Your CPA Charges $300 an Hour to Sort Through a Shoebox. The Ohio Department of Taxation Assumes You Already Know Which Forms Apply. The IRS Covers Federal Requirements and Nothing Else. And Nobody Mentioned That Ohio Repealed Its Estate Tax a Decade Ago --- But Left Six Other Tax Obligations in Its Place.

Someone died in Ohio, and now you are the person responsible for their taxes. You have a stack of W-2s and 1099s addressed to someone who is no longer alive. You do not know whether that income belongs on the deceased's final individual return or on the estate's fiduciary return. You searched "Ohio estate tax" and found a dozen articles --- half of them still referencing the pre-2013 tax that no longer exists. You called the county probate court and learned that Ohio has 88 counties, each with its own local rules, fee schedules, and addendum requirements layered on top of the Standard Probate Forms. And nobody told you that the $100,000 Release from Administration threshold for surviving spouses is different from the $35,000 threshold for everyone else.

Meanwhile, the IRS covers its own forms and assumes you will figure out Ohio's. The Ohio Department of Taxation publishes IT 1041 instructions written for tax professionals, not for grieving family members handling this for the first time. CPA firm blogs give you enough information to realize you need help, then invite you to schedule a $300-per-hour consultation. And no single source connects the federal requirements, the state requirements, the municipal tax requirements, and the 88-county probate variations into a sequence you can actually follow.

The Ohio Final Tax & Estate Tax Guide is a Tax Sequence Navigator for every tax obligation that follows a death in Ohio --- from the immediate EIN application through the final estate closure. Not a tax preparation manual. Not a substitute for a CPA. A structured, Ohio-specific roadmap that tells you which forms apply, which deadlines you cannot miss, which documents to gather from the deceased's records, and how to organize everything so your CPA spends their time preparing returns instead of billing you $300 an hour to figure out what you brought.

What's Inside the Tax Sequence Navigator

A 17-chapter guide plus a quick-start checklist --- covering every tax obligation, every form, every deadline, and every document-gathering step that Ohio executors, surviving spouses, trustees, and beneficiaries face after a death:

Chapter 1: Ohio's Tax Landscape After Death --- The Relief You Need to Hear

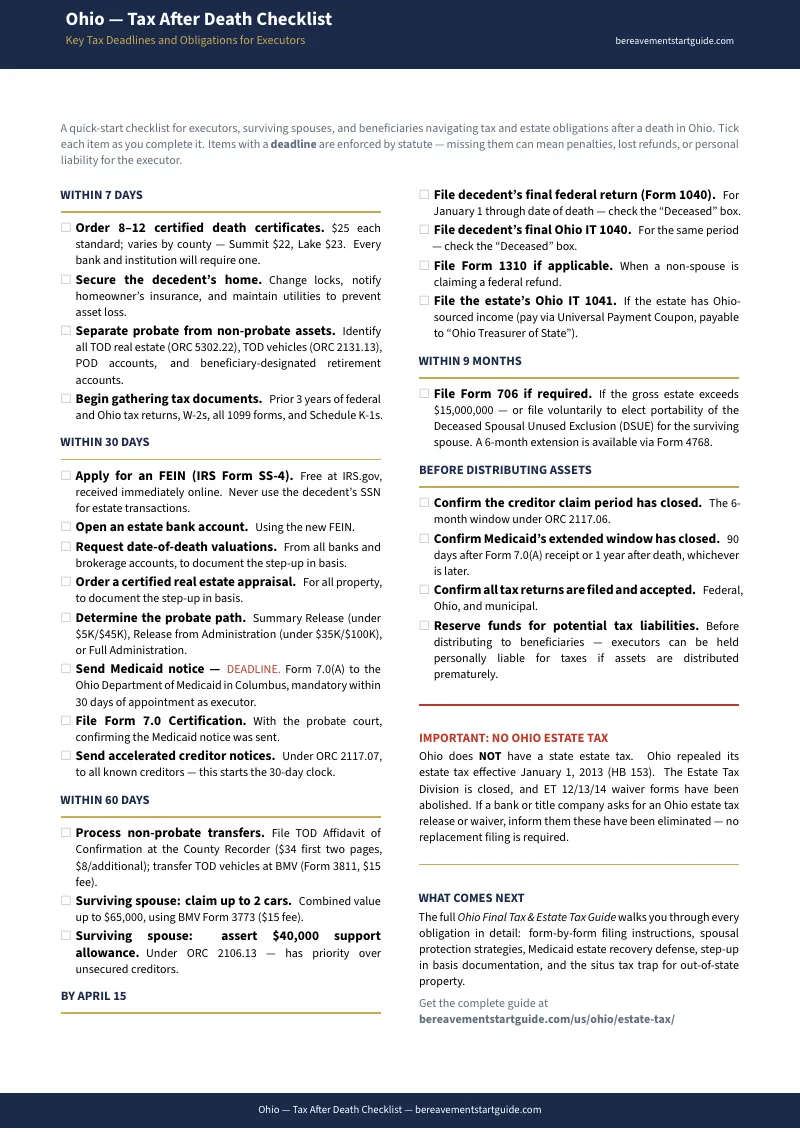

The single most important fact for most Ohio families: Ohio repealed its estate tax effective January 1, 2013, via House Bill 153. The ET 12, ET 13, and ET 14 waiver forms have been abolished. The Estate Tax Division is closed. If a bank or title company asks for an Ohio estate tax release, they are wrong. This chapter confirms what you can stop worrying about --- and immediately redirects your attention to the six categories of tax obligation that remain.

Chapter 2: The First 15 Days --- Urgent Steps That Affect Taxes

Death certificate ordering and costs by county. Asset security protocols. The critical separation of probate vs. non-probate assets --- TOD designations, POD accounts, joint tenancy, and beneficiary designations that transfer automatically. Getting a FEIN (and the warning never to use the deceased's SSN for estate transactions). Opening the estate bank account. Notifying agencies before filing any returns.

Chapter 3: Probate Path Selection --- Which Track You Are On

Ohio's three probate tracks and how to choose: Release from Administration ($100,000 for surviving spouses, $35,000 for other heirs), Summary Release from Administration (the simplest path for the smallest estates), and Full Administration. The decision flowchart that determines which Standard Probate Forms you need and which county-specific addendums may apply.

Chapter 4: Filing the Final Income Tax Return

The deceased's tax year ends on the date of death. How to file the federal Form 1040 and Ohio IT 1040. The April 15 deadline. Joint return rules for surviving spouses. How to claim a refund using IRS Form 1310. The municipal income tax obligation --- RITA vs. CCA jurisdictions and why this catches executors off guard.

Chapter 5: The Surviving Spouse's Rights and Protections

The mansion house right (two vehicles, $40,000 personal property allowance, one year of rent-free residence). The $100,000 Release from Administration shortcut. The BMV surviving spouse affidavit for vehicles up to $65,000 combined value. Why date-of-death appraisals are non-negotiable for the step-up in basis.

Chapter 6: Estate Income Tax --- Ohio IT 1041

The estate becomes a separate taxable entity at death. When Ohio requires IT 1041. The golden rule: estates only pay tax on retained income --- if income is distributed to beneficiaries, the tax liability follows the distribution. FEIN requirement. The interaction between federal Form 1041 and Ohio IT 1041. K-1 schedules for beneficiaries.

Chapter 7: Federal Estate Tax --- The $15 Million Decision Tree

The One Big Beautiful Bill Act set the 2026 federal exemption at $15 million per individual. The Form 706 portability election: why surviving spouses must file even when no tax is due --- to capture the deceased spouse's unused exclusion and create a $30 million future shield. The 9-month filing deadline.

Chapter 8: Step-Up in Basis

Inherited assets receive a basis adjustment to fair market value at date of death. How this works in Ohio's common-law property framework. Why the step-up effectively eliminates capital gains tax if you sell shortly after death. The double step-up strategy for surviving spouses using QTIP trusts. The documentation you need to prove basis to the IRS.

Chapter 9: Selling Inherited Real Estate in Ohio

Clearing title through probate vs. Transfer on Death designations. The Certificate of Transfer (Form 12.1). How to coordinate with the county recorder. The step-up in basis calculation for real estate and why most families owe far less capital gains tax than they fear. Ohio's county-by-county real estate transfer tax.

Chapter 10: Inherited Retirement Accounts

The hidden tax trap: inherited traditional IRAs and 401(k)s are taxed as ordinary income when withdrawn. The SECURE Act's 10-year distribution rule for non-spouse beneficiaries. Spousal rollover options. How forced distributions can push beneficiaries into higher tax brackets during their peak earning years. The 1099-R documentation strategy.

Chapter 11: Ohio Medicaid Estate Recovery

If the decedent was 55 or older and received Medicaid, Ohio's Department of Medicaid can recover costs from the probate estate. Form 7.0 notification requirements. The mandatory 30-day filing window. Exemptions: surviving spouse, child under 21, blind or disabled dependents. The undue hardship waiver process. Why this applies to every probate estate --- even if you are not sure whether the decedent used Medicaid.

Chapter 12: Municipal Income Tax

Ohio's unique local income tax system. Which municipalities require filings for estate income. RITA vs. CCA jurisdictions. How municipal taxes interact with the Ohio IT 1041. The trap that catches executors who assume county and municipal are the same thing.

Chapters 13-17: Trust Administration, Unclaimed Property, Executor Compensation, CPA Handoff, and Master Deadline Calendar

Trust-to-estate transition procedures and revocable trust tax treatment after the grantor's death. The Ohio Commerce Department unclaimed funds search. Statutory executor compensation (4% on the first $100,000, 3% on the next $300,000, 2% above $400,000) and the fee petition process. The organizational protocol that turns a $450 document-sorting session into a focused return preparation meeting. And the master deadline calendar organizing every filing from the immediate FEIN application through final estate closure.

Plus: The Ohio Tax After Death Checklist

A standalone quick-start reference organized by timeframe --- immediately after death, within 30 days, within 3 months, by April 15, and ongoing until the estate closes. Every deadline, every form number, every action item. Enough to start immediately, even before reading the full guide.

Who This Guide Is For

- The executor who just realized the deceased still owes a tax return --- you have W-2s and 1099s addressed to someone who is no longer alive, you do not know whether to file Ohio IT 1040 or IT 1041, and April 15 is approaching. The guide gives you the filing requirements, the deadlines, and the document list --- organized so your CPA can prepare the returns without billing you for three hours of sorting.

- The surviving spouse navigating the $100,000 threshold --- you know Ohio offers a Release from Administration but are not sure whether you qualify, whether it covers the house, or how to handle the vehicles. The guide explains the threshold, the BMV affidavit for vehicles up to $65,000, and the mansion house protections --- including the step-up in basis for jointly owned property.

- The out-of-state executor managing an Ohio estate remotely --- you live in another state and are trying to decipher Ohio's county-by-county probate variations from 500 miles away. The guide explains which Standard Probate Forms apply, warns about county-specific addendums, and identifies the municipal tax obligations that trip up executors unfamiliar with Ohio's local income tax system.

- The adult child sorting through a parent's filing cabinet --- you have a stack of 1099 forms, old tax returns, property tax bills, and retirement account statements. You do not know what is relevant. The guide tells you exactly which documents matter, which ones to discard, and how to sort them into the two piles your CPA needs: pre-death and post-death.

- The family selling inherited property --- you want to sell the house and need to know your tax exposure. The step-up in basis determines whether you owe $0 or $50,000 in capital gains. But the title needs to clear probate first, the Certificate of Transfer requires Form 12.1, and the county transfer tax may apply.

- The beneficiary worried about the IRA distribution --- you inherited a traditional IRA and someone told you it is tax-free because Ohio has no inheritance tax. That is only half true. The IRA distributions are taxed as ordinary income when you withdraw them, the SECURE Act forces you to empty the account within 10 years, and Ohio's state income tax applies on top of the federal tax.

Why Free Resources Leave You Sorting Receipts at $300 an Hour

The information exists. It is spread across a dozen government websites, a hundred CPA blog posts, and a thousand forum threads. Assembling it into a single actionable sequence --- while you are grieving and a dozen deadlines are running simultaneously --- does not.

- IRS.gov covers federal tax forms. It does not cover Ohio IT 1041 filing thresholds, the Release from Administration, the municipal income tax system, or any Ohio-specific rule. It covers its own forms and nothing else.

- The Ohio Department of Taxation publishes form instructions for tax professionals, not for executors handling this for the first time. No chronological workflow, no explanation of how state requirements interact with federal filings, no document-gathering protocol.

- CPA firm blogs are designed to generate $300-per-hour consultations. The article tells you enough to realize you need help. No standalone checklist, no chronological roadmap, no document list you can use independently.

- TurboTax and H&R Block assume you already have every document organized and classified. The software calculates math once the data is entered. It offers zero help in locating documents, separating pre-death from post-death income, or determining which forms apply.

- Nolo and LegalZoom provide national overviews. They will not tell you about the Ohio IT 1041 municipal income tax interaction, the 88-county probate variations, the $100,000 surviving spouse threshold, or the Form 7.0 Medicaid notification requirement.

Free resources answer one agency's questions. The Tax Sequence Navigator answers them all --- in sequence, with deadlines, with the exact forms and documentation, and with the Ohio-specific rules that no single agency or software platform provides.

--- Less Than One Hour of CPA Time

An Ohio CPA charges $200 to $400 per hour for estate and fiduciary work. The typical first meeting --- where the CPA inventories what you brought and tells you what is missing --- costs $300 to $600 before any returns are prepared. The guide costs a fraction of that first meeting and ensures you never need it.

Your download includes the complete 17-chapter guide, the Ohio Tax After Death Checklist, and 6 standalone printable tools: the Deadline Calendar, Probate Path Decision Tree, Step-Up in Basis Worksheet, CPA Document Checklist, Medicaid Recovery Compliance Guide, and Municipal Tax Reference Card. Print the tools you need, use them immediately, and work through the full guide chapter by chapter as each deadline approaches.

30-day money-back guarantee. If the guide does not give you a clear map of every tax obligation, every form, every deadline, and every document you need to gather --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Ohio Tax After Death Checklist --- a summary of the most time-sensitive deadlines, form numbers, and action items that most executors do not discover until they are sitting in a CPA's office being billed for the information.

You did not plan to be the person handling the taxes for someone who died. But the April 15 deadline does not care, the Form 7.0 Medicaid notification has a 30-day window, and every hour your CPA spends sorting paperwork is an hour billed to the estate. This guide turns a fragmented, multi-agency maze into a single organized sequence --- so you walk into your accountant's office prepared, not panicked.