Someone You Love Just Died in Massachusetts. The Bank Froze the Accounts. The Probate Court Requires Forms You Have Never Heard Of. And You Just Found Out That Massachusetts Has a $2 Million Estate Tax Threshold That a Single Family Home in Greater Boston Can Blow Through on Its Own.

You are standing in the middle of something no one prepared you for. Maybe you were named personal representative in a will that was drafted ten years ago. Maybe there was no will at all, and the family is looking at you because you are the surviving spouse, the eldest child, or simply the only one who lives in Massachusetts. The funeral director is asking how many death certificates you need at roughly $45 each. The bank told you the checking account is frozen until you produce something called a "Letter of Authority" from the Probate and Family Court. Your sister is asking about the house. And somewhere in the back of your mind, a question keeps circling: if I pay the wrong bill first, miss a deadline I do not know about, or file the wrong form with the probate court — can they come after me personally?

Yes, they can. Massachusetts General Laws Chapter 190B, Section 3-805 establishes a strict statutory priority for paying estate debts. If you pay a credit card company before you pay the funeral expenses, the court filing fees, or the MassHealth recovery claim — and the estate later runs short — you are personally liable for the difference. That is not a worst-case scenario. That is the statute. And it is just one of the traps waiting in a state that splits probate into Voluntary Administration, Informal, and Formal tiers at precise asset thresholds — a state where the Department of Revenue places an automatic tax lien on every piece of real estate the moment someone dies, and where MassHealth can pursue the family home to recover years of nursing care costs.

The When Someone Dies in Massachusetts — Estate Settlement Guide is a MUPC Triage System for every legal, financial, and administrative step between the funeral home and final distribution. Not a law textbook. Not a generic national checklist that cannot tell Massachusetts from Maryland. A structured, Massachusetts-specific manual built around the Massachusetts Uniform Probate Code — the actual statute that governs everything — that separates what must be done in the first 48 hours from what can safely wait months, so you stop guessing and start working through this in the right order.

What's Inside the MUPC Triage System

A comprehensive guide and the First 48 Hours Checklist — covering every stage from the moment of death through final asset distribution, built specifically for Massachusetts statutes, the Probate and Family Court system, the Department of Revenue, MassHealth recovery rules, and the state-specific traps that make settling an estate here different from any other state:

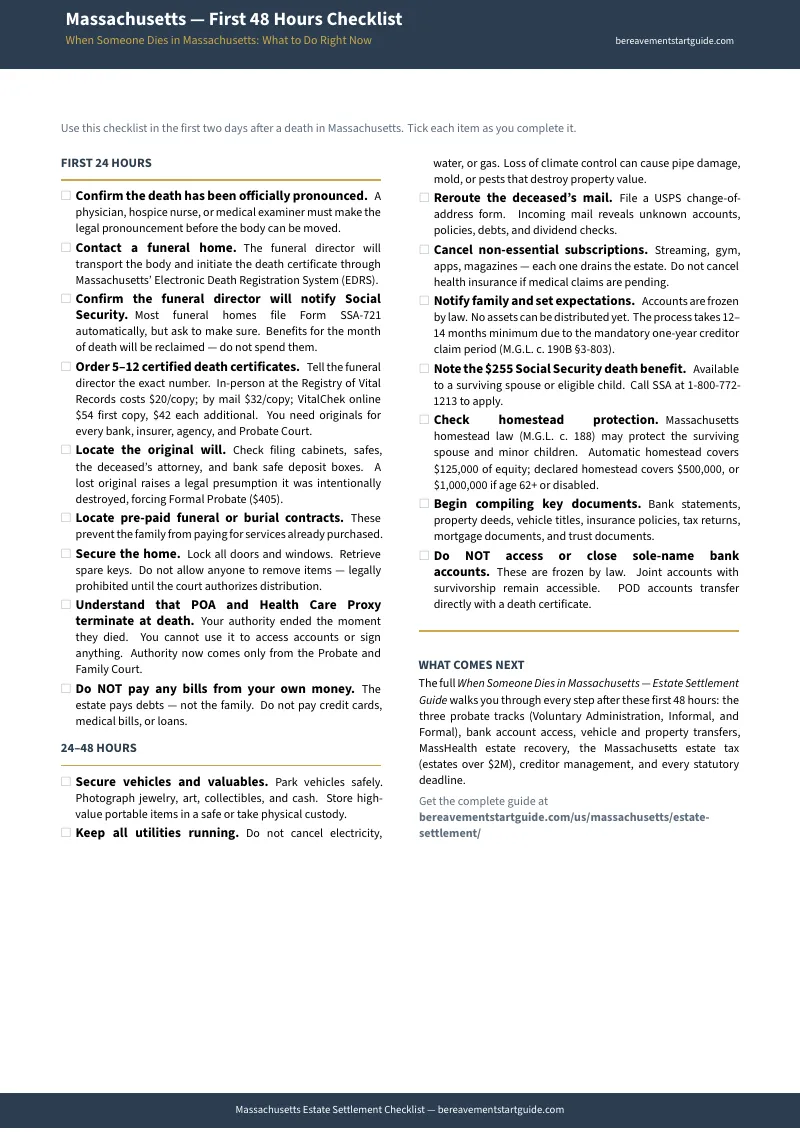

The First 48 Hours: Death Certificates and Immediate Actions

The funeral director is going to ask how many certified death certificates to order, and most families guess wrong. State-certified copies from the Massachusetts Registry of Vital Records cost approximately $45 each, and the Probate and Family Court, every bank, every insurance company, the Registry of Motor Vehicles, and the IRS will each demand an original with the raised seal — not a photocopy. The guide gives you the exact calculation based on the deceased's assets so you order the right number now instead of waiting weeks for additional copies later. This chapter also covers what to do today, what to do tomorrow, and the single most important rule in this entire guide: do not pay any of the deceased's bills with your own money.

The First Week: Securing the Estate and Setting Family Expectations

Before the Probate and Family Court gives you legal authority over the estate, you have a duty to prevent assets from being lost, stolen, or damaged. This chapter covers locking the home, securing vehicles and valuables, rerouting mail (your best forensic tool for discovering unknown accounts and debts), canceling subscriptions that drain the estate, and the family meeting where you set one critical expectation: no one takes anything until the court says so. It also addresses Massachusetts-specific property concerns — understanding whether the deceased's home is Recorded Land at the Registry of Deeds or Registered Land through the Land Court, because that distinction dictates which probate track you are forced onto later.

Banking and Financial Accounts: Unlocking Frozen Money

When a bank receives notice that an account holder has died, individual accounts are frozen immediately. Being the surviving spouse does not override the freeze. But not every account is locked. Payable-on-Death accounts transfer directly to named beneficiaries with just a death certificate. Joint accounts with right of survivorship stay open — though Massachusetts courts will scrutinize whether joint status was created merely for the convenience of the decedent. And if the total estate is personal property under $25,000, the Voluntary Administration process can unlock accounts with a $115 filing fee and streamlined paperwork. The guide maps every account type, what unlocks it, and what paperwork you need so you stop getting turned away at the counter.

Vehicle Title Transfers: The RMV Process

Vehicles are often the first asset families try to transfer — and the first place they get rejected. But Massachusetts law provides a massive statutory shortcut for surviving spouses. Under M.G.L. Chapter 90D, Section 15A, the state presumes that a vehicle held by a married couple is jointly owned with rights of survivorship. A surviving spouse can transfer the title entirely outside of probate by presenting the original title, a death certificate, and an Affidavit of Surviving Spouse to the RMV. The guide walks you through every scenario — spouse, non-spouse, with will, without will — the exact documents to bring to the RMV, and what to do when the name on the death certificate does not match the name on the title.

The Big Decision: Voluntary Administration vs. Informal vs. Formal Probate

Not every estate needs the full probate process. Massachusetts structures probate into three distinct tiers, and choosing the wrong one wastes months and potentially thousands of dollars. Voluntary Administration is the fast track for estates consisting solely of personal property valued at $25,000 or less (excluding one vehicle) — it costs just $115 and can be completed in two to six weeks. Informal Probate is an administrative process handled by a magistrate, appropriate when all heirs agree and the will is clear. Formal Probate involves a judge and is required for contested wills, unclear terms, or property registered through the Land Court. The guide includes a decision tree that walks you through the exact criteria for each tier and tells you definitively which path applies to your estate.

The Land Court Trap: Recorded Land vs. Registered Land

This is the chapter that prevents the most common real estate delay in Massachusetts. Most properties are standard Recorded Land filed at the Registry of Deeds, and an Informal Probate proceeding is typically sufficient to pass title. But if the property is Registered Land — filed through the Massachusetts Land Court — the court strictly requires a Formal Probate proceeding to determine testacy and heirs-at-law, or an explicit power of sale in a probated will, before it will issue a new Certificate of Title. If you do not check this distinction before filing, you may discover months into a real estate transaction that you filed the wrong type of probate and cannot transfer the property. The guide tells you exactly how to check your deed for this distinction and what to do about it.

The Massachusetts Estate Tax: The $2 Million Threshold

This is the chapter that justifies the entire guide for families with real estate. While the federal estate tax exemption approaches $15 million, Massachusetts maintains a notoriously low $2 million threshold with only a $99,600 credit. Given the hyper-inflated real estate market in the Greater Boston area, a modest family home combined with routine retirement accounts and life insurance can easily push a middle-class family over this line. Worse, the Department of Revenue places an automatic estate tax lien on all real estate immediately upon death. To sell the family home, the personal representative must file a notarized affidavit or a full M-706 return to obtain an M-4422 Certificate Releasing Massachusetts Estate Tax Lien from the DOR. This bureaucratic hurdle blindsides sellers weeks before closing. The guide walks you through identifying the lien early, calculating whether the estate hits the threshold, and the exact steps to obtain the release.

MassHealth Estate Recovery: The Fear That the State Will Take the House

If the deceased received MassHealth long-term care benefits after age 55 or nursing home care at any age, the state can pursue recovery from the probate estate. The pervasive fear that MassHealth will seize the family home is the single most anxiety-inducing topic in Massachusetts estate settlement — and the rules are more nuanced than most families realize. MassHealth can only recover from the probate estate, meaning assets structured outside of probate may be shielded. The guide breaks down the specific hardship waivers in plain English: the Residence and Financial Hardship Waiver for heirs who lived in the home for two years and have income below 133% of the federal poverty level, the Care Provided Waiver for heirs who kept the deceased out of a nursing facility for two years, and the automatic waiver for probate estates valued at $25,000 or less.

Creditor Management: The Debt Priority That Protects You

The estate pays the debts, not the family. But when the estate does not have enough money to pay everyone, Massachusetts law under M.G.L. Chapter 190B, Section 3-805 dictates a strict seven-tier priority: costs of administration first, then funeral expenses, then federal taxes, then medical expenses of the last illness, then state taxes and MassHealth recovery, and only then general unsecured creditors. If you pay a credit card company before satisfying higher-priority obligations and the estate later runs short, you can be held personally liable for the deficiency. The guide maps this hierarchy in plain language and gives you the framework for managing creditor demands without making mistakes that expose you to personal liability.

Government Notifications: SSA, IRS, DOR, and MassHealth

Each agency operates on its own timeline with its own forms and its own penalties for delay. Social Security benefits deposited for the month of death will be clawed back if you do not act. The IRS needs a final Form 1040 filed for the deceased. The Massachusetts Department of Revenue handles the state estate tax return. And MassHealth estate recovery operates on its own separate timeline. The guide covers every agency, every form, every deadline, and the specific exemptions that may protect your family.

Spousal and Family Protections

Massachusetts law protects surviving spouses with specific statutory rights that sit above creditor claims. The Homestead Act provides protection for the primary residence against certain creditors up to $500,000 — and a surviving spouse automatically inherits this protection. Beyond the homestead, Massachusetts provides spousal allowances, family allowances, and the right to claim an elective share of the estate regardless of what the will says. The guide explains how each protection works, which ones apply automatically, and which ones require you to file before a deadline passes.

The Complete Timeline: Every Statutory Deadline in One Calendar

From Day 1 through Month 12 and beyond, every Massachusetts statutory deadline in one sequential reference. The 30-day waiting period before filing Voluntary Administration. The one-year creditor claim period for Informal and Formal Probate. The Inventory (MPC 854) and Final Accounting (MPC 853) filing deadlines. The M-706 estate tax return deadline. Every deadline that matters, in the order it appears, with clear language about what happens if you miss it.

Who This Guide Is For

- The surviving spouse whose partner just died and whose bank accounts were frozen this morning — who needs to know which accounts stay accessible, which ones require a Letter of Authority, how to use the RMV Affidavit of Surviving Spouse to transfer the car outside of probate, and how the Homestead Act protects the family home before any creditor gets paid

- The adult child named as personal representative who lives in Connecticut or New York and is trying to manage a Massachusetts estate remotely — who needs the complete sequence of fiduciary duties, court deadlines, the MUPC timeline, and the exact forms to file with the Probate and Family Court in one document

- The family with no will who just learned that Massachusetts intestate succession laws will decide everything — who needs to understand exactly who inherits what, whether the estate qualifies for Voluntary Administration, and whether Informal or Formal Probate is required

- The person who just got rejected at the bank trying to access their deceased parent's checking account — who needs to know whether a POD designation, a joint account, or the $25,000 Voluntary Administration threshold can bypass full probate, or whether a Letter of Authority is the only path forward

- The executor dealing with real estate who just discovered that the Department of Revenue placed an automatic estate tax lien on the family home — who needs to understand the $2 million threshold, how to file for an M-4422 Certificate Releasing the lien, and whether the property is Recorded Land or Registered Land before the real estate closing falls apart

- The family terrified about MassHealth who heard that "the state will take the house" because the deceased received nursing home benefits — who needs to understand the actual recovery rules, that MassHealth can only recover from the probate estate, and which hardship waivers may apply

- The small estate administrator dealing with personal property under $25,000 who cannot justify $3,000 to $5,000 for a probate attorney — who needs step-by-step guidance on the $115 Voluntary Administration process that can be completed in weeks, not months

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across the Massachusetts Court System website, the Department of Revenue, the Registry of Motor Vehicles, MassHealth, funeral home aftercare pages, and a dozen federal agency portals that do not reference each other. Here is what you actually encounter when you try to settle a Massachusetts estate using free sources alone:

- Mass.gov gives you raw forms and tells you nothing about the sequence. The Massachusetts Court System provides downloadable MPC forms — MPC 170 for Voluntary Administration, MPC 162 for Heirs at Law, MPC 854 for Inventory. But every page exists in isolation. There is no chronological workflow connecting the Probate Court to the Department of Revenue to the RMV to MassHealth. You get the puzzle pieces without the picture on the box — raw paperwork without instructions telling you which office to call first, which forms to file before others, and which ones to ignore entirely for your situation.

- Massachusetts probate law firms write blog posts designed to sell $3,000-plus retainers. Firms like Generations Law Group and Spinnaker Probate produce excellent, detailed content on MUPC timelines, non-probate assets, and MassHealth recovery. Every article is designed to convince you the process is too dangerous to attempt without representation. They intentionally omit the procedural how-to so you book a consultation. For contested estates and complex trusts, professional representation is essential. For the majority of straightforward estates, the answer costs a fraction of a retainer.

- National platforms miss Massachusetts-specific details that cause real harm. Trust & Will, Nolo, and EZ-Probate offer polished overviews of probate. They consistently fail to accurately address the $2 million state estate tax threshold, the automatic DOR lien on real property, the distinction between Recorded Land and Registered Land, the three-tier MUPC probate structure, and the specific MassHealth hardship waivers. Massachusetts is not a footnote — it has one of the lowest estate tax thresholds in the nation, and generic tools miss that entirely.

- Local funeral homes give you surface-level checklists for the first 72 hours. They tell you to "notify the bank" and "contact Social Security." They do not mention the Section 3-805 debt priority, the $2 million estate tax threshold, the Land Court distinction for real property, or the MassHealth recovery rules. Their advice ends where the hard questions begin.

Free resources give you fragments from a dozen sources that do not reference each other. The MUPC Triage System puts every Massachusetts-specific statute, form, deadline, and procedure into one document, in the order you actually need them.

— Less Than Fifteen Minutes With a Massachusetts Probate Attorney

A single consultation with a Massachusetts probate attorney costs $250 to $400 per hour. Standard probate representation runs $3,000 to $5,000 as a flat fee. National estate software platforms charge $149 or more per year in recurring subscription fees. This guide costs less than fifteen minutes of professional legal time and gives you the complete Massachusetts-specific roadmap — every statute, every deadline, every form, and the decision trees that tell you whether you even need an attorney at all.

Your download includes 8 PDFs: the complete guide, the First 48 Hours Checklist, and six standalone reference sheets — the MUPC Probate Tier Decision Tree, the Estate Tax and DOR Lien Reference, the MassHealth Recovery and Hardship Waiver Guide, the Creditor Priority Reference, the Statutory Deadline Calendar, and the Vehicle Title Transfer Reference. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on what to do next and confidence that you are doing it in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Massachusetts First 48 Hours Checklist — covering everything that must happen in the first two days after a death in Massachusetts: death certificates, securing the home, notifying Social Security, what not to pay, and what to gather. It is enough to get through tonight and tomorrow.

You did not ask for this job. But you can do it. The guide shows you how, one step at a time.