The Division of Taxation Filed a Lien on the House Before Anyone Told You About It. The Estate Tax Return Is Due in Nine Months. And Half the Forms People Online Are Telling You to Use Were Abolished Four Years Ago.

The moment someone dies in Rhode Island, the state places an automatic statutory lien on every piece of real estate they owned. Not because the estate owes taxes. Not because anyone filed anything wrong. The lien is automatic, imposed under RIGL 44-23-12 the instant the death certificate is issued. Until the Division of Taxation signs off, no title company in the state will close a sale, no bank will approve a refinance, and no deed transfer will record. The property is frozen.

You went online to figure out what to file and found dozens of articles telling you to submit Form RI-100 or RI-100A. Those forms were abolished on January 1, 2022. They no longer exist. Every executor who downloads one, fills it out, and mails it in gets an immediate rejection. The correct form is the RI-706 — and it must be filed even if the estate is worth $300,000 and nowhere near the $1,838,056 taxable threshold. But nobody searching "Rhode Island estate tax forms" learns that until after the rejection letter arrives.

Meanwhile, the estate has three separate tax obligations running on different deadlines: the decedent's final personal income tax return (due April 15), the estate's own fiduciary income tax return if any assets generated income during probate, and the estate tax return (due nine months from death). Miss any one of them, and the state charges interest and penalties. Distribute assets to beneficiaries before settling the tax debts, and you — the executor — are personally liable.

The Rhode Island Tax Clearance Sequence — Every Filing, in the Right Order, to the Right Office, With the Right Forms

The Rhode Island Final Tax & Estate Tax Guide takes the three overlapping tax tracks, the obsolete-form minefield, and the real estate lien discharge process and organizes them into one chronological filing sequence. It tells you which return to file first, which forms to attach, where to submit them, how to calculate what you owe, and how to get the state to release its grip on the property.

This is not a general overview of how estate taxes work. Every form number, every threshold, every deadline, and every calculation is specific to Rhode Island — built on the current 2026 Division of Taxation rules, not the obsolete RI-100/RI-100A workflow that still dominates search results.

What You Get

The Complete Rhode Island Final Tax & Estate Tax Guide

A comprehensive guide covering every tax obligation an executor faces after a death in Rhode Island — organized by timeline, not by tax type. Written for executors and family members, not CPAs.

- The Three Tax Tracks Explained — A plain-English breakdown of the three separate returns the state may require: the decedent's final RI-1040 (personal income tax for the year of death), the RI-1041 (fiduciary income tax for any income earned by the estate during probate), and the RI-706 (estate tax return). Which ones apply to your estate, what triggers each one, and how they interact with their federal counterparts.

- The 2026 Estate Tax Threshold and Rate Tables — Rhode Island's estate tax exemption is $1,838,056 for 2026, indexed annually for inflation. If the estate exceeds this threshold, progressive marginal rates scale from 0.8% up to 16%. The guide includes the complete rate table, the calculation methodology, and the critical warning that non-probate assets — jointly held property, retirement accounts, life insurance payouts, revocable trusts — count toward the gross estate total, frequently pushing estates over the line that families assumed they were safely below.

- No Inheritance Tax — What That Actually Means — Rhode Island does not tax beneficiaries on what they receive. The estate tax is paid from the estate before distribution. The guide explains the distinction, identifies the five states that do levy an inheritance tax so beneficiaries in those states know what to watch for, and clarifies why "no inheritance tax" does not mean "no tax consequences" when inheriting Traditional IRAs, annuities, or income-producing assets.

- No Portability — Why Surviving Spouses Cannot Rely on the Federal Playbook — Federal estate tax law allows a surviving spouse to inherit the deceased spouse's unused exemption amount. Rhode Island does not. The guide walks through the implications of this critical difference and the planning strategies available to married couples whose combined estates approach the threshold.

- The Real Estate Lien Discharge Process — Step-by-step instructions for clearing the automatic statutory lien under RIGL 44-23-12. How to file Form T-77 in triplicate with the exact tax assessor's property description from the municipal tax bill (Plat, Lot, Map, Block, and Parcel), why the Division of Taxation rejects T-77 submissions for minor typos, and how to obtain the Notice of No Tax Due for non-taxable estates. Covers Form T-79 for discharging liens on Rhode Island securities and domestic corporate interests.

- The Final Income Tax Return — Form RI-1040 — Filing the decedent's last personal income tax return for the year of death. Filing status rules when a surviving spouse is involved, claiming medical expenses paid within one year of death as deductions, and the Form 1310 requirement when the estate is owed a refund and there is no surviving spouse.

- The Fiduciary Income Tax Return — Form RI-1041 — When the estate generates income during probate — rental income from a multi-family property, stock dividends, interest on accounts — the estate becomes its own taxpaying entity. The guide covers the filing triggers, the relationship between the federal 1041 and the state RI-1041, how to attach federal K-1 schedules and Rhode Island Schedule W, and the Pass-through Entity Election Tax option.

- Step-Up in Basis and Capital Gains — How the federal step-up in basis resets the cost basis of inherited assets to fair market value on the date of death, potentially eliminating years of capital gains appreciation. Includes a worked example: a Narragansett coastal home purchased for $100,000 in 1985, valued at $800,000 at death — sold for $800,000, with zero capital gains tax on the $700,000 of appreciation. Explains how this interacts with Rhode Island's 5.99% capital gains rate.

- Selling Inherited Property — The Non-Resident Withholding Trap — Rhode Island mandates a 6% withholding on net sale proceeds for non-resident sellers and trusts. If you are an out-of-state beneficiary selling inherited coastal property, the title company will withhold this amount automatically. The guide explains how to calculate the withholding, how to claim it back on a non-resident tax return, and the timeline for receiving the refund.

- The Nine-Month Filing Deadline and Extensions — The RI-706 is due nine months from the date of death. Form RI-4768 grants a six-month filing extension, but the tax payment itself is not extended — the estate must estimate and pay the full amount by the nine-month mark to avoid interest. The guide explains when to use the extension and how to estimate the payment when the estate valuation is still in progress.

- Small Estate Tax Shortcuts — For personal property estates of $15,000 or less with no real estate, Rhode Island allows a simplified affidavit process under RIGL 33-24-1. The guide explains the qualifications, the interaction with the tax clearance process, and why a small estate affidavit does not eliminate the need to address the real estate lien if any property is involved.

- Medicaid Estate Recovery and Tax Interactions — If the deceased received Medicaid-funded care after age 55, the state can file a recovery claim against the estate. The guide maps the categorical exemptions (surviving spouse, child under 21, disabled child), the hardship waiver process, and how recovery claims interact with the estate tax return and lien discharge timeline.

- When You Need a CPA or Attorney — Estates approaching the $1,838,056 threshold, estates with business interests or complex trust structures, and estates with multi-state property holdings functionally require professional oversight. The guide identifies the specific trigger points and explains how to reduce professional fees by arriving with organized paperwork, completed checklists, and the right data already collected.

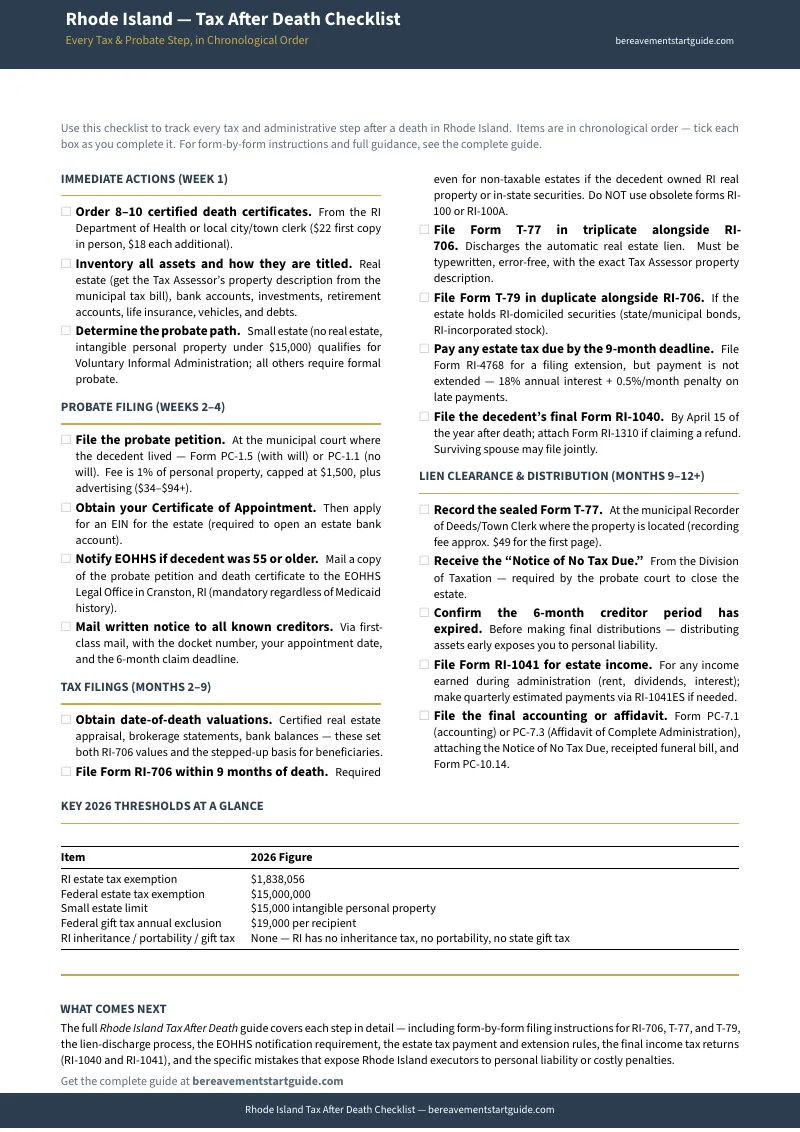

The Tax After Death Checklist

A standalone printable checklist organized by timeline: First 30 Days, Within 90 Days, Within 9 Months, and Before Closing the Estate. Every action item includes the specific Rhode Island form number, the office to contact, and the deadline. Start immediately — even before reading the full guide.

6 Standalone Printable Tools

Print what you need, when you need it — each tool works independently without opening the main guide:

- Tax Obligation Decision Tree — Work through a series of yes/no questions to determine which of the three tax returns apply to your estate and the deadlines for each

- Real Estate Lien Discharge Worksheet — Step-by-step T-77 completion guide with fields for each property's tax assessor description, a submission tracking section, and common rejection reasons to avoid

- Estate Tax Calculation Worksheet — Fillable worksheet for calculating the gross estate, applicable deductions, and estimated tax using the 2026 progressive rate brackets — including the non-probate assets that most executors forget to count

- Step-Up in Basis Calculator — Side-by-side comparison of original cost basis vs. date-of-death fair market value for each inherited asset, with the resulting capital gains exposure (or elimination)

- Tax Filing Timeline — Every tax deadline from the date of death through final returns, with the specific form numbers and filing addresses, in one wall-postable reference

- Form Reference Sheet — Every tax form referenced in the guide (RI-706, T-77, T-79, RI-1040, RI-1041, RI-4768, Form 1310, federal 706, federal 1041) with its purpose, where to get it, and where to file it

Who This Is For

- Executors who just learned the state placed a lien on the inherited house and need to know exactly how to get it released — the right forms, in the right order, filed without the typos that trigger rejection

- Family members trying to determine whether the estate owes Rhode Island estate tax and discovering that life insurance, retirement accounts, and jointly held property all count toward the $1,838,056 threshold

- Out-of-state beneficiaries selling inherited Rhode Island coastal property who need to understand the 6% non-resident withholding, the lien discharge sequence, and how the step-up in basis affects their capital gains

- Surviving spouses who assumed federal portability rules applied in Rhode Island and just learned they do not — the deceased spouse's unused exemption cannot be transferred

- Executors of modest estates who know they owe zero estate tax but cannot sell or transfer the house until they file the RI-706 and receive a Notice of No Tax Due

- Anyone managing an estate that generated income during probate — rental income, dividends, interest — who did not know the estate itself must file a separate fiduciary income tax return

Why Free Online Resources Fall Short

The information exists. It is scattered across the Division of Taxation website, the Secretary of State's forms portal, 39 municipal tax assessor offices, and dozens of law firm blogs. Assembling it into one actionable sequence while grieving and managing concurrent deadlines is a fundamentally different problem:

- The Division of Taxation website hosts the current RI-706, T-77, and RI-4768 forms as blank PDFs — with no instructions on which forms your estate needs, in what order they must be filed, or how they interact with each other and the municipal lien discharge process

- Dozens of online articles and law firm blogs still reference Form RI-100 and RI-100A — forms that were abolished on January 1, 2022. Executors following this outdated advice submit dead forms and receive rejection letters, losing weeks at a point when the nine-month deadline is already running

- National platforms like SmartAsset and Nolo publish Rhode Island estate tax pages that mention the exemption threshold but skip the operational mechanics — the T-77 triplicate filing requirement, the tax assessor's property description that must match exactly, the fact that non-taxable estates still need to file the RI-706 to unfreeze the property

- Local attorney blogs outline the dangers in enough detail to justify a $300-to-$600-per-hour consultation — the lien, the personal liability, the penalties — but deliberately withhold the step-by-step filing sequence that would let you handle the administrative work independently

- None of these sources present the three tax tracks (income, fiduciary, estate) as one integrated timeline — executors piece together fragments from different websites and different tax years, never certain whether they have the current rules or last year's thresholds

— Less Than One Hour of CPA Time

A Rhode Island CPA charges $200 to $400 per hour for estate tax work. A probate attorney charges $300 to $600. The data-gathering alone — collecting date-of-death valuations, identifying which non-probate assets count toward the gross estate, pulling the correct tax assessor descriptions for Form T-77 — consumes hours of billable time before any actual tax strategy begins. This guide costs a fraction of one professional consultation and covers the entire tax clearance process from the date of death through the final return.

For estates well below the $1,838,056 threshold, this guide walks you through the mandatory RI-706 filing and T-77 lien discharge that still must happen before any property can change hands. For estates approaching or exceeding the threshold, organizing the data with this guide before your first CPA meeting can save thousands in billable hours — because you arrive with the gross estate calculated, the non-probate assets identified, and the filing timeline mapped.

60-day, no-questions-asked refund guarantee. If this guide does not save you time, reduce your confusion about Rhode Island's tax obligations after a death, or help you avoid the obsolete-form trap, email us for a full refund. You keep the guide.

Not ready for the full guide? Download the free Rhode Island — Tax After Death Checklist — the phased action plan covering every tax obligation from the first 30 days through estate closure, with the correct 2026 form numbers, deadlines, and filing addresses.

The state filed a lien on the house before you knew it existed. The estate tax return is due in nine months whether or not the estate owes a dollar. The forms half the internet tells you to use have not existed since 2022. And three separate tax deadlines are running simultaneously while you are trying to grieve. This guide turns the Division of Taxation's scattered forms and rigid deadlines into one clear filing sequence — so you clear the lien, file the returns, and protect yourself from personal liability without paying an attorney to organize your paperwork for you.