New Hampshire Abolished the Small Estate Affidavit. The Probate Court Requires Mandatory E-Filing. The Medicaid Recovery Unit Can Pierce Your Living Trust. And the Health Insurance Carrier Just Told You COBRA Expires in 36 Months --- Even Though State Law Says Otherwise.

Someone has died, and now you are the person responsible for figuring out what the surviving family is owed. You called Social Security and waited on hold for forty minutes before learning that the lump-sum death payment is $255. You called the New Hampshire Retirement System and were told the pension depends on whether the member selected "Option 2" or "Option 3" at retirement --- and nobody can tell you which one was chosen until you file a formal request with a notarized beneficiary designation form. You went to the town clerk for death certificates and paid $15 for the first copy and $10 for each additional, but you have no idea how many you actually need. You searched online for a "New Hampshire Small Estate Affidavit" because three different legal websites told you to file one --- and discovered that New Hampshire repealed that procedure in 2006 and it no longer exists.

Meanwhile, deadlines are running. The health insurance carrier has 30 days to send you a continuation notice, and you have exactly 45 days after that to elect coverage or lose it permanently. The property tax credit application is due by April 15 --- miss it and you forfeit the entire year's credit. The probate court requires mandatory electronic filing and will reject paper forms mailed to the local courthouse. Workers' compensation burial benefits cap at $10,000, but only if you file Form LAB 500 through the employer's insurer before the claim window closes. And the DHHS Estate Recovery Unit is already assessing whether it can file a lien against the family home.

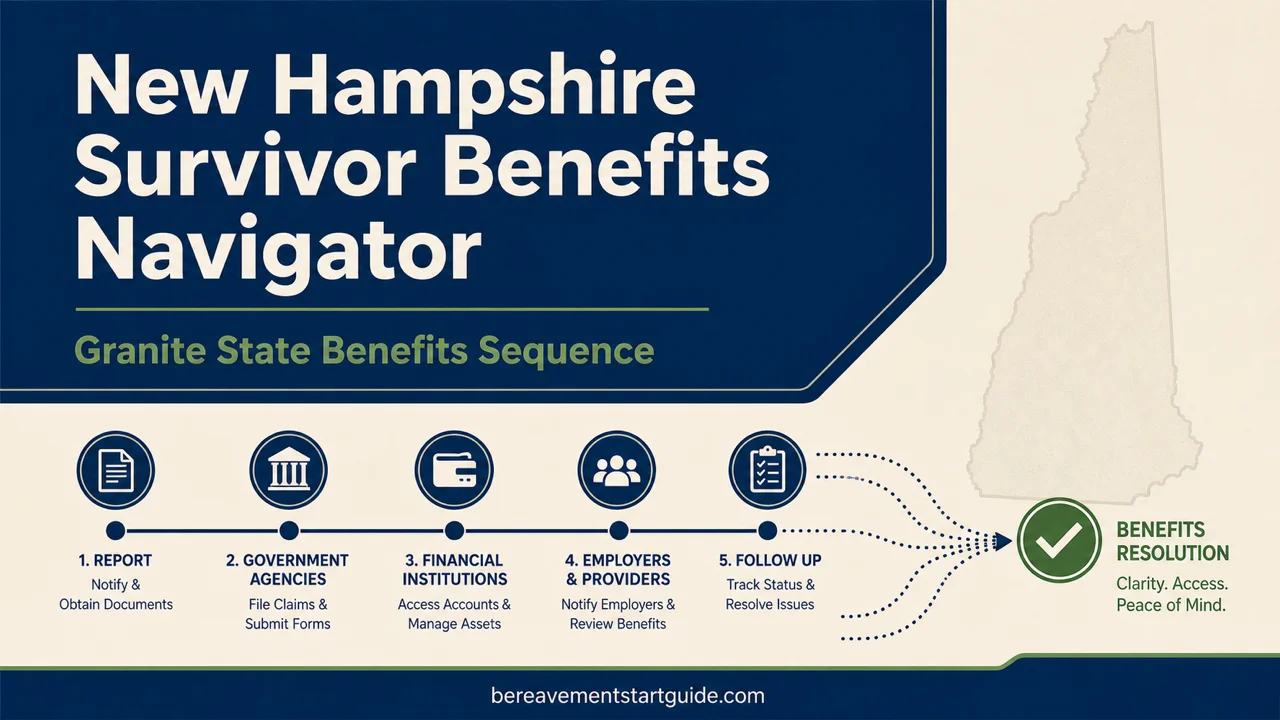

The New Hampshire Survivor Benefits Navigator is a Granite State Benefits Sequence --- a single, plain-English administrative reference that maps every federal payment, state pension, municipal tax credit, and statutory entitlement available to surviving families in New Hampshire. Not a grief resource. Not a blog post from a funeral home. Not generic legal advice written for another state. A New Hampshire-specific roadmap built from current RSA statutes, agency procedures, and court rules --- telling you which benefits exist, who qualifies, what forms to file, what documents to bring, and which deadlines will permanently disqualify you if you miss them.

What's Inside the Granite State Benefits Sequence

A 13-chapter guide with 2 appendices, plus a quick-start checklist --- covering every survivor benefit, application process, and statutory deadline that New Hampshire families face after a death:

Chapter 1: Death Certificates --- Your Foundation Document

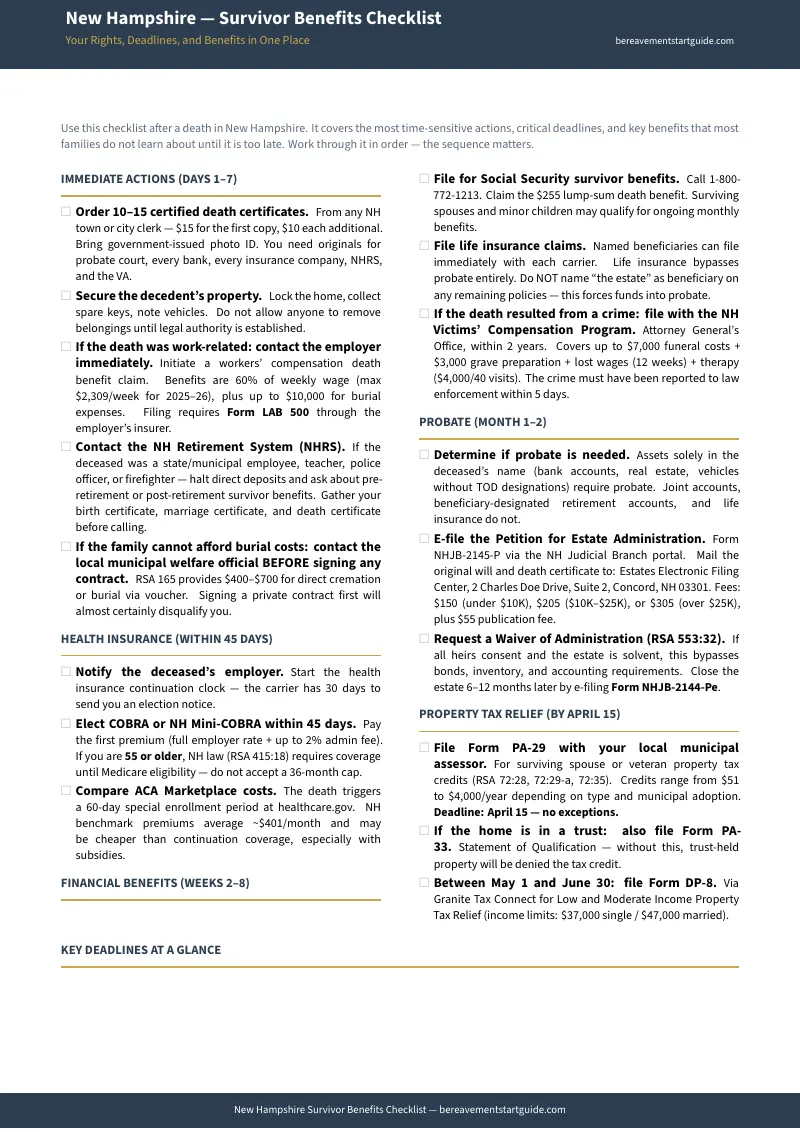

Every benefit in this guide requires a certified death certificate. The guide tells you exactly where to get them (any NH town or city clerk for deaths since 1990), how much they cost ($15 first copy, $10 each additional), who qualifies to request them under New Hampshire's "direct interest" rule, what identification you must present, and why you need 10 to 15 certified originals ordered at the same time. It explains the specific requirements for mail-in requests, the credit card surcharge, and the amendment process if corrections are needed --- because a death certificate with errors will be rejected by every agency you file with.

Chapter 2: Health Insurance --- The 45-Day Clock

If your spouse carried the household's health insurance, you have a narrow window to keep it. The guide maps the complete decision tree: federal COBRA versus New Hampshire Mini-COBRA under RSA 415:18, with the critical age distinction most carriers ignore. If you are 54 or younger, continuation lasts 36 months. If you are 55 or older, New Hampshire law mandates coverage until Medicare eligibility --- potentially bridging a decade-long gap. The guide explains the 30-day carrier notification requirement, the 45-day election deadline, what happens if the employer goes out of business (39 weeks of extended coverage), and when the ACA Marketplace at ~$401/month average benchmark premium may be cheaper than paying 102% of the group rate. It also tells you exactly how to escalate through the NH Insurance Department Consumer Services Division if a carrier tries to impose a 36-month cap that violates state law.

Chapter 3: Workers' Compensation Death Benefits

When death results from a workplace injury or occupational illness, New Hampshire provides substantial compensation: 60% of the deceased employee's average weekly wage (maximum $2,309/week for 2025-2026), plus a one-time burial expense of up to $10,000 paid directly by the employer's workers' compensation carrier. The guide covers the complete benefit structure --- duration rules for surviving spouses (benefits continue until death or remarriage), dependent children (benefits extend to age 25 for full-time students), and the special presumption for firefighters with 10+ years of service whose cancers are legally presumed occupational. Filing requires Form LAB 500 approved by the Labor Commissioner.

Chapter 4: NHRS Pension Survivor Benefits

If the deceased was a state employee, municipal worker, teacher, police officer, or firefighter enrolled in the New Hampshire Retirement System, survivor benefits depend on whether the death was pre- or post-retirement, whether it was job-related, and which survivorship option the member chose. The guide walks through every scenario: Ordinary Death with less than 10 years of service (lump sum only), Ordinary Death with 10+ years (the critical choice between lump sum and a lifetime pension at 50% of projected retirement), Accidental Death (50% of Average Final Compensation for Group I; 50% of earnable compensation for Group II), and the post-retirement options --- including the Group II automatic spousal allowance that pays 50% of the retiree's pension regardless of which option was selected, provided you were married on the retirement date. It covers every administrative requirement: notarized beneficiary forms, the documents you need before contacting NHRS (birth certificate, marriage certificate, W-4P, W-9), and the military service exception under the HEART Act.

Chapter 5: Property Tax Credits and Exemptions

New Hampshire relies heavily on local property taxes, making credits and exemptions worth hundreds to thousands of dollars annually. The guide covers every available credit: Surviving Spouse of Active Duty Deceased (RSA 72:29-a, $700-$2,000/year), Service-Connected Total Disability Survivor (RSA 72:35, $700-$4,000/year), Standard Veterans' Tax Credit Survivor (RSA 72:28, $51-$750/year), and the Elderly Exemption (RSA 72:39-a, varies by age bracket and municipality). Every credit requires Form PA-29 filed with your local assessor by the non-negotiable April 15 deadline. And if the home is in a revocable living trust --- the guide explains the Trust Tax Credit Trap: you must also file Form PA-33 (Statement of Qualification) or your credit application will be denied. Plus the Low and Moderate Income Property Tax Relief program (Form DP-8, filed May 1 through June 30) that most families never learn about.

Chapter 6: Probate --- Navigating the Circuit Court

New Hampshire's probate system is fully electronic, which is efficient but unfamiliar to most families. The guide explains the mandatory e-filing process step by step: creating an account on the NH Judicial Branch portal, generating the Petition for Estate Administration (Form NHJB-2145-P), and the critical requirement to physically mail the original will and death certificate to the Estates Electronic Filing Center at 2 Charles Doe Drive, Suite 2, Concord, NH 03301. It covers filing fees ($150 for estates under $10,000, $205 for $10,001-$25,000, $305 for over $25,000, plus $55 publication fee), the Waiver of Administration pathway (RSA 553:32) that eliminates bonds, inventory, and accounting requirements, the Summary Administration fallback (RSA 553:33), and every creditor deadline from the 6-month demand period through the 2-year absolute bar on claims against real estate.

Chapter 7: Medicaid Estate Recovery --- Protecting the Family Home

The DHHS Estate Recovery Unit is authorized to recover medical and cash assistance costs from the estates of deceased recipients --- and New Hampshire's definition of "estate" extends far beyond probate to include revocable living trusts, joint tenancies, tenancy in common interests, and life estates. The guide explains exactly what the ERU can and cannot do: the critical protection that prevents liens on a home occupied by a surviving spouse, minor child, or disabled child; the difference between cash assistance recovery (which carries over to the surviving spouse's estate) and medical assistance recovery (which does not); the hardship waiver process using BFA Form 785; and the specific circumstances that require an elder law attorney.

Chapter 8: Crime Victim Compensation

Families of homicide victims in New Hampshire can receive up to $50,000 per claimant through the Victims' Compensation Program (RSA 21-M:8): up to $7,000 for funeral and burial costs, $3,000 for grave preparation, 12 weeks of lost wages, $4,000 or 40 sessions of mental health therapy for family members, and categorical eligibility for minor children. The guide explains the filing deadlines (crime reported within 5 days, claim filed within 2 years), the payer-of-last-resort rule, and the direct filing process through the NH Department of Justice.

Chapter 9: Burial and Funeral Assistance

Three distinct programs: VA burial benefits ($1,002-$2,000 reimbursement plus free headstone, plus the NH State Veterans Cemetery in Boscawen at approximately $450 for a non-veteran spouse); Municipal Indigent Burial Assistance under RSA 165 ($400-$700 via voucher for families who apply before signing a funeral home contract); and the workers' compensation $10,000 burial expense for workplace deaths.

Chapter 10: Tax Considerations for Survivors

New Hampshire has no state income tax, no estate tax, no inheritance tax, and the Interest and Dividends Tax was fully repealed for periods beginning after December 31, 2024. The guide explains what this means for inherited trusts, brokerage accounts, and retirement distributions --- plus the legacy I&D Tax filing obligations for prior tax years (Form DP-10, rates from 3% to 5%), and the federal estate tax certification required before closing an estate with Form NHJB-2144-Pe.

Chapter 11: Educational Benefits for Surviving Children

Tuition waivers at USNH (RSA 187-A:20) and CCSNH (RSA 188-F:16) for children of fallen firefighters, police officers, and totally disabled veterans. Workers' compensation extended benefits to age 25 for full-time students. Federal Social Security survivor benefits for minors through age 18 (or 19 if still in high school).

Chapter 12: The Master Timeline

Every deadline from this guide consolidated into one chronological reference: days 1-15, within 45 days, within 6 months, by April 15, May 1 through June 30, and 6-12 months after appointment. Print this page and put it on the refrigerator.

Chapter 13: When You Need Professional Help

The specific circumstances that require an elder law attorney (Medicaid liens, trust-piercing by the ERU, BFA Form 785 hardship waivers), a probate litigation attorney (multi-county insolvent estates, strategic use of the 2-year creditor bar under RSA 556:29, contested wills), and when to escalate directly to the NH Insurance Department or 603 Legal Aid.

2 Master Appendices

The Form Directory (every form number, issuing agency, purpose, deadline, and filing method in one consolidated table --- NHJB-2145-P, NHJB-2144-Pe, NHJB-2149-P, PA-29, PA-33, DP-8, DP-10, BFA Form 785, LAB 500, and more). The Statute Reference (every RSA cited in the guide with its subject, from RSA 72:28 through RSA 556:29).

Who This Guide Is For

- The surviving spouse whose household income just disappeared --- who needs to know whether the NHRS pension continues, how to elect health insurance continuation before the 45-day window closes, which property tax credits to file for by April 15, and whether the Medicaid Estate Recovery Unit can force the sale of the family home. The guide maps the entire income-preservation sequence from the first phone call through estate closure.

- The adult child who just became an accidental estate administrator --- who searched for "New Hampshire Small Estate Affidavit" and discovered it does not exist, who needs to navigate mandatory e-filing on a court portal they have never seen, and who wants to know if the estate qualifies for a Waiver of Administration so they can skip bonds, inventory, and accounting. The guide gives you the exact criteria, the exact forms, and the exact timeline.

- The out-of-state executor settling a parent's New Hampshire estate --- who needs to know about the Appointment of Resident Agent requirement, the book-and-page-number Registry of Deeds documentation for multi-county real estate, the corporate surety bond threshold for estates over $25,000, and the centralized Concord mailing address for original wills. The guide covers every procedural trap that trips up non-residents.

- The family of a first responder or public employee killed on duty --- who may not know that Group II police and fire survivors receive an automatic 50% pension regardless of which option was selected, that firefighters with 10+ years of service have a cancer presumption under workers' compensation, that CCSNH tuition waivers exist for their children, or that the $10,000 burial expense is paid directly by the employer's carrier. The guide covers every enhanced benefit available to public service families.

- The surviving spouse over 55 whose insurance carrier just said COBRA expires in 36 months --- who needs to know that RSA 415:18 overrides the federal limit and requires coverage until Medicare eligibility, and who needs the exact escalation path through the NH Insurance Department to enforce it. The guide tells you what the law says, what to demand, and who to call when the carrier refuses.

Why Free Resources Leave Money on the Table

Survivor benefit information exists in New Hampshire. It is spread across the Social Security Administration in one set of forms, the NHRS in another, the Circuit Court Probate Division in a third, the Department of Revenue Administration in a fourth, the Department of Labor in a fifth, the DHHS Estate Recovery Unit in a sixth, and town clerk offices that each operate independently. Here is what happens when you try to navigate all of this yourself:

- The SSA website covers Social Security benefits. It does not mention the NHRS pension, the property tax credits under RSA 72:28, the Mini-COBRA age protection under RSA 415:18, or the crime victim compensation program. Every federal agency covers only its own programs. If you stop at Social Security, you miss everything New Hampshire provides at the state and municipal level.

- The VA covers veterans benefits. It does not cross-reference New Hampshire property tax credits. A surviving spouse of a veteran killed on active duty can receive $700 to $2,000 annually in property tax credits under RSA 72:29-a. The VA will never tell you this benefit exists --- it is administered by local municipal assessors, not the federal government.

- Courts.nh.gov provides the e-filing portal and blank forms. It does not explain which probate pathway your estate qualifies for. The court will not tell you whether to request a Waiver of Administration or file for Summary Administration. It will not explain that Form PA-33 is needed if the home is in a trust. It will not warn you that national websites recommending a "Small Estate Affidavit" are giving advice that has been legally invalid in New Hampshire since 2006.

- National legal websites are actively dangerous for New Hampshire estates. LegalZoom, Nolo, and similar services routinely advise filing a "Small Estate Affidavit" or "Voluntary Administration" --- procedures New Hampshire abolished. Following this advice wastes weeks of effort and forces you to start over with the correct Waiver of Administration process.

- Hiring a New Hampshire probate attorney for straightforward benefit claims costs $250-$350 per hour. For a surviving spouse who needs to know which forms to file with which agencies in which order, a legal retainer is a disproportionate expense for what is fundamentally an organizational problem --- not a legal one.

Free resources give you one agency at a time, with no sequencing, no cross-referencing, and no way to know what you are missing. The Granite State Benefits Sequence maps every benefit to every scenario, organizes every form by deadline, and tells you exactly which agencies to contact in which order --- so you can claim everything your family is owed without spending weeks navigating portals that were never designed to talk to each other.

--- Less Than One Hour of a New Hampshire Probate Attorney's Time

New Hampshire families leave thousands of dollars in unclaimed survivor benefits every year --- not because they are ineligible, but because no one told them the benefit existed. A surviving spouse over 55 loses health insurance because a carrier imposed a 36-month cap that violates RSA 415:18. An NHRS pension worth hundreds of dollars per month goes unclaimed because the surviving spouse did not know they needed to actively file. A property tax credit worth $700 to $4,000 annually goes unclaimed because no one mentioned the April 15 deadline or the Form PA-33 requirement for trust-held properties. A $10,000 workers' compensation burial expense goes unpaid because the family did not know about Form LAB 500. This guide costs less than any of those lost benefits and tells you where to find every one of them.

Your download includes 6 PDFs: the complete 13-chapter guide, a quick-start checklist organized by timeframe (days 1-7, within 45 days, weeks 2-8, month 1-2, by April 15, and 6-12 months), a master form directory with every form number and filing method, a key statute reference listing every RSA cited in the guide, a master timeline fridge sheet consolidating every deadline into one printable page, and a health insurance decision tree mapping the COBRA versus Mini-COBRA choice with the critical age-55+ protection under RSA 415:18.

30-day money-back guarantee. If the guide does not give you a clear map of every survivor benefit available to your family, every form you need to file, and every deadline you need to meet --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New Hampshire --- Survivor Benefits Checklist --- a summary of the most time-sensitive actions, deadlines, and forms that most families do not discover until it is too late. Enough to start contacting the right agencies in the right order.

You did not plan for this. But you can plan what happens next. The guide gives you the benefits, the forms, the deadlines, and the filing sequence --- so the next six months are spent claiming what your family is owed, not discovering what you missed.