You Were Just Named Personal Representative in Minnesota. The Court Registrar Needs Forms You Have Never Seen. The Estate Might Qualify for a Small Estate Affidavit That Skips Probate Entirely. And Nobody Mentioned That Minnesota Has Its Own Estate Tax Starting at $3 Million — With No Spousal Portability.

You did not plan for this. Maybe you were named in the will. Maybe there was no will and the family decided you are the one who handles things. Either way, the funeral is barely over and the bank already froze the accounts. They want something called "Letters Testamentary" before they will release a dollar. The county court has a packet of blank forms — PRO802, PRO902, PRO912 — but the Self-Help Center staff are legally prohibited from telling you which ones to file, in what order, or what happens if you get it wrong. Your brother is asking about the house. And you just discovered that if the deceased received Medical Assistance for nursing home care, the state can attach a lien that survives for up to 20 years — even on joint tenancies and life estates.

Welcome to Minnesota probate. Not one process, but four possible paths — a Small Estate Affidavit, Summary Proceedings, Informal Probate through a registrar, or Formal Probate before a judge — each with its own thresholds, forms, and consequences for choosing wrong. The court clerk has the paperwork but cannot advise you. Local probate attorneys will gladly help, at $150 to $400 per hour, with total fees routinely running $3,000 to $10,000 for straightforward estates.

The Minnesota Probate Process Guide is a Four-Path Probate Navigation System for every procedural step between the death certificate and the final distribution order. Not a law textbook. Not a generic probate overview that treats Minnesota like every other state. A structured, Minnesota-specific manual built around MN Statutes Chapter 524 and the county-level procedures of all 87 district courts — covering the exact forms, the exact deadlines, the exact fee schedules, and the exact decision points that determine whether this takes 3 months or 18.

What's Inside the Four-Path Probate Navigation System

A comprehensive 15-chapter guide, 4 appendices, and a Quick-Start Probate Checklist — covering every stage from locating the will through closing the estate, built specifically for Minnesota's multi-path probate system, the Uniform Probate Code framework, and the state-specific rules that make probate here different from any other state:

Do You Actually Need Probate? The Decision Flowchart

Before you file a single form, you need to know whether probate is even necessary. Joint accounts, POD/TOD accounts, life insurance proceeds, trust assets, Transfer-on-Death Deed real estate, and vehicles with TOD beneficiaries all pass outside probate. The guide walks through an asset-by-asset classification table so you can identify which assets require court involvement and which transfer automatically. Many families go through the full process because nobody showed them the shortcut.

The Small Estate Affidavit: Skipping Probate Entirely

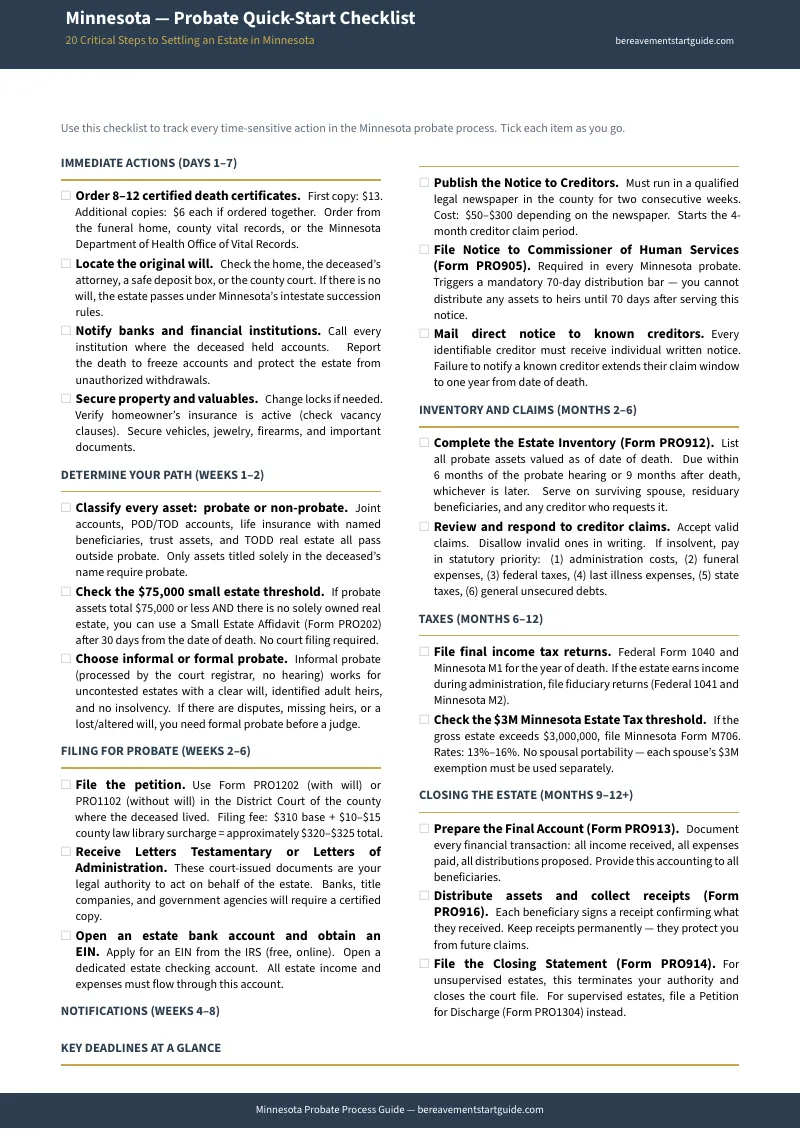

If the probate assets total $75,000 or less and there is no solely owned real estate, you can bypass the court system entirely using a Small Estate Affidavit (Form PRO202). Wait 30 days from the date of death, prepare the notarized affidavit, present it with a certified death certificate at each institution — and the bank is legally required to release the funds. No filing fees. No court hearings. No attorney required. But one overlooked detail disqualifies you: a single piece of real estate, even a $30,000 vacant lot, forces you into probate regardless of total estate value. The guide covers the exact eligibility criteria and what to bring to the bank window.

Informal vs. Formal Probate: Choosing the Right Track

Minnesota's Uniform Probate Code gives you a choice most states do not offer. Informal probate runs through a court registrar with no hearing, no judge, and minimal oversight — ideal for uncontested estates with a clear will and identified adult heirs. Formal probate puts a judge in the room, required when there are missing heirs, a lost or altered will, insolvency, distributions to minors, or any active disagreement. The guide explains the disqualifying factors for informal probate — including county-specific registrar requirements in Hennepin and Ramsey that trip up applicants over technicalities like improper will markings or unfiled renunciations.

Filing the Petition: Every Form, Every Fee, Every Step

Filing for probate is not one form — it is a sequence. Form PRO1202 if there is a will, PRO1102 without one. The Acceptance of Appointment (PRO902). The filing fee of $310 base plus $10–$15 county law library surcharge. The EIN application from the IRS. The estate bank account. The guide walks through each component in order, tells you which county to file in, and explains the bond requirement — including when you can waive it and when you cannot.

The Creditor Notification Process

Minnesota mandates that you publish a Notice to Creditors in a qualified legal newspaper for two consecutive weeks. This starts a strict 4-month window — creditors who do not file within that window are permanently barred. But there is a second notice most executors forget: Form PRO905, the mandatory notice to the Commissioner of Human Services, which triggers a 70-day distribution bar. You cannot distribute a single dollar to heirs until those 70 days expire. Fail to serve it and you have personal liability if the state later asserts a Medical Assistance claim. The guide covers both notices, the timeline math, and what to do when creditor claims arrive.

Building the Estate Inventory

Every probate asset must be valued as of the date of death and cataloged on Form PRO912. Deadline: 6 months after the probate hearing or 9 months after death, whichever is later. The guide covers what goes on the inventory, what stays off (non-probate assets), how to get date-of-death valuations for bank accounts, real estate, and vehicles, and who must receive a copy — surviving spouse, all residuary beneficiaries, and any creditor who requests it.

Surviving Spouse and Family Protections

Minnesota law gives the surviving spouse specific protections that override the will. The homestead passes by descent. Exempt personal property up to $15,000 can be claimed. One automobile transfers regardless of its value. The family maintenance allowance provides living expenses during administration. The elective share gives the surviving spouse a statutory minimum that cannot be circumvented. The guide explains each protection, the forms required to claim them, and how they interact with the estate tax and Medical Assistance recovery.

Managing Creditor Claims: The Priority Rules

When the estate cannot pay all its debts, Minnesota law dictates a strict priority: (1) administration costs and attorney fees, (2) reasonable funeral expenses, (3) federal taxes, (4) medical expenses of the last illness, (5) state taxes, (6) general unsecured debts. Pay a lower-priority creditor before a higher-priority one and you are personally liable for the difference. The guide covers the priority hierarchy, how to accept or disallow claims in writing, and the timeline for each.

The Minnesota Estate Tax: The $3 Million Cliff

Minnesota imposes its own estate tax on gross estates exceeding $3,000,000 — dramatically lower than the federal exemption of approximately $15 million. Rates range from 13% to 16%. And unlike the federal system, Minnesota does not allow portability between spouses. If the first spouse dies with an unused exemption, it is lost permanently. The guide explains the exemption, the rate brackets, the Form M706 filing requirements, and the planning strategies that apply when an estate approaches the threshold.

Medical Assistance Estate Recovery: Zombie Liens

This is the chapter that could save the surviving family thousands. If the deceased was 55 or older and received Medical Assistance for nursing home or long-term care, the Minnesota Department of Human Services can file a recovery claim against the estate. Minnesota's recovery program goes beyond the federal minimum — the state can pursue claims against life estates, joint tenancies, and survivor arrangements. These "zombie liens" can attach to property the family assumed was protected and persist for up to 20 years. The guide explains the actual recovery rules, the exemptions for surviving spouses and dependents, the hardship waiver process, and the 70-day distribution bar that protects you from distributing assets prematurely.

Transferring Real Estate: Torrens vs. Abstract

Minnesota has a dual property registration system that exists almost nowhere else. Torrens-registered property — common in Hennepin and Ramsey counties — transfers through the Examiner of Titles, not the standard county recorder process. If you file the wrong way, the title transfer will be rejected. The guide covers both systems: Abstract property (file a Personal Representative's Deed with the county recorder) and Torrens property (file through the Examiner of Titles office with Form 52.09 and additional certificates). Plus Transfer-on-Death Deeds, the homestead transfer process, and what happens when the house needs to be sold during administration.

Transferring Vehicles

Surviving spouses get an expedited path: present the death certificate and marriage certificate at a DVS office to transfer the title without probate. Everyone else needs Letters Testamentary or Letters of Administration, the original title, and Form PS2000. The guide covers every scenario — spouse transfer, probate transfer, small estate affidavit transfer, and vehicles with existing TOD beneficiary designations.

Final Accounting, Distribution, and Closing

The Final Account (Form PRO913) documents every transaction — income received, expenses paid, distributions proposed. Every beneficiary gets a copy. Each beneficiary signs a receipt (Form PRO916). Then the Closing Statement (Form PRO914) for unsupervised estates, or a Petition for Discharge (PRO1304) for supervised ones. Once filed and the statutory period passes without objection, you are discharged from fiduciary liability. The guide walks through each closing document and the timeline for each.

When You Need a Lawyer and When You Do Not

This chapter is honest. Contested wills, insolvent estates, Medical Assistance recovery disputes, Torrens property transfers, business interests, distributions to minors, and estates above the $3M tax threshold require professional help. For uncontested estates with adult heirs and straightforward assets, the guide is built to get you through the process independently. And for everything in between, it helps you walk into the attorney's office organized — so you are paying for legal judgment, not for someone to sort your paperwork.

Who This Guide Is For

- The executor who just got turned away at the bank trying to access the deceased's checking account — who needs Letters Testamentary from the district court but does not know which forms to file, whether the estate qualifies for the small estate affidavit, or whether informal probate through the registrar is even an option

- The family member handling a small estate who needs to know whether the $75,000 affidavit threshold applies, what the 30-day waiting period means, and exactly what documents to bring to the bank — because one missing piece means another trip and another week of waiting

- The surviving spouse trying to protect the homestead who needs to understand the exempt property allowance, the family maintenance provision, and whether Medical Assistance recovery can reach assets that were held jointly or in a life estate

- The out-of-state adult child named personal representative for a parent who died in Minnesota — who needs the complete sequence of fiduciary duties, forms, and deadlines in one document so they can manage the process without repeated trips to the courthouse

- The executor facing the $3M estate tax cliff who just discovered Minnesota's exemption is a fraction of the federal threshold and that unused spousal portability does not exist — who needs to understand Form M706, the rate brackets, and the planning implications before filing

- The family terrified of Medical Assistance recovery who heard "the state will take the house" because the deceased received nursing home benefits — who needs to understand the actual zombie lien rules, the hardship waiver, the spousal exemption, and which assets are genuinely at risk

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across the Minnesota Judicial Branch website, county-specific court packets, the Department of Human Services, the Department of Revenue, DVS, and a dozen federal agency portals. Here is what you encounter when you try to navigate Minnesota probate using free sources alone:

- The Minnesota Judicial Branch gives you forms but is legally prohibited from telling you what to do with them. The Self-Help Center provides blank PDFs — PRO802, PRO902, PRO912, PRO914 — without instructions on which form applies to which situation, what order to file them in, or how the county-specific rules in Hennepin or Ramsey differ from the statewide defaults. They hand you the pieces without the sequence.

- Minnesota probate law firms write content designed to sell $150-to-$400-per-hour retainers. Local firms produce accurate blog posts that carefully omit the procedural how-to. Every article ends with a "Contact Us" button. For contested estates, they are right — you need an attorney. For straightforward, uncontested estates, paying $3,000 to $10,000 is buying organization you can build yourself.

- LawHelpMN provides generalized fact sheets that do not sequence the process. Their content is accurate but academic — focused on eligibility and definitions rather than step-by-step execution. No checklists, no decision trees, no way to track your progress through a 12-month timeline.

- National platforms miss the details that make Minnesota different. Nolo, FindLaw, and similar sites consistently fail to cover the four-path system, the $3M estate tax cliff with no portability, the aggressive Medical Assistance zombie lien program, the Torrens vs. Abstract property distinction, and the 70-day distribution bar triggered by Form PRO905. Minnesota is not a footnote — it has structural differences that generic guides miss entirely.

Free resources give you fragments from a dozen sources that do not reference each other. The Four-Path Probate Navigation System puts every Minnesota-specific statute, form, deadline, and procedure into one document, in the order you actually need them.

— Less Than Fifteen Minutes With a Minnesota Probate Attorney

A single consultation with a Minnesota probate attorney costs $150 to $400 per hour. Full representation runs $3,000 to $10,000 for straightforward estates — and significantly more when real estate, estate tax, or Medical Assistance recovery is involved. National estate software charges $100 to $150 per year in recurring subscriptions. This guide costs less than fifteen minutes of professional legal time and gives you the complete Minnesota-specific roadmap — every path, every form, every deadline, and the decision trees that tell you whether you even need an attorney at all.

Your download includes the complete 15-chapter guide with 4 appendices, the standalone Minnesota Probate Quick-Start Checklist, and 9 printable reference tools — the Probate Path Decision Flowchart, Asset Classification Table, Small Estate Affidavit Eligibility Checklist, Creditor Notification Timeline, Estate Inventory Worksheet, Minnesota Estate Tax Reference, Medical Assistance Recovery Guide, Real Estate Transfer Checklist (Torrens and Abstract), and Vehicle Transfer Reference. Every tool you need to walk into the district court with confidence. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on which probate path your estate follows and confidence that you are filing the right forms in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Minnesota Probate Quick-Start Checklist — a printable 20-step action list covering death certificates, securing the estate, determining your probate path, filing for appointment, and the critical deadlines for the first 90 days. Enough to get started tonight.

You did not ask for this job. But the process is knowable, the forms are finite, and the deadlines are clear. The guide shows you the path through it, one step at a time.