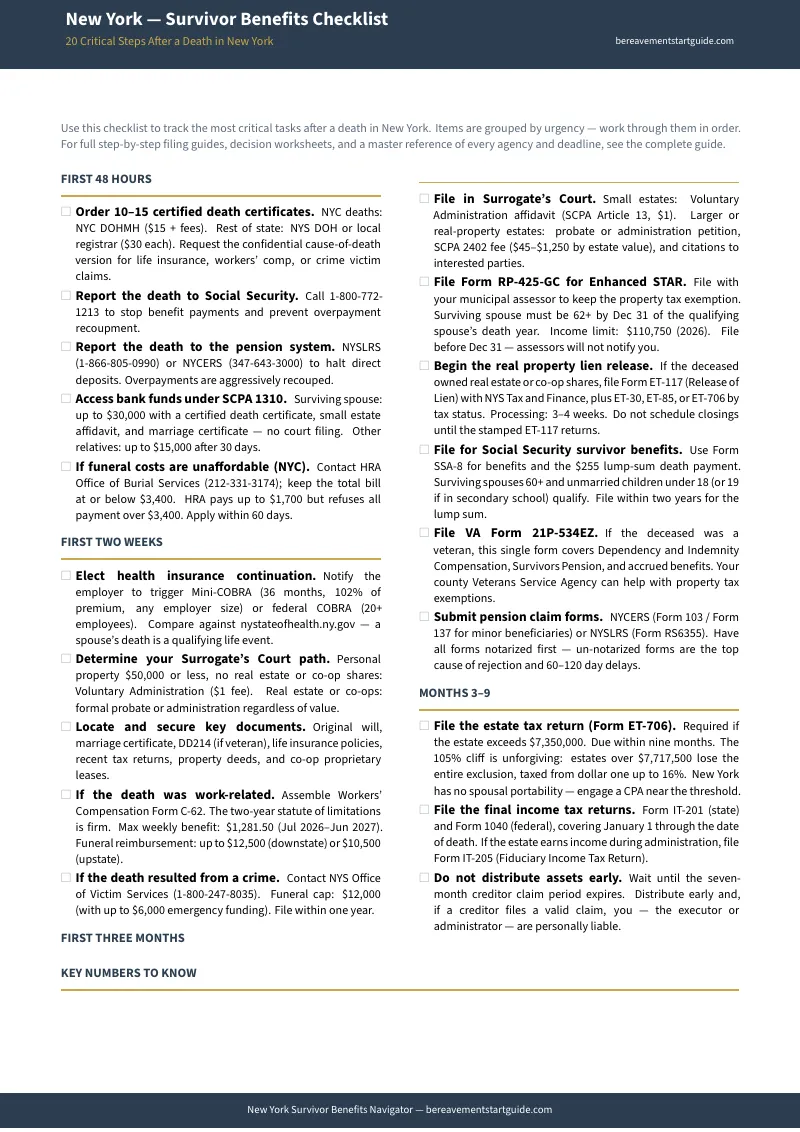

The SSA Says Call Back Monday. NYSLRS Sent a Form You Cannot Decipher. The Surrogate's Court Clerk Says You Need Letters Testamentary Before You Can Do Anything. And Nobody Has Mentioned the $30,000 You Can Collect From the Bank Today Under SCPA 1310.

Someone has died, and now you are the person responsible for figuring out what the surviving family is owed. You called Social Security and spent forty-five minutes on hold before learning that the lump-sum death payment is $255 --- a figure that has not changed in decades and will not cover even the processing fee on a New York death certificate. You called the New York State and Local Retirement System and were told the deceased elected "Option A" at retirement, which means survivor payments depend on a beneficiary designation filed years ago --- and you are not sure whether that designation was ever updated after the divorce. You called NYCERS about a city pension and were told to submit Form 103, but the representative could not explain why the benefit amount differs from what NYSLRS quoted for a state pension with similar service years. And nobody --- not the SSA, not NYSLRS, not the Surrogate's Court --- has told you that under SCPA 1310, a surviving spouse can walk into the bank and collect up to $30,000 from the deceased's account immediately, without probate, without letters testamentary, without waiting.

Meanwhile, benefits are expiring. The workers' compensation death claim requires Form C-62 filed within two years, but the funeral expense reimbursement has a separate clock. NYC HRA's burial assistance caps at $1,700 with a 60-day deadline. The Office of Victim Services has a one-year filing deadline and a $12,000 funeral cap. Your mini-COBRA election window is running. The Enhanced STAR exemption requires Form RP-425-GC before the next tax year's filing deadline. And the estate tax --- New York's 105% cliff provision --- can transform a $7,350,000 exclusion into a tax bill on the entire estate from dollar one if total assets exceed the threshold by even a few thousand dollars. Every agency has its own clock, its own forms, and its own rejection criteria --- and none of them will tell you about the other agencies you should also be contacting.

The New York Survivor Benefits Navigator is a Cross-Agency Benefits Tracker for every federal payment, state pension, city benefit, county program, and statutory entitlement available to surviving families in New York --- from the SCPA 1310 bank collection on day one through unclaimed property recovery months later. Not a grief resource. Not a blog post written by a funeral home or an insurance company trying to sell you a policy. A plain-English, New York-specific administrative reference that tells you which benefits exist, who qualifies, what forms to file, what documents to bring, and which deadlines will permanently disqualify you if you miss them.

What's Inside the Cross-Agency Benefits Tracker

A 19-chapter guide, a quick-start checklist, and 4 reference matrices --- covering every survivor benefit, application process, and statutory deadline that New York families face after a death:

Chapter 1: Immediate Administrative Triage

The first-call sequence that prevents cascading problems. Who to contact first and in what order: financial institutions (the SCPA 1310 right of the surviving spouse to collect up to $30,000 directly from the bank, without probate or court approval --- but you must bring the right documents), public assistance agencies (SNAP and Medicaid reporting requirements), employer HR (final paycheck, group life insurance, mini-COBRA or COBRA election), credit bureaus (obituary-driven identity theft runs rampant in the tri-state area), and the Surrogate's Court clerk in the correct county. Plus the critical distinction between non-probate assets that pass by operation of law and probate assets that require Surrogate's Court involvement --- because New York is strict about which assets require court supervision, and co-op apartments are treated as personal property, not real estate.

Chapter 2: Document Consolidation

Every agency demands certified originals and every agency has different requirements. New York death certificates cost $30 from the state or $15 from NYC's Office of Vital Records plus processing fees --- and you will need 10 to 15 of them because banks, insurers, and pension systems all require certified originals they will not return. The master document checklist tells you exactly what to gather before you file anything: death certificates, marriage certificate, divorce decree, Social Security numbers, birth certificates, the will (if one exists), and the specific forms each pension system requires. Having the full package ready when you walk into the Surrogate's Court eliminates the most common cause of delay and rejection.

Chapter 3: Social Security Survivor Benefits

The $255 lump-sum death payment, ongoing survivor annuities, and every age rule and eligibility exception the SSA applies. Full retirement age benefits vs. reduced benefits starting at age 60 (or age 50 with a qualifying disability). The child-in-care exception that lets a surviving spouse of any age collect benefits. The divorced spouse rule requiring 10+ years of marriage. Why the Government Pension Offset and Windfall Elimination Provision no longer reduce benefits for New York public employees who paid into a state pension instead of Social Security — both were repealed for benefits payable January 2024 onward — including how to tell whether either ever applied to a NYSLRS or NYCERS pension, how to check the SSA paid the retroactive catch-up it owes you, and why a restored benefit can put your Enhanced STAR exemption at risk. The forms: SSA-10 for widow/widower claims, SSA-5 for child-in-care, SSA-3368 and SSA-827 for disability-based applications.

Chapter 4: NYSLRS Pension Survivor Benefits

The New York State and Local Retirement System administers pensions for state employees, local government workers, and police/fire members through the Employees' Retirement System (ERS) and the Police and Fire Retirement System (PFRS). The guide covers the retirement option the member selected at enrollment --- Option A, B, C, D, or E --- and the permanent consequences each option has for survivor payments. The ordinary death benefit calculation. The accidental death benefit for line-of-duty deaths. The post-retirement death benefit. The required forms, the beneficiary designation rules, and the common traps: a beneficiary designation filed before a divorce that was never updated, a second marriage that triggers automatic revocation of the prior spouse's designation, and the difference between a lump-sum payout and a lifetime monthly annuity.

Chapter 5: NYCERS and NYC Teachers' Retirement Survivor Benefits

New York City employees belong to separate pension systems that operate independently of NYSLRS. NYCERS covers city workers outside of police, fire, and teachers. The NYC Teachers' Retirement System covers DOE employees. Each system has its own survivor benefit rules, its own forms (NYCERS Form 103 for survivor claims, Form 137 for claims involving minor beneficiaries), and its own processing timelines. The guide covers both systems, including the in-service death benefit, the post-retirement death benefit, and the specific documentation each system requires --- because filing the wrong form with the wrong system is one of the most common mistakes city employee families make.

Chapter 6: VA Burial Allowances and New York Veterans Benefits

Federal VA burial benefits, Dependency and Indemnity Compensation, the Fully Developed Claim program that cuts processing time, and every New York-specific veteran entitlement. The service-connected and non-service-connected burial allowances. The New York State Division of Veterans' Services and the county-level veterans service agencies that provide free advocacy. The real property tax exemption for Gold Star families and surviving spouses of veterans who died from service-connected causes. The Veteran Burial Fund administered by the Division of Veteran's Services. The county VSO system and how to use it.

Chapters 7-9: Employer Benefits, Unpaid Wages, and Tax Refunds

New York mini-COBRA provides 36 months of continuation coverage at 102% of the group premium --- and unlike federal COBRA, it covers employers with fewer than 20 employees, which means surviving families of workers at small businesses have health insurance rights that families in most other states do not. The guide covers the mini-COBRA election timeline, employer notification requirements, and the interaction between state and federal continuation. Plus unpaid wage recovery (the surviving spouse's right to collect final wages), 401(k) death-year Required Minimum Distribution waivers, group life insurance claims, and IRS Form 1310 for claiming a federal tax refund owed to the deceased.

Chapter 10: Workers' Compensation Death Benefits

When death results from a workplace injury or occupational disease, New York's workers' compensation system provides income replacement of two-thirds of the deceased's average weekly wage, capped at $1,281.50 per week (effective July 2026 through June 2027). Benefits continue for the duration of dependency. Funeral expenses are reimbursed up to $12,500 for downstate counties (New York City, Nassau, Suffolk, Westchester, Rockland, Putnam, Orange, Dutchess) or $10,500 for the rest of the state. The claim requires Form C-62 filed with the Workers' Compensation Board within two years of the date of death --- and the distinction between an accidental injury claim and an occupational disease claim matters because they trigger different sections of the Workers' Compensation Law.

Chapter 11: Enhanced STAR and Property Tax Exemptions

New York's Enhanced STAR exemption provides property tax savings for seniors 65 and older --- and a surviving spouse aged 62 or older can retain the exemption if the household income falls below the $110,750 limit (2026 threshold). The application requires Form RP-425-GC filed with the local assessor. The guide also covers the veterans' real property tax exemptions under RPTL sections 458 and 458-a, the Senior Citizens Homeowners' Exemption (SCHE), and the Disabled Homeowners' Exemption (DHE) --- because the interaction between these exemptions is county-specific, and losing one can trigger reassessment of others.

Chapter 12: Crime Victims Compensation

The New York Office of Victim Services provides compensation for deaths caused by criminal conduct, with a $12,000 funeral expense cap, up to $6,000 in emergency awards for immediate needs, and ongoing support for counseling and lost wages. The OVS is a payer of last resort --- it covers only expenses not reimbursed by insurance or other sources. Filing deadline: one year from the date of death, though extensions are available in limited circumstances. The guide covers the application process, the required police report documentation, and the common reasons claims are denied.

Chapter 13: Voluntary Administration and Small Estate Shortcuts

If the estate's personal property (excluding real estate) totals $50,000 or less, a surviving spouse or eligible family member can file a Voluntary Administration petition with the Surrogate's Court for a $1 filing fee --- avoiding full probate entirely. But the threshold is strict: it applies only to personal property, which means co-op apartments (classified as personal property in New York, not real estate) count toward the $50,000 limit while condos (classified as real property) do not. The guide covers the exact threshold calculation, the petition process, and the conditions that disqualify an estate from using this streamlined procedure.

Chapter 14: New York Estate Tax and the 105% Cliff

New York imposes its own estate tax with a $7,350,000 exclusion (2026) --- but the exclusion works as a cliff, not a phase-out. If the taxable estate exceeds 105% of the exclusion amount, the entire estate is taxed from dollar one at rates up to 16%. There is no portability between spouses (unlike the federal exemption). The guide covers Form ET-706 filing, the required Release of Lien form ET-117 (which must be filed before any real property can be transferred, even if the estate falls below the tax threshold), the 7-month creditor claim period that affects estate settlement timing, and the interaction between the state estate tax and the federal estate tax. For families with assets near the cliff, a few thousand dollars can mean a tax bill in the hundreds of thousands.

Chapters 15-16: Public Assistance, Medicaid, and NYC HRA

If the deceased received SNAP, TANF, Medicaid, or other public assistance, the surviving household faces mandatory reporting deadlines and potential benefit termination. The guide covers Medicaid estate recovery in New York --- limited to probate assets after the 2012 repeal of broader recovery authority, which means jointly held property, payable-on-death accounts, and assets with named beneficiaries are shielded. Plus the NYC Human Resources Administration burial assistance program: up to $1,700 toward funeral costs, with a total bill cap of $3,400, and a strict 60-day application deadline that most families miss.

Chapters 17-19: Unclaimed Property, Life Insurance, and Fraud Protection

How to search for unclaimed property through the New York State Comptroller's Office of Unclaimed Funds. How to locate lost life insurance policies using the free NAIC Policy Locator and New York's own life insurance policy locator service. And a complete fraud protection chapter covering obituary-driven identity theft, the deceased's credit freeze process, and the IRS identity protection PIN --- particularly critical in New York, where the density of financial accounts per capita makes estates a high-value target for fraud.

4 Reference Matrices

Printable tools designed to be used independently: the New York Survivor Benefit Eligibility Map (every benefit matched to every persona type), the Form Index and Application Tracker (every form number, agency, and submission method in one table), the Deadline Calendar (every time-sensitive filing organized chronologically), and the Denial Management and Appeal Pathways (what to do when a claim is rejected).

Who This Guide Is For

- The surviving spouse who just lost the household's primary income --- who needs to know how to file for Social Security survivor benefits, whether the NYSLRS or NYCERS pension continues, how to collect up to $30,000 from the bank under SCPA 1310, what happens to the health insurance under mini-COBRA, and whether the Enhanced STAR exemption survives. The guide maps the entire income replacement and benefit preservation sequence from the first phone call through monthly benefit activation.

- The adult child who just became an accidental executor --- who has been named in the will but has never dealt with Surrogate's Court, does not know the difference between letters testamentary and letters of administration, and needs to figure out which benefits to claim, which forms to file, and which deadlines are running. The guide gives you the chronological action plan, the document checklist, and the cross-agency filing sequence so you can process everything systematically.

- The out-of-state executor dealing with New York from a distance --- who needs to understand Surrogate's Court procedures, New York-specific forms, and the ET-117 Release of Lien requirement for real property transfers. The guide consolidates every New York-specific procedural requirement so you are not learning the state's system through trial and error from another time zone.

- The family of a worker killed on the job --- who needs to file Form C-62 with the Workers' Compensation Board, claim up to $1,281.50 per week in survivor benefits and up to $12,500 in funeral reimbursement, and understand why downstate and upstate funeral caps differ. The guide covers the full workers' compensation death benefit process, including the occupational disease distinction.

- The family of a crime victim --- who may not know that the Office of Victim Services provides up to $12,000 for funeral expenses and $6,000 in emergency awards, with a one-year filing deadline that no agency will proactively communicate. The guide covers the full OVS application process, the police report requirements, and the common denial reasons.

- The family worried about Medicaid estate recovery --- who needs to know that New York's 2012 repeal limits recovery to probate assets only, that jointly held property and payable-on-death accounts are shielded, and that the NYC HRA burial assistance program has a 60-day deadline and a $3,400 total bill cap that most families discover too late. The guide maps the Medicaid landscape so you know which assets are protected and which are at risk.

Why Free Resources Leave Money on the Table

Survivor benefit information exists. It is spread across the Social Security Administration in one set of forms, the VA in another, NYSLRS in a third, NYCERS in a fourth, the Workers' Compensation Board in a fifth, the Surrogate's Court in a sixth, the Office of Victim Services in a seventh, and county offices that maintain wildly inconsistent websites across 62 counties. Here is what happens when you try to navigate all of this yourself:

- The SSA website covers Social Security benefits. It does not mention NYSLRS pensions, NYCERS pensions, Enhanced STAR, or the SCPA 1310 bank collection right. Every federal agency covers only its own programs. If you stop at Social Security, you miss everything New York provides at the state, city, and county level.

- NYSLRS covers state pensions. NYCERS covers city pensions. Neither explains the other. A surviving spouse of a New York City employee who also had state service could have benefits in both systems --- and filing with one does not trigger notification from the other. If you do not know to check both, you miss one.

- The Surrogate's Court website provides filing instructions for probate. It does not explain survivor benefits, pension claims, or workers' compensation. The court handles estate administration, not benefit navigation. Families who focus only on the probate process miss the benefit claims that have shorter deadlines and higher dollar values than the estate itself.

- Benefits.gov provides a broad overview of national programs. It lacks New York-specific procedural details. It will not tell you about the 105% estate tax cliff, the co-op vs. condo distinction for Voluntary Administration, the ET-117 Release of Lien requirement, or the $12,500 vs. $10,500 workers' compensation funeral cap split. When you need to file an actual claim in New York, you need New York statute numbers and New York forms --- not a national overview.

- Hiring a New York estate attorney for straightforward benefit claims is the most expensive possible solution. A New York estate attorney charges $350-$600 per hour. For a surviving spouse who simply needs to know which forms to file with which agencies in which order, a legal retainer is a disproportionate expense for what is fundamentally an organizational problem --- not a legal one.

Free resources give you one agency at a time, with no sequencing, no cross-referencing, and no way to know what you are missing. The Cross-Agency Benefits Tracker maps every benefit to every persona, organizes every form by deadline, and tells you exactly which agencies to contact in which order --- so you can claim everything your family is owed without spending weeks navigating portals that were never designed to talk to each other.

--- Less Than One Hour of a New York Estate Attorney's Time

New York families leave thousands of dollars in unclaimed survivor benefits every year --- not because they are ineligible, but because no one told them the benefit existed. A surviving spouse does not collect $30,000 from the bank under SCPA 1310 because no one explained that the right exists. A pension survivor benefit goes unclaimed because the family filed with NYSLRS but did not know about the separate NYCERS claim. An Enhanced STAR exemption worth thousands over the surviving spouse's lifetime lapses because nobody mentioned Form RP-425-GC. A workers' compensation death benefit of $1,281.50 per week goes unfiled because the family assumed the employer's insurance would contact them. This guide costs less than any of those lost benefits and tells you where to find every one of them.

Your download includes the complete 19-chapter guide, the New York Survivor Benefits Quick-Start Checklist, and 4 printable reference matrices --- the Survivor Benefit Eligibility Map (every benefit matched to every persona), the Form Index and Application Tracker (every form number and agency in one table), the Deadline Calendar (every time-sensitive filing organized chronologically), and the Denial Management and Appeal Pathways (what to do when a claim is rejected). Print the ones you need. Use them independently or alongside the full guide.

30-day money-back guarantee. If the guide does not give you a clear map of every survivor benefit available to your family, every form you need to file, and every deadline you need to meet --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New York Survivor Benefits Checklist --- a summary of the most time-sensitive actions, deadlines, and forms that most families do not discover until it is too late. Enough to start contacting the right agencies in the right order.

You did not plan for this. But you can plan what happens next. The guide gives you the benefits, the forms, the deadlines, and the filing sequence --- so the next six months are spent claiming what your family is owed, not discovering what you missed.