The Federal Estate Tax Exemption Is $15 Million. Hawaii's Is $5.49 Million. Nobody Told You About the Gap.

Your accountant said the estate is nowhere near the federal threshold. Your attorney mentioned something about Hawaii having its own rules but did not explain what that means in actual dollars. And now you are staring at the Department of Taxation website trying to figure out whether an estate worth seven or eight million dollars — an estate that owes the IRS nothing — somehow owes Hawaii a six-figure tax bill at the highest state estate tax rate in the country.

Meanwhile, the bank wants an EIN before it will release a dollar. The county wants you to report the death within 30 days or pay a $300 penalty. The final income tax return is due at 4.5 months. The estate tax return is due at 9 months. And you have beneficiaries calling every week asking when they will see their share while you are still trying to figure out which version of Form N-11 applies to a deceased Hawaii resident.

The Exclusion Gap Defense System

This guide exists because Hawaii's frozen $5.49 million estate tax exemption creates a trap that catches thousands of families every year. The federal exemption has climbed to $13.99 million in 2025 and $15 million in 2026 — and families assume that if they owe no federal estate tax, they owe no estate tax at all. They are wrong. Hawaii imposes a progressive estate tax starting at 10% and peaking at 20%, the highest top rate of any state in the nation. This guide walks you through every calculation, every form, and every deadline so you can determine your exposure, file correctly, and close the estate without leaving money on the table or triggering penalties you did not know existed.

The Complete Tax Timeline — Five Returns, One Sequence

An executor in Hawaii may need to file up to five separate tax returns: the deceased's final state income tax (Form N-11 or N-15), the federal final return (Form 1040), the Hawaii fiduciary income tax (Form N-40) if the estate earns more than $400 during administration, the federal estate tax (Form 706) if it exceeds the federal threshold, and the Hawaii estate tax (Form M-6) if it exceeds $5.49 million. Each return has its own deadline, its own threshold, and its own set of supporting forms. The guide sequences all five in chronological order so you know exactly which return to file when, and which ones you can skip entirely.

The County Property Tax Trap That Costs Families Thousands

When a homeowner dies in Hawaii, the existing property tax exemption — the $120,000 standard exemption or the $160,000 senior exemption in Honolulu County — is automatically voided. The county must be notified within 30 days of death. Miss that deadline, and the penalty is $200. Miss the September 30 re-filing deadline for the new occupant or trust beneficiary, and the property loses its exemption entirely for the next tax year — which can mean thousands of dollars in additional property taxes on a home the family still lives in. The guide covers the notification requirements, re-filing procedures, and exemption amounts for all four Hawaii counties.

Step-Up in Basis — The Calculation That Saves Heirs the Most Money

When you inherit property, the tax basis resets to fair market value at the date of death. This eliminates decades of capital gains in a single step. But Hawaii is not a community property state, which means a surviving spouse generally gets a step-up on only 50% of the property value — not the full 100% that spouses in community property states receive. The guide explains how joint tenancy, tenancy by the entirety, and trust ownership affect the step-up calculation, what documentation the executor needs to establish the new basis, and how to avoid the costly mistake of using the original purchase price when filing the eventual sale.

The HARPTA Withholding Trap for Nonresident Executors

If the deceased was a nonresident of Hawaii, or if a nonresident executor sells Hawaii real estate during estate administration, the state withholds 7.25% of the gross sale price under the Hawaii Real Property Tax Act — on top of the 15% federal FIRPTA withholding. On an $800,000 Honolulu condo, that is $58,000 withheld by HARPTA alone. The guide covers the withholding calculation, the Form N-288C refund process, and the exemption filing procedures so nonresident executors do not lose tens of thousands of dollars to a withholding requirement they did not know existed.

The M-6A Tax Release — The Form That Closes Probate

Hawaii probate cannot officially close until the executor files Form M-6A (Request for Release) with the Department of Taxation. This form proves that all estate taxes have been paid — or that none are owed. Without it, the circuit court will not accept your closing statement, and the estate stays open indefinitely. The guide explains the M-6A filing process, the documentation the Department of Taxation requires, and the timeline for receiving your release so you can close the estate and complete distributions.

What You Get — 10 Printable PDFs

- The Complete Hawaii Final Tax and Estate Tax Guide (55 pages) — 14 chapters covering the exclusion gap calculation, all five tax returns in chronological order, the step-up in basis rules for non-community property states, HARPTA withholding and refund procedures, real property transfers through both recording systems, county property tax exemption re-filing, and a complete forms directory with every DOTAX and circuit court form number

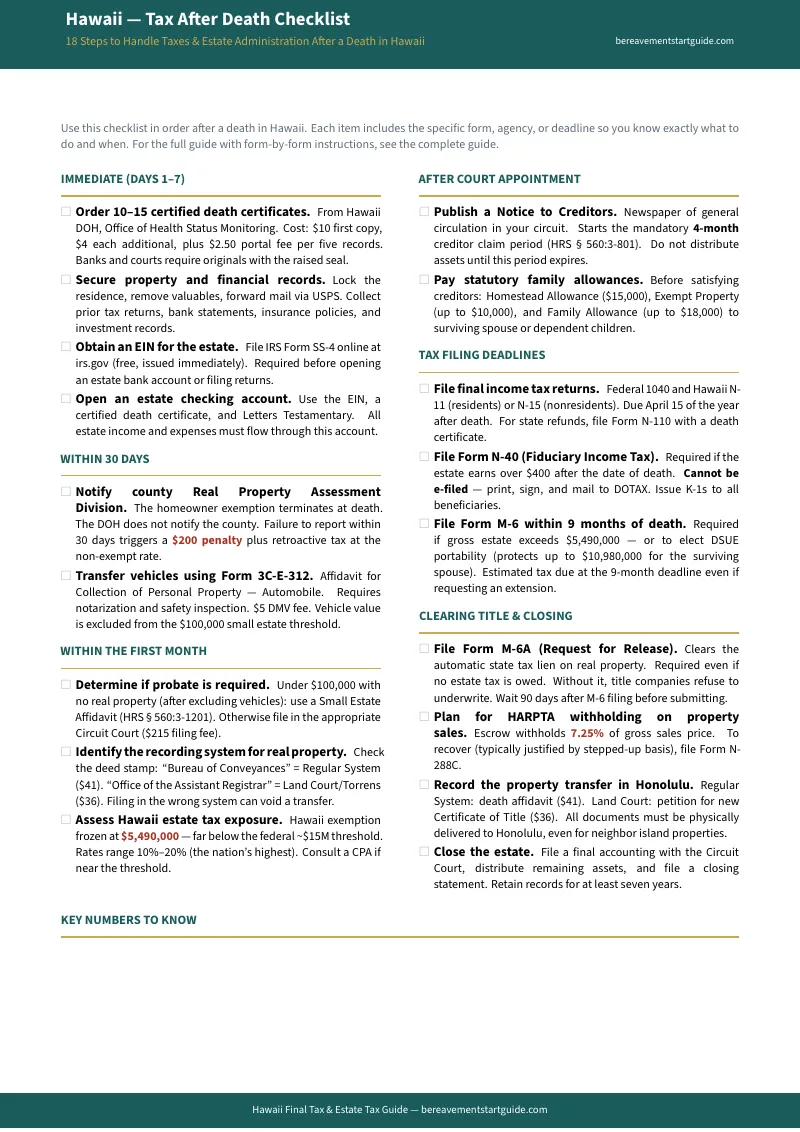

- Hawaii Tax After Death Checklist — 19-item printable checklist organized by deadline: immediate actions (days 1-7), 30-day county notification, court appointment tasks, tax filing deadlines, and closing procedures

- Exclusion Gap Worksheet — fillable asset inventory to calculate whether the estate falls between Hawaii's $5.49M threshold and the federal $15M exemption, with the progressive rate bracket calculator

- Five-Return Filing Sequence — one-page chronological reference showing all five tax returns, deadlines, thresholds, and form numbers

- Step-Up in Basis Worksheet — calculate the new tax basis for every inherited asset, with the 50% surviving spouse limitation worked through step by step

- HARPTA Withholding Worksheet — the 7.25% nonresident withholding calculation, Form N-288C refund process, and cash flow planning for the escrow hold

- County Property Tax Guide — 30-day notification deadline, all four county contacts, exemption amounts, September 30 re-filing instructions, and a confirmation tracker

- CPA Handoff Organizer — document preparation checklist so you arrive at the accountant's office with everything sorted and pay for tax strategy, not file organization

- Forms Directory — every DOTAX, circuit court, and county form in one printable page with form numbers, filing methods, and fees

- Key Deadlines Tracker — wall-mount reference with every critical deadline from date of death through estate closure, with space to write your actual due dates

Who This Is For

- Named executors who need to know whether the estate falls in the exclusion gap — owing Hawaii estate tax despite owing zero federal tax — and how to calculate the liability, file Form M-6, and secure the M-6A tax release to close probate

- Surviving spouses who need to understand the DSUE portability election, the 50% step-up limitation in a non-community property state, and how to protect the homeowner property tax exemption after the owner's death

- Out-of-state adult children inheriting Hawaii real estate who need to understand HARPTA withholding, the Form N-288C refund process, and the conveyance tax exemption filing on Form P-64B

- Beneficiaries who want to understand why distributions are delayed — why the executor cannot legally release funds until all tax returns are filed, the creditor window closes, and the M-6A tax release is secured

- Executors preparing for a CPA handoff who want to organize the estate's financial records, track down missing 1099s and K-1s, and arrive at the accountant's office with everything sorted so they are not paying $350 an hour for document organization

Why Free Resources Fall Short

The Hawaii Department of Taxation provides blank forms — Form M-6, Form N-40, Form N-110, Form P-64B — but it does not tell you which ones apply to your estate, in what order to file them, or how the thresholds interact. SmartAsset and national finance blogs mention the $5.49 million exemption but skip the county property tax traps, the HARPTA withholding rules, and the M-6A release requirement. Attorney websites give you enough information to understand you have a problem, then quote you $4,000 to $8,000 to solve it.

This guide covers only Hawaii. Every form number, every threshold, every deadline, and every calculation applies to your estate and your state. It is the missing manual between free government forms that assume you are a tax professional and an attorney retainer that depletes the estate before the family sees a distribution.

What This Guide Does Not Do

This is an educational and administrative tool — not tax advice or legal representation. If the estate is valued near the $5.49 million exclusion threshold, involves complex business structures, includes Hawaiian Home Lands leaseholds, or faces a dispute between beneficiaries, you need a licensed Hawaii CPA or estate attorney. When that is the case, the guide tells you exactly why and what kind of professional to hire. For straightforward estates where the family agrees and you need to file the right forms on time without paying thousands in professional fees for basic guidance, this guide gives you the complete roadmap.

— Less Than Ten Minutes of a Hawaii CPA's Time

Hawaii CPAs specializing in estate and fiduciary tax charge $250 to $400 per hour. A full estate tax engagement runs $3,000 to $6,000. Filing fees for the circuit court alone are approximately $215. This guide costs less than ten minutes of billable CPA time and covers every tax form, threshold, and deadline those fees are supposed to pay for.

Every purchase includes a 30-day money-back guarantee. If the guide does not give you the clarity and confidence you need to handle the estate's tax obligations, email us for a full refund.

The free Tax After Death Checklist covers the immediate deadlines — ordering death certificates, notifying the county within 30 days, obtaining an estate EIN, and identifying which returns are required. The full guide covers every calculation, form, and filing procedure from there through the M-6A tax release and final distributions, with step-up in basis worksheets, HARPTA refund instructions, and the complete five-return filing sequence.