South Carolina Has No Estate Tax. The State Still Collected Money From the Estate — and Nobody Warned the Executor.

Maybe you just discovered that the estate owes South Carolina Fiduciary Income Tax because the decedent's savings account earned $800 in interest during probate — and you had no idea a separate tax return existed. Maybe you inherited a Charleston beach house and the county just reassessed the property taxes at full market value, quadrupling the annual bill overnight. Maybe you are staring at Form SC1041 instructions that assume you already know the difference between an estate's gross income and a decedent's final individual return — and every search result either tells you "South Carolina has no death tax" (true but dangerously incomplete) or pitches a $300-per-hour consultation with an estate attorney.

You are grieving. There are deadlines. The probate court will not tell you whether you actually need to file a fiduciary return. The county assessor will not explain the Assessable Transfer of Interest rules before they reassess the inherited property. And the IRS will not remind you that failing to get a Date of Death appraisal now means losing the step-up in basis later — turning a tax-free inheritance into a five-figure capital gains bill when you sell the house.

Here is what the government websites, the national legal aggregators, and the law firm blogs are not giving you: a single, sequential document that tells you which taxes and fees actually apply to this estate, in what order to address them, and exactly how to minimize each one under current South Carolina law — including the 2025 legislative changes that most sources have not updated for yet.

The South Carolina Final Tax & Estate Tax Guide is the Estate Tax Defense System — a plain-English action plan that translates the SC Department of Revenue fiduciary rules, county probate court fee schedules, federal estate tax thresholds, property tax reassessment mechanics, and the 2025 small estate expansion into a single chronological reference. Not a fifty-state overview. Not a law firm blog designed to scare you into a retainer. A South Carolina-specific operational guide built for the executor or beneficiary who needs to settle the tax side of an estate without paying thousands in professional fees for routine administrative work.

What's Inside the Estate Tax Defense System

A comprehensive guide covering every tax obligation, filing deadline, fee structure, and wealth-preservation strategy that applies after a death in South Carolina — organized in the sequence you actually need to act, from the first week through final estate closure:

Chapter 1: The South Carolina Tax Landscape After Death

The critical orientation chapter that prevents the most common and costly mistake: assuming "no estate tax" means "no tax obligations." South Carolina eliminated its state estate tax for deaths after January 1, 2005. South Carolina has no inheritance tax. But the estate still faces up to four distinct financial obligations — the decedent's final individual income tax, the estate's fiduciary income tax, county probate court sliding-scale fees, and property tax reassessments — and missing any one of them exposes the executor to personal liability. This chapter maps all four obligations so you know exactly which ones apply to your estate before you file a single form.

Chapter 2: The Decedent's Final Income Tax Return

Filing the final Form 1040 and SC1040 for the year of death. How a surviving spouse can still elect to file jointly. The mechanics of signing returns on behalf of a deceased taxpayer. Prorating income between the date of death and year-end. The April 15 deadline and extension procedures. How to claim medical expenses paid within one year of death — and whether to deduct them on the final individual return or the estate's fiduciary return for maximum tax benefit.

Chapter 3: The Fiduciary Income Tax Trap

The tax obligation that blindsides most executors. When a person dies, the estate becomes a separate legal entity with its own tax ID and its own compressed tax brackets. If the estate earns just $600 in gross income — bank interest, stock dividends, rental income from an inherited property — the executor must file Form SC1041. South Carolina's top fiduciary rate of 6.0% kicks in almost immediately because estate brackets are compressed far more aggressively than individual brackets. This chapter walks through the filing triggers, the electronic filing mandate for liabilities over $15,000, the quarterly estimated payment schedule, and the 110% underpayment penalty that the SC Department of Revenue applies when executors miss estimated payments.

Chapter 4: Getting the Estate's Tax ID (EIN)

The decedent's Social Security Number cannot be used for estate transactions. The estate needs its own Employer Identification Number from the IRS — and the bank will not open an estate account without one. How to apply online in minutes for free. The explicit warning about predatory websites charging $200 for this free government service. Why the EIN must be obtained before filing the SC1041 or opening the estate checking account that segregates estate funds from personal assets.

Chapter 5: The Step-Up in Basis — The Most Valuable Tax Rule Most Families Miss

The single most important wealth-preservation mechanism available to heirs inheriting real estate. The tax code resets the property's cost basis to its fair market value on the date of death — legally eliminating decades of accrued capital gains. A parent who bought a home in Greenville for $100,000 thirty years ago leaves an heir a property now worth $600,000. Without the step-up, the heir faces capital gains tax on $500,000 of appreciation. With the step-up, the gain is zero. But claiming it requires a professional Date of Death appraisal obtained during probate — and if you sell the property without one, the IRS can challenge your basis and impose the full capital gains tax. This chapter covers the appraisal timeline, documentation requirements, and the specific records to preserve.

Chapter 6: Property Tax Reassessment — The Assessable Transfer of Interest

South Carolina generally caps property tax reassessment increases at 15% over a five-year cycle. When property transfers by inheritance, that cap is removed. The county reassesses the property at current market value, and if the heir does not occupy it as a primary residence, the assessment ratio jumps from 4% (owner-occupied) to 6% (non-owner-occupied) — which can multiply the annual tax bill several times over. This chapter explains the ATI rules county by county, the 90-day window to appeal a reassessment, how to apply for the 25% ATI exemption on 6% ratio properties, and the specific affidavits required to claim the primary residence ratio if the heir moves in.

Chapter 7: Heirs' Property Tax Relief

A uniquely South Carolina chapter. Families holding ancestral property passed down without formal probate — common in Lowcountry and Gullah-Geechee communities — face a devastating catch-22: clearing the title triggers a property tax reassessment that can make the land unaffordable. The 2025/2026 Heirs' Property Tax Relief Act allows qualified family members to transfer and clear title without triggering an ATI reassessment, provided the correct affidavits are filed with the county assessor. This chapter translates the legislation into a step-by-step process for families protecting generational land.

Chapter 8: Federal Estate Tax and Portability Elections

The federal estate tax exemption — $15 million per individual in 2026, $30 million for married couples. Why 99% of estates owe nothing to the federal government but 100% of surviving spouses should understand the portability election. Filing Form 706 to claim a deceased spouse's unused exemption amount — even when no federal tax is owed — protects future generational wealth if exemption limits decrease. The nine-month filing deadline and the specific circumstances where hiring a CPA for this single filing saves the family far more than it costs.

Chapter 9: Probate Court Fees — The Shadow Tax on Every Estate

South Carolina probate courts charge sliding-scale fees based on gross estate value — not net value after debts. In Lexington County, an estate valued at $325,000 pays $95 on the first $100,000 plus 0.15% on the remaining $225,000, totaling $432.50 in mandatory court fees. The guide includes fee calculation tables for major South Carolina counties, explains how the gross estate valuation method inflates these fees, and identifies the specific valuation strategies that legally minimize your exposure — including how the 2025 small estate expansion changes the math for estates under $45,000.

Chapter 10: The 2025 Small Estate Expansion

On May 8, 2025, Act No. 26 raised South Carolina's small estate affidavit limit, exempt property allowance, and homestead allowance from $25,000 to $45,000. Estates that would have required formal probate under the old threshold can now use the streamlined "collection by affidavit" process — bypassing court fees, attorney retainers, and months of delay. This chapter walks through the qualification criteria, the Form 420ES filing process, the specific assets that count toward the threshold, and the exempt property claim (Form 435ES) that protects household furnishings, vehicles, and health aids from unsecured creditors.

Chapter 11: Spousal Elective Share and Non-Probate Offsets

South Carolina law prevents a surviving spouse from being completely disinherited. The elective share statute entitles the spouse to one-third of the probate estate — and South Carolina courts treat revocable trust assets as "illusory" transfers included in the calculation. But life insurance payouts, retirement account distributions, and the $45,000 homestead allowance are credited against that one-third share. This chapter provides calculation worksheets and explains the strict filing window: eight months after death or six months after probate opens, whichever is later.

Chapter 12: Medicaid Estate Recovery Defense

For estates where the decedent received Medicaid long-term care benefits after age 55, the SC Department of Health and Human Services can place a lien on the family home. This chapter details the undue hardship waiver — available when an immediate family member earning under 185% of the federal poverty line has resided in the home for at least two years. It covers the application timeline, required documentation, and the specific statutory basis for the waiver under both federal and South Carolina law.

Chapter 13: Executor Tax Timeline and Personal Liability

The master chronological calendar that ties everything together. Day 1 through final estate closure: when to file the will, when to obtain the EIN, when to order the Date of Death appraisal, when the probate inventory is due (90 days), when the creditor claim period expires (8 months), when each tax return must be filed, and when it becomes safe to distribute assets to beneficiaries without exposing the executor to personal liability for unpaid taxes. This is the chapter that replaces the sequence you cannot find anywhere else — the chronological order of operations that government websites, law firm blogs, and national aggregators refuse to publish.

Chapter 14: Complete Tax Checklist and Filing Templates

Every form, every deadline, every filing obligation consolidated into a printable checklist with checkboxes, responsible-party assignments, and direct links to current state and federal forms. The checklist covers the final SC1040, Form SC1041, Form 1041, Form 706 (if applicable), EIN application, Date of Death appraisal scheduling, county probate inventory, property tax reassessment appeals, and Medicaid recovery waiver applications.

Who This Guide Is For

- Executors handling their first estate who were told "South Carolina has no death tax" and are now discovering fiduciary income tax obligations, sliding-scale court fees, and property tax reassessments that function as hidden taxes on the estate

- Surviving spouses who need to file the decedent's final return, understand the elective share calculation, claim the $45,000 homestead allowance, and determine whether a portability election protects their own estate down the road

- Out-of-state beneficiaries inheriting South Carolina real estate who need to understand the step-up in basis, the ATI property tax reassessment, the 6% non-owner-occupied ratio, and the fiduciary withholding rules that apply to non-resident heirs receiving income from SC property

- Families with estates under $45,000 who can now bypass formal probate entirely under the 2025 small estate expansion — if they know how to qualify and file the correct affidavit

- Heirs' property families protecting ancestral Lowcountry and Gullah-Geechee land from tax sales and forced partition — who need the 2025/2026 legislative relief translated into a plain-English action plan

- Families defending against Medicaid estate recovery who need to file an undue hardship waiver before the state places a lien on the family home

- Anyone preparing paperwork before meeting a CPA or attorney who wants to complete 90% of the administrative legwork themselves and hand a perfectly organized file to a professional — saving thousands in billable hours spent on tasks that do not require a license

Why Free Resources Leave You Exposed

The forms and statutes governing post-death taxes in South Carolina are public record. The problem is not access. The problem is that nobody publishes the sequence — and missing the sequence is where the real financial damage happens:

- The SC Department of Revenue publishes Form SC1041 and instructions. It does not tell you whether you actually need to file it — or that the $600 gross income threshold means most estates with a single bank account or piece of rental property are required to file. It does not warn you about the 110% underpayment penalty or the quarterly estimated payment obligation.

- County probate courts post fee schedules and inventory forms. They explicitly state they cannot provide tax advice. No county connects the probate timeline to the fiduciary tax timeline to the property reassessment timeline. Each agency owns one piece. Nobody publishes the order of operations.

- National aggregators like SmartAsset and Nolo publish "South Carolina Estate Tax" pages. They correctly state there is no state estate tax — and then provide generic federal information that misses the SC-specific fiduciary income tax, the ATI property tax mechanism, the 2025 small estate threshold expansion, and the heirs' property relief legislation. Their South Carolina pages read identically to their North Carolina pages because they are programmatically generated.

- Local law firms write detailed blog posts about every tax trap. Then they withhold the actionable steps until you schedule a $300-per-hour consultation. Their content is designed to demonstrate complexity, not resolve it.

Free resources give you fragments scattered across dozens of government websites, county portals, and law firm lead-generation blogs. The Estate Tax Defense System gives you the complete sequence — every filing obligation, deadline, calculation, and form in the chronological order you actually need them.

— Less Than One Hour of a CPA's Time

A single hour with an estate attorney runs $250 to $400 in South Carolina. A CPA preparing a fiduciary return charges $500 to $1,500 depending on complexity. Missing the step-up in basis documentation can cost the estate tens of thousands in avoidable capital gains taxes. An ATI property tax reassessment can add thousands per year to the holding cost of inherited real estate. This guide costs less than any of those individual exposures and gives you the complete South Carolina-specific tax defense manual: every obligation, every deadline, every form, every calculation, and every wealth-preservation strategy — organized in the exact sequence a grieving executor needs.

Your download includes the complete South Carolina Final Tax & Estate Tax Guide covering final income taxes, fiduciary income taxes, federal estate tax, step-up in basis, property tax reassessments, heirs' property relief, Medicaid recovery defense, probate court fees, the 2025 small estate expansion, spousal elective share calculations, and a master timeline — plus 7 standalone printable worksheets you can use independently:

- Tax Timeline Worksheet — every statutory deadline with a fill-in "Your Date" column

- Step-Up in Basis Checklist — secure the DOD appraisal and protect the estate from capital gains

- Spousal Rights Worksheet — elective share, exempt property, and homestead calculations

- Nonresident Property Sale Checklist — avoid the 7% withholding trap on inherited real estate

- Probate Fee Schedule — county court fees by estate value with calculation examples

- Medicaid Recovery Defense Worksheet — evaluate deferrals and hardship waivers

- Forms Directory — every SC tax and probate form with agency and source

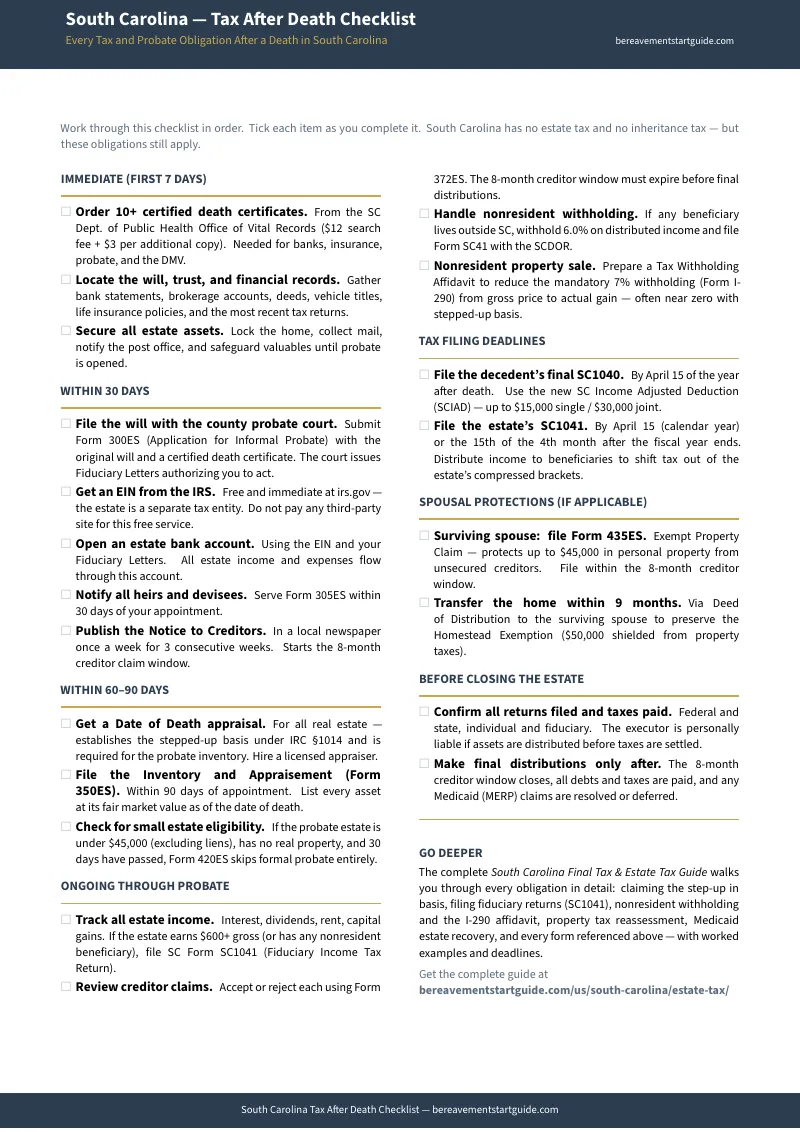

Free download includes the standalone South Carolina Tax After Death Checklist covering the critical first steps every executor must take to protect the estate from unnecessary tax exposure.

30-day money-back guarantee. If the guide does not give you clarity on every tax obligation the estate faces and confidence to handle the administrative work without overpaying for professional help, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free South Carolina Tax After Death Checklist — covering the immediate tax obligations every executor needs to know: whether the estate triggers fiduciary income tax, which returns are due and when, how to obtain the estate's EIN, and when to order the Date of Death appraisal to protect the step-up in basis. It is enough to prevent the most costly early mistakes.

The tax code does not pause for grief. This guide makes sure the estate does not pay more than it owes.