Delaware Repealed Its Estate Tax. Then It Buried the Paperwork in Three Different Counties.

Your loved one died in Delaware. Someone told you there is no state estate tax, which is true. You assumed that meant the tax side was simple. Then the Register of Wills told you to file an "Affidavit of No Delaware Estate Tax" before you could sell the house. A sworn form to prove a tax does not exist. Without it, the title company refuses to close. No affidavit, no sale. No sale, no distribution.

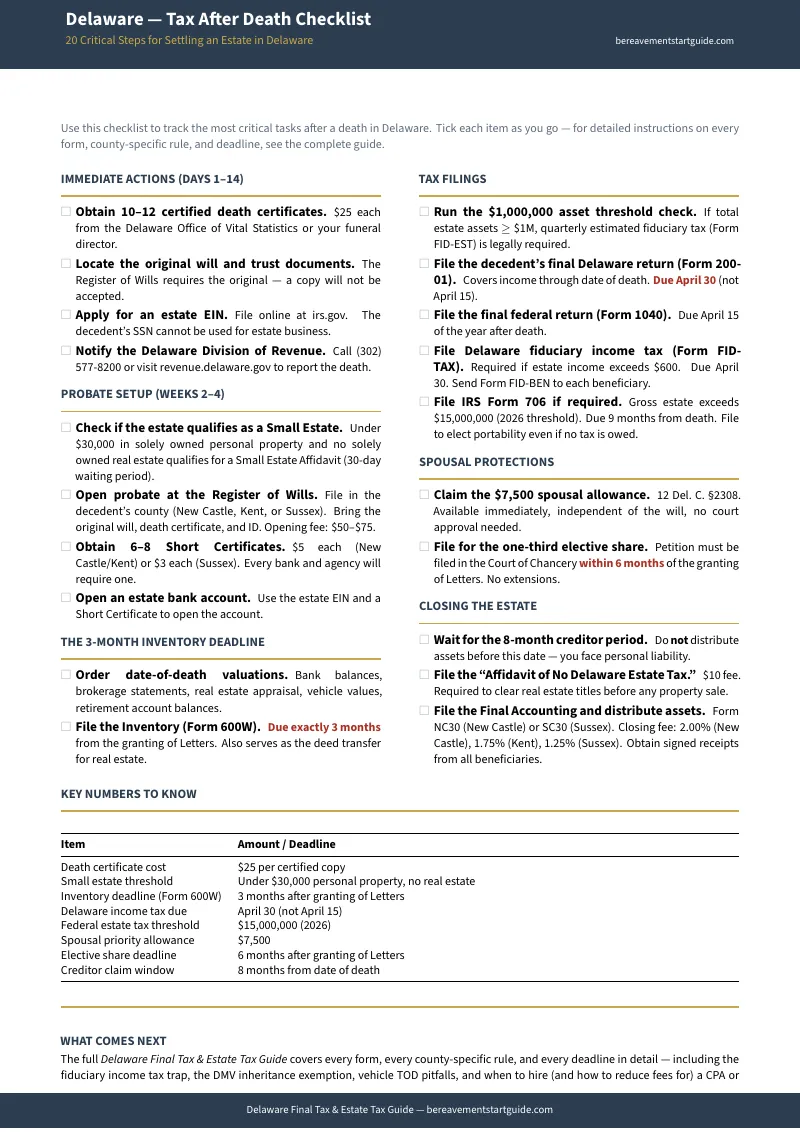

Meanwhile, Delaware's unique April 30 income tax deadline is approaching and you did not know it was different from the federal April 15 deadline. The Division of Revenue charges 5% per month for late filing, up to 50%. You called them. They told you to file Form 200-01 but could not explain how to report a deceased taxpayer's income. You called the Register of Wills. They told you the estate inventory is due in exactly three months and that it doubles as the legal deed transfer for real property. They also mentioned the closing fee, which ranges from 1.25% in Sussex County to 2.00% in New Castle County. You had no idea probate fees varied by county.

So you searched online. The Division of Revenue website offers downloadable PDFs of Form FID-TAX and Form 200-01 with instructions written for CPAs. Reddit threads confuse the State of Delaware with Delaware County, Pennsylvania. Attorney blogs explain just enough to justify a $300/hour consultation. No single source connects the Division of Revenue's tax filings to the Register of Wills' probate requirements to the county-specific forms and fees. These three systems do not coordinate, and nobody has built you a bridge between them.

The Delaware Tax Bridge -- One Guide Across Three Systems

The Delaware Final Tax & Estate Tax Guide takes the scattered demands of the Division of Revenue, the Register of Wills, and the county-specific forms and organizes them into one chronological action plan. It translates the statutory language into plain English and tells you which forms to file, to which office, in what order, by when, and what to bring.

What You Get

The Complete Tax & Estate Tax Guide

A comprehensive guide covering every tax obligation after a death in Delaware -- organized by timeline, not by agency. Written for executors and families, not CPAs.

- April 30 Final Income Tax Walkthrough -- Delaware's filing deadline is two weeks later than the federal deadline, and most executors do not discover this until it is too late. The guide walks you through the decedent's final Form 200-01, how to report income through the date of death, how to file as a surviving spouse, and how to use Form PIT-CFR to claim a refund on behalf of the estate.

- The $1,000,000 Fiduciary Tax Trap -- If total estate assets equal or exceed $1,000,000, Delaware requires quarterly estimated fiduciary tax payments on Form FID-EST. A house worth $300,000, a 401(k) worth $250,000, a life insurance policy worth $250,000, and modest savings easily breach this threshold. The guide includes a diagnostic worksheet so you know in five minutes whether you are legally required to file quarterly -- and what happens if you miss it.

- "No Estate Tax" Affidavit Procedure -- The paradox that catches every executor: filing a sworn affidavit to prove a repealed tax does not apply, so the title company will clear the property. The guide covers the $10 filing, which county office to use, and the exact timing relative to the home sale.

- County-by-County Fee and Form Reference -- New Castle, Kent, and Sussex counties charge different closing fees (2.00%, 1.75%, and 1.25% respectively), use different accounting forms, and have different rules about whether pro se executors can use the Affidavit in Lieu of Receipts. The guide breaks down every material difference so you know exactly what your county requires.

- Step-Up in Basis Explainer -- How the federal step-up resets the cost basis of inherited property to its date-of-death fair market value, potentially eliminating tens or hundreds of thousands of dollars in capital gains. The guide explains how to document the stepped-up basis and why the valuations on the Inventory must match.

- CPA Handoff Organizer -- If you hire a CPA, this section tells you exactly which documents, schedules, and basis calculations to organize before your first meeting. Walk in prepared instead of paying $300/hour for them to sort your paperwork.

- Vehicle Transfer and DMV Exemptions -- The 4.25% document fee exemption for inherited vehicles, the 30-day transfer window, and the Transfer-on-Death title trap that catches families who filed TOD paperwork but never had it printed on the title.

- Spousal Protections Reference -- The $7,500 immediate spousal allowance, the one-third elective share with its strict six-month Court of Chancery deadline, and the mock Form 706 requirement that surprises even attorneys.

The Tax After Death Checklist

A printable checklist covering every tax-related action from the first week through estate closing. Organized by deadline -- the 3-month inventory, the April 30 income tax deadline, the 8-month creditor period, and the closing fee payment -- so nothing falls through the cracks.

Printable Standalone Tools

Separate PDF worksheets you can print and bring to meetings with banks, CPAs, and the Register of Wills:

- $1,000,000 Threshold Diagnostic Worksheet -- Fill-in tables for every asset category to determine immediately whether you need to file quarterly estimated fiduciary taxes. Most executors do not realize a perfectly ordinary middle-class estate can breach this threshold.

- Master Timeline and Deadline Tracker -- Every critical deadline on one page: the 3-month inventory, the 6-month elective share petition, the 8-month creditor period, the April 30 income tax returns, the 9-month federal estate tax return, and the quarterly FID-EST payments.

- Forms Quick Reference Card -- One-page reference mapping every Delaware form to where it goes and when it is due: Form 200-01, Form FID-TAX, Form FID-EST, Form FID-BEN, Form 600W, the No Estate Tax Affidavit, and the federal forms that connect to each.

Who This Is For

- Executors and administrators who need to file Delaware tax returns and the probate inventory but cannot get straight answers from the Division of Revenue or the Register of Wills about how the two systems connect

- Families trying to sell an inherited home who discovered the "No Estate Tax" affidavit requirement during the title search and need to clear it before the buyer walks away

- Surviving spouses who need to understand the April 30 filing deadline, the spousal allowance, the elective share deadline, and the step-up in basis on the family home

- Executors managing impatient beneficiaries who demand immediate distributions -- this guide explains the 8-month creditor waiting period and the tax clearance requirements that legally prevent early payouts, and gives you the documentation to prove it

- Anyone preparing documents for a CPA who wants to minimize billable hours by walking in with organized schedules instead of a stack of unsorted paperwork

Why Not Free Resources?

The Division of Revenue and the Register of Wills provide every form you need. They do not provide the one thing you actually need -- a coherent explanation of how to use them together:

- The Division of Revenue publishes Form 200-01 and Form FID-TAX instructions written for tax professionals who already know the Delaware code -- they assume you understand the difference between a decedent's final return and a fiduciary return

- The Register of Wills in each county provides its own forms but cannot offer legal or tax advice about how the inventory connects to the tax returns or the closing fee calculation

- SmartAsset and Nolo rank for "Delaware estate tax" by confirming the tax was repealed in a single paragraph -- they say nothing about the No Estate Tax Affidavit, the county closing fees, or the $1,000,000 fiduciary threshold

- Reddit threads routinely confuse the State of Delaware with Delaware County, Pennsylvania, leading executors to follow the wrong state's rules

- No single free source connects all three systems -- Division of Revenue, Register of Wills, and county-specific procedures -- into one sequential workflow

-- Less Than One Hour With a Delaware CPA

A Delaware estate CPA charges $300 or more per hour. A local estate attorney charges $350 or more. This guide costs less than fifteen minutes of professional time -- and it can replace dozens of hours of confused research across scattered government websites.

For straightforward estates, this guide can eliminate the need for a tax professional entirely. For complex estates, organizing your paperwork with this guide before your first CPA meeting can save hundreds in billable hours -- because you walk in with completed worksheets instead of questions.

60-day, no-questions-asked refund guarantee. If this guide does not save you at least 10 hours of frustrating tax research, email us for a full refund. You keep the guide.