The Bank Froze Half the Joint Account. The State Filed a Lien on the House You Haven't Even Listed Yet. The Inheritance Tax Return Is Due in Eight Months. The Division of Taxation Wants Form L-8 or L-9 or IT-R or 0-1 -- and Nobody Will Tell You Which One Applies to Your Situation.

You called the bank to access the checking account your parent left behind. The representative told you that New Jersey law requires them to freeze 50% of all jointly held accounts upon death -- and the funds cannot be released until you produce a "tax waiver" from the state. You searched the Division of Taxation website and found four different waiver forms. Form L-8 appears to release bank accounts, but the instructions say it applies only to "Class A beneficiaries" and you have no idea which class you belong to. Form L-9 mentions real property. The IT-R is a full inheritance tax return. Form 0-1 is the official waiver you apparently receive after filing the IT-R -- but only after the state processes it, which takes up to 90 days.

Meanwhile, the title company told you the house cannot be sold until the state's automatic death tax lien is cleared. The real estate agent said something about a "Realty Transfer Fee" exemption and a "step-up in basis" that should protect you from capital gains, but nobody has explained how to actually file the paperwork that makes any of that happen. The mortgage company is still sending bills. The estate bank account does not exist yet because you have not applied for an EIN. And the eight-month deadline for the inheritance tax return is already ticking -- with a 10% annual interest penalty if you miss it.

Your spouse is a Class A beneficiary who owes zero inheritance tax. Your sister-in-law is a Class C beneficiary facing 11% to 16% on everything above $25,000. Your late parent's longtime friend who was named in the will is Class D and owes 15% starting from the first dollar above $500. Each person's tax waiver path is different. Each form goes to a different place. Filing the wrong one wastes months.

You came here because New Jersey has the most complex tax waiver system of any state in the country -- and the free government forms come without instructions on which one to use, where to file it, or what order to do anything in.

The New Jersey Final Tax & Estate Tax Guide is a Tax Waiver Navigation System built around the New Jersey Division of Taxation's actual form requirements, the County Surrogate's probate process, federal filing thresholds, and the state's Medicaid estate recovery rules. It maps every tax obligation, every waiver form, every filing deadline, and every beneficiary-class calculation into one chronological sequence -- so you clear the liens, unfreeze the accounts, file the correct returns, and distribute assets without personal liability.

What's Inside the Tax Waiver Navigation System

A 17-chapter guide with tax calculation tables, decision flowcharts, a deadline tracker, and a complete forms reference -- covering every tax obligation that follows a death in New Jersey:

Chapter 1: The Taxes That Apply After a Death in New Jersey

The definitive answer to the question every executor asks first. The New Jersey Estate Tax was completely repealed in 2018 -- you do not owe it. The federal estate tax exemption was permanently set at $15 million per individual by the One Big Beautiful Bill Act in 2025 -- irrelevant for 99% of families. What you DO owe: the New Jersey Inheritance Tax (active and aggressively enforced), the decedent's final state income tax, and possibly a fiduciary income tax return if the estate generates more than $10,000 in income. This chapter strips away the confusion between four taxes that sound similar and tells you exactly which ones apply.

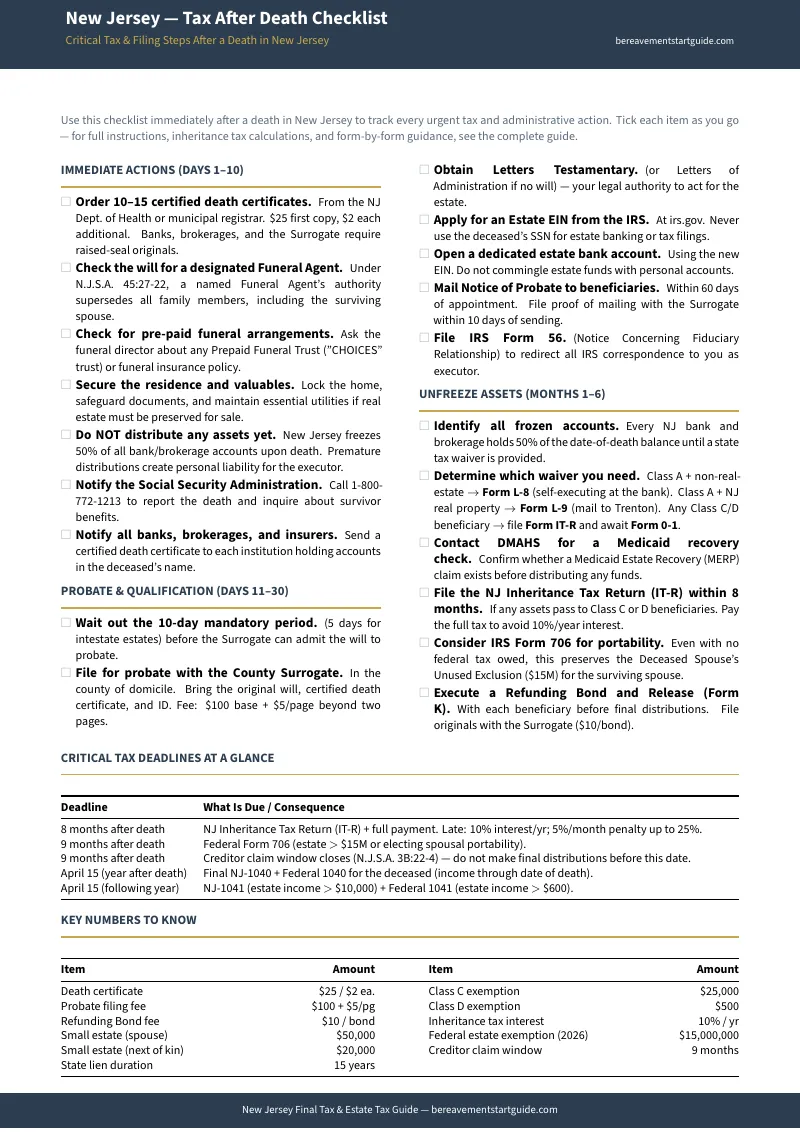

Chapters 2-4: Immediate Actions, Probate, and Small Estate Shortcuts

The 10-day waiting period before a will can be probated. What to bring to the County Surrogate's office (the original will, certified death certificates, valid photo ID, and the $100+ filing fee that varies by county and page count). How to get Letters Testamentary. When you can skip probate entirely -- the Surviving Spouse Affidavit ($50,000 threshold) and the Next-of-Kin Affidavit ($20,000 threshold). How to apply for an estate EIN. Why using the deceased's Social Security Number for any estate transaction is illegal.

Chapter 5: The 50% Asset Freeze and the Tax Waiver System

The chapter that solves the most common crisis. How the mandatory 50% freeze works and why every financial institution enforces it. Form L-8 -- the self-executing waiver that releases frozen bank accounts immediately for Class A beneficiaries. You hand it directly to the bank, not to the state. If you mail it to the Division of Taxation, they discard it and the account stays frozen. Form L-9 -- the real property waiver for Class A beneficiaries, filed with the Division of Taxation in Trenton to clear the death tax lien before a sale can close. Form L-4 -- the preliminary waiver for estates that need liquidity before the full IT-R is processed. Form 0-1 -- the official state waiver issued only after the inheritance tax return is filed and processed. Includes a decision flowchart that matches every beneficiary scenario to the correct form and filing location.

Chapters 6-9: The Inheritance Tax Return

Line-by-line guidance on the newly updated 2024 fillable IT-R form. How to identify beneficiary classes -- Class A (spouse, children, parents: 0% tax, unlimited exemption), Class C (siblings, sons-in-law, daughters-in-law: $25,000 exemption, 11-16% rates), Class D (nieces, nephews, friends: $500 exemption, 15-16% rates), and Class E (charities: fully exempt). How to calculate the taxable estate. How to take allowable deductions on Schedule D -- funeral expenses, surrogate fees, attorney fees, debts of the decedent. The eight-month filing deadline and the 10% annual interest penalty for late payment. Pre-payment requirements and estimated tax obligations. What happens during the 90-day processing delay and why you cannot distribute assets until the 0-1 waivers arrive.

Chapters 10-11: The Decedent's Final Income Tax and Fiduciary Returns

The final NJ-1040 covering January 1 through the date of death. The critical income cutoff -- anything earned one day after death belongs on the NJ-1041 fiduciary return, not the personal return. When the estate crosses the $10,000 gross income threshold that triggers the NJ-1041 filing requirement. How to issue Schedule NJK-1 forms to beneficiaries so the estate does not pay tax on income it has already distributed. The federal Form 1041 threshold ($600 in gross income) that catches executors who only check the state rules. Extension procedures and the 80% estimated tax pre-payment requirement.

Chapter 12: Medicaid Estate Recovery

The hidden bill that arrives after you think everything is settled. New Jersey runs one of the most aggressive Medicaid estate recovery programs in the country -- pursuing reimbursement from estates of recipients over age 55 for claims exceeding just $500 against estates valued over $3,000. Unlike most states, New Jersey pursues non-probate transfers and places strict liens on property that prevent refinancing. Mandatory deferrals when a surviving spouse, minor child, or disabled child exists. Why distributing assets before resolving Medicaid claims creates personal liability for the executor. The undue hardship waiver process and why it is nearly impossible to obtain.

Chapters 13-14: Selling Inherited Real Estate and Non-Resident Estates

The step-up in basis that resets the property's cost basis to fair market value on the date of death -- and how a New Jersey home purchased for $50,000 in 1980 and valued at $500,000 at death generates zero capital gains tax upon immediate sale. How to clear the death tax lien with the correct waiver form before the title company will allow a closing. The Realty Transfer Fee and the executor exemption under $100. The complete real estate sale timeline from establishing basis through recording the deed. For non-resident executors: what New Jersey taxes on out-of-state decedents (real property only, not intangibles), the Form L9-NR filing requirement, and the step-by-step process for selling a New Jersey shore house from out of state.

Chapters 15-17: Timeline, Forms Reference, and When to Hire a Professional

The master deadline tracker from day one through month 14 -- every filing deadline, processing delay, and distribution checkpoint on one page. A complete forms directory listing every NJ form referenced in the guide (L-8, L-9, L-4, IT-R, 0-1, NJ-1040, NJ-1041, NJK-1, L9-NR, and more) with where to download each one and where to submit it. Clear criteria for when you can handle the process yourself (all Class A beneficiaries, no Medicaid claims, no disputes) versus when you need a probate attorney or CPA.

Appendices: Quick-Reference Tax Tables, Key Contacts, and Glossary

Class C and Class D inheritance tax calculation tables with exact rates at every bracket. Contact information for the Division of Taxation, all 21 County Surrogates, the Division of Medical Assistance, and the IRS. A glossary covering every legal term used in the guide from "ancillary administration" to "tax waiver."

Who This Guide Is For

- The executor whose bank just froze $80,000 in joint accounts -- who was told the funds require a "tax waiver" to release but cannot determine whether to file Form L-8 directly with the bank, Form L-9 with the Division of Taxation, or the full IT-R. You need the tax waiver decision flowchart in Chapter 5 and the step-by-step L-8 instructions that explain exactly what to hand the bank teller.

- The sibling named in a will who just learned they owe inheritance tax -- who knows they are a Class C beneficiary but does not know how to calculate the tax, which deductions reduce the taxable estate, or when the eight-month deadline started running. You need the IT-R walkthrough, the Class C tax calculation table in Appendix A, and the Schedule D deduction checklist.

- The out-of-state executor trying to sell a New Jersey shore house -- who discovered the title company will not close until a tax waiver clears the state's death tax lien, and the non-resident filing requirements are different from resident requirements. You need Chapter 14 on non-resident estates and the Form L9-NR process.

- The surviving spouse who was told the estate tax was repealed but still cannot access anything -- who correctly understood that the estate tax ended in 2018 but did not realize the inheritance tax is a completely different tax that is still active, and that the 50% asset freeze applies regardless of tax liability. You need Chapter 1 to understand what actually applies and Chapter 5 to unfreeze the accounts immediately.

- The executor managing a rental property that keeps generating income -- who did not realize the estate is a separate taxable entity that needs its own EIN, its own bank account, and a fiduciary income tax return once gross income exceeds $10,000. You need the NJ-1041 chapter and the NJK-1 distribution instructions.

- The family discovering a Medicaid recovery claim months after the funeral -- who distributed cash to beneficiaries before learning that New Jersey's DMAHS pursues reimbursement from estates for long-term care costs, including non-probate transfers. You need Chapter 12 to understand your personal liability and the deferral rules that may still protect you.

Why Free Government Forms Are Not Enough

Every form referenced in this guide is available for free on the New Jersey Division of Taxation website. The IT-R, the L-8, the L-9, and the 0-1 are all downloadable PDFs. Here is why having the forms leaves you stranded:

- The state provides the forms but not the instruction manual. The Division of Taxation website hosts Forms L-8, L-9, IT-R, and 0-1 as isolated documents written in statutory language. There is no page that explains which form applies to which situation, what order to file them in, or where each one goes. An executor who mails Form L-8 to the Division of Taxation instead of handing it directly to the bank will have the form discarded and the account will remain frozen indefinitely.

- Law firms explain the complexity but charge $300 to $500 per hour to solve it. New Jersey estate and elder law firms publish excellent articles about the inheritance tax, the waiver system, and Medicaid recovery. The content is accurate and deliberately incomplete -- designed to demonstrate that the process is too complex to handle alone. For the majority of uncontested estates where all beneficiaries are Class A, the forms are straightforward and an attorney is unnecessary.

- National tax websites miss the NJ-specific waiver system entirely. TurboTax, Nolo, and FindLaw cover the federal estate tax exemption and generic inheritance tax overviews. They do not explain the L-8 bank release, the L-9 real property waiver, the L-4 preliminary waiver for liquidity emergencies, or the 90-day processing delay that keeps assets frozen even after you file. Executors who follow national guides miss the specific New Jersey steps that actually unlock the money.

- Getting it wrong does not just delay things -- it creates personal liability. An executor who distributes assets before the 0-1 waivers arrive is personally liable for any unpaid inheritance tax. An executor who fails to file the IT-R within eight months faces 10% annual interest on the outstanding balance. An executor who distributes before resolving a Medicaid estate recovery claim faces personal liability for the state's reimbursement. The cost of a procedural mistake is measured in thousands of dollars and months of delay -- not just inconvenience.

Free resources give you isolated forms with no sequence, no beneficiary-class guidance, and no protection against the mistakes that create personal liability. The Tax Waiver Navigation System maps every form, every class, every deadline, and every filing location into one chronological guide -- so you file the right form with the right office in the right order, and distribute assets only when the state says you are clear.

-- Less Than One Hour of a New Jersey Probate Attorney's Time

New Jersey executors lose months to frozen bank accounts because nobody told them about a one-page Form L-8 they could have handed directly to the bank teller. Siblings inherit property and cannot sell it because nobody explained that the death tax lien must be cleared with a specific waiver form before any title company will close. Executors face 10% annual interest penalties because they did not know the inheritance tax return deadline started running on the date of death, not the date of probate. Families distribute cash to beneficiaries and receive a Medicaid recovery demand from the state months later -- and the executor is personally liable because the state claims were not resolved first. Each of these mistakes costs more than this guide.

Your download includes the complete 17-chapter guide plus 10 standalone printable worksheets and reference sheets -- a tax waiver decision flowchart, an inheritance tax calculation worksheet, Class C and Class D rate tables, a master deadline tracker, a small estate eligibility worksheet, a final income tax checklist, a real estate sale timeline worksheet, a complete forms reference directory, and a key contacts sheet for the Division of Taxation, all 21 County Surrogates, and the IRS. Each standalone works on its own so you can print the ones you need and keep them at your desk.

30-day money-back guarantee. If the guide does not give you a clear map of every tax obligation, every waiver form, every filing deadline, and every beneficiary-class calculation that applies to your estate -- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New Jersey Tax After Death Checklist -- a one-page overview of the tax waiver forms, critical deadlines, and key numbers that most executors do not discover until the bank has already frozen the accounts and the eight-month interest clock has started running.

You did not choose this job. But you can choose to do it right. The guide gives you the forms, the deadlines, the calculations, and the filing sequence -- so the next eight months are spent clearing the estate correctly, not discovering the mistakes you already made.