Florida Has No State Income Tax. The Estate Still Owes Taxes. And the Property Tax Bill on the House Just Tripled.

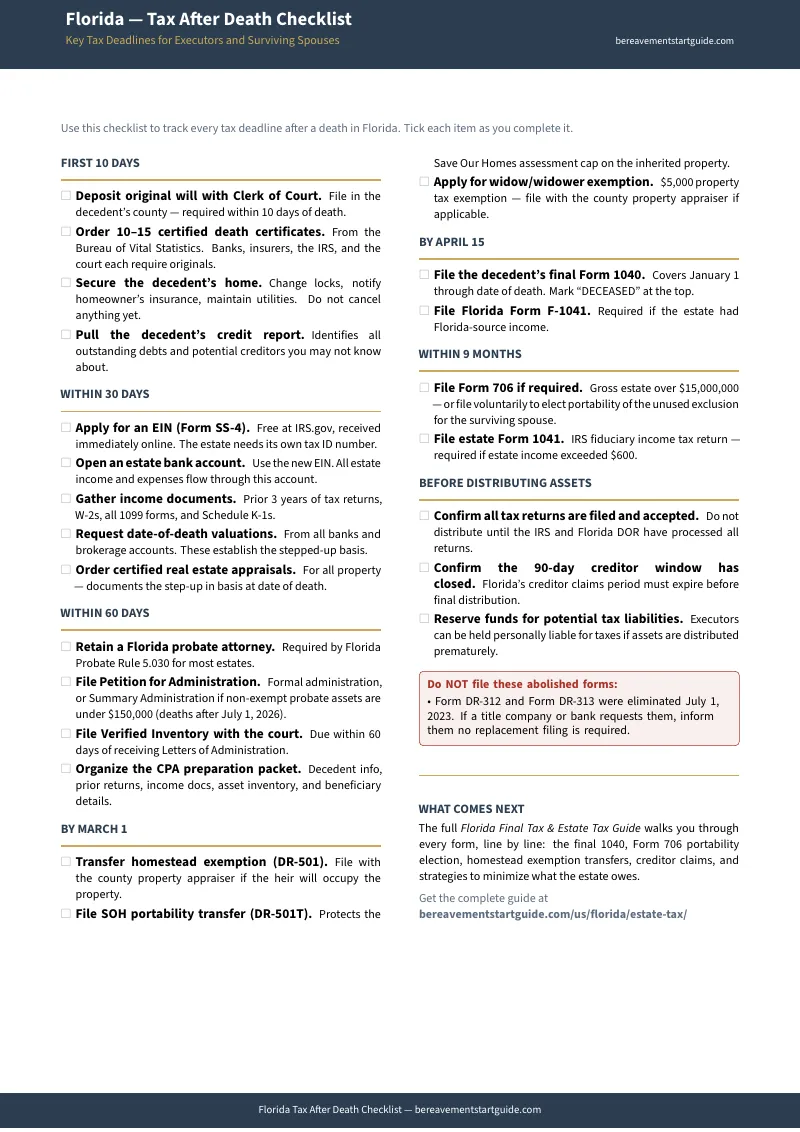

Someone you love just died in Florida. You went to the bank to close the account, and the teller said they need an EIN for the estate before they can release anything. You did not know the estate needed its own tax ID. You went home and searched "Florida taxes after death" and the first result said Florida has no state income tax. The second result said the estate might need to file a Florida fiduciary return on Form F-1041. The third result told you to file a "No Tax Due" affidavit with the Department of Revenue — a form that was abolished in 2023 and no longer exists.

Meanwhile, a title company is asking for proof that no Florida estate tax is owed before they will clear the deed. The county property appraiser's office just sent a notice that the "Save Our Homes" assessment cap has been removed from the house. The property taxes are about to jump from $2,800 to $8,400 per year — permanently — unless someone files Form DR-501T by March 1. You did not know this form existed until right now. And three family members are calling to ask when they get their inheritance, while you are quietly terrified that distributing anything before taxes are settled could make you personally liable.

Here is the truth: Florida is one of the most tax-friendly states for estates. There is no state income tax, no state estate tax, and no state inheritance tax. The federal estate tax exemption is $15 million under the One Big Beautiful Bill Act. Fewer than 0.1% of estates will owe federal estate tax. But "tax-friendly" does not mean "no tax obligations." The final income tax return must be filed. The estate may need its own tax returns. Capital gains must be documented correctly to preserve the step-up in basis. And the property tax trap — the one nobody warns you about — can cost the family thousands of dollars per year for as long as they own the house.

The Florida Final Tax & Estate Tax Guide is the Tax Compliance Roadmap — the structured, chronological system that tells you exactly which tax obligations apply to your estate, in what order to handle them, and which outdated advice to ignore. It does not replace your CPA. It makes sure you walk into that CPA's office with every document organized, every form identified, and every deadline marked — so you stop paying for education at $300 to $500 an hour and start paying only for execution.

What Is Inside the Tax Compliance Roadmap

A 17-chapter guide, the Tax After Death Checklist, and standalone reference sheets — covering every tax obligation from the first 10 days after death through final distribution, built specifically for Florida statutes, IRS requirements, and the county-level property tax rules that make Florida different from every other state:

Florida's Tax Landscape: What You Actually Owe (and What You Do Not)

Florida has no state income tax, no state estate tax, and no state inheritance tax. But the estate still has obligations. The guide maps every federal and Florida-specific filing requirement: the final Form 1040, the fiduciary Form 1041 if the estate earns more than $600 during administration, Florida Form F-1041 if the estate has Florida-source income, and the portability election on Form 706 that can shield up to $30 million for married couples. It also tells you what was eliminated — Form DR-312 and Form DR-313, the "No Tax Due" affidavits that Florida abolished in July 2023 — so you stop searching for ghost forms that every outdated blog still tells you to file.

The Save Our Homes Trap: The Tax Bill Nobody Warns You About

This is where Florida executors lose the most money without realizing it. The "Save Our Homes" constitutional amendment caps annual property tax increases at 3% or CPI, whichever is less. Over 20 years, this creates a massive gap between the assessed value and market value. When the owner dies, the cap resets. If the property was assessed at $180,000 but the market value is $520,000, the new assessment jumps to full market value — and the property tax bill jumps with it. The March 1 deadline to file Form DR-501T with the county property appraiser is the only way to transfer the cap to a qualifying heir. Miss it, and the reassessment is permanent. This chapter walks you through every step: who qualifies, what to file, and how to avoid the mistake that costs families thousands per year with no remedy.

The Step-Up in Basis: Erasing Capital Gains on Inherited Property

The decedent bought the house for $85,000 in 1992. It is worth $475,000 today. If the decedent had sold it while alive, the capital gains tax on $390,000 of appreciation would have been substantial. But under IRC Section 1014, inherited property receives a "step-up" to fair market value at the date of death. The $390,000 in appreciation is legally erased. If the heir sells for $475,000, the capital gain is zero. But this benefit only holds if you document it correctly — a certified date-of-death appraisal, not a Zillow estimate. The guide tells you exactly how to secure the appraisal, what the IRS requires, and how to hand the documentation to your CPA so it survives an audit.

Filing the Final Income Tax Return (Form 1040)

The decedent's final individual income tax return covers January 1 through the date of death. You are the one responsible for filing it. The guide walks you through gathering the missing 1099s and W-2s, handling income that arrived after the date of death (it belongs to the estate, not the final 1040), the strategic choice of deducting final medical expenses on the 1040 versus Form 706, and filing as "Married Filing Jointly" for the year of death if the surviving spouse has not remarried.

The Fiduciary Income Tax Return (Form 1041) and the EIN

If the estate earns more than $600 during administration — from rental income, dividends, or interest on retained cash — you must file IRS Form 1041 and issue Schedule K-1s to beneficiaries. That requires an EIN first. The guide covers the free online EIN application through IRS Form SS-4, the strategic choice of a fiscal year (estates get this option — individuals do not), and the filing mechanics that CPAs charge hundreds of dollars to explain.

Documentary Stamp Tax: The Surprise Tax on Inherited Real Estate

Transferring unencumbered property to a beneficiary does not trigger documentary stamp tax. But if the property carries a mortgage, the tax hits at $0.70 per $100 of the outstanding mortgage balance — $0.60 plus a $0.45 surtax in Miami-Dade County. On a $280,000 mortgage, that is nearly $2,000 in tax that nobody warned you about. The Florida Department of Revenue actively audits these transfers. The guide covers the exemption for personal representative deeds, the rate calculations by county, and the rule that can save the estate hundreds or thousands on real estate transfers.

County-by-County Filing Guide

Filing fees vary by county and by probate track. Formal Administration costs $401 in Miami-Dade, Broward, and Palm Beach, and $400 in Orange, Hillsborough, and Pinellas. But the real differences are procedural: Broward County requires auto-populating "Smart Forms" and rejects standard state templates. Orange County mandates Word-format orders emailed directly to chambers. Collier County requires physical, in-person will deposit at the Naples courthouse. Sarasota uses Probate Coordinators who pre-audit every filing. The guide covers the top 10 Florida counties with filing fees, mandatory checklists, and local procedural requirements.

Working With Professionals: The Smart Handoff

The guide does not replace your CPA or attorney. It eliminates the billable hours you spend educating them about your situation. Chapter 15 includes a structured CPA preparation packet — a pre-organized dossier of every document, form, and calculation your CPA needs — so they can start preparing returns immediately instead of spending two hours at $400 per hour sorting through a shoebox of papers. The guide also covers statutory attorney fee schedules and the flat-fee negotiation framework that can save the estate thousands in percentage-based legal fees.

Who This Guide Is For

- The executor who just learned the estate needs its own tax ID — the bank froze the accounts, the CPA wants an EIN, and you have no idea whether the estate needs a Form 1041 or how to get one. The guide gives you the step-by-step process, from the free online SS-4 application to the fiscal year election that can defer tax liabilities.

- The surviving spouse whose property taxes just tripled — the Save Our Homes cap reset when your spouse died, and nobody told you about Form DR-501T until the tax bill arrived. If the March 1 deadline has not passed, this guide tells you exactly what to file and where. If it has, the guide tells you that too — plainly and honestly.

- The adult child about to sell an inherited house — your parents bought the house for $100,000 and it is worth $500,000 today. You need to know whether you owe capital gains tax on $400,000 of appreciation. The answer depends entirely on whether the step-up in basis was documented correctly. The guide walks you through the appraisal requirement and the IRS documentation.

- The executor facing pressure to distribute immediately — beneficiaries want their inheritance now. You know that distributing before taxes are settled could make you personally liable. The guide gives you the statutory authority to withhold distributions until all returns are filed and accepted, and the language to explain that to impatient family members.

- The family trying to figure out what Florida actually requires — every search result contradicts the next one. One says to file DR-312. Another says the estate needs a Florida income tax return even though Florida has no income tax. A third says the federal exemption dropped to $7 million. The guide cuts through the noise and tells you exactly what is current for 2026.

- The out-of-state executor managing a Florida estate remotely — you live in another state and the decedent died in Florida. You need to coordinate with a local CPA and attorney without paying for basic orientation. The guide gives you county-specific filing fees, local procedural requirements, and every form reference so you arrive at that first consultation as an informed client.

Why Free Resources Will Not Get You Through This

The IRS forms exist for free. The Florida Department of Revenue website is publicly accessible. And yet:

- The DR-312 trap is everywhere. Florida eliminated the "Affidavit of No Florida Estate Tax Due" (Form DR-312) in July 2023. But as of 2026, most attorney blogs, checklist websites, and even some title companies still instruct executors to file it. You will waste days searching for a form that does not exist, and then more days explaining to a title company clerk that the form was abolished. The guide addresses this change on page one and tells you what to say when someone demands a form Florida no longer requires.

- National tax sites miss the Florida-specific traps. TurboTax, H&R Block, and Nolo cover federal filing requirements cleanly. They do not cover Form F-1041 (the Florida fiduciary return for estates with Florida-source income), the Save Our Homes property tax reset, the documentary stamp tax on mortgaged inherited property, or the county-specific filing requirements that vary across Florida's 67 counties. A generic "estate tax guide" written for all 50 states will not mention any of these.

- Attorney blogs create fear to justify retainer fees. Florida tax and estate planning attorneys produce detailed, technically accurate blog posts about capital gains, fiduciary returns, and property tax resets. Every article ends the same way: "This is complex — call our office for a consultation." For estates near the $15 million federal threshold, that advice is sound. For the vast majority of Florida estates — where the real work is filing a final 1040, getting an EIN, and protecting the property tax cap — the process is sequential and documented in statute. You need a roadmap, not a retainer.

- Government websites cover their own slice and refuse to connect the dots. The IRS explains Form 1041. The Florida Department of Revenue explains documentary stamp tax. The county property appraiser explains Save Our Homes. None of them tells you the order. None of them warns you that missing the property appraiser's March 1 deadline while you are focused on the April 15 income tax deadline creates a permanent, irreversible tax increase on the house.

Free resources give you forms, statutes, and warnings not to make mistakes. The Tax Compliance Roadmap gives you the complete Florida sequence — every filing, every deadline, every county-specific variation — in the order you actually need them, with the outdated advice stripped out and the hidden traps marked in advance.

— Less Than One Hour With a Florida CPA

A single meeting with a Florida CPA costs $300 to $500 per hour. Half that meeting will be spent explaining your situation and handing over disorganized documents. An estate planning attorney charges $250 to $400 per hour for consultations and thousands in statutory percentage fees for representation. This guide costs less than the time it takes a CPA to sort through your paperwork — and it makes sure you walk into that meeting with every document organized, every form identified, and every deadline on a calendar.

Your download includes the complete 17-chapter guide with county filing fee tables, the Florida Tax After Death Checklist, and standalone reference sheets — the CPA Preparation Packet template, the Save Our Homes Decision Tree, the Documentary Stamp Tax Calculator reference, the Step-Up in Basis Valuation Log, and the County Filing Fee and Attorney Fee Reference. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on exactly which tax obligations apply to your estate and confidence that you are handling them in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Florida — Tax After Death Checklist — covering the first 10 days of critical actions, the March 1 property tax deadline, the April 15 income tax deadline, and the abolished forms you do not need to file. It is enough to get through the first week and know what comes next.

You did not choose this job. But the IRS does not care, the county property appraiser does not care, and the bank will not release the money until someone gets it right. This guide puts every Florida tax obligation into one sequence so you stop searching, stop guessing, and start settling.