PERS Says Submit Form 9A SRVR Through the Employer. The Employer Says Call PERS. The Bank Won't Release $800 Without a Court Order. And Nobody Mentioned the 30-Day Waiting Period That Determines Whether You Need Chancery Court at All.

Your spouse worked for a Mississippi school district for twenty-two years. The HR office handed you a packet about PERS survivor retirement benefits and said to submit Form 9A SRVR --- but the form has to go through the employer first, not directly to PERS, and nobody explained what happens after that. You called PERS and were told you have ninety days to return Form 14 once the pre-application is processed --- but you do not know when that clock starts or what happens to retroactive payments if you miss it.

Meanwhile, the funeral home sent a bill. You heard that Mississippi workers' compensation pays a $1,000 lump sum and up to $5,000 for burial expenses if the death was work-related --- but the employer's insurer has not returned your calls, and you have sixty days to file medical records before they can deny the claim outright. A neighbor mentioned the Small Estate Affidavit for accessing bank accounts without a lawyer, but only after a thirty-day waiting period --- and only if the personal property is under $75,000. You do not know whether the house counts. You went to the bank on day twelve and were turned away.

The Mississippi Survivor Benefits Navigator is a Chancery Court Bypass System built entirely around the Mississippi Code --- mapping every benefit, deadline, form number, and statutory threshold into one chronological roadmap. It diagnoses whether your estate qualifies for a statutory bypass or whether Uniform Chancery Court Rule 6.1 forces you to hire an attorney. It tells you which agencies to contact in which order so no benefit expires because nobody told you it existed.

What's Inside the Chancery Court Bypass System

A 17-chapter guide, a printable 30-day action checklist, and five standalone reference sheets --- covering every survivor benefit, probate shortcut, tax protection, and insurance transition available under Mississippi law:

Chapters 1-2: Vital Records and Immediate Triage

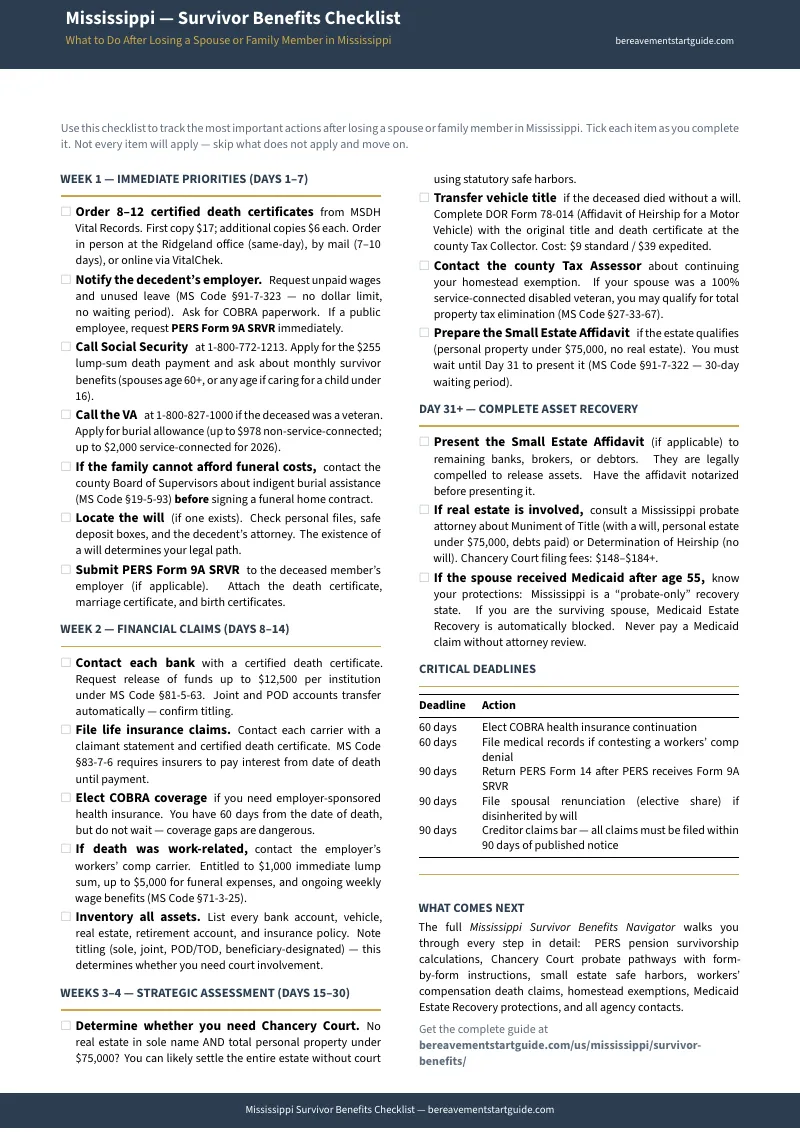

Where to order certified death certificates from MSDH ($17 first copy, $6 each additional), how many you actually need (8-12 minimum), and the day-by-day triage sequence for the first fourteen days. Which calls to make first: Social Security ($255 lump-sum death payment), the employer (unpaid wages under Section 91-7-323 --- no dollar limit, no waiting period), each bank (release of funds up to $12,500 per institution under Section 81-5-63), and the Chancery Clerk (homestead exemption verification). Securing vehicles, property, and safe deposit boxes before probate claims complicate access.

Chapter 3: Claiming Assets Without Court

Four statutory safe harbors that bypass Chancery Court entirely. The bank account release for accounts up to $12,500. The unpaid wages claim under Section 91-7-323 (hierarchy of payees: spouse first, then adult children, then parents --- and the sixty-day suit deadline if the employer refuses to pay). Motor vehicle title transfer via DOR Form 78-014. And the Small Estate Affidavit for personal property under $75,000 --- including the mandatory thirty-day waiting period under Section 91-7-322 that trips up nearly everyone who tries to use it too early. Real property is explicitly excluded from the threshold.

Chapter 4: Do You Even Need Chancery Court?

A three-question flowchart that tells you whether the estate qualifies for a statutory bypass or requires formal probate. Based on three variables: whether the estate includes solely-titled real estate, whether personal property exceeds $75,000, and whether the decedent left a will. If the flowchart sends you to court, you know exactly why. If it does not, you just saved a legal retainer.

Chapter 5: Formal Chancery Court Proceedings

When bypass options fail: filing in Chancery Court, current filing fees by county ($148-$184+), the difference between testate and intestate administration, and the mandatory attorney requirement under Uniform Chancery Court Rule 6.1 --- every fiduciary must be represented by counsel unless the fiduciary is an attorney themselves. The guide explains what this means for your estate and how to evaluate whether the retainer is justified before you sign it.

Chapter 6: Spousal Protections

The Widow's Allowance (one year of support from the estate under Section 91-7-135). The Elective Share and Mississippi's unique "one-fifth rule" under Section 91-5-29 --- if the surviving spouse's separate estate equals or exceeds their lawful portion of the decedent's estate, they are legally barred from renouncing the will. The ninety-day creditor claims bar and what it protects. How these rules interact when the will leaves you less than you expected.

Chapter 7: PERS Survivor Pension Benefits

The complete PERS process in plain English. Duty-related deaths (no vesting requirement, no marriage duration threshold) versus non-duty-related deaths (member must be vested, spouse must have been married to the member for at least one year immediately preceding the death). The two-phase application: Form 9A SRVR submitted through the employer first, then Form 14 within ninety days after the pre-application is received. Retroactive payment rules and the one-year cap. What happens if you miss the ninety-day Form 14 deadline.

Chapter 8: Workers' Compensation Death Benefits

The exact statutory payouts under Senate Bill 2576: $1,000 immediate lump sum to the surviving spouse, up to $5,000 for funeral expenses, and ongoing weekly wage benefits capped at 450 weeks. The sixty-day medical records filing deadline. Remarriage rules and how they affect ongoing payments. What to do when the employer's insurer disputes the claim and the Mississippi Workers' Compensation Commission schedules an administrative hearing.

Chapters 9-10: Federal Benefits and Life Insurance

Social Security: the $255 lump-sum death payment, monthly survivor benefits for spouses (age 60+, or age 50+ if disabled), the child-in-care exception, and earnings limit penalties. VA: Dependency and Indemnity Compensation, burial allowances, and national cemetery eligibility. How federal benefits interact with Mississippi PERS annuities. Life insurance: how to locate policies, file claims, and enforce Mississippi's interest-on-proceeds statute under Section 83-7-6. The creditor protection under Section 85-3-11 that keeps proceeds from being seized for the decedent's debts.

Chapters 11-12: Health Insurance and Property Tax

The sixty-day Special Enrollment Period triggered by a spouse's death. Federal COBRA versus marketplace options. Mississippi Medicaid eligibility and the estate recovery implications of applying. The Homestead Exemption and how it continues to the surviving spouse. The Tier 3 total exemption for unremarried spouses of totally disabled veterans under Section 27-33-75 --- complete elimination of property taxes on the homestead. Procedural steps and what to bring to the Chancery Clerk's office.

Chapter 13: Medicaid Estate Recovery

The biggest fear for Medicaid-vulnerable survivors, answered directly. Mississippi law requires the Division of Medicaid to waive estate recovery claims when there is a surviving spouse, a dependent child under 21, or a blind or disabled child of any age. The homestead protection established in Estate of Darby v. Stinson --- the Mississippi Supreme Court held that homestead property passing to a surviving spouse, children, or grandchildren is entirely exempt from Medicaid estate recovery. How to respond to a recovery notice from Health Management Systems or the Office of Third Party Recovery. Hardship waiver procedures and the two-year caregiver child exemption.

Chapters 14-17: Children, Intestacy, Real Estate, and Attorney Decisions

PERS dependent child payments (25% of average compensation for duty-related deaths). Social Security child survivor benefits. Who inherits when there is no will --- the Determination of Heirs process, the Rule 81 Summons by publication, and the mandatory thirty-day notice period. Clearing real estate title through Muniment of Title (personal property under $10,000, all debts satisfied) without appointing an executor. And the specific scenarios where Chancery Court Rule 6.1 forces you to hire an attorney versus the statutory paths that let you handle everything yourself.

Who This Guide Is For

- The surviving spouse of a Mississippi public employee trying to decode the PERS survivor retirement packet, understand the difference between duty-related and non-duty-related death benefits, and meet the ninety-day Form 14 deadline before retroactive payments start slipping away.

- The adult child managing a parent's estate from out of state who needs to know whether the estate qualifies for the $75,000 Small Estate Affidavit or the Muniment of Title --- or whether Chancery Court Rule 6.1 requires hiring a Mississippi attorney before anything else can move forward.

- Families terrified of Medicaid estate recovery who received a notice from HMS or the Office of Third Party Recovery and need to know that Mississippi law requires an automatic waiver when a surviving spouse lives in the home.

- Spouses of workers who died from a job-related injury trying to claim the $1,000 lump sum and ongoing weekly wage benefits under Mississippi workers' compensation --- facing a sixty-day medical records deadline and an adversarial employer insurer that has stopped returning calls.

- Low-income survivors who cannot afford a probate attorney and need the complete map of statutory safe harbors --- bank releases, wage claims, vehicle transfers, and the Small Estate Affidavit --- to settle the estate without court.

Why Free Government Forms Do Not Replace a Sequenced Roadmap

Every form referenced in this guide is available for free on a government website. PERS Form 9A SRVR is on pers.ms.gov. The Social Security forms are on ssa.gov. The Small Estate Affidavit is a standard notarized document. Here is why the forms alone are not enough:

- PERS covers PERS. Social Security covers Social Security. Neither agency mentions the other. PERS will not tell you that Social Security survivor benefits may interact with your pension annuity. The SSA will not tell you about PERS at all. If you file with only one agency, you miss the other.

- National form vendors use the wrong terminology for Mississippi. Sites like eForms reference "Probate Court" instead of the correct term --- Chancery Court. They rarely warn you about the mandatory thirty-day waiting period for the Small Estate Affidavit, or clarify that real property cannot be transferred using it. Families buy and notarize forms that do not work.

- Law firm websites explain the problem. They withhold the solution. Mississippi elder law and probate firms publish detailed articles about the dangers of DIY estate administration. The content is accurate. It is also deliberately incomplete --- designed to trigger a consultation call, not to empower you to handle it yourself. The diagnostic question is not "how complicated is this?" but "does my estate actually require an attorney?" The answer, for many Mississippi estates under $75,000 in personal property, is no.

- Filing out of sequence triggers delays that compound. Claiming unpaid wages before notifying the bank can create clawback problems when post-mortem payments reverse. Attempting the Small Estate Affidavit before the thirty-day waiting period expires results in rejection. Submitting PERS Form 14 before Form 9A SRVR is processed by the employer means PERS has no record of your pre-application. The forms exist. The sequence is what turns them into money in your account.

Free resources give you one agency at a time, with no sequencing, no cross-referencing, and no way to know what you are missing. The Chancery Court Bypass System maps every benefit to your situation, organizes every form by deadline, and tells you exactly which agencies to contact in which order --- so you claim everything your family is owed without spending weeks navigating portals that were never designed to talk to each other.

--- Less Than Fifteen Minutes of a Probate Attorney's Time

Mississippi families leave thousands of dollars in survivor benefits unclaimed every year --- not because they are ineligible, but because no one told them the benefit existed. A PERS survivor pension worth hundreds of dollars per month goes unclaimed because the spouse did not know about the ninety-day Form 14 deadline and retroactive payments were capped at one year. A Tier 3 property tax exemption worth thousands over a lifetime goes unclaimed because the VA never mentions state-level tax benefits. A Medicaid estate recovery claim goes unchallenged because no one told the surviving spouse about Estate of Darby v. Stinson. This guide costs less than any of those missed benefits.

Your download includes the complete 17-chapter guide, the Mississippi Survivor Benefits Quick-Start Checklist, and five standalone reference sheets --- the Chancery Court Bypass Flowchart, Statutory Safe Harbor Reference, PERS Survivor Benefits Roadmap, Medicaid Estate Recovery Defense Guide, and Critical Deadline Calendar. Seven PDFs covering every time-sensitive step from the calls you make on day one through the filings due at day thirty-one and beyond.

30-day money-back guarantee. If the guide does not give you a clear map of every survivor benefit available to your family, every form you need to file, and every deadline you need to meet --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Mississippi Survivor Benefits Checklist --- a summary of the most time-sensitive actions, deadlines, and forms that most families do not discover until it is too late. Enough to start contacting the right agencies in the right order.

You did not plan for this. But you can plan what happens next. The guide gives you the benefits, the forms, the deadlines, and the filing sequence --- so the next six months are spent claiming what your family is owed, not discovering what you missed.