The Inheritance Tax Was Repealed. The Estate Tax Doesn't Apply. But You Still Owe Taxes on This Estate --- And Louisiana's Civil Law System Means the Forms, Deadlines, and Rules Are Different from Every Other State.

Someone has died, and you are trying to figure out what taxes the estate owes --- in a state where the answers are unlike anywhere else in the country. You searched for "Louisiana inheritance tax" and found conflicting information: some sites say it was repealed, others reference forms you've never seen. You called the Louisiana Department of Revenue and were told to file an IT-541 by May 15 --- a form and a deadline that do not exist in any other state's tax code. You went to the bank to open an estate account and were told you need an EIN from the IRS first. Meanwhile, you discovered that selling the family home requires a Judgment of Possession before any title company will touch the transaction --- and that something called a "double step-up in basis" could eliminate the capital gains tax entirely, but only if you handle the paperwork in the right order.

Here is what makes Louisiana different: property is classified as community or separate. A surviving spouse does not automatically inherit --- they receive a usufruct. Children under 24 are forced heirs with a guaranteed share regardless of the will. The state income tax just changed to a flat 3% rate. Estates under $125,000 can bypass court through a Small Succession Affidavit that was dramatically expanded by Act 90 of 2026. And the federal estate tax exemption of $15 million means 99% of families will never file Form 706 --- but may need to file it anyway for portability. National tax guides written for common-law states will steer you wrong on every one of these points.

The Louisiana Final Tax & Estate Tax Guide is a Civil Law Tax Navigation System built for the only state in the nation where succession law, community property rules, and tax obligations all operate under a framework the other 49 states do not use. Not a generic estate planning article. Not a funeral home checklist. A plain-English, Louisiana-specific tax reference that tells you which taxes apply, which do not, what forms to file, what deadlines to meet, and how to structure every transaction for maximum tax efficiency under Louisiana's civil code.

What's Inside the Civil Law Tax Navigation System

A 15-chapter guide and a quick-start tax checklist --- covering every tax obligation, filing procedure, asset transfer strategy, and statutory deadline that Louisiana executors and beneficiaries face after a death:

Chapter 1: The Three Taxes That Actually Apply

The chapter that stops the panic. Louisiana repealed its inheritance tax in 2008. The state estate transfer tax is gone. But three taxes do apply: the final individual income tax return (IT-540), the fiduciary income tax return (IT-541) for income the estate earns after the date of death, and the federal estate tax (Form 706) for estates exceeding $15 million. The guide explains exactly which ones affect your estate and which ones you can ignore --- so you stop searching for forms that do not exist.

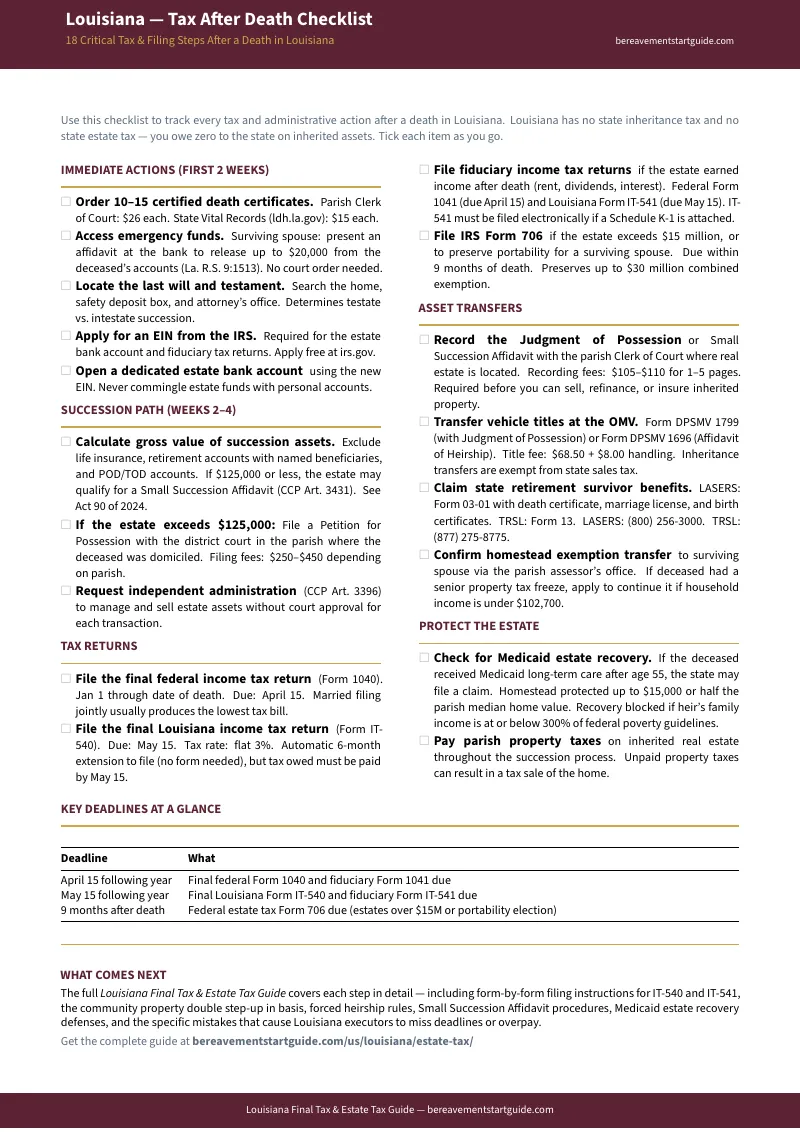

Chapter 2: Immediate Actions in the First 30 Days

The procedural steps that cannot wait. How many certified death certificates to order and from where ($7.00 from the state registrar vs. $26.00 from parish clerks). How to access emergency funds before the estate account is opened. How to apply for the estate's EIN from the IRS --- the number you need before you can file any fiduciary returns or open an estate bank account. And the agencies you must notify immediately: Social Security, the VA, employers, financial institutions, and the Louisiana Department of Revenue.

Chapter 3: Does the Estate Qualify for a Small Succession?

The most valuable chapter for modest estates. If the gross estate is $125,000 or less, you can bypass the entire formal succession process using the Small Succession Affidavit. The guide covers the Act 90 of 2024 changes that most competitors have not updated for: the 90-day waiting period is eliminated, death certificate attachment is no longer required, testate estates without real estate now qualify, and the notice period for non-signing heirs is 30 days. Step-by-step instructions from eligibility calculation through notary execution and parish recording.

Chapter 4: The Formal Succession Process

When the estate exceeds $125,000 or involves real estate with a will. How to file the Petition for Possession in the parish where the decedent was domiciled. How Independent Administration under La. C.C.P. art. 3396 lets you sell property and pay debts without court approval for every transaction. Inventory requirements, creditor notification rules, and the special considerations for non-resident executors serving in Louisiana.

Chapter 5: Community Property, Usufruct, and Forced Heirship

The Louisiana-specific legal framework that changes everything about how taxes are calculated. Community property vs. separate property --- and why the classification determines whose name goes on which tax return. Usufruct --- the surviving spouse's right to use, occupy, and collect income from the deceased's property, and who pays the income tax on those fruits (the usufructuary, not the naked owners). Forced heirship --- why children under 24 are guaranteed 25% or 50% of the estate regardless of the will, and how this affects distribution planning and tax liability.

Chapter 6: Filing the Final Individual Income Tax Returns

The deceased's last personal tax returns. Federal Form 1040 for income earned from January 1 through the date of death, due April 15. Louisiana Form IT-540 for the same period. How surviving spouses can file jointly in the year of death to maximize deductions. The flat 3% Louisiana income tax rate effective for 2025 and 2026 --- replacing the old graduated brackets. And the critical dividing line: income earned before death goes on the IT-540, income earned after death goes on the IT-541.

Chapter 7: Filing the Fiduciary Income Tax Returns

The estate's own income tax returns --- the forms that confuse most executors. Federal Form 1041 for estate income after the date of death. Louisiana Form IT-541, which uses the federal modified taxable income as its starting point. The May 15 filing deadline for calendar-year estates. The electronic filing mandate when a Schedule K-1 is attached. And the new flat 3% rate that replaced the old 1.85% to 4.25% graduated brackets.

Chapter 8: The Federal Estate Tax and Portability

The chapter most executors need but misunderstand. The $15 million federal exemption means 99% of estates owe zero federal estate tax. But filing Form 706 anyway --- within 9 months of death --- lets the surviving spouse capture the deceased spouse's unused exemption through portability, effectively doubling the couple's lifetime exemption to $30 million. In Louisiana's community property regime, this is a critical wealth protection strategy that many families skip because they think the form is only for taxable estates.

Chapter 9: Step-Up in Basis and the Louisiana Double Step-Up

The most powerful tax advantage available to married couples in Louisiana. When one spouse dies, both halves of community property receive a full step-up to fair market value --- the deceased's half and the surviving spouse's half. A family home purchased for $200,000 that is worth $400,000 at the date of death gets a stepped-up basis of $400,000 for both halves. Sell it the next day and the capital gains tax is zero. The guide explains how to secure this benefit through a properly recorded Judgment of Possession and a date-of-death appraisal.

Chapter 10: Property Tax and the Homestead Exemption

The ongoing obligations that executors must not miss. Parish property taxes must continue to be paid during the succession --- failure creates tax sale liability for the executor personally. How to transfer the $75,000 homestead exemption. How to apply for the assessment freeze for surviving spouses age 65 or older. And how to handle the special assessment freeze for disabled veterans' surviving spouses.

Chapter 11: Medicaid Estate Recovery

The chapter that provides the most relief for families who fear losing the family home to the state. If the decedent received Medicaid long-term care after age 55, the Louisiana Department of Health is mandated to seek reimbursement. But recovery is deferred entirely while the surviving spouse is alive. And the undue hardship waiver --- available when an heir's family income is 300% or less of the Federal Poverty Level --- can stop recovery permanently. The guide details every exemption, every waiver criterion, and every procedural step.

Chapters 12-15: Asset Transfers, Vehicle Titles, Retirement Benefits, and Closing

Transferring real estate through a Judgment of Possession recorded in parish conveyance records. Vehicle title transfers through the OMV using Forms DPSMV 1696 and 1799. State retirement survivor benefits from LASERS and TRSL --- including what the repeal of the Government Pension Offset changed, so a survivor can now draw the full state pension and the full Social Security survivor benefit together. And the complete succession-closing procedure: final accountings, filing final tax returns, obtaining tax clearances, and distributing assets to heirs.

Who This Guide Is For

- The executor who just discovered Louisiana has different rules --- who searched for "probate" and learned Louisiana calls it "succession," who searched for "life estate" and learned Louisiana uses "usufruct," and who now realizes that every national guide they downloaded uses terminology their parish court clerk will not accept. The guide uses correct Louisiana civil law terminology throughout and explains every procedural difference.

- The out-of-state adult child managing a parent's estate remotely --- who was named as the succession representative but lives in a common-law state and cannot figure out how Louisiana's forced heirship rules, community property classification, or the IT-541 filing deadline affect the decisions they need to make. The guide walks through every step in the order you need to take it.

- The surviving spouse trying to understand the double step-up --- who just learned that selling the family home could trigger zero capital gains tax under Louisiana's community property rules, but only if they get a date-of-death appraisal and record a Judgment of Possession before the sale. The guide explains the exact sequence of actions required to capture this benefit.

- The modest-estate heir trying to avoid a $5,000 attorney retainer --- who needs to determine whether the estate qualifies for the Small Succession Affidavit under the new Act 90 rules, how to calculate the $125,000 threshold, and how to execute the affidavit without formal succession proceedings. The guide covers every step from eligibility through parish recording.

- The family worried about Medicaid taking the house --- who received a recovery notice from the Louisiana Department of Health and does not know that recovery is deferred while the surviving spouse is alive, or that the undue hardship waiver exists for families under 300% of the Federal Poverty Level. The guide details every defense available.

- The executor confused about which tax forms to file --- who cannot tell the difference between the IT-540, the IT-541, Form 1041, Form 706, and Form R-3318, and needs a clear explanation of which forms apply to their estate, when each is due, and how the numbers flow from one return to the next. The guide maps every form to its purpose, deadline, and filing sequence.

Why Free Resources Leave Money on the Table

Tax forms are free. The Louisiana Department of Revenue provides every form you need at no cost. Government websites list the filing deadlines. Here is what happens when you try to navigate all of this yourself:

- The LDR website provides Form IT-541. It does not explain how it interacts with the federal Form 1041. The modified federal taxable income from your 1041 flows directly into the Louisiana return. File one without the other and you will either double-count income or miss deductions entirely.

- TurboTax handles the federal 1040 and 1041. It does not mention the Louisiana IT-540 or IT-541. National tax software exists in a federal-only silo. It will not tell you about Louisiana's May 15 fiduciary deadline, the flat 3% state rate, or the electronic filing mandate for returns with a K-1.

- National estate planning websites explain the step-up in basis. They do not mention the Louisiana double step-up. In every common-law state, only the deceased's half of jointly held property gets a step-up. In Louisiana, both halves of community property step up. Missing this means paying capital gains tax on a home sale that should have been tax-free.

- Local succession attorneys provide accurate advice. They charge $2,500 to $6,500 for an uncontested succession. For an estate that owes no estate tax, no inheritance tax, and needs three returns filed in the correct order, that retainer is a disproportionate expense for what is fundamentally an organizational and sequencing problem.

- Competitors have not updated for Act 90 of 2024 or the 2025 flat tax rate. Pages still reference the old graduated brackets, the old 90-day waiting period for small successions, and the old requirement to attach a death certificate. Following outdated instructions creates unnecessary complications with the parish clerk.

Free resources give you one form at a time, with no sequencing, no cross-referencing, and no warning about how Louisiana's civil law system changes the tax calculations. The Civil Law Tax Navigation System maps every tax obligation to your estate's specific situation, organizes every form by deadline, and tells you exactly which returns to file in which order --- so you pay what you owe, capture every deduction and exemption available, and do not discover a missed filing deadline six months after it has passed.

--- Less Than One Hour of a CPA's Time

Louisiana executors overpay on taxes and underclaim deductions every year --- not because they are careless, but because no single resource connects the state's unique civil law framework to the federal tax code in plain English. A surviving spouse misses the double step-up because no one explained the Judgment of Possession requirement. An executor pays the old graduated state rate because no one mentioned the 2025 flat tax change. A modest estate hires a $5,000 attorney because no one explained the Act 90 Small Succession Affidavit. This guide costs less than any of those mistakes and shows you how to avoid every one of them.

Your download includes 9 PDFs --- the complete 15-chapter guide, the Louisiana Tax After Death Checklist, and 7 standalone reference sheets: the Community Property Double Step-Up Explainer, Act 90 Small Succession Update, Tax Form Filing Sequence Map, Medicaid Estate Recovery Defense, Federal Estate Tax Portability Strategy, Critical Deadlines Calendar, and Forms Reference Card. Print the checklist first. Start at the top. Work down.

30-day money-back guarantee. If the guide does not give you a clear map of every tax obligation, every form you need to file, every deduction you can claim, and every deadline you need to meet --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Louisiana Tax After Death Checklist --- a summary of the most critical tax actions, deadlines, and forms that most executors do not discover until a filing window has already closed. Enough to start organizing the estate's tax obligations in the right order.

You did not plan for this. But you can plan how the taxes get handled. The guide gives you the forms, the deadlines, the filing sequence, and the Louisiana-specific strategies --- so the next twelve months are spent settling the estate efficiently, not discovering what you missed.