Oklahoma Has No Estate Tax. The State Still Demands Three Tax Returns, a Fiduciary Filing for Every Royalty Check, and a Nine-Month Deadline That Nobody Mentions Until It's Too Late.

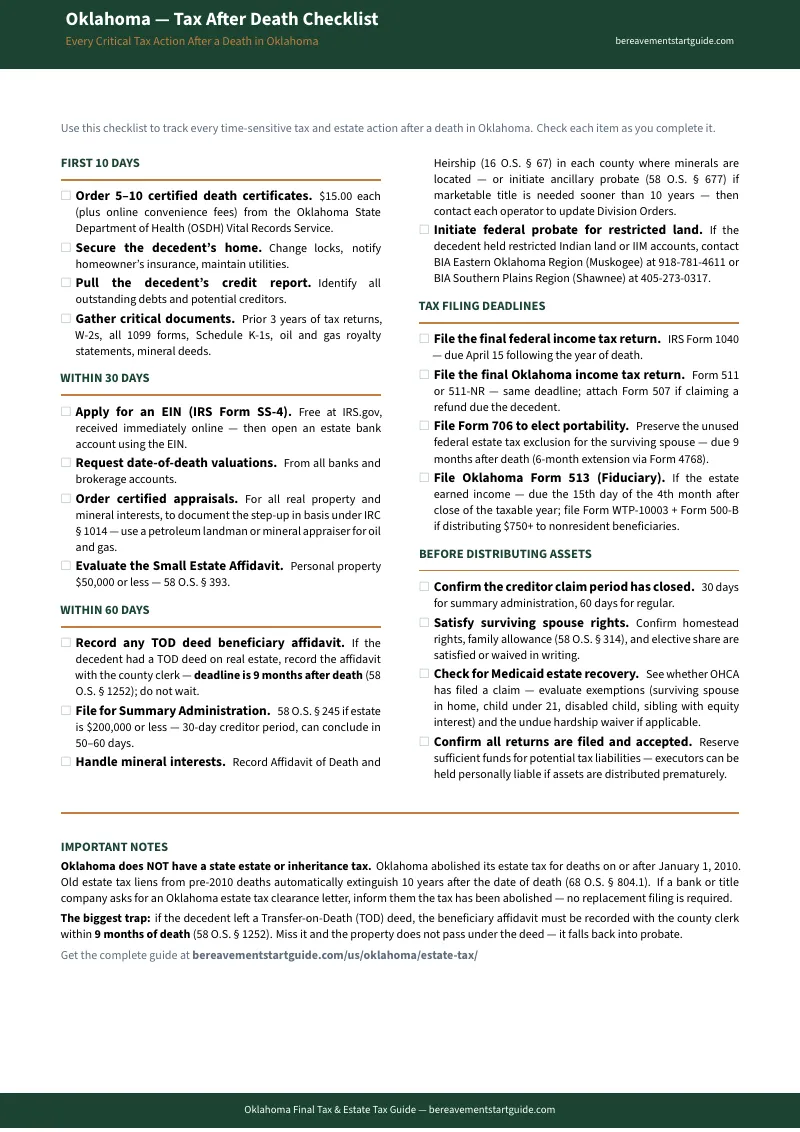

You heard that Oklahoma abolished the estate tax. You assumed that meant the tax side was simple. Then you discovered the deceased earned mineral royalties — and the estate now owes a fiduciary income tax return on Form 513 that you have never seen and no one at the Oklahoma Tax Commission will walk you through. The final Form 511 is due April 15 and the deceased had income from three sources you are still tracking down. The oil company suspended royalty payments until you produce clear title. And buried in the Transfer-on-Death deed paperwork is a nine-month acceptance window that, if missed, forces the property into the very probate the deed was set up to avoid.

The Tax Commission's website has blank forms. The county clerk says they cannot give legal advice. Attorney blogs explain just enough complexity to justify a $3,250 retainer. No single source connects the final income tax to the fiduciary return to the step-up in basis to the Medicaid lien clearance — because those responsibilities are split across four agencies that do not coordinate with each other.

The Tax-First Settlement Sequence — Every Filing in the Right Order

The Oklahoma Final Tax & Estate Tax Guide takes the scattered requirements of the Oklahoma Tax Commission, the IRS, the Oklahoma Health Care Authority, and the county clerk and chains them into one chronological action plan. Form 511 to Form 513 to step-up basis documentation to Medicaid lien clearance to distribution — in the order that prevents penalties, preserves exemptions, and keeps the executor out of personal liability. Not a national template with "Oklahoma" pasted into the header. A guide built around the specific Oklahoma rules that make tax obligations here unlike any other state.

What's Inside

Final Income Tax Return — Form 511 (Residents) and Form 511-NR (Non-Residents)

The deceased's last Oklahoma income tax return, due April 15 of the year after death. The guide covers the specific Oklahoma rules: how to file as a surviving spouse, how to handle Oklahoma income when the decedent lived elsewhere, the Form 507 required to claim a refund due a deceased taxpayer, and the critical rule that Oklahoma does not allow deduction of federal income tax paid on the state return — a trap that overstates the refund if you calculate it wrong.

Fiduciary Income Tax — Form 513 and the Mineral Royalty Trigger

If the estate earns any income after the date of death — and in Oklahoma, mineral royalties make this far more common than in most states — a separate fiduciary return is required. The guide explains when Form 513 is triggered, how to obtain the estate EIN, how to report oil and gas royalties and depletion, and the Oklahoma-specific prohibition on deducting federal income tax paid. Most executors do not learn about Form 513 until a royalty check arrives and they have no idea how to report it.

Step-Up in Basis — The Rule That Saves Oklahoma Families Thousands

Under IRC Section 1014, the tax basis of every inherited asset resets to fair market value at the date of death. For Oklahoma families, this matters enormously: the family farm bought for $40,000 in 1975 that is now worth $600,000 owes zero capital gains tax if sold at that value. Mineral rights acquired decades ago at nominal cost get the same reset. The guide explains how to establish, document, and defend the stepped-up basis — including appraisal requirements and the difference between community property and separate property treatment.

Federal Estate Tax — Form 706 and Portability

The federal estate tax exemption exceeds $15 million per person in 2026. Most Oklahoma estates owe nothing. But the guide covers the threshold calculation, the portability election that lets a surviving spouse claim the deceased spouse's unused exemption, and the specific assets — mineral rights, farm land, oil and gas working interests — that push Oklahoma estates closer to the line than families expect. If the estate exceeds the exemption, the guide maps the Form 706 filing process and tells you when specialized counsel is not optional.

The Nine-Month Transfer-on-Death Deed Trap

A Transfer-on-Death deed lets real property pass outside probate — but the named beneficiary must record an acceptance affidavit with a certified death certificate at the county clerk within exactly nine months of death. Miss it and the deed is void. The property reverts to the estate and is forced into probate. This is not a tax obligation, but it intersects directly with tax planning: the step-up in basis, the fiduciary return trigger, and the Medicaid lien all depend on whether the property transferred cleanly or fell back into the estate. The guide sequences this deadline into the tax timeline so it cannot be missed.

Medicaid Estate Recovery — The Lien Aimed at the Family Home

If the deceased was 55 or older and received SoonerCare nursing-facility benefits, the Oklahoma Health Care Authority is mandated to recover those costs from the estate — and the family home is the primary target. The guide explains the exact exemptions that block a lien: a surviving spouse living in the home, a minor child, a disabled child, a resident sibling with equity interest. It covers the undue-hardship waiver, the burial expense carve-out, and how the recovery claim interacts with the step-up in basis and the final tax filings. Most families panic when the OHCA notice arrives. This chapter tells you whether you have a defense and how to assert it.

Mineral Rights — The Oklahoma Wild Card in Every Tax Calculation

Mineral rights are the single most common complication in Oklahoma estate taxes. They generate fiduciary income (triggering Form 513), they require separate basis calculations for depletion, and they cannot be transferred by small estate affidavit. The guide consolidates every tax implication of inherited mineral interests — royalty reporting, depletion methods, the step-up in basis for mineral rights versus surface rights, and the title clearance required before oil companies will resume payments.

CPA Handoff Organizer

If you hire a CPA, this section tells you exactly which documents, schedules, and basis calculations to prepare before your first meeting. Walk in with organized files instead of a shoebox of royalty statements and 1099s at $150 to $300 an hour.

Who This Guide Is For

- The executor who just learned the estate earns mineral royalties — a royalty check arrived, the oil company wants clear title, and you have no idea whether to report the income on the deceased's final return or a separate fiduciary return. The guide answers that question in the first chapter and walks you through Form 513.

- The surviving spouse who needs the step-up in basis before selling the family home or farm — you know the property gained value over decades, but you do not know how to document the new basis or how the capital gains calculation works. The guide gives you the appraisal steps and the documentation the IRS expects.

- The out-of-state heir whose parent owned Oklahoma mineral rights — you live in Texas or Colorado, the royalties are suspended, and you need to understand both the tax filings and the title clearance before the payments resume. The guide covers both and tells you what can be done remotely.

- The family terrified of losing the home to SoonerCare recovery — OHCA sent a recovery notice and you do not know whether the exemptions apply to your situation. The guide lists every exemption, every defense, and the timeline for responding.

- The executor preparing for a CPA meeting — you want to minimize billable hours by arriving with organized documents instead of questions. The CPA Handoff Organizer tells you exactly what to bring.

Why Free Resources Will Not Get You Through This

- The Oklahoma Tax Commission provides blank forms and instructions written for preparers. Form 513 instructions reference IRC sections and assume you already know fiduciary taxation. Form 507 has no plain-English explanation of when to use it or how to attach it to the final return.

- National platforms gloss over the Oklahoma rules that matter. TurboTax, H&R Block, and Nolo mention Oklahoma has no estate tax and move on — saying nothing about Form 513, the federal tax deduction prohibition, or mineral royalty reporting. Their checklists miss the fiduciary return entirely.

- Attorney and CPA blogs explain just enough to sell the engagement. Local firms write accurate content designed to convince you the process is too dangerous to do alone. For estates with contested mineral interests or active wells, they may be right. For straightforward estates, the filings are sequential, predictable, and doable with the right guide.

- Government sites cover one slice each and never connect the dots. The Tax Commission handles income tax. The OHCA handles Medicaid recovery. The county clerk handles deed recording. The IRS handles federal filings. None tells you the order, the dependencies, or the consequence of filing one before clearing another.

Free resources give you blank forms and scattered instructions. The Tax-First Settlement Sequence gives you every filing in the right order — Tax Commission to IRS to OHCA to county clerk — translated into plain English and built for Oklahoma law.

— Less Than One Hour With an Oklahoma CPA

An Oklahoma estate CPA charges $150 to $300 per hour. A probate attorney retainer starts around $3,250. This guide costs less than a fraction of a single professional consultation and gives you the complete Oklahoma-specific tax roadmap — every form, every deadline, every sequence dependency, and the honest line that tells you whether you even need to make that call.

Your download includes the complete Tax-First Settlement Sequence guide, the standalone Oklahoma Tax After Death Checklist, and five printable reference sheets — the Form 511/513 Filing Decision Tree, the Step-Up in Basis Documentation Worksheet, the Mineral Rights Tax Reference, the Medicaid Recovery Exemptions Card, and the Tax Deadline Calendar. Seven PDFs total, instant download, no account required.

60-day money-back guarantee. If this guide does not save you at least 10 hours of confused tax research across scattered government websites, email us for a full refund. You keep the guide.

Not ready for the full guide? Download the free Oklahoma — Tax After Death Checklist — every tax deadline, every form, and the one filing most executors miss entirely. It is enough to know what is due and when, starting tonight.

You did not ask to become the executor. But the Tax Commission expects its forms filed correctly, the oil company will not resume payments until you clear title, and the nine-month clock on the TOD deed is already running. This guide puts every Oklahoma tax obligation into one sequence so you can stop searching and start filing.