The Bank Froze 50% of the Account the Day You Called. The Division of Taxation Requires a Form L-8 but Nobody at the Surrogate's Court Explains How It Works. The Inheritance Tax Was Supposed to Be Repealed but Class C and D Beneficiaries Still Owe Up to 16%. The 21 County Surrogates All Run Different Procedures. And the 8-Month Filing Deadline Carries a 10% Annual Interest Penalty With No Extensions.

Your father died in Bergen County on a Wednesday. By Friday you had a stack of hospital bills, a credit card statement addressed to him, and a funeral director asking how many certified death certificates you want at $25 for the first copy and $2 for each additional. You said five. You will need twelve. Every bank, every insurance company, every government office requires an original raised-seal copy, and the NJ Office of Vital Statistics takes weeks to process reorders by mail.

You called the bank to ask about his checking account. The teller confirmed the death and immediately froze half the balance. You did not ask them to freeze anything. They told you it was state law --- New Jersey Administrative Code 18:26-11.16 --- and that the other half could not be released until you presented something called a "tax waiver." You had never heard of a tax waiver. You searched online and found references to Form L-8, Form L-9, Form IT-R, and Form 0-1. Nobody explained which one you needed, or in what order, or why New Jersey requires a different form depending on whether the beneficiary is a spouse, a child, a sibling, or a friend.

The NJ Estate Settlement Navigator is an Estate Settlement Sequence built entirely around New Jersey Revised Statutes, the NJ Administrative Code, and the procedures of the 21 County Surrogates --- mapping every form, fee, deadline, beneficiary class, tax waiver path, and agency requirement into one chronological sequence. It diagnoses whether your estate qualifies for a Small Estate Affidavit (bypassing full administration entirely), which tax waiver forms apply to your specific beneficiary classes, how to unfreeze bank accounts without waiting 90 days for the state, and when you actually need an attorney versus when you are paying $350 an hour for tasks you can complete with the correct form and a certified death certificate.

What's Inside the Estate Settlement Sequence

A comprehensive guide with appendices, a printable action checklist, and standalone worksheets --- covering every probate shortcut, tax waiver path, asset transfer, creditor defense, and agency procedure available under New Jersey law:

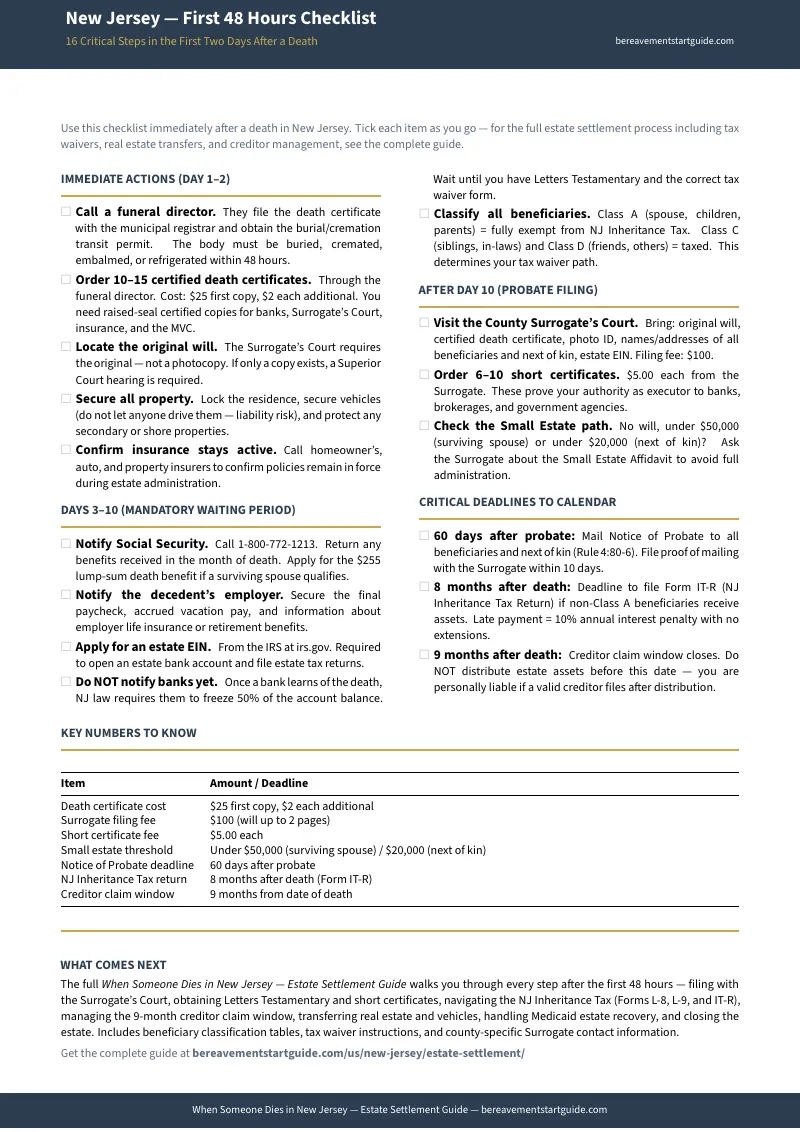

Chapters 1-2: The First 48 Hours and the 10-Day Waiting Period

What makes New Jersey different from every other state: the mandatory 50% bank freeze on every account the moment a financial institution learns of the death, the four-class inheritance tax system that survived even after the estate tax was repealed in 2018, the 21 independent County Surrogates who each run their own procedures, and the aggressive Medicaid estate recovery program that reaches beyond probate assets into joint accounts and POD designations. Day-by-day triage for the first 48 hours: ordering certified death certificates through the funeral director ($25 first copy, $2 each additional from the state), securing the residence and vehicles, locating the original will (the Surrogate requires the original --- a photocopy triggers a Superior Court hearing), and understanding that New Jersey imposes a mandatory 10-day waiting period before probate can begin. What NOT to do --- do not notify banks until you have your Letters Testamentary and the correct tax waiver form ready, do not pay the decedent's credit card bills with your own money, and do not distribute assets before the 9-month creditor window closes.

Chapter 3: Small Estate Shortcuts

The diagnostic that tells you whether you can bypass full probate administration entirely. If the decedent died without a will and the estate is under $50,000 (surviving spouse) or under $20,000 (next of kin), New Jersey allows a streamlined Affidavit process through the Surrogate's Court that avoids formal accounting, expensive administration fees, and the requirement to post a surety bond. How to determine eligibility. How to gather the specific asset information the affidavit requires --- bank names, account numbers, vehicle VINs, and precise valuations. The $5,000 creditor shield available to surviving spouses. When the shortcut works and when it does not.

Chapter 4: Probate vs. Non-Probate Assets

The classification that determines everything else in the settlement process. Which assets you control as executor (sole-name bank accounts, individually titled real estate, vehicles without TOD designations) and which transfer automatically outside your authority (joint accounts with survivorship, POD accounts, life insurance with named beneficiaries, retirement accounts with designated beneficiaries, vehicles with the new Transfer on Death designation under N.J.S.A. 39:3-30.1b). The critical trap: just because an asset bypasses probate does not mean it bypasses the New Jersey Inheritance Tax or the tax waiver requirement. A surviving spouse's joint bank account still gets 50% frozen until a Form L-8 is filed. Non-probate assets passing to Class C or D beneficiaries still count toward the inheritance tax calculation.

Chapter 5: Motor Vehicle Transfers

Four distinct paths depending on how the vehicle was titled: the TOD beneficiary transfer (enacted 2022, bypasses the Surrogate entirely), the joint-owner spouse transfer using Form BA-62, the estate transfer using a Surrogate's Short Certificate, and the Small Estate Affidavit transfer. The $60 title fee at the MVC. Why relying on older guides that predate the TOD law forces families through unnecessary probate steps for vehicles that now qualify for direct transfer.

Chapter 6: The Tax Waiver System --- Unfreezing Your Assets

The chapter that addresses the single most frustrating aspect of settling an estate in New Jersey. The complete breakdown of the 50% bank freeze: how the math works, what the bank retains, and the one exception (checks written to pay the NJ Inheritance Tax). The four beneficiary classes --- Class A (spouse, children, parents, grandchildren: 100% exempt), Class C (siblings, in-laws: $25,000 exemption then 11-16%), Class D (nieces, nephews, friends: taxed on amounts over $500 at 15-16%), and Class E (charities: exempt but still require filing). The fast-track path: if all beneficiaries are Class A, you file Form L-8 directly with the bank to release frozen funds instantly, and Form L-9 with the Division of Taxation for real estate. The full-return path: if any beneficiary is Class C or D, you must file the comprehensive Form IT-R within 8 months of death, pay all assessed tax, and wait approximately 90 days for the state to issue Form 0-1 waivers. The estimated payment form (IT-PMT) that stops the 10% annual interest penalty even before the full return is complete.

Chapter 7: Real Estate Transfers

Transferring the decedent's New Jersey property --- often the highest-value and most procedurally complex task in the entire settlement. Tenancy by the entirety (married couples: automatic transfer, no waiver needed). Property passing to Class A beneficiaries (Form L-9 to the Division of Taxation, then record Form 0-1 with the County Clerk). Property passing to Class C or D beneficiaries (full IT-R required before any transfer). The 15-year statutory tax lien that blocks any sale until a waiver is recorded. County Clerk recording fees ($40-$45 for the first deed page, $15 for the inheritance tax waiver recording). Ancillary probate for out-of-state executors managing Jersey Shore properties --- how to obtain an Exemplified Copy of the will from the original probate state and file it with the New Jersey Surrogate.

Chapter 8: Creditors, Debts, and the 9-Month Window

The biggest fear for executors, answered directly: New Jersey heirs do not inherit debt. The 9-month creditor claim window under N.J.S.A. 3B:22-4. The exact statutory priority of payments for insolvent estates under N.J.S.A. 3B:22-2 --- funeral expenses first, administration costs second, federal taxes third, medical expenses of the last illness fourth, state taxes and Medicaid liens fifth, unsecured debts last. Why you must never distribute assets before month 10. Why you must never pay a decedent's credit card bill with your own money. How to handle aggressive debt collectors: require all claims in writing and under oath, and give yourself the full 3-month review window the statute allows. New Jersey repealed the newspaper publication requirement for creditor notice in 2005 --- you are not required to take out an ad.

Chapter 9: Medicaid Estate Recovery

New Jersey's Division of Medical Assistance and Health Services (DMAHS) runs one of the most aggressive Medicaid recovery programs in the country. The "expanded estate" definition under N.J.A.C. 10:49-14.1 that reaches beyond probate into joint bank accounts, POD accounts, living trust assets, and annuities. The specific exemptions that protect the family home (surviving spouse, child under 21, permanently disabled child). The critical 20-day window to file an undue hardship waiver after receiving a DMAHS recovery notice. Why distributing any expanded estate assets before resolving the lien is a breach of fiduciary duty that exposes you to personal liability.

Chapters 10-11: Final Tax Returns and Closing the Estate

Filing the decedent's final federal Form 1040 and NJ Form NJ-1040 for the year of death. Estate income tax returns (Form 1041 and NJ-1041) if the estate earns income during administration. The Refunding Bond and Release --- the mandatory document every beneficiary must sign and notarize before receiving their final distribution, legally protecting you as executor from future claims. Filing the executed bonds with the Surrogate's Court ($10.00 fee). Closing the estate bank account. New Jersey does not require a formal judicial accounting unless a beneficiary demands one --- the closing process is simpler than most families expect.

Chapters 12-15: Professional Help, County Surrogates, Master Timeline, and Forms Reference

When to hire an estate attorney immediately: the original will is missing (Superior Court required), the will is holographic, someone files a caveat, or beneficiaries are in active dispute. When to hire a CPA: any Class C or D beneficiary triggers the mandatory IT-R, and the 8-month deadline with its 10% interest penalty leaves no room for error. A reference guide to all 21 County Surrogates and their varying procedures --- appointment requirements, accepted payment methods, and local filing quirks. The master timeline of every statutory deadline from the 48-hour disposition rule through the 15-year real estate tax lien. A complete forms directory with download links for every form referenced in the guide.

Appendices: Asset Inventory, Creditor Log, and Notification Tracker

Printable worksheets to organize the estate from day one. The Asset Inventory Worksheet classifies every financial account, real estate parcel, vehicle, insurance policy, and retirement account by probate status, beneficiary class, and required tax waiver form. The Creditor Claim Log tracks dates, amounts, oath status, and resolution for every claim received during the 9-month window. The Notification Tracker covers every agency and institution that must be contacted --- Social Security, employers, banks, brokerages, insurers, the MVC, the Division of Taxation, DMAHS, pension custodians, utilities, and the post office.

Who This Guide Is For

- The surviving spouse whose bank account was just frozen --- who walked into the bank expecting to access the joint checking account and was told that 50% of the balance is locked under state law until a "tax waiver" is filed. You need to know that Form L-8 is the self-executing waiver that releases the funds immediately, that you as a Class A beneficiary owe zero inheritance tax, and that you should have had this form in hand before the bank learned of the death.

- The adult child named as executor who accepted the role because the will named them, but has never filed at a County Surrogate's Court, never heard of Form L-8 or Form L-9, and does not know the difference between the inheritance tax (which still exists) and the estate tax (which was repealed in 2018) --- or that the 8-month filing deadline for the IT-R carries a 10% annual interest penalty with no extensions.

- The out-of-state executor managing a Jersey Shore property who discovered they need to file ancillary probate in the county where the property is located, obtain a tax waiver from the Division of Taxation before the title company will clear the sale, and pay county recording fees they did not know existed --- all from another state.

- The sibling, niece, nephew, or friend named as a beneficiary who just learned they are Class C or Class D under New Jersey's inheritance tax and owe between 11% and 16% on their share --- and that the executor can be held personally liable if the tax goes unpaid and assets are distributed prematurely.

- The family facing Medicaid estate recovery who received a DMAHS notice and has exactly 20 days to file an undue hardship waiver --- and does not know which statutory exemptions protect the family home or that the "expanded estate" definition reaches into joint accounts and POD designations that were supposed to bypass probate.

- The small estate family trying to close a modest estate without spending thousands on legal fees --- who needs to know whether the Affidavit of Surviving Spouse ($50,000 threshold) or Affidavit of Next of Kin ($20,000 threshold) applies, and how to complete the process at the Surrogate's Court without formal administration or expensive accounting fees.

Why Free Government Forms and Websites Are Not Enough

Every form referenced in this guide is available for free from a New Jersey government website. The Division of Taxation publishes Form L-8, Form L-9, and Form IT-R. The County Surrogates provide small estate affidavit forms. The MVC has Form BA-62 for vehicle transfers. Here is why the forms alone are not enough:

- The state provides the forms but not the sequence. The NJ Division of Taxation publishes tax waiver forms. The County Surrogate publishes probate information. The MVC handles vehicle titles. The DMAHS handles Medicaid recovery. These are four separate bureaucracies that do not coordinate with each other. No single government page tells you in what order to file, what to gather before you start, or how a tax waiver filed with the Division of Taxation connects to a deed recorded at the County Clerk. They hand you raw paperwork without sequencing, without cross-references, and without any acknowledgment that you are doing this while grieving.

- National legal websites miss the NJ-specific traps. Nolo, FindLaw, and eForms publish generic probate overviews that rank well in search results. They do not explain the 50% bank freeze. They do not distinguish between Form L-8 (self-executing, handed to the bank) and Form IT-R (filed with the state, 90-day processing time). They do not mention that New Jersey's inheritance tax survived the 2018 estate tax repeal. They do not cover the four beneficiary classes or explain why the class distinction determines your entire tax waiver path. Families follow these generic guides and discover, weeks in, that New Jersey has rules the national websites never mentioned.

- Law firm websites explain the problem but withhold the solution. New Jersey probate attorneys publish detailed articles about inheritance tax classes, the bank freeze, and Medicaid recovery. The content is accurate. It is also deliberately incomplete --- designed to convince you that the process is too dangerous to attempt alone and to trigger a consultation call at $150 to $650 per hour. The question is not "how complicated is this?" but "does my estate actually require an attorney?" The answer, for many New Jersey estates where all beneficiaries are Class A, is no.

- The 21 County Surrogates each run different procedures. Some counties require appointments. Some use eProbate systems. Some demand in-person appearances. Some have specific local filing forms. Fees are standardized by statute but auditing and accounting fees scale by estate value in ways that are not obvious from the published fee schedule. A guide built for "New Jersey" generically does not tell you what to expect when you walk into the Camden County Surrogate versus the Somerset County Surrogate.

- Filing out of sequence triggers delays that compound. Notifying the bank before you have Letters Testamentary and a tax waiver freezes your access to funds for months. Filing Form L-9 when you should have filed the IT-R (because a Class D beneficiary exists) restarts the entire process. Distributing assets before the 9-month creditor window closes creates personal liability. Paying low-priority debts before funeral expenses violates the statutory priority order. The forms exist. The sequence is what turns them into money in your account and a deed in your name.

Free resources give you one agency at a time, with no sequencing, no cross-referencing, and no way to know what you are missing. The Estate Settlement Sequence maps every asset, every form, every beneficiary class, and every deadline into one chronological guide --- so you unfreeze every account, avoid every common rejection, and determine whether you actually need an attorney before spending a dollar on one.

--- Less Than Twenty Minutes of a New Jersey Probate Attorney's Time

New Jersey families lose weeks and thousands of dollars every year --- not because the estate was complicated, but because nobody told them about the shortcuts the law provides. A surviving spouse watches $50,000 sit frozen in a joint bank account for three months because nobody told them a one-page Form L-8 would release it in a single visit. A family hires an attorney at $350 per hour to gather death certificates, call Social Security, and fill out forms that require no legal expertise. An executor misses the 8-month inheritance tax deadline and triggers the 10% annual interest penalty because they confused the repealed estate tax with the active inheritance tax. A small estate worth $18,000 goes through full probate administration --- with its sliding-scale accounting fees --- because nobody mentioned the Affidavit of Next of Kin. A family home that should be protected from Medicaid recovery goes undefended because nobody explained the surviving spouse exemption or the 20-day hardship waiver window. This guide costs less than any of those mistakes.

Your download includes the complete guide with appendices, the New Jersey --- First 48 Hours Checklist, and 8 standalone printable tools --- the Asset Inventory Worksheet, the Creditor Claim Log, the Notification Tracker, the Settlement Timeline, the Forms Reference, and the Probate Decision Tree --- covering every time-sensitive step from securing the estate on day one through the 10-day probate waiting period, the 60-day Notice of Probate requirement, the 8-month inheritance tax deadline, the 9-month creditor claim window, and the 15-year real estate tax lien.

30-day money-back guarantee. If the guide does not give you a clear map of every tax waiver path available for your New Jersey estate, every form you need to file, and every deadline you need to meet --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New Jersey --- First 48 Hours Checklist --- a summary of the most time-sensitive actions, forms, and beneficiary class distinctions that most families do not discover until the bank has already frozen the account. Enough to start the right sequence on day one.

You did not plan for this. But you can plan what happens next. The guide gives you the forms, the deadlines, the tax waiver paths, and the filing sequence --- so the next nine months are spent settling the estate correctly, not discovering what you missed.