The Federal Exemption Is $15 Million. Illinois Says $4 Million. And Nobody Told You.

Someone you love just died in Illinois. You Googled "estate tax" and the first result told you the exemption is $15 million per person -- so you assumed the estate was fine. Then your CPA called. Or the bank officer mentioned something about a "state estate tax." Or a financial advisor said the words "cliff calculation."

Now you're staring at the reality: Illinois has its own estate tax with a $4,000,000 threshold -- less than a third of the federal number. That threshold includes the house, the retirement accounts, the life insurance death benefit, the cars, everything. In the Chicago suburbs, a modest home plus a 401(k) and a term life policy can push a family over that line without anyone realizing it until after the funeral.

And here's what makes the Illinois estate tax truly dangerous: it's a cliff. An estate worth $3,999,999 owes nothing. An estate worth $4,100,000 owes roughly $28,000 to $30,000. There's no gradual phase-in. The tax hits retroactively across the entire estate using a calculation based on pre-2001 federal tables that almost nobody outside of estate attorneys understands.

Meanwhile, you're also supposed to file the decedent's final income tax return with the Illinois Department of Revenue. If the estate earned any income during probate -- bank interest, dividends, rental payments -- that goes on a separate fiduciary return filed with a different division of the same agency. And the estate tax itself? That goes to a third agency entirely: the Illinois Attorney General. Three agencies. Three sets of forms. Three different mailing addresses. Zero coordination between them.

The Three-Agency Tax Navigator

This guide does what no single government website, legal aid page, or attorney consultation does: it puts every Illinois post-death tax obligation into one chronological sequence -- with the exact forms, the specific agency for each filing, the real deadlines, and the traps that catch families every year.

It's built specifically for Illinois executors and beneficiaries. Not a generic national tax overview with "check your state laws" footnotes. Every chapter addresses the exact agencies, thresholds, and calculations that make Illinois different from the other 49 states -- the $4 million cliff, the interrelated computation, the non-portable exemption, the Attorney General filing requirement, the three-agency split, and the property tax exemption clawbacks that hit families who forget to notify the county assessor.

What You Get

The Complete Guide

- The full tax landscape after a death in Illinois -- all five possible tax obligations mapped out: final income tax (IL-1040), fiduciary income tax (IL-1041), state estate tax (Form 700), federal estate tax (Form 706), and property tax adjustments. Which apply to you, who you file with, and when each is due

- The $4 million estate tax cliff explained -- how the Illinois interrelated calculation actually works, why an estate worth $4.1 million owes $28,000 while $3.99 million owes nothing, the graduated rate structure from 0.8% to 16%, and what the State Death Tax Credit Table means in plain English

- Form 700 filing walkthrough -- the Illinois estate tax return filed with the Attorney General's Revenue Litigation Bureau, including which office to mail it to (Chicago for Cook, DuPage, Lake, and McHenry counties; Springfield for all others), required attachments, the 6-month extension process, and the separate payment procedure through the State Treasurer

- Final income tax return instructions -- how to file the decedent's last IL-1040 covering January 1 through date of death, signature requirements for executors, and how to claim a refund using Form IL-1310 with the specific court certificates IDOR demands

- Fiduciary income tax (IL-1041) -- when the estate itself must file as a separate entity, the $600 federal threshold, fiscal year election strategy, and how to report estate income that Illinois taxes differently than the federal government

- Step-up in basis for inherited property -- how the basis resets to date-of-death fair market value, capital gains implications when selling the family home, the community property trust double step-up, and common appraisal mistakes that cost beneficiaries thousands

- The portability trap -- why Illinois does not allow portability of the unused $4 million exemption between spouses (unlike the federal system), what this means for the surviving spouse's estate plan, and the Bypass Trust strategy that must be implemented before death to preserve both exemptions

- Property tax exemption adjustments -- what happens to the Senior Citizens Homestead Exemption and Senior Citizens Assessment Freeze after a death, which county assessor to contact, and the clawback penalties families face when they forget to cancel exemptions

- Estate EIN application -- the step-by-step Form SS-4 process, online vs. phone application, and why the bank will reject every financial transaction until you have this number

- CPA preparation checklist -- the exact documents and organized information your tax professional needs, structured to minimize their billable hours so you pay for strategy, not for sorting through a shoebox of receipts

- Complete deadline calendar -- every federal and Illinois deadline on one timeline, from the first week through final distributions, including extension procedures for each filing

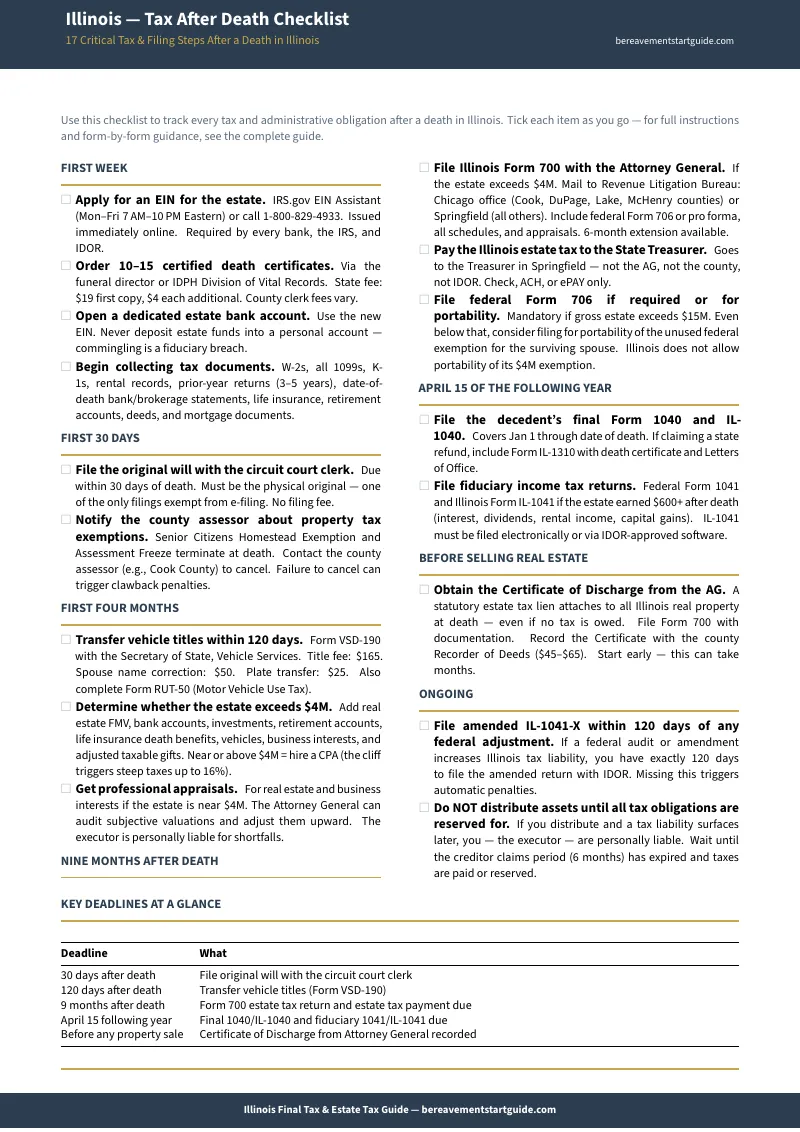

The Tax After Death Checklist

- 18 sequenced action items -- from applying for the estate EIN in the first week through filing the final fiduciary return, organized by time period (first week, first 30 days, first four months, nine months, April 15)

- Every form referenced by name -- Form 700, IL-1040, IL-1041, Form 706, IL-1310, SS-4, VSD-190, RUT-50. No hunting through agency websites to figure out which form you need next

- Agency and contact details included -- so you know exactly who to call and where to send each filing

8 Standalone Printable Tools

- Three-Agency Filing Roadmap -- one-page reference showing which form goes to which agency, with mailing addresses for the Attorney General (Chicago and Springfield offices), State Treasurer, and IDOR

- Tax Deadline Calendar -- every statutory deadline from the first week through final filing, with a fillable "Your Date" column to track progress

- Gross Estate Calculation Worksheet -- fillable worksheet to estimate whether the estate exceeds the $4 million Illinois threshold

- CPA Preparation Packet -- six-folder document organization system with checkboxes for every document your tax professional needs

- Step-Up in Basis Valuation Log -- log each inherited asset's stepped-up basis with space for appraisals, securities, business interests, and other assets

- Forms and Agency Reference -- every form, agency, address, and phone number in one desk reference

- County Probate Fee Reference -- filing fees for nine major Illinois counties, plus additional costs, the Small Estate Affidavit threshold, and priority statutory awards

- Property Tax Exemption Alert -- action items to cancel property tax exemptions after death and prevent clawback penalties

The Free Illinois Tax Obligations Checklist

A printable one-page checklist covering the core tax obligations and deadlines after a death in Illinois. Available as a free download so you can see the full scope of what's required while deciding whether the complete guide is right for your situation.

Who This Is For

- Executors navigating the Illinois estate tax for the first time -- you've been told the estate might exceed $4 million and need to understand what that means before your first meeting with a CPA or attorney

- Surviving spouses who need to understand the portability trap, the final joint return options, and how the $4 million threshold applies differently when one spouse dies first

- Adult children settling a parent's estate who are overwhelmed by the three-agency split and need a single roadmap that connects the dots between the Attorney General, IDOR, and the IRS

- Beneficiaries selling inherited property who need to understand step-up in basis and capital gains before listing the family home, and want to know whether the estate tax lien must be cleared first

- Anyone preparing to meet with a professional -- an organized executor who walks in with documents sorted and questions prepared saves the estate thousands of dollars in billable hours versus one who hands over a file box and says "figure it out"

Why Not Just Use the Free Government Websites?

Every form in this guide is available for free from an Illinois state agency. The IDOR publishes Form IL-1040 instructions. The Attorney General's website has the Form 700 and an estate tax calculator. The IRS has Form SS-4 online.

What's not free -- and what no government website provides -- is how these pieces connect. The Attorney General's website won't tell you that you also need to file a fiduciary return with IDOR if the estate earns income during probate. IDOR's instructions for Form IL-1041 won't mention that the estate tax payment goes to the State Treasurer -- not to IDOR, not to the Attorney General, not to the county. The IRS will help you get an EIN but won't explain the Illinois cliff calculation that makes the state estate tax so much more punishing than the federal one.

Each agency handles its piece. None of them tell you what the next agency in line requires. This guide puts the three-agency maze into one straight line -- every form, every deadline, every agency, in the order you actually need them.

-- Less Than 15 Minutes of CPA Time

Illinois CPAs with estate tax experience charge $300 to $500 per hour. Probate attorneys charge similar rates. If you walk into a consultation without understanding the difference between Form 700 and Form IL-1041, or without knowing that the estate tax payment goes to the State Treasurer while the return goes to the Attorney General, you'll spend your first billable hour getting educated on basics. This guide covers those fundamentals so your professional time is spent on strategy -- the interrelated calculation, QTIP elections, and distribution planning -- not on explaining which agency gets which form.

If the guide doesn't save you at least five hours of frustrating research across scattered government websites, email us within 30 days for a full refund. No questions asked.