The Estate Is Worth $1.2 Million on Paper. Oregon Wants $20,000 of It Before Anyone Gets a Dime. And the Filing Extension You Just Requested Does Not Extend the Deadline to Pay.

Someone just died in Oregon, and the estate math is worse than you expected. The house in Portland or Bend that appreciated over two decades, plus a life insurance payout, plus the retirement accounts — the total crosses $1 million. Oregon's estate tax threshold is exactly $1,000,000. Not indexed for inflation. Not adjusted since 2012. Not aligned with the $15,000,000 federal exemption. One million dollars, and the state starts taking 10% on every dollar above it.

You filed for an extension, because nine months felt impossibly tight while you were still sorting through bank statements and ordering property appraisals. The extension was granted — six more months to file the paperwork. What nobody flagged in bold on the form: the extension applies only to filing. The payment deadline does not move. Interest starts accruing the day after the original nine-month mark. Miss it, and there is a 5% penalty on top of the interest. The extension gave you more time to organize the forms. It did not give you more time to find the money.

And the estate tax is only one of four separate tax returns you are now responsible for. The decedent's final income tax return (Form OR-40). The fiduciary income tax return (Form OR-41) if the estate earned any income during probate — rent from the house, dividends from the brokerage account, interest from the savings account. The federal Form 706 if the estate exceeds $15 million. And the Oregon Form OR-706 that triggered all of this. Four different forms, three different agencies, four different deadlines. Miss any of them and you are personally liable as the personal representative.

The Oregon Final Tax & Estate Tax Guide is an Estate Tax Defense Roadmap — a 12-chapter sequencing guide that walks you through every tax return, every filing deadline, every deduction strategy, and every distribution rule specific to Oregon law. Not a generic national probate checklist. Not a law firm blog post that explains just enough to make you call for a $400-per-hour consultation. A complete reference built on Oregon Revised Statutes, Department of Revenue requirements, and federal regulations — organized around the deadlines that actually cost families money when they are missed.

What's Inside the Estate Tax Defense Roadmap

A 12-chapter guide with tax tables, filing sequences, deduction strategies, and deadline calendars covering every post-death tax obligation Oregon executors face — from the first week through final distribution:

Chapter 1: The Four Taxes — What You Actually Owe and What You Don't

Oregon has no inheritance tax. Beneficiaries do not owe state tax on money they receive from the estate. But the estate itself may owe four distinct taxes — the final income tax, the estate transfer tax, the fiduciary income tax, and the federal estate tax — each with different forms, different deadlines, and different agencies. This chapter separates them clearly so you stop conflating obligations that have nothing to do with each other and start tracking only the ones that apply to your estate.

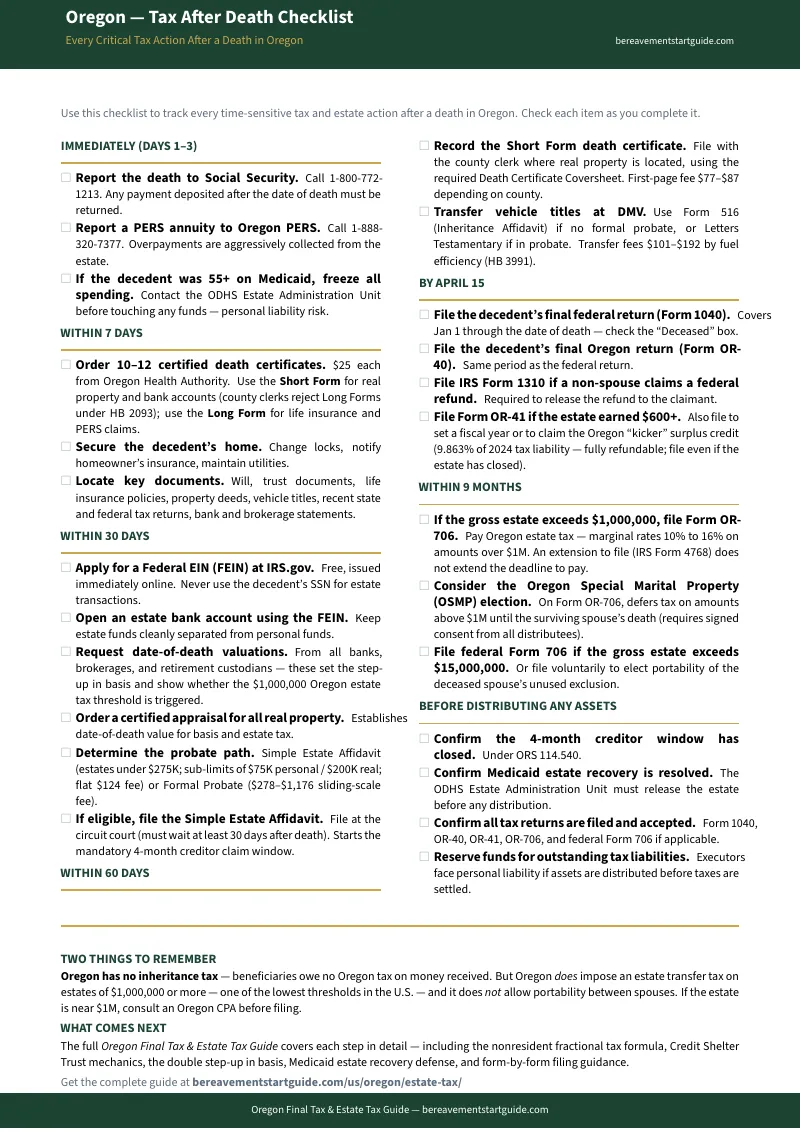

Chapter 2: The First 15 Days — Urgent Steps That Affect Every Tax Filing

Ordering both Short Form and Long Form death certificates — because Oregon county clerks reject Long Forms for real estate recording under HB 2093. Getting a Federal Employer Identification Number before you touch a single bank account. Separating probate assets from non-probate assets so you know whether you qualify for Oregon's Simple Estate Affidavit or need formal probate. Requesting date-of-death valuations from every financial institution — the numbers that determine whether you cross the $1,000,000 threshold.

Chapter 3: The Oregon Estate Transfer Tax — The $1 Million Cliff

The complete rate schedule from 10% to 16% on estates above $1 million. The exact Form OR-706 filing instructions. The nonresident fractional apportionment formula that catches out-of-state property owners who assume their Oregon vacation cabin does not trigger a filing. The natural resource exemption for farms and timber. The Oregon Special Marital Property election that defers the tax until the surviving spouse's death — and the signed consent from all distributees required to use it.

Chapter 4: The Final Income Tax Return

Filing Form OR-40 for income earned from January 1 through the exact date of death. How a surviving spouse files jointly. Who signs the return when the court has not yet appointed a personal representative. How to claim the Oregon "kicker" surplus credit — a fully refundable credit worth 9.863% of the decedent's 2024 Oregon tax liability that many executors miss entirely because they do not realize the estate qualifies.

Chapter 5: The Fiduciary Income Tax Return

The estate becomes a separate taxable entity the moment the person dies. Any income it earns — rent from the house sitting unsold, dividends from the investment portfolio, interest from the bank accounts — gets reported on Form OR-41. The IRC Section 645 election that lets you treat a revocable trust as part of the estate for tax purposes. How income passes through to beneficiaries via Schedule K-1, and what that means for their personal tax returns.

Chapter 6: The Federal Estate Tax and How It Interacts with Oregon

The $15,000,000 federal exemption means most Oregon estates will not owe federal estate tax. But filing federal Form 706 voluntarily can elect portability of the deceased spouse's unused exclusion — a tool Oregon does not offer at the state level. When voluntary filing makes sense. When it does not. How to coordinate the federal and state returns when both are required.

Chapter 7: Step-Up in Basis — The Rule That Saves Beneficiaries Thousands

Inherited assets receive a new tax basis equal to their fair market value at the date of death. A house purchased for $120,000 in 1995 and inherited at $580,000 can be sold immediately with zero capital gains. But Oregon's Tenancy by the Entirety ownership — the default for married couples — only grants a step-up on the deceased spouse's half. Surviving spouses who sell the family home without understanding this face capital gains tax on their original half. The double step-up available to couples who moved from community property states. The valuation strategies that protect the family.

Chapter 8: Deductions That Reduce the Taxable Estate

Every dollar deducted below the $1 million threshold eliminates 10 cents in estate tax. Funeral expenses, cremation fees, burial plots, headstones, and clergy fees — all deductible on Schedule J. Administration expenses — attorney fees, accountant fees, appraisal costs, court filing fees. Debts owed by the decedent. The marital deduction for property passing to the surviving spouse. Charitable bequests. The Natural Resource Credit for qualifying farms, ranches, and forestland. This chapter provides the complete deduction inventory so nothing is left on the table.

Chapter 9: Medicaid Estate Recovery

If the deceased received Medicaid after age 55, the Oregon Department of Human Services operates as a priority creditor. The state's expanded estate definition reaches assets most families assume are protected — joint tenancy, payable-on-death accounts, Transfer-on-Death designations, and living trusts all fail to shield assets after the surviving spouse dies. Deferrals while a surviving spouse is alive. The exemption for children under 21 or children meeting Social Security disability criteria. The $6,000 funeral expense cap for insolvent estates.

Chapter 10: The Master Deadline Calendar

Every filing deadline — federal and state — in chronological order from the date of death through final distribution. The deadlines that cost money when missed. The deadlines that merely delay the process. Which extensions actually protect you and which ones only delay the paperwork while interest accrues on unpaid obligations.

Chapters 11-12: Distribution Rules and When to Hire a Professional

The 4-month creditor window that must close before any distribution. The priority order of claims against the estate. The personal liability exposure for executors who distribute prematurely. Vehicle title transfers through DMV Form 516. Real property recording requirements. And a clear framework for when self-management ends and a CPA or probate attorney is genuinely necessary — because some estates absolutely require professional intervention, and this guide tells you exactly which ones.

Who This Guide Is For

- The personal representative facing the $1 million cliff — who just discovered that a paid-off Portland house, a retirement account, and a life insurance policy add up to more than Oregon's estate tax threshold, and needs to know exactly which deductions reduce the taxable estate, which forms to file, and which deadlines cannot be extended.

- The surviving spouse navigating taxes alone for the first time — who needs to file the decedent's final return, decide whether the Oregon Special Marital Property election makes sense, understand the step-up in basis before selling the family home, and avoid triggering Medicaid estate recovery on assets that seemed protected.

- The adult child managing a parent's estate from out of state — who needs to determine the probate path (Simple Estate Affidavit vs. formal probate), calculate the estate's tax exposure, and avoid the personal liability that follows from distributing assets before taxes and creditors are satisfied.

- The beneficiary waiting for a distribution — who needs to understand that Oregon has no inheritance tax, but that income from tax-deferred retirement accounts and K-1 pass-through income from the estate will appear on their personal tax return. And who needs to know what questions to ask the personal representative to ensure the estate is being handled correctly.

- The executor of a nonresident's Oregon property — who assumed a $150,000 vacation cabin does not trigger a state filing, but learned that Oregon applies the fractional apportionment formula based on the decedent's worldwide estate — and a $2 million total estate means Oregon taxes a proportional share even if the Oregon property is modest.

- The family hovering near the $1 million line — who needs the deduction inventory in Chapter 8 to determine whether funeral expenses, administration costs, debts, and the marital deduction can push the taxable estate below the threshold and eliminate the tax entirely.

Why Free Resources Leave You Exposed

Oregon estate tax information exists online. It is scattered across the Department of Revenue, the Oregon State Bar, law firm blogs, and national content farms — each covering one fragment of the process without telling you how it connects to the others. Here is what you actually encounter:

- The Oregon Department of Revenue publishes Form OR-706 and its instructions, but does not walk you through the filing sequence. The forms assume you already know what the gross estate includes, which deductions apply, and how to calculate the nonresident apportionment. If you have never filed an estate tax return, the blank form and its 20-page instruction booklet create more confusion than they resolve.

- Oregon law firm blogs explain the $1 million threshold, then stop at the point where a $300-per-hour consultation begins. They describe the problem in vivid detail — "Oregon's estate tax is one of the lowest in the country" — and then direct you to schedule a call. The gap between "you might owe estate tax" and "here is exactly how to calculate it, file it, and pay it" is the gap they are paid to fill at hourly rates.

- National tax sites (Nolo, TurboTax, NerdWallet) cover Oregon in a paragraph within a 50-state overview. They mention the $1 million threshold but miss the nonresident trap, the lack of spousal portability, the OSMP election, the natural resource exemption, and the distinction between filing extensions and payment extensions. The most expensive mistakes in Oregon estate tax are the ones these sites do not cover because they are too state-specific for a national audience.

- CPA firm websites focus on pre-death estate planning for high-net-worth clients, not post-death administration for the $1-3 million estates that actually get caught by Oregon's threshold. The family that just discovered they owe $30,000 in estate tax on a $1.3 million estate does not find their situation addressed in articles written for clients with $10 million in assets and a team of advisors.

Free resources give you fragments — a form here, a threshold there, a blog post that stops where the billing starts. The Estate Tax Defense Roadmap sequences every obligation across every agency in chronological order, so you handle the $30,000 decisions before they compound into $35,000 problems with penalties and interest.

— Less Than One Hour With an Oregon CPA

The average Oregon CPA charges $250 to $400 per hour for estate work. A single missed payment deadline — the one that the filing extension did not cover — costs 5% of the unpaid tax plus daily interest. A single overlooked deduction on Schedule J means the estate pays tax on expenses that were legitimately deductible. This guide costs less than a single certified death certificate and covers every form, every deadline, every deduction, and every distribution rule that Oregon law imposes on the personal representative.