Someone You Love Died in Minnesota. Now You Have Three Separate Tax Returns to File, a $3 Million Estate Tax Cliff That Nobody Warned You About, and a 90% Payment Rule That Triggers Penalties Before the Filing Deadline Even Arrives.

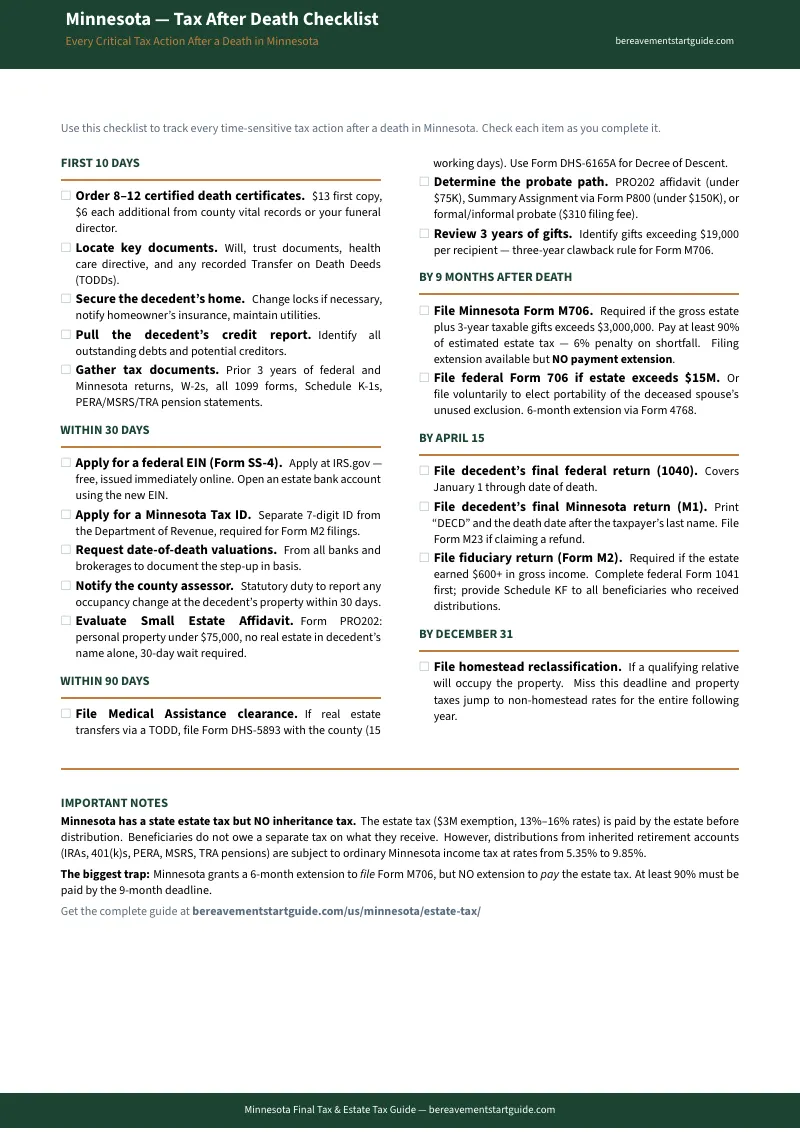

The funeral director handled the death certificate. The bank froze the accounts. And now the real administrative nightmare begins: the Minnesota Department of Revenue expects a final income tax return for the year of death. If the estate earned more than $600 in bank interest or rental income during administration, they want a second return — the fiduciary income tax on Form M2. And if the total estate, including any gifts over $19,000 per recipient made in the last three years, exceeds $3,000,000, they want a third return — Form M706, the Minnesota estate tax — with 90% of the estimated tax paid within nine months of the death. No extension on the payment. Just a 6% penalty on whatever you underpay.

Meanwhile, the federal government has its own parallel set of forms. The surviving spouse is asking about the step-up in basis on the family cabin. An out-of-state sibling wants to know if Minnesota has an inheritance tax. The county assessor needs to be notified before December 31 or the property taxes will jump to non-homestead rates. And you just discovered that Minnesota does not allow portability between spouses — meaning the deceased's unused $3 million exemption vanishes permanently if the estate plan was not structured correctly.

The Minnesota Final Tax & Estate Tax Guide is a Complete Tax Clearing System for every filing obligation between the date of death and the final estate closing letter. Not a generic national overview that mentions Minnesota in a footnote. Not a law firm blog post designed to sell a $4,500 retainer. A structured, 18-chapter manual built around Minnesota Statutes, Department of Revenue procedures, and the specific forms, thresholds, and deadlines that make Minnesota estate taxation fundamentally different from every other state.

What's Inside the Tax Clearing System

A comprehensive 18-chapter guide with appendices and a standalone Tax After Death Checklist — covering every tax obligation from the first death certificate through the final estate closing letter, built specifically for Minnesota's three-tax system and the state-specific rules that trip up executors who rely on generic federal guidance:

The Three Taxes Nobody Explained in One Place

Most families hear "the estate is under $3 million" and assume there are no tax obligations at all. That assumption is dangerously wrong. The final individual income tax (Form M1) is owed on income earned during the year of death — regardless of estate size. The fiduciary income tax (Form M2) is owed if the estate generates $600 or more in bank interest, dividends, rental income, or capital gains during administration — estate size is irrelevant. The estate tax (Form M706) is the only tax tied to the $3 million threshold. All three have different forms, different deadlines, and different payment rules. The guide separates them clearly so you know exactly which apply to your situation.

The Minnesota Estate Tax: $3 Million Threshold With No Spousal Portability

This is what makes Minnesota different. The federal estate tax exemption is $15 million. Minnesota's is $3 million — one-fifth of the federal threshold. Progressive rates run from 13% to 16% on the excess. And unlike the federal system, Minnesota does not allow a surviving spouse to capture the deceased spouse's unused exemption. If the first spouse leaves everything outright to the survivor, that $3 million exemption is permanently gone. The guide walks through the rate brackets, the three-year gift clawback rule that adds deathbed gifts back into the estate, the qualified farm and small business deduction that can shield up to $2 million in additional value, and the planning implications for married couples whose combined assets sit anywhere near the threshold.

The 90% Payment Rule: The Deadline Trap

Minnesota grants a six-month extension to file Form M706. It grants no extension to pay the tax. At minimum, 90% of the estimated estate tax must be remitted by the nine-month deadline. Fall below 90% and you trigger a 6% late payment penalty on the shortfall, plus accruing interest. The guide explains the safe harbor strategy: overestimate, overpay by the nine-month deadline, and claim a refund of any excess when you file the final return. Most executors learn about the 90% rule after the penalty hits.

Filing the Final Income Tax Return (Form M1)

The decedent's last Minnesota income tax return captures all income from January 1 through the date of death. The guide covers the joint filing option for surviving spouses, the requirement to print "DECD" and the date of death after the taxpayer's last name, the refund claim process using Form M23, and the Income in Respect of a Decedent rules that determine which income items go on this return and which go on someone else's.

The Fiduciary Income Tax (Form M2): The $600 Threshold Most Families Miss

If the estate earns $600 or more in gross income assignable to Minnesota during administration — bank interest, stock dividends, rental income from inherited property, capital gains from selling assets — the executor must file Form M2. The guide covers the fiscal year election, the relationship between federal Form 1041 and Minnesota Form M2, the Schedule KF that each beneficiary needs for their personal return, and the six-month automatic extension.

The Step-Up in Basis: Thousands in Capital Gains Tax You Do Not Have to Pay

When you inherit property, the tax basis resets to fair market value on the date of death. A cabin purchased 30 years ago for $50,000 and now worth $400,000 has a new basis of $400,000 — sell it immediately and the capital gain is zero. But Minnesota is a common-law property state, not a community property state. For jointly owned property, only the decedent's half receives the step-up. The guide includes concrete numerical examples for Minnesota cabin property, explains which assets do and do not receive a step-up (retirement accounts do not), and covers the joint property rule that surviving spouses need to understand before selling the family home.

Medical Assistance Recovery: The Lien That Follows the Deed

If the deceased received long-term care through Minnesota's Medical Assistance program, the state can recover those costs from the estate. This applies to property transferring through probate, Transfer on Death Deeds, and Decrees of Descent. The guide covers the clearance certificate process, Form DHS-5893 for TODDs, Form DHS-6165A for Decrees of Descent, and what to do when the clearance certificate comes back showing a substantial claim against the family home.

Property Tax: The December 31 Deadline That Creates a Year of Higher Taxes

When the homeowner dies, the property loses its homestead classification unless a qualifying relative files for reclassification with the county assessor before December 31. Miss that deadline and the property is assessed at non-homestead rates for the entire following year — a significant tax increase that cannot be reversed until the next assessment cycle. The guide explains who qualifies as a relative, the homestead market value exclusion, and the Class 1b disability classification that expires immediately upon death.

Public Pensions: PERA, MSRS, and TRA Survivor Benefits

Minnesota has a large public employee workforce, and pension survivor benefits are among the most common assets beneficiaries receive. The tax treatment is more complex than most families expect — involving the IRS Simplified Method for calculating the taxable portion and a Minnesota-specific Qualified Public Pension Subtraction that can reduce state income tax. The guide covers both, including which pension plans qualify for the subtraction and the income phase-out thresholds.

Selling Inherited Real Estate

Many families need to sell inherited property to distribute proceeds among beneficiaries. The guide covers the stepped-up basis calculation, the Minnesota State Deed Tax (0.33% of the sale price, with additional Environmental Response Fund taxes in Hennepin and Ramsey counties), the requirement to clear property taxes and Medical Assistance liens before closing, and the reporting obligations for capital gains on the estate's fiduciary return or the beneficiary's individual return.

The Complete Tax Deadline Timeline

Every deadline in one chapter: death certificates immediately, county assessor within 30 days, the final M1 by April 15, the M706 with 90% payment at nine months, the M2 by the fourth month after the fiscal year close, and the homestead reclassification by December 31. The guide consolidates all of them into a single chronological table so you can plan months ahead rather than scrambling at each deadline.

Who This Guide Is For

- The executor who just learned there are three separate tax returns to file — and that the deadlines, forms, and payment rules are completely different for each one. You need the sequence, not just the forms.

- The surviving spouse trying to understand the step-up in basis on jointly owned property — because the cabin, the house, and the brokerage account all follow different rules, and the common-law property state calculation is not what you assumed.

- The out-of-state adult child managing a parent's Minnesota estate — who needs every tax obligation, every form number, and every deadline in one document instead of scattered across the Department of Revenue, the IRS, and three county offices.

- The family who assumed "under $3 million" meant no tax work — who just discovered that the final income tax and fiduciary income tax are owed regardless of estate size, and that retirement account distributions are taxed as ordinary income to the beneficiary.

- The executor of a $3M+ estate facing the Minnesota estate tax cliff — who needs to understand the rate brackets, the three-year gift clawback, the 90% payment safe harbor, and the no-portability rule before the nine-month deadline arrives.

- The family worried about Medical Assistance liens on the family home — who needs the actual clearance certificate process, the specific forms, and the timeline before transferring any real estate.

Why Free Resources Will Not Get You Through This

The Minnesota Department of Revenue hosts Forms M1, M2, and M706. The Minnesota Judicial Branch provides probate forms. The Department of Human Services handles Medical Assistance clearances. Here is what you encounter when you try to navigate Minnesota's post-death tax obligations using free sources alone:

- The Department of Revenue provides the forms but does not explain the sequence. Forms M1, M2, and M706 each have their own instructions, but none of them explain how the three interact, which must be completed first, or how income from inherited retirement accounts flows between the decedent's final return and the beneficiary's return. They give you the puzzle pieces without the picture on the box.

- National tax software handles the federal side but misses Minnesota's specifics. TurboTax and H&R Block walk you through Form 1040 and sometimes Form 1041, but they do not explain the $3 million state estate tax cliff, the no-portability rule, the three-year gift clawback, or the 90% payment trap. Minnesota is not a footnote — it has structural differences that generic software does not address.

- Law firm blog posts are designed to sell $400/hour consultations. Local probate and estate planning attorneys produce accurate content that carefully stops short of actionable instructions. Every article ends with "Contact us for a consultation." For estates with contested wills or complex trusts, they are right. For straightforward estates with clear heirs and known assets, paying a $4,500 retainer to organize paperwork is buying organization you can build yourself.

- Legal aid organizations cover single topics without connecting them. LawHelpMN provides excellent guides on Transfer on Death Deeds or Small Estate Affidavits, but each guide exists in isolation. None of them integrate the tax obligations, the probate path, the Medical Assistance clearance, and the property tax reclassification into a single chronological workflow.

Free resources give you fragments from a dozen agencies that do not reference each other. The Tax Clearing System puts every Minnesota-specific tax form, deadline, threshold, and procedure into one document, in the order you actually need them.

— Less Than Four Minutes With a Minnesota Estate Attorney

A single hour with a Minnesota probate or estate attorney costs $326 to $495. A flat-fee engagement for estate tax filing starts around $4,500. National estate software charges $100 to $200 per year. This guide costs less than four minutes of professional legal time and gives you the complete Minnesota-specific tax roadmap — every form, every threshold, every deadline, and the decision framework that tells you whether your estate even owes state tax at all.

Your download includes five PDFs: the complete 18-chapter guide with appendices, the standalone Minnesota Tax After Death Checklist, a one-page Tax Deadline Timeline with fill-in dates, a Forms & Numbers Quick Reference card listing all 16 official forms and 30 key financial thresholds, and a Probate Path Decision Guide for choosing the right court process based on your estate's asset profile. Every tool you need to clear the estate's tax obligations with confidence. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on which tax returns your estate must file and confidence that you are meeting every Minnesota deadline, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Minnesota Tax After Death Checklist — a printable timeline covering the three tax returns, the key thresholds ($600 for M2, $3 million for M706), the payment deadlines, and the property tax reclassification cutoff. Enough to map out what you owe and when, starting tonight.

You did not create this situation. But the tax obligations are finite, the deadlines are knowable, and the forms have right answers. The guide shows you how to clear every one of them, one step at a time.