Your Attorney Charges $300 an Hour to Organize What You Already Have. The Mississippi Department of Revenue Publishes Forms Designed for CPAs. The IRS Covers Federal Filings and Nothing Else. And Nobody Told You the Estate Itself Owes Income Tax on Every Dollar of Rent and Dividends Earned While Sitting in Chancery Court.

Someone died in Mississippi, and now you are the person responsible for their taxes. You have been told Mississippi has no death tax, so you assumed the tax side was handled. Then you discovered that the estate earned rental income from an inherited property and dividends from a brokerage account during the months it took Chancery Court to process the paperwork --- and that income must be reported on a Mississippi Fiduciary Income Tax Return you did not know existed. You also learned that filing the deceased's final state income tax return requires an attached death certificate, a completed federal Form 1310, and potentially a Statement of Heirship to claim a refund --- none of which was mentioned by the government website that told you Mississippi eliminated its estate tax in 2005.

Meanwhile, the Mississippi Department of Revenue publishes Form 80-105 and Form 81-110 with instructions written for tax professionals, not for grieving family members filing for the first time. CPA firm blogs in Jackson and Gulfport give you enough information to realize you need help, then invite you to schedule a $200-per-hour consultation. Chancery Court requires you to retain an attorney under Rule 6.01, but the attorney assumes you have already gathered and classified every financial document before the first meeting. And no single source connects the federal filing requirements, the state filing requirements, the Chancery Court administrative deadlines, and the creditor notification timeline into one sequence you can actually follow.

The Mississippi Final Tax & Estate Tax Guide is a Chancery Court Tax Roadmap for every tax obligation that follows a death in Mississippi --- from the immediate EIN application through the final estate closure. Not a tax preparation manual. Not a substitute for a CPA or attorney. A structured, Mississippi-specific framework that tells you which forms apply, which deadlines you cannot miss, which documents to gather from the deceased's home, and how to organize everything so your CPA prepares returns and your attorney files petitions --- instead of billing you $300 an hour to inventory what you should have brought to the first meeting.

What's Inside the Chancery Court Tax Roadmap

A comprehensive guide plus a quick-start checklist --- covering every tax obligation, every form, every deadline, and every document-gathering step that Mississippi executors, surviving spouses, administrators, and beneficiaries face after a death:

Mississippi's Tax Landscape --- The Relief You Need to Hear First

The single most important fact for most Mississippi families: Mississippi repealed its estate tax in 2005 and imposes a 0% inheritance tax. Beneficiaries owe the Mississippi Department of Revenue nothing for receiving inherited assets. This section confirms what you can stop worrying about --- and immediately redirects your attention to the obligations that remain: the final income tax return, the fiduciary income tax return, federal estate tax thresholds, and the capital gains exposure on inherited property.

Federal Estate Tax --- The $15 Million Decision Tree

The One Big Beautiful Bill Act permanently set the 2026 federal exemption at $15 million per individual. If the gross estate is under that threshold, no Form 706 is needed for tax purposes. But surviving spouses face a critical decision: filing Form 706 anyway to capture the deceased spouse's unused $15 million exemption through portability --- creating a $30 million future shield. The decision flowchart, the asset inventory worksheet, and the deadline for the portability election.

Filing the Final Individual Tax Return (Form 80-105)

The deceased's tax year ends on the date of death. Which Mississippi form to use for residents (Form 80-105) and non-residents (Form 80-205), the April 15 deadline, the extension rules, joint return rules for surviving spouses, and the critical requirement to attach a completed federal Form 1310 and an official death certificate. The specific steps for claiming a state tax refund using the Statement of Heirship (Form 80-699) when the refund is under $500 --- which lets the family bypass formal court involvement for that specific asset.

Estate Income Tax --- Mississippi Form 81-110

The estate becomes a separate taxable entity at death. If it earns any income during the administration period --- rent from an inherited house, dividends from a brokerage account, interest from a bank account --- that income must be reported on Form 81-110. This section covers how the state return uses the federal Form 1041 as its starting reconciliation point, the requirement to attach a complete copy of the federal return and all Schedule K-1s, and the filing deadline on the fifteenth day of the fourth month following the close of the estate's fiscal year. The trap most executors miss: income earned by the estate during probate is not automatically covered by the deceased's final return.

Step-Up in Basis --- The Capital Gains Shield

Inherited assets receive a basis adjustment to fair market value at the date of death. A Mississippi farm purchased decades ago for $40,000 and worth $350,000 at death has a new basis of $350,000 --- selling immediately means zero capital gains. But holding the property and selling later means only post-death appreciation is taxable. Why date-of-death appraisals are non-negotiable, and how to document the basis adjustment for the IRS.

The Small Estate Affidavit --- Bypassing Chancery Court

Under Mississippi Code Section 91-7-322, estates with personal property valued under $75,000 can transfer assets without formal court administration --- provided thirty days have elapsed since death and no personal representative has been appointed. The threshold was increased from $50,000 to $75,000 in 2020, expanding the number of families who qualify. The requirements, the statutory language, and the worksheet for determining whether the estate meets the threshold by separating probate assets from non-probate assets (life insurance, joint accounts, and payable-on-death designations do not count toward the cap).

Muniment of Title --- Transferring Real Estate Without Full Probate

When the deceased died with a valid will and the personal estate is valued under $10,000 (excluding exempt property), Mississippi law allows real property to transfer through a Muniment of Title --- without opening a full probate administration. The strict qualifying criteria, the Chancery Court filing procedure, and the worksheet for determining whether the estate qualifies.

Spousal Protections Unique to Mississippi

Mississippi law provides surviving spouses with protections that override the will. The widow's or widower's allowance for one year of financial support determined by court-appointed appraisers. The absolute right to occupy the homestead regardless of who inherits the property title --- meaning a surviving spouse cannot be legally displaced from the family home even if it was willed to someone else. The right to elect against the will and claim up to 50% of the estate. The timelines for exercising these rights and the Chancery Court procedures for each.

Creditor Claims and the 90-Day Window

After the executor publishes notice in a local newspaper, creditors have exactly 90 days to file claims against the estate. The required publication format, the three consecutive weekly publications, and the strategic timing: publishing early starts the clock so the estate can close sooner. The executor's personal liability for distributing assets before this window closes and before satisfying the federal priority statute.

Medicaid Estate Recovery

The Mississippi Medicaid Estate Recovery Program requires the state to seek recovery from estates of deceased recipients who were 55 or older and had assets valued at $5,000 or more. The statutory exemptions --- surviving spouse, child under 21, blind or disabled child, or a sibling with an equity interest who lived in the home for at least one year before the decedent entered the nursing facility. The notification procedure and the timeline for responding.

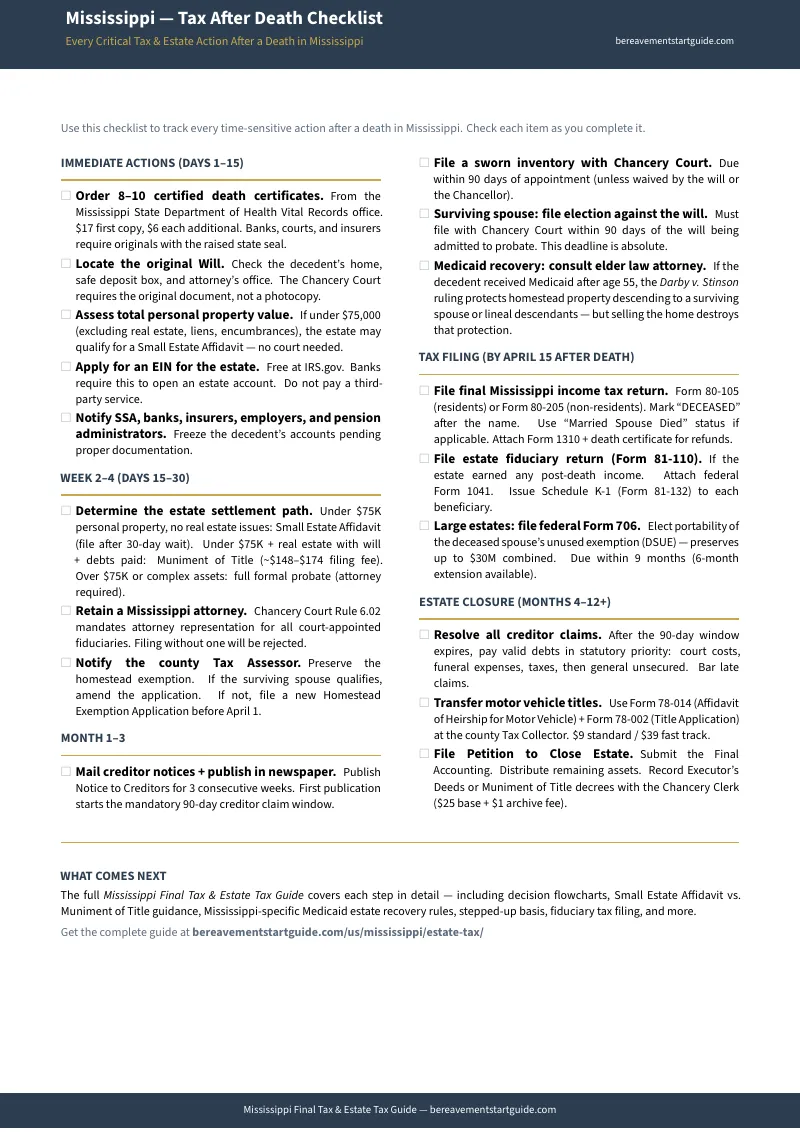

Plus: Mississippi Tax After Death Checklist

A standalone quick-start reference organized by timeframe --- immediately after death, within 30 days, within 90 days, by April 15, and ongoing until the estate closes. Every deadline, every form number, every action item. Enough to start immediately, even before reading the full guide.

Plus: Printable Standalone Tools

Every worksheet, reference card, and decision tree you need --- extracted from the guide so you can print them separately and use them at the kitchen table, at the CPA's office, or at the attorney's conference room:

- Master Deadline Calendar --- Every filing deadline with checkboxes, organized chronologically from the immediate EIN application through final estate closure. Pin it to the wall.

- CPA Document Checklist --- The complete document list organized by category. Bring this to your CPA meeting with everything checked off --- so they spend their time preparing returns, not inventorying what you brought.

- Form Decision Tree --- Visual flowchart for determining which Mississippi and federal forms apply: Form 80-105 vs. Form 81-110, Form 80-699 refund claims, and Form 706 portability elections.

- Step-Up in Basis Worksheet --- Fillable tracker for the basis adjustment on inherited assets, with date-of-death appraisal documentation fields.

- Small Estate Affidavit Worksheet --- Asset classification worksheet to determine whether the estate qualifies under the $75,000 threshold by separating probate from non-probate assets.

- Spousal Rights Reference Card --- One-page summary of the widow's allowance, homestead occupancy right, and elective share --- the three Mississippi-specific protections most out-of-state executors do not know exist.

Who This Guide Is For

- The executor who just learned the estate owes a fiduciary tax return --- you were told Mississippi has no death tax, so you assumed the tax side was finished. Then the estate earned rental income from an inherited house and dividends from a brokerage account, and now you need Form 81-110 and the federal Form 1041 --- two returns you had never heard of before this month. The guide walks you through both, step by step, with the document list your CPA needs.

- The surviving spouse trying to protect the family home --- you know you have a right to stay in the house, but the will names someone else as the owner. The guide explains your absolute homestead occupancy right under Mississippi law, your widow's allowance, and your option to elect against the will for up to 50% of the estate --- with the Chancery Court procedures and deadlines for each.

- The adult child managing a parent's estate from out of state --- you live in Texas or Georgia and are dealing with Mississippi's Chancery Court system for the first time. You do not know the local rules, the required attorney representation, or the specific protections that Mississippi law provides to surviving family members. The guide translates the Chancery Court requirements into a sequence you can manage remotely.

- The family deciding whether they need Chancery Court at all --- the estate may be small enough to bypass formal probate entirely. The guide provides the worksheet to determine whether the $75,000 Small Estate Affidavit applies, or whether the $10,000 Muniment of Title pathway works for transferring real estate without opening a full administration.

- The family selling inherited property --- you want to sell the house and need to know your capital gains exposure. The step-up in basis determines whether you owe $0 or tens of thousands in taxes. But the title needs to be cleared through Chancery Court, and you need to understand how the Muniment of Title or formal probate affects the timeline for selling.

Why Free Resources Leave You Paying Your Attorney to Sort Paperwork

The information exists. It is spread across the Mississippi Department of Revenue, the IRS, Chancery Court local rules, Medicaid recovery notices, and a hundred attorney blog posts. Assembling it into a single actionable sequence --- while you are grieving and multiple deadlines are running simultaneously --- does not.

- IRS.gov covers federal tax forms. It does not cover Mississippi Form 81-110, the Statement of Heirship (Form 80-699), Chancery Court deadlines, or any Mississippi-specific procedure. It covers its own forms and nothing else.

- The Mississippi Department of Revenue publishes form instructions for tax professionals, not for executors handling this for the first time. No chronological workflow, no explanation of how state fiduciary returns interact with federal filings, no document-gathering protocol.

- CPA and attorney blogs in Jackson, Gulfport, and Hattiesburg give you enough information to realize you need help. The article ends with an invitation to schedule a $200-per-hour consultation. No standalone checklist, no chronological roadmap, no document list you can use independently.

- EstateExec and Atticus provide national overviews behind subscription paywalls. They will not tell you about the $75,000 Small Estate Affidavit threshold, the Form 81-110 reconciliation with Form 1041, the Muniment of Title requirements, or Rule 6.01's attorney requirement in Chancery Court.

- Better Chancery Practice --- the most authoritative Mississippi source --- is written for practicing attorneys, not for families. Dense legal commentary on courtroom procedures and case law updates, not a consumer-facing action plan.

Free resources answer one agency's questions. The Chancery Court Tax Roadmap answers them all --- in sequence, with deadlines, with the exact forms and documentation, and with the Mississippi-specific rules that no single agency, software platform, or blog post provides.

--- Less Than One Hour of Attorney Time

A Mississippi attorney charges $150 to $300 per hour for estate work. A CPA charges $120 to $250 per hour for fiduciary returns. The typical first meeting --- where the professional inventories what you brought and tells you what is missing --- costs $250 to $450 before any work begins. The guide costs a fraction of that first meeting and ensures you never need it.

Your download includes the complete guide, the Mississippi Tax After Death Checklist, and all standalone printable tools --- the deadline calendar, CPA document checklist, form decision tree, step-up worksheet, small estate affidavit worksheet, and spousal rights reference card. Print the standalone tools, use the checklist immediately, and work through the full guide section by section as each deadline approaches.

30-day money-back guarantee. If the guide does not give you a clear map of every tax obligation, every form, every deadline, and every document you need to gather --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Mississippi --- Tax After Death Checklist --- a summary of the most time-sensitive deadlines, form numbers, and action items that most executors do not discover until they are sitting in an attorney's office being billed for the information.

You did not plan to be the person handling the taxes for someone who died. But the April 15 filing deadline does not care, the creditor claims window is already running, and every hour your attorney or CPA spends organizing paperwork is an hour billed to the estate. This guide turns a fragmented, multi-agency maze into a single organized sequence --- so you walk into your first professional meeting prepared, not panicked.