, the 50% spousal reduction, and exactly which non-probate assets are included in the calculation — so you know what the court will charge before the invoice arrives and can verify their math.

- Final Income Tax Return (CT-1040) Walkthrough — The decedent's last individual state income tax return, with specific guidance on filing as a surviving spouse, handling the tax year split, claiming refunds using federal Form 1310, and the deadline that catches executors off guard.

- Fiduciary Income Tax Return (CT-1041) Guide — If the estate earns any income after the date of death — interest, dividends, rental income — a separate fiduciary return is required. The guide explains when the CT-1041 is triggered, how to obtain the Estate EIN, and the critical difference between estate income and the decedent's final individual income.

- Step-Up in Basis Calculator — Selling inherited property? Your cost basis resets to fair market value at the date of death, which usually eliminates most capital gains. The guide explains how to establish and document the stepped-up basis before listing the home.

- CPA Handoff Organizer — If you hire a CPA, this section tells you exactly which documents, schedules, and basis calculations to organize before your first meeting. Walk in prepared instead of handing over a shoebox of receipts at $350 an hour.

- Taxable Estate Escalation Path — For the rare estate exceeding the $15 million exemption, the guide covers Form CT-706/709, the 12% flat tax rate, the DRS filing process, and when to hire specialized counsel.

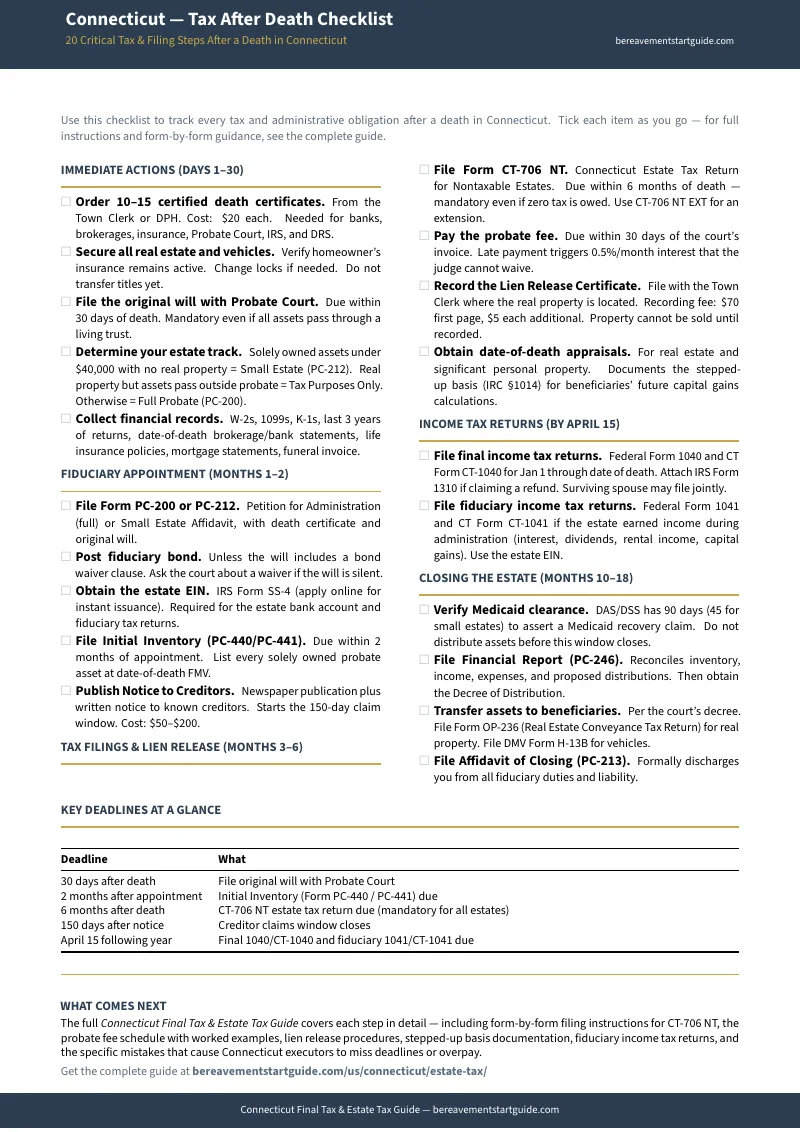

The Tax After Death Checklist

A printable checklist covering every tax-related action from the first week through the final filings. Organized by deadline — the six-month CT-706 NT, the April 15 income tax returns, and the probate fee payment window — so nothing falls through the cracks.

Printable Standalone Tools

Separate PDF worksheets you can print and bring to meetings with banks, CPAs, and the Probate Court:

- Gross Estate Calculation Worksheet — Fill-in tables for every asset category that Connecticut includes in the gross estate: solely owned property, joint accounts, life insurance, retirement accounts, and trust assets. Use this to prepare the CT-706 NT and estimate your probate fee.

- Tax Deadline Calendar — Every critical tax deadline mapped to a single timeline: the 6-month CT-706 NT, the extension filing window, the April 15 income tax returns, and the probate fee payment due date with interest calculations.

- Forms Reference Card — One-page quick reference mapping every Connecticut tax form to where it goes and when you need it: CT-706 NT for non-taxable estates, CT-706/709 for taxable estates, CT-1040, CT-1041, and the federal forms that connect to each.

Who This Is For

- Executors and administrators who need to file the CT-706 NT but cannot decipher the Probate Court's instructions — and cannot afford to have it rejected again

- Families trying to sell an inherited home who discovered the automatic state lien during the title search and need to clear it before the buyer walks away

- Surviving spouses who need to understand the CT-1040 joint filing rules, the spousal probate fee reduction, and the step-up in basis on the family home

- Executors managing impatient beneficiaries who demand immediate distributions — this guide explains the tax clearance requirements that legally prevent early payouts and gives you the documentation to prove it

- Anyone preparing documents for a CPA who wants to minimize billable hours by walking in with organized schedules instead of a stack of unsorted paperwork

Why Not Free Resources?

The Connecticut DRS and Probate Court websites provide every form you need. They do not provide the one thing you actually need — a coherent explanation of how to use them:

- The Probate Court provides the CT-706 NT form but explicitly refuses to help you fill it out — families report filings rejected repeatedly with no useful feedback on what to fix

- The DRS publishes CT-1040 and CT-1041 instructions written for tax professionals using IRC code references that assume you already know what you are doing

- AARP mentions the $15 million exemption in a single paragraph and says nothing about the mandatory CT-706 NT filing, the inchoate lien, or the probate fee

- SmartAsset and Nolo rank for "Connecticut estate tax" but provide generic overviews designed to capture leads for expensive advisor referrals, not to guide you through the actual forms

- No single free source connects all three agencies — Probate Court, DRS, and Town Clerk — into one sequential workflow

— Less Than One Hour of a CPA's Time

A Connecticut estate CPA charges $350 or more per hour. A local estate attorney charges $400 or more. This guide costs less than fifteen minutes of professional time — and it can replace dozens of hours of confused research across scattered government websites.

For straightforward estates, this guide can eliminate the need for a tax professional entirely. For complex estates, organizing your paperwork with this guide before your first CPA meeting can save hundreds in billable hours — because you walk in with completed schedules instead of questions.

60-day, no-questions-asked refund guarantee. If this guide does not save you at least 10 hours of frustrating tax research, email us for a full refund. You keep the guide.