The IRS Wants the Final Income Tax Return. New York State Wants the ET-706 Filed Within Nine Months or the Entire Estate Gets Taxed From Dollar One. The Surrogate's Court Wants Letters Testamentary Before the Bank Will Unfreeze a Single Account. The Co-op Board Wants a Separate Transfer Package That Has Nothing to Do With Real Estate Law. You Are Settling an Estate in New York, and Nobody Told You There Are Four Separate Tax Returns With Four Separate Deadlines.

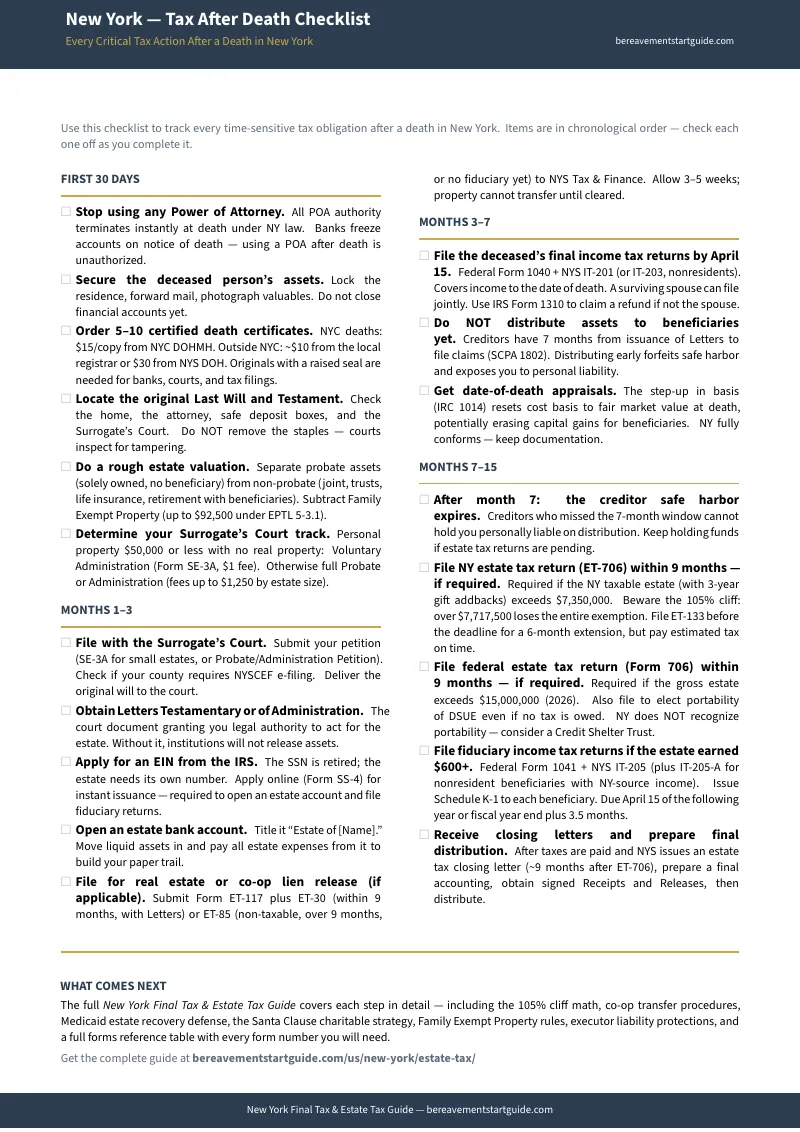

You called the New York State Department of Taxation and Finance to ask about taxes after the death. They told you Form ET-706 is due nine months from the date of death and that the final individual return is due April 15. You asked which one to file first. They said to consult a tax professional. You called the bank to access the deceased's accounts. They said they froze everything the moment they received the death certificate and will not release a dollar until you present Letters Testamentary from the Surrogate's Court. You tried to use the existing Power of Attorney to pay funeral expenses from the deceased's checking account. The bank said the POA terminated the instant the principal died under New York General Obligations Law. That document is worthless now.

You searched online. You found Nolo explaining the New York estate tax threshold. You found FindLaw summarizing the difference between estate tax and inheritance tax. You found three elder law firms in Westchester and Long Island publishing blog posts about the estate tax "cliff" that ended with "schedule a free consultation" and $5,000 retainer agreements. You found the IRS Publication 559 explaining Form 1041 but saying nothing about New York's Form IT-205, the IT-205-A fiduciary allocation schedule, or the known e-filing glitch where the IT-205-A must be submitted even when it is left entirely blank. Nobody connected the federal and state requirements into one filing sequence. Nobody told you what order to file in.

Meanwhile, critical tax decisions are compounding. New York's 2026 estate tax exemption is $7,350,000 — but unlike the federal system, which taxes only the amount above the threshold, New York uses a phase-out "cliff." If the taxable estate exceeds the exemption by more than 5% — above $7,717,500 — the entire exemption disappears and the full estate is taxed from the first dollar at rates from 3.06% to 16%. An estate worth $7,800,000 can owe over $700,000 in New York estate tax that an estate worth $7,350,000 would owe nothing on. New York does not recognize federal portability, so a surviving spouse cannot claim the deceased spouse's unused exemption for state purposes — a planning tool available federally but completely absent at the state level. If the estate includes a Manhattan or Brooklyn cooperative apartment, the co-op is classified as personal property — shares in a corporation and a proprietary lease — not real estate. It transfers through Surrogate's Court with different letters, different appraisal rules, and a co-op board approval process that has nothing to do with the deed system. If the estate was structured around the new Transfer-on-Death deed statute enacted in July 2024, the property bypasses probate but carries an 18-month creditor clawback window during which title insurance companies refuse to issue clean title. Every one of these issues is governed by a different section of New York law, administered by a different agency, with different deadlines and different consequences for getting it wrong.

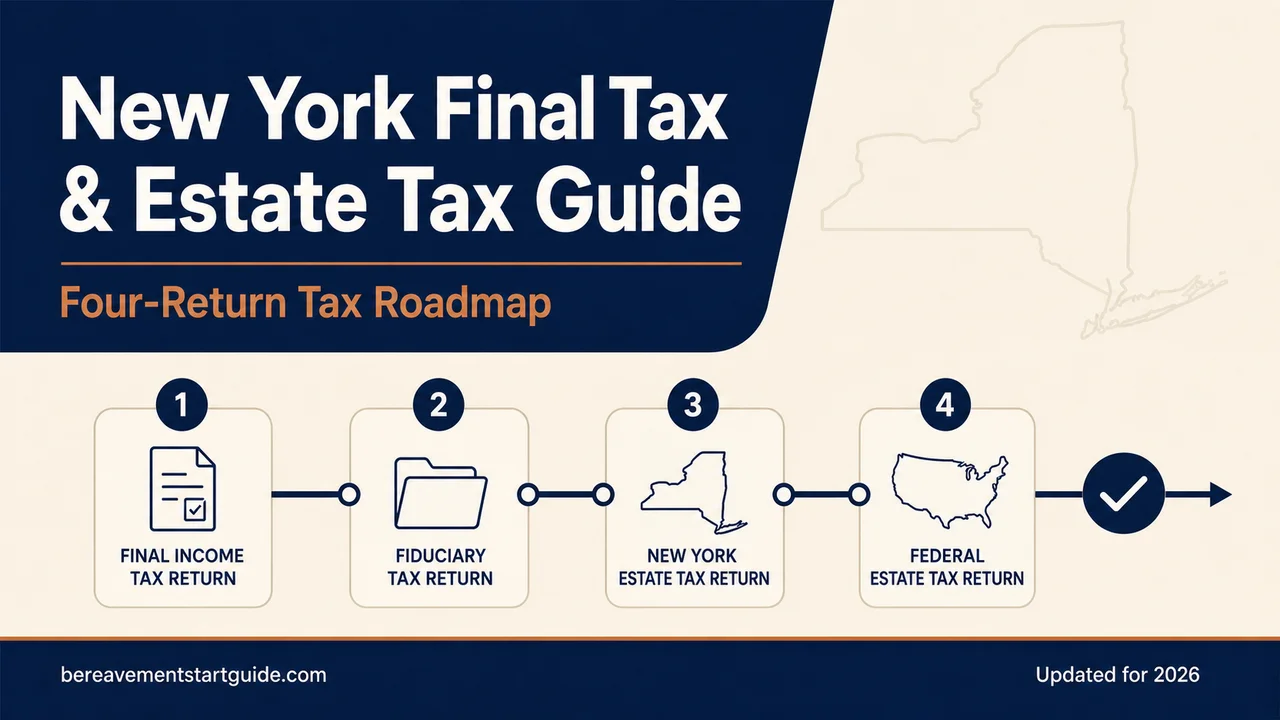

The New York Final Tax & Estate Tax Guide is a Four-Return Tax Roadmap for every tax return, form, deadline, and filing obligation an executor or beneficiary faces after a death in New York. Not a generic national estate tax primer with New York's name attached. Not a law firm blog designed to generate $5,000 retainer agreements. A plain-English, New York-specific manual that tells you what the Department of Taxation and Finance forms, the Surrogate's Court filing instructions, and the IRS publications cannot: which taxes actually apply to your estate, which forms to file, in what order, by which deadlines, and which common mistakes create personal liability for the executor.

What's Inside the Four-Return Tax Roadmap

A step-by-step guide, a tax obligations checklist, and standalone reference sheets covering every tax return, filing obligation, and asset transfer decision an executor or beneficiary faces after a death in New York, built on the Estates, Powers and Trusts Law (EPTL), the Surrogate's Court Procedure Act (SCPA), the New York Tax Law, and IRS Publication 559 — not a generic template repurposed with New York terminology:

Final Income Tax Returns: Federal Form 1040 and New York IT-201

The deceased's final individual tax returns must be filed for the year of death. The guide walks you through the federal Form 1040 and New York Form IT-201 filing process step by step — how a surviving spouse can elect to file jointly for the final year, what income must be reported on the decedent's return versus the estate's return, how to handle income received after death but earned before death (income in respect of a decedent), and the documentation the Department of Taxation and Finance requires. The April 15 deadline applies regardless of probate status. You must write "Deceased," the decedent's name, and the date of death across the top of the paper return, and use IRS Form 1310 to claim any refund due to the deceased.

New York Fiduciary Income Tax: Form IT-205 Decoded

If the estate earns any income during administration — rental payments, stock dividends, bank interest, business income, co-op maintenance refunds — a separate New York Fiduciary Income Tax Return (Form IT-205) is mandatory. This is the filing most executors miss entirely, because nothing in the Surrogate's Court process alerts you to its existence. The guide explains the trigger threshold, the filing deadline, how income is allocated among beneficiaries, and the critical IT-205-A fiduciary allocation schedule — including the known e-filing requirement where IT-205-A must be submitted even when left blank for electronic filing to process, and the specific handling when all income is distributed to nonresident beneficiaries. The guide connects the federal Form 1041 to the state IT-205, step by step.

The New York Estate Tax Cliff: Form ET-706 and the 105% Threshold

The New York State Estate Tax Return (ET-706) is due exactly nine months from the date of death. This is the single highest-stakes tax filing in the estate and the one governed by the most punitive structure in the nation. The 2026 basic exclusion amount is $7,350,000. If the taxable estate exceeds the exclusion by more than 5%, the entire exemption is wiped out and the full estate is taxed from the first dollar. The guide explains the cliff mathematics in concrete dollar terms, the phase-out zone between $7,350,000 and $7,717,500, the graduated rate schedule from 3.06% to 16%, and the "Santa Clause" charitable deduction strategy — a provision drafted into wills to artificially reduce the estate below the cliff threshold through charitable bequests, saving heirs hundreds of thousands of dollars. Filing extensions are available but the estimated tax must be paid within the original nine months to avoid compounding interest and penalties.

No Portability in New York: Why the Federal Rule Does Not Apply

Under federal law, a surviving spouse can elect portability to claim the deceased spouse's unused estate tax exclusion. New York does not recognize this rule. A surviving spouse in New York cannot inherit the deceased partner's unused state exemption, period. This means every New York estate must be planned and valued independently for state purposes, regardless of what the federal Form 706 allows. The guide explains the practical consequences of no portability, how to determine whether filing a federal Form 706 solely for portability is worth the cost, and how the state and federal calculations diverge for married couples.

Step-Up in Basis: Common Law Rules for New York

When you inherit property, the tax basis resets to the fair market value on the date of death — potentially eliminating decades of capital gains. But New York is a common law state, not a community property state. If a house was jointly owned with a surviving spouse, only the deceased spouse's 50% share receives the step-up. The surviving spouse's original cost basis for their half remains intact, creating complex future capital gains calculations when the property is eventually sold. The guide explains how to document the step-up for New York residential real estate, investment property, and cooperative apartment shares, including the alternate valuation date election available to estates filing Form 706.

NYC Cooperative Apartments: Personal Property, Not Real Estate

In New York City, cooperative apartments are classified as personal property — shares of stock in a corporation paired with a proprietary lease — not real estate. This distinction changes everything about how they are appraised, transferred, and sold after death. Co-ops do not transfer through deeds. They require separate Surrogate's Court Letters, a board-approved transfer package, and an appraisal methodology based on comparable share prices and lease terms rather than standard real property comparables. The guide covers the co-op transfer process from Surrogate's Court through board approval, the valuation approach for estate tax purposes, and the specific fiduciary obligations that differ from traditional real estate.

Transfer-on-Death Deeds: The 18-Month Creditor Window

New York enacted a Transfer-on-Death (TOD) deed statute in July 2024 allowing real property to bypass probate entirely. But the statute carries an 18-month creditor clawback provision. If the estate is insolvent, creditors can reach back into TOD property for eighteen months after death. Title insurance companies are aware of this provision and many refuse to issue clean title policies to beneficiaries attempting to sell before the window closes. The guide explains when a TOD deed actually protects the property, when the creditor window creates real exposure, and how to navigate the title insurance obstacle during the waiting period.

Medicaid Estate Recovery: New York's Probate-Only Rule

If the deceased received Medicaid long-term care benefits, the state will initiate an estate recovery claim. But since 2011, New York has operated strictly as a "probate-only" recovery state. The state can only recover from assets that pass through the formal probate estate. Non-probate assets — living trusts, joint tenancies, payable-on-death accounts, and TOD designations — are entirely shielded from recovery. Recovery is prohibited while a surviving spouse is alive, or if there is a surviving child under 21, blind, or disabled. The guide explains the exact scope of recovery authority, the assets that are protected, and the exemptions that prevent recovery against the family home in most situations.

Executor Liability and Commissions

An executor has a strict fiduciary duty under New York law and can be held personally liable for unpaid taxes if they distribute assets to beneficiaries before clearing all estate debts and tax liens. Executor commissions in New York are set by SCPA Section 2307 on a sliding percentage scale, and those commissions are classified as taxable personal income to the executor. The guide covers the commission calculation, the personal income tax obligation, and the specific sequence of distributions that protects executors from personal liability — pay taxes first, distribute to beneficiaries last.

Who This Guide Is For

- The executor who just learned the estate exceeds $7,350,000 and is terrified of the cliff — who needs to understand the exact mathematics of the 105% phase-out zone before filing the ET-706, and whether a charitable deduction or other planning strategy can bring the taxable estate below the threshold before the nine-month deadline

- The executor who discovered the estate earned income during probate — who has never heard of Form IT-205, does not know the filing deadline, and cannot determine whether the estate's rental income, stock dividends, or interest triggers a fiduciary return that nobody in the Surrogate's Court process mentioned

- The surviving spouse trying to understand why portability does not apply in New York — who assumed the deceased spouse's unused exemption would carry over to their own estate, and now needs to understand the state-level planning implications of New York's refusal to recognize the federal portability election

- The beneficiary preparing to sell an inherited co-op apartment in Manhattan or Brooklyn — who assumed it transfers like real estate but now faces a co-op board transfer process, a different appraisal methodology, and Surrogate's Court Letters specific to personal property

- The family relying on a Transfer-on-Death deed who cannot get clear title — who structured the estate around the new TOD statute to avoid probate, and now finds the title company refusing to insure the property until the 18-month creditor window closes

- The adult child settling a parent's estate from another state — who is coordinating final returns, fiduciary returns, ET-706 filings, and beneficiary distributions across New York and federal jurisdictions and needs every form, deadline, and filing sequence in one document

Why Free Resources Will Not Get You Through This

New York tax and estate information exists. The Department of Taxation and Finance publishes forms and instructions, the Unified Court System publishes Surrogate's Court forms, and the IRS publishes Publication 559 on estate taxes. Here is what you actually encounter when you try to navigate estate taxes using free sources:

- The Department of Taxation and Finance publishes ET-706 and IT-205 instructions — in statutory language for CPAs. The instructions assume you already understand the cliff calculation, fiduciary allocation schedules, and the interaction between the New York estate tax and federal Form 706. They tell you which lines to fill in. They do not tell you whether your estate triggers the cliff, how to calculate whether the 105% threshold applies, or that the IT-205-A must be submitted even when blank for electronic filing to process.

- The IRS publishes Publication 559 — covering federal rules only. Publication 559 explains federal estate tax, final income tax, and fiduciary returns. It has zero information about New York-specific filings: no ET-706 cliff calculation, no IT-205 fiduciary return, no co-op transfer procedures, no Medicaid probate-only recovery rule. A federal guide cannot navigate a state-level tax system.

- Nolo and FindLaw explain the overview — and stop before the details that matter. National legal aggregators summarize the New York estate tax threshold and explain the difference between estate tax and inheritance tax. They rarely discuss the cliff mathematics, the IT-205-A e-filing requirement, the co-op personal property classification, or the TOD deed creditor window. Their content is accurate at the headline level and absent at the operational level.

- Law firm blogs explain the dangers — and end with a retainer agreement. Every elder law and estate planning firm in Manhattan, Westchester, and Long Island publishes blog posts about executor liability, the estate tax cliff, and Medicaid recovery. The posts are accurate, alarming, and deliberately incomplete. They explain the risk in enough detail to frighten you. They never explain the solution in enough detail to act on it. Every post ends with a consultation invitation at $5,000 or more in retainer fees.

- No free resource connects the four returns into one filing sequence. The IRS handles federal returns. The Department of Taxation and Finance handles state returns. The Surrogate's Court handles estate administration. Each agency knows its own forms and nothing about the others. No free resource tells you that filing the federal Form 1041 feeds directly into the New York IT-205, that the ET-706 must be filed within nine months while the final IT-201 is due April 15, that the IT-205-A allocation schedule has e-filing requirements that the instructions do not explain, or that distributing assets before clearing all tax liens creates personal liability for the executor.

Free resources give you Department of Taxation and Finance instruction manuals written for CPAs, IRS publications that ignore New York filings entirely, national legal summaries that stop before the cliff math, and law firm blogs that end with a $5,000 retainer. The Four-Return Tax Roadmap puts every tax return, form, deadline, and filing sequence into one document, in the order you actually need them.

— Less Than Fifteen Minutes With a New York Estate Attorney

A consultation with a New York probate or estate attorney runs $400 per hour or more in the metro area. A CPA preparing the federal Form 1041, New York IT-205, and ET-706 charges $1,500 to $5,000 depending on estate complexity. A real estate attorney handling a co-op transfer adds another $2,000 to $4,000. This guide costs less than fifteen minutes of professional legal time and gives you the complete New York-specific tax roadmap — every return, every form, every deadline, and the filing sequence that determines whether the executor faces personal liability or not.

Your download includes the complete step-by-step guide covering every tax obligation category, the standalone New York Tax After Death Checklist, and printable reference sheets: the Four-Return Filing Sequence, the ET-706 Estate Tax Cliff Calculator, the IT-205 Fiduciary Return Quick Reference, the Step-Up in Basis Valuation Guide, the Co-op Transfer Checklist, the Medicaid Estate Recovery Quick Reference, the Executor Liability and Commission Worksheet, and the New York Estate Tax Timeline with every federal and state deadline mapped to a calendar. Instant download, no account required.

30-day money-back guarantee. If this guide does not save you hours of confusion with the Department of Taxation and Finance and make the estate tax filing process immediately clearer, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New York — Tax After Death Checklist — an overview of the tax obligations that apply after a death in New York, the key forms and deadlines, and the most common executor mistakes. Enough to understand what you need to file and whether you need the full guide.

Nobody trained you for this. The Department of Taxation and Finance assumes you understand the cliff calculation and fiduciary allocation. The Surrogate's Court assumes you know the difference between real property and personal property transfers. The IRS assumes you can navigate Publication 559 without New York context. You have something none of them provide — a single roadmap that connects all four tax returns into one sequence, with plain-English instructions for each one.