The IRS Wants the Final Income Tax Return. The Kansas Department of Revenue Wants the Fiduciary Return. The Title Company Wants an Inheritance Tax Waiver for a Tax That Was Repealed in 1998. The Estate Generated Farm Rent Last Month and Nobody Told You That Triggers a Separate Tax Filing. You Are Settling an Estate in Kansas, and Every Agency Assumes You Already Know Which Forms to File and When.

You called the Kansas Department of Revenue to ask about taxes after the death. They told you the final individual return is due April 15 and the estate's fiduciary return is due by the fifteenth day of the fourth month after the close of the taxable year. You asked what that means. They said to consult a tax professional. You called the title company to transfer the house. They said they need an "Inheritance Tax Waiver" before they will clear the title. You told them Kansas eliminated the inheritance tax. They said the property was originally transferred decades ago and the old statute still applies to that transfer. They cannot proceed without the waiver.

You searched online. You found three law firm blogs that explained Form K-41 is mandatory for estate income and ended with "contact us for a consultation at $300 per hour." You found the KDOR website with a dense PDF instruction manual for the K-41 that assumes you already understand fiduciary modifications, beneficiary allocation schedules, and Kansas source income withholding. You found a Reddit thread where someone said the executor is personally liable for unpaid taxes. You do not know what is true, what applies to your estate, or what to file first.

Meanwhile, critical tax decisions are compounding. If the estate includes out-of-state beneficiaries, Kansas law requires the fiduciary to withhold state income tax and issue Form K-18 to each nonresident beneficiary — a requirement most executors learn about only after the KDOR issues an assessment. If the estate includes inherited farmland or real estate, the step-up in basis resets the property's tax value to the date-of-death fair market value — potentially eliminating hundreds of thousands of dollars in capital gains taxes — but only if you establish the valuation correctly. If the deceased received Medicaid benefits, Kansas operates an Expanded Estate Recovery program that reaches non-probate assets including TOD deeds and joint tenancy, regardless of whether those assets pass through probate. Every one of these issues is governed by a different section of the Kansas code, administered by a different agency, with different deadlines and different consequences for getting it wrong.

The Kansas Final Tax & Estate Tax Guide is a Kansas Tax Compliance Roadmap for every tax return, form, deadline, and filing obligation an executor or beneficiary faces after a death in Kansas. Not a generic national estate tax primer with Kansas's name attached. Not a law firm blog designed to generate $300-per-hour consultations. A plain-English, Kansas-specific manual that tells you what the KDOR instruction manuals, county title companies, and IRS publications cannot: which taxes actually apply to your estate, which forms to file, in what order, by which deadlines, and which common mistakes create personal liability for the executor.

What's Inside the Kansas Tax Compliance Roadmap

A step-by-step guide, a tax obligations checklist, and standalone reference sheets covering every tax return, filing obligation, and asset transfer decision an executor or beneficiary faces after a death in Kansas, built on the Kansas Statutes Annotated, the Kansas Department of Revenue instructions, and IRS Publication 559 — not a generic template repurposed with Kansas terminology:

Final Income Tax Returns: Federal and Kansas K-40

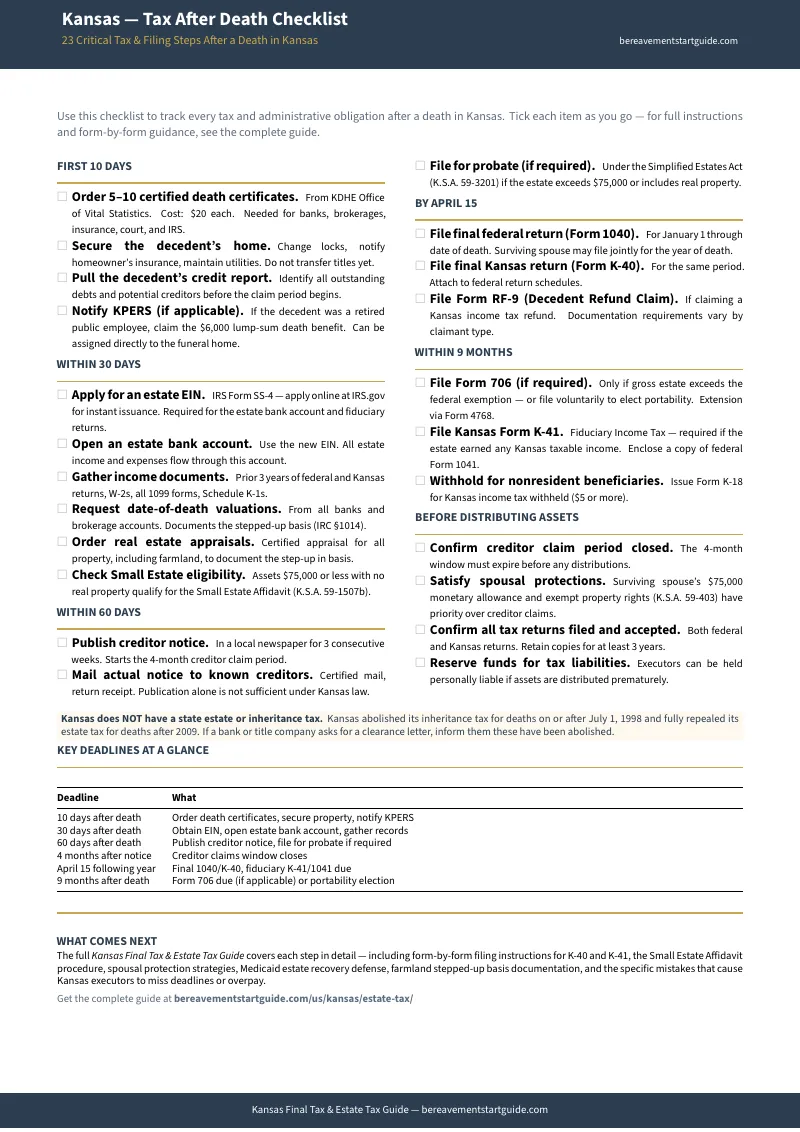

The deceased's final individual tax returns must be filed for the year of death. The guide walks you through the federal Form 1040 and Kansas Form K-40 filing process step by step — how a surviving spouse can elect to file jointly for the final year, what income must be reported on the decedent's return versus the estate's return, how to handle income received after death but earned before death (income in respect of a decedent), and the documentation the KDOR requires. The April 15 deadline applies regardless of probate status. Extensions are available but must be requested before the deadline, not after.

Kansas Fiduciary Income Tax: Form K-41 Decoded

If the estate earns any income during administration — farm rent, stock dividends, bank interest, business income, rental payments — a separate Kansas Fiduciary Income Tax Return (Form K-41) is mandatory. This is the filing most executors miss entirely, because nothing in the probate process alerts you to its existence. The guide explains the trigger threshold, the filing deadline (fifteenth day of the fourth month after the close of the estate's taxable year), the Kansas fiduciary modification calculation, how income is allocated proportionately among beneficiaries, and the critical requirement to enclose a complete copy of the federal Form 1041 with every K-41 submission.

Nonresident Beneficiary Withholding: Form K-18

If any beneficiary lives outside Kansas, the executor is legally required to withhold Kansas income tax on that beneficiary's share of estate income and issue them a Form K-18. Failure to withhold creates direct personal liability for the executor — the KDOR can assess the unpaid tax against you individually, not the estate. The guide covers the withholding calculation, the K-18 reporting requirements, the interaction between the K-41 and K-18 filings, and the specific documentation that protects you from personal assessment.

The Kansas Estate and Inheritance Tax: History, Repeal, and Title Clearing

Kansas levies neither an estate tax nor an inheritance tax for deaths occurring today. The inheritance tax was abolished for deaths after July 1, 1998, and the standalone estate tax was phased out entirely for deaths after 2009. But the legacy of these repealed taxes still creates real friction. Title companies and the Register of Deeds regularly demand inheritance tax waivers to clear title on property originally transferred before the repeal. The guide explains the full history, walks you through the waiver process, clarifies when Form K-706NT (Request for Determination of No Kansas Estate Tax Liability) applies, and identifies the one situation where a Kansas beneficiary could still owe inheritance tax — inheriting property located in a state that maintains one.

Step-Up in Basis: Protecting Inherited Property from Capital Gains

The step-up in basis is the single most valuable tax protection available to Kansas beneficiaries — and the one most frequently mishandled. When you inherit property, the tax basis resets to the fair market value on the date of death. Farmland purchased in 1975 for $50,000 that is worth $800,000 at the date of death carries a new basis of $800,000. An immediate sale generates zero federal capital gains tax. But this protection requires proper valuation documentation established at the time of death, not years later when you decide to sell. The guide explains how to document the step-up for Kansas farmland, residential real estate, and investment property, including the alternate valuation date election available to estates filing Form 706.

Federal Estate Tax: Form 706 and Portability

The federal estate tax applies only to estates exceeding the exemption threshold — currently $15 million per individual for 2026 deaths, with a scheduled reduction in 2026. Most Kansas estates fall well below this threshold. But two critical planning tools exist even for smaller estates. The portability election allows a surviving spouse to claim the deceased spouse's unused exclusion, effectively doubling the exemption for the surviving spouse's eventual estate. Filing a Form 706 solely to elect portability costs time but can save the family millions in future taxes. The guide explains the nine-month filing deadline, the portability election mechanics, and how to determine whether your estate triggers the Form 706 requirement.

Medicaid Estate Recovery: The Expanded Estate Trap

If the deceased received KanCare long-term care benefits, the Kansas Department of Health and Environment will file a recovery claim against the estate — and Kansas uses an Expanded Estate definition that reaches far beyond probate. TOD deeds, joint tenancy, survivorship property, pay-on-death accounts, and life estates are all subject to recovery. The guide explains the exact scope of KDHE's recovery authority, the exemptions that protect surviving spouses and minor children, the priority of funeral expenses over Medicaid claims, and how to apply for a hardship waiver or caregiver exemption when the estate consists primarily of the family home.

Small Estate Bypass and Spousal Protections

Kansas provides statutory mechanisms to avoid or minimize probate entirely. The K.S.A. 59-1507b Small Estate Affidavit allows heirs to claim assets without court involvement when the estate does not exceed $75,000, excluding real estate. The K.S.A. 59-403 statutory allowance gives the surviving spouse up to $75,000 in cash or property, plus the homestead, vehicles, and household furnishings — shielded from the claims of unsecured creditors. The K.S.A. 59-2287 Refusal to Grant Letters of Administration provides an additional bypass when estate value falls within statutory allowances. The guide maps the exact parameters and filing procedures for each mechanism.

Who This Guide Is For

- The executor who just discovered the estate earned income during probate — who has never heard of Form K-41, does not know the filing deadline, and cannot determine whether the estate's farm rent, stock dividends, or rental income triggers a fiduciary return that nobody in the probate process mentioned

- The out-of-state executor managing a Kansas estate remotely — who needs to understand Form K-18 withholding requirements for nonresident beneficiaries before the KDOR discovers the omission and issues a personal assessment against the executor individually

- The beneficiary preparing to sell inherited Kansas farmland or real estate — who knows the step-up in basis exists but does not know how to document the date-of-death fair market value, whether an appraisal is required, or how the alternate valuation date works for estates that also file Form 706

- The family whose title company is demanding an inheritance tax waiver — who cannot clear title to inherited property because the Register of Deeds requires documentation for a tax that was repealed decades ago, and no one at the county office can explain the process

- The surviving spouse trying to protect assets from creditors and Medicaid recovery — who assumed the TOD deed on the house meant the property bypassed probate and Medicaid, and now needs to understand the Expanded Estate recovery rule and the K.S.A. 59-403 statutory allowance that shields up to $75,000 from unsecured creditors

- The adult child settling a parent's estate from another state — who is coordinating final returns, fiduciary returns, property transfers, and beneficiary distributions across Kansas and federal jurisdictions and needs every form, deadline, and filing sequence in one document

Why Free Resources Will Not Get You Through This

Kansas tax and estate information exists. The Kansas Department of Revenue publishes forms and instructions, the Kansas Judicial Council publishes probate court forms, and the IRS publishes Publication 559 on estate taxes. Here is what you actually encounter when you try to navigate estate taxes using free sources:

- The Kansas Department of Revenue publishes Form K-41 instructions — in statutory language for accountants. The instructions assume you already understand fiduciary modifications, beneficiary income allocation, and the interaction between the K-41 and federal Form 1041. They tell you which lines to fill in. They do not tell you whether your estate needs to file in the first place, or how to determine what constitutes taxable estate income, or that enclosing the federal 1041 is mandatory to prevent processing delays.

- The IRS publishes Publication 559 — covering federal rules only. Publication 559 explains federal estate tax, final income tax, and fiduciary returns. It has zero information about Kansas-specific filings: no K-41, no K-18 withholding for nonresident beneficiaries, no inheritance tax waiver process, no K-706NT. A federal guide cannot navigate a state-level tax system.

- Title companies demand waivers — and cannot explain the process. When a title company requires an inheritance tax waiver to clear a property transfer, they send you to the Register of Deeds. The Register of Deeds sends you to the county clerk. The county clerk tells you to contact the KDOR. The KDOR tells you to file Form K-706NT. None of them explains the full sequence or that this applies only to transfers predating the 1998 repeal. You spend days in a loop between offices.

- Law firm blogs explain the dangers — and end with a phone number. Every estate planning and probate firm in Kansas City, Wichita, and Topeka publishes blog posts about executor liability, fiduciary tax obligations, and Medicaid recovery. The posts are accurate, alarming, and deliberately incomplete. They explain the risk in enough detail to frighten you. They never explain the solution in enough detail to act on it. Every post ends with a consultation invitation at $300 or more per hour.

- No free resource connects federal and Kansas filings into one sequence. The IRS handles federal returns. The KDOR handles state returns. The county handles property transfers. Each agency knows its own forms and nothing about the others. No free resource tells you that filing the federal 1041 is a prerequisite for the Kansas K-41, that the K-18 withholding must be completed before you distribute income to nonresident beneficiaries, or that the step-up in basis documentation must be established before you sell the property — not after.

Free resources give you KDOR instruction manuals written for CPAs, IRS publications that ignore Kansas filings entirely, and law firm blogs that end with a billable-hour phone number. The Kansas Tax Compliance Roadmap puts every tax return, form, deadline, and filing sequence into one document, in the order you actually need them.

— Less Than Fifteen Minutes With a Kansas Estate Attorney

A consultation with a Kansas probate or estate attorney runs $300 per hour or more. A CPA preparing the federal 1041 and Kansas K-41 fiduciary returns charges $500 to $1,500 depending on estate complexity. A title company charging for inheritance tax waiver research adds another $200 to $500. This guide costs less than fifteen minutes of professional legal time and gives you the complete Kansas-specific tax roadmap — every return, every form, every deadline, and the filing sequence that determines whether the executor faces personal liability or not.

Your download includes the complete step-by-step guide covering every tax obligation category, the standalone Kansas Tax After Death Checklist, and printable reference sheets: the Tax Filing Decision Flowchart, the Kansas Fiduciary Return (K-41) Quick Reference, the Nonresident Beneficiary Withholding Worksheet (K-18), the Step-Up in Basis Valuation Guide, the Estate Tax versus Inheritance Tax Clarifier, the Medicaid Estate Recovery Quick Reference, and the Kansas Estate Tax Timeline with every federal and state deadline mapped to a calendar. Instant download, no account required.

30-day money-back guarantee. If this guide does not save you hours of confusion with the KDOR and make the estate tax filing process immediately clearer, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Kansas — Tax After Death Checklist — an overview of the tax obligations that apply after a death in Kansas, the key forms and deadlines, and the most common executor mistakes. Enough to understand what you need to file and whether you need the full guide.

Nobody trained you for this. The KDOR assumes you understand fiduciary modifications. The title company assumes you know the inheritance tax waiver process. The IRS assumes you can navigate Publication 559 without Kansas-specific context. You have something none of them provide — a single roadmap that connects every federal and Kansas tax obligation into one sequence, with plain-English instructions for each one.