Pennsylvania Hits You With Four Separate Taxes After a Death. Nobody Tells You They Have Four Different Deadlines, Four Different Forms, and Four Different Agencies.

Your loved one died in Pennsylvania, and now you are responsible for the taxes. Not one tax. Four. Pennsylvania's inheritance tax — one of only six states that still imposes one — is due within nine months on Form REV-1500. The fiduciary income tax return (PA-41) triggers on estate income over just $33. The decedent's final personal income tax (PA-40) is due by April 15. And if the estate exceeds $15 million, federal Form 706 adds a fourth layer. Each tax goes to a different agency. Each has its own deadline. Each has its own penalty structure. And none of them will tell you about the others.

You searched "Pennsylvania inheritance tax" and found the Department of Revenue website — which provides the 30-page REV-1500 form and instructions written for estate attorneys billing $250 to $550 an hour. You found Reddit threads from executors who discovered too late that TOD and POD accounts — the ones the bank told them bypass probate — are still subject to Pennsylvania inheritance tax, and that the beneficiary is personally liable for it. You found AARP articles that mention the 4.5% rate for children but say nothing about the 12% rate for siblings or the 15% rate for unmarried partners. And you found the 5% discount for prepaying within three months — but no clear explanation of how to calculate the tax accurately enough to prepay it with confidence.

The average Pennsylvania probate attorney charges roughly $14,000 for full estate administration. Hourly rates run $250 to $550. And the first thing they tell you is that they wish you had come sooner — because three of these four deadlines start running from the date of death, not the date you hire a lawyer.

The 4-Tax Deadline System — One Sequence Through Four Agencies

The Pennsylvania Final Tax & Estate Tax Guide takes the overlapping obligations of the PA Department of Revenue, the IRS, your county's Register of Wills, and the Orphans' Court and organizes them into one chronological action plan. It tells you which tax applies to your situation, which forms to file, which agency receives each one, and — critically — the sequence that lets you capture the 5% prepayment discount before it expires while still filing the other three returns on time.

What You Get

The Complete Tax & Estate Tax Guide

A 16-chapter guide covering every tax obligation after a death in Pennsylvania — organized by deadline priority, not by agency. Written for executors and families, not tax attorneys.

- REV-1500 Field-by-Field Decoder — Pennsylvania's inheritance tax return is the most complex state-level death tax form in the country. The guide walks you through every schedule: Schedule A (real estate), Schedule B (stocks and bonds), Schedule C (bank accounts and cash), through Schedule H (funeral expenses and administrative costs). Every line explained in plain English, every calculation shown with examples, every trap flagged before you fall into it.

- The 5% Discount Countdown — Pay the inheritance tax within three months of death and Pennsylvania knocks 5% off the bill. On a $500,000 estate taxed at 4.5%, that saves $1,125. On a $1 million estate taxed at 15% for non-lineal heirs, that saves $7,500. The guide gives you the calculation method, the payment procedure, and the filing strategy to prepay with confidence — because submitting an inaccurate prepayment creates a different set of problems.

- Class-Rate Navigator — Pennsylvania's inheritance tax rate depends entirely on the beneficiary's relationship to the decedent: 0% for surviving spouses and minor children, 4.5% for lineal descendants and ascendants, 12% for siblings, and 15% for everyone else — including unmarried partners, nieces, nephews, and friends. The guide explains how to classify every beneficiary, handle mixed-class distributions, and plan around the rates where planning is still possible.

- The Non-Probate Tax Trap — Most states exempt TOD accounts, POD accounts, and joint accounts from state death taxes. Pennsylvania does not. These assets bypass probate but remain fully subject to inheritance tax — and the beneficiary, not the estate, is personally liable for paying it. The guide explains which non-probate transfers are taxable, how to calculate the tax on each one, and how to file the beneficiary's portion of the REV-1500.

- PA-41 Fiduciary Return Guide — Pennsylvania triggers a fiduciary income tax return on estate income exceeding just $33. That is not a typo. If the estate earns $34 in bank interest after the date of death, you owe a PA-41. The guide covers the filing threshold, the flat 3.07% rate, the income classification system unique to Pennsylvania (eight classes of income, each with its own rules), and the coordination with federal Form 1041.

- Final Personal Return (PA-40) Walkthrough — The decedent's last individual state income tax return. Filing as a surviving spouse, handling the income split at the date of death, claiming refunds, and the April 15 deadline that applies regardless of where you are in the inheritance tax process.

- 15-Month Safe Harbor for Real Estate — If inherited real estate is sold within 15 months of death, Pennsylvania allows the actual sale price to be used as the date-of-death value on the REV-1500 — eliminating the need for a separate appraisal and reducing the risk of a valuation dispute. The guide explains the rule, the documentation required, and when it helps versus when it hurts.

- Family Settlement Agreement Toolkit — Pennsylvania allows heirs to bypass the Orphans' Court formal accounting process through a Family Settlement Agreement. The guide explains when this is available, what must be included, how it interacts with the inheritance tax filing, and the scenarios where it saves months of court proceedings and thousands in legal fees.

- 67-County Register of Wills Navigator — Pennsylvania's probate system is decentralized across 67 counties, each with its own Register of Wills, its own filing procedures, and its own local rules layered on top of the state requirements. The guide identifies the key county-level variations that affect tax filings and provides the contact strategy for your specific county.

- Step-Up in Basis Calculator — Inherited assets receive a basis adjustment to fair market value at the date of death. How this works in Pennsylvania, why it usually eliminates most capital gains if you sell soon after death, and the documentation you need to prove basis to the IRS. Includes the interaction with the 15-month safe harbor rule for real estate.

- Medicaid Estate Recovery Defense — Pennsylvania's Medicaid Estate Recovery Program targets only probate property — not TOD deeds, joint accounts, or beneficiary-designated assets. The guide explains the scope, the caregiver child exception, the surviving spouse protection, and the hardship waiver process for estates that do face a claim.

- Federal Estate Tax and Portability — For estates exceeding the $15 million federal exemption, the guide covers Form 706 and the portability election that allows surviving spouses to capture the deceased spouse's unused exclusion — creating up to $30 million in future protection. Even estates well below the threshold should understand when a portability-only filing makes sense.

- CPA Handoff Organizer — If you hire a CPA, this section tells you exactly which documents, schedules, and calculations to organize before your first meeting. Walk in with a completed asset inventory and beneficiary classification instead of a shoebox — because every hour a Pennsylvania CPA spends sorting paperwork at $250 to $550 per hour is an hour billed to the estate.

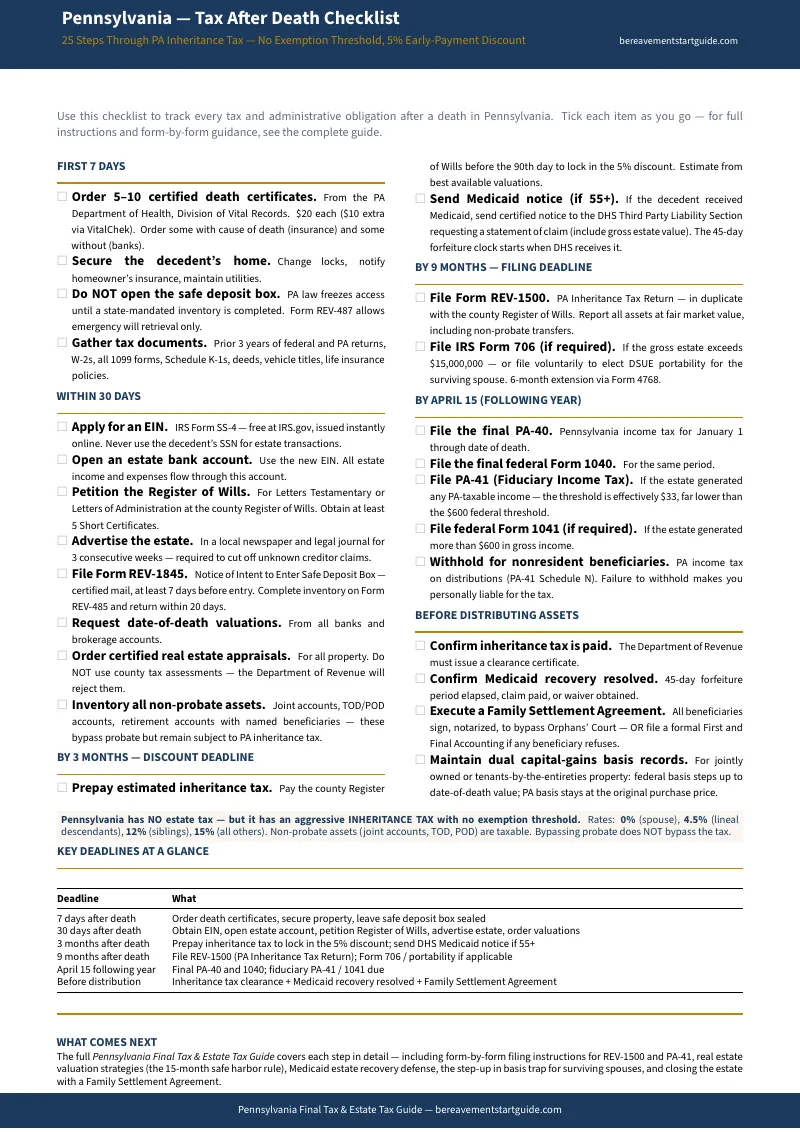

The Tax After Death Checklist

A 20-item printable checklist covering every tax-related action from the first week through final filings. Organized by deadline — the 3-month discount window, the 9-month REV-1500 deadline, the April 15 income tax returns, and the ongoing obligations until the estate closes. Enough to start immediately, even before reading the full guide.

Printable Standalone Tools

Separate PDF worksheets you can print and bring to meetings with banks, CPAs, and the Register of Wills:

- Beneficiary Classification Worksheet — Fill-in table for listing every beneficiary with their relationship to the decedent, the applicable inheritance tax class (0%, 4.5%, 12%, or 15%), and the assets allocated to each. Use this to calculate the total inheritance tax before filing the REV-1500.

- 4-Tax Deadline Calendar — Every critical tax deadline mapped to a single timeline: the 3-month prepayment discount cutoff, the 9-month REV-1500 delinquency date, the April 15 income tax returns, and the 9-month federal Form 706 deadline. One page, four taxes, no missed deadlines.

- Non-Probate Asset Tracker — Inventory sheet for TOD accounts, POD accounts, joint accounts, and beneficiary-designated assets that bypass probate but remain subject to Pennsylvania inheritance tax. Tracks the asset, the beneficiary, the applicable tax rate, and the personal liability assignment.

- Forms Reference Card — One-page quick reference mapping every Pennsylvania and federal tax form to the agency that receives it, the deadline, and the chapter in the guide that covers it: REV-1500, PA-41, PA-40, Form 706, Form 1041, and county-specific Register of Wills filings.

Who This Is For

- Executors who received the REV-1500 form and its 30 pages of instructions and realized this is not something they can figure out from a government website — and who want to understand the form before paying an attorney $250 to $550 an hour to explain it

- Beneficiaries who inherited a TOD or POD account and had no idea they are personally liable for Pennsylvania inheritance tax on it — not the estate, not the executor, them

- Families within the 3-month prepayment window who want to capture the 5% discount but need to calculate the inheritance tax accurately enough to prepay with confidence

- Surviving spouses who qualify for the 0% inheritance tax rate but still need to file the REV-1500, handle the PA-40 and PA-41, and navigate the Medicaid estate recovery rules

- Out-of-state executors managing a Pennsylvania estate remotely who need to understand which of the 67 county Registers of Wills has jurisdiction and what that county's specific requirements are

- Anyone preparing documents for a CPA who wants to minimize billable hours by walking in with organized schedules, a completed beneficiary classification, and a clear picture of which of the four taxes apply

Why Not Free Resources?

The information exists. It is scattered across a dozen government PDFs, a hundred attorney blog posts, and a thousand forum threads. Assembling it into one actionable sequence — while you are grieving and four different deadlines are running simultaneously — is a different problem entirely:

- The PA Department of Revenue provides the REV-1500 form and instructions — split across multiple PDFs, written for attorneys, with no chronological workflow and no connection to the PA-41, PA-40, or federal filings that must be coordinated alongside it

- TurboTax and H&R Block do not support PA-41 fiduciary returns or REV-1500 inheritance tax returns — they handle the decedent's final PA-40 and nothing else

- National sites like Nolo and SmartAsset mention Pennsylvania's inheritance tax in overview articles but miss the non-probate tax trap, the $33 PA-41 threshold, the 5% prepayment discount mechanics, and the 15-month real estate safe harbor

- Attorney blogs explain the problem in just enough detail to justify a $14,000 retainer — no standalone checklist, no chronological roadmap, no document list you can use independently

- Reddit threads contain well-intentioned advice from executors in other states whose inheritance tax rules do not apply in Pennsylvania — a state where non-probate assets are taxable and unmarried partners pay 15%

— Less Than One Hour of Attorney Time

A Pennsylvania estate attorney charges $250 to $550 per hour. The average full estate administration runs roughly $14,000. This guide costs a fraction of one consultation and covers all four tax obligations in one organized sequence — so you understand what you owe, to whom, by when, and in what order.

For straightforward estates, this guide can replace dozens of hours of confused research across scattered government websites. For complex estates, organizing your paperwork with this guide before your first attorney meeting can save thousands in billable hours — because you walk in with a completed beneficiary classification and asset inventory instead of questions.

60-day, no-questions-asked refund guarantee. If this guide does not save you at least 10 hours of frustrated research across Pennsylvania's fragmented tax system, email us for a full refund. You keep the guide.

Not ready for the full guide? Download the free Pennsylvania Tax After Death Checklist — the 20 most critical deadlines, form numbers, and action items that most executors do not discover until the 3-month discount window has already closed.

You did not plan to be the person handling four separate taxes for someone who died. But the 3-month discount window is already shrinking, the 9-month delinquency deadline is approaching, and every hour your attorney spends sorting paperwork is an hour billed to the estate. This guide turns Pennsylvania's fragmented, four-agency tax maze into a single organized sequence — so you walk into your first professional meeting prepared, not panicked.