Someone You Love Just Died in South Dakota. Everyone Told You There Are No Taxes. Now the IRS Wants a Final Return, the Estate Is Generating Income You Did Not Know About, and the Department of Social Services Just Filed a Lien Against the House.

You are sitting at the kitchen table with a folder of papers from the funeral home, a stack of unopened mail, and a phone full of messages from family members who heard that South Dakota has no estate tax and assume everything is simple. The bank told you the checking account is frozen until someone produces Letters Testamentary. The county treasurer's office said the vehicle title needs to be transferred within 45 days or penalties start accruing at a dollar per week. Your sister found a letter from the Department of Social Services about Medicaid reimbursement for nursing home care. And the accountant who filed your parent's taxes for twenty years just told you that the IRS still requires a final income tax return even though South Dakota does not have a state income tax.

South Dakota has no state income tax, no state estate tax, and no state inheritance tax. Voters repealed the inheritance tax by constitutional amendment in 2001, and the legislature dismantled the remaining estate tax provisions in 2014. That is all true. And it creates the most dangerous knowledge gap in estate administration: the assumption that "no state taxes" means "no tax obligations at all." It does not. The IRS still requires the decedent's final Form 1040. If the estate earns more than $600 in income — rent from a farmhouse, dividends from a brokerage account, interest on a savings account — the executor must file a federal fiduciary income tax return on Form 1041, and the estate's compressed tax brackets hit 37% at just $16,250. If the decedent was married and the estate is under $15 million, the executor should strongly consider filing a federal Form 706 anyway to preserve portability of the deceased spouse's unused exemption — and failure to file permanently forfeits that protection. Meanwhile, South Dakota's expanded Medicaid estate recovery program can reach into joint bank accounts, living trusts, TOD deeds, and payable-on-death designations — assets most families believe are completely protected.

The South Dakota Final Tax & Estate Tax Guide is a Federal Filing Roadmap for every tax obligation, capital gains decision, and Medicaid recovery defense between the date of death and final distribution. Not a generic national checklist that treats South Dakota like an afterthought. Not a law firm blog post designed to convince you that you need a $300-per-hour attorney for a $60,000 estate. A structured, South Dakota-specific manual that separates what the state will never tax from what the IRS absolutely will — so you stop guessing, stop overpaying, and start handling this in the right order.

What's Inside the Federal Filing Roadmap

An 18-chapter guide and the Tax After Death Checklist — covering every federal filing requirement, state-specific deadline, capital gains strategy, and Medicaid defense available to South Dakota executors and beneficiaries:

Chapter 1: South Dakota's Tax Landscape — What Applies and What Does Not

The chapter that dismantles the myth. South Dakota will never send you a state tax bill for inheriting assets. But the IRS will send you a penalty notice if you miss the final Form 1040 deadline. This chapter separates the five distinct tax and recovery obligations that still apply — federal estate tax, federal income tax, federal fiduciary income tax, county property taxes, and Medicaid estate recovery — from the three state taxes that do not exist. Every executor should read this chapter first, because the rest of the guide depends on understanding what South Dakota exempts you from and what it does not.

Chapter 2: Immediate Actions — The First 15 Days

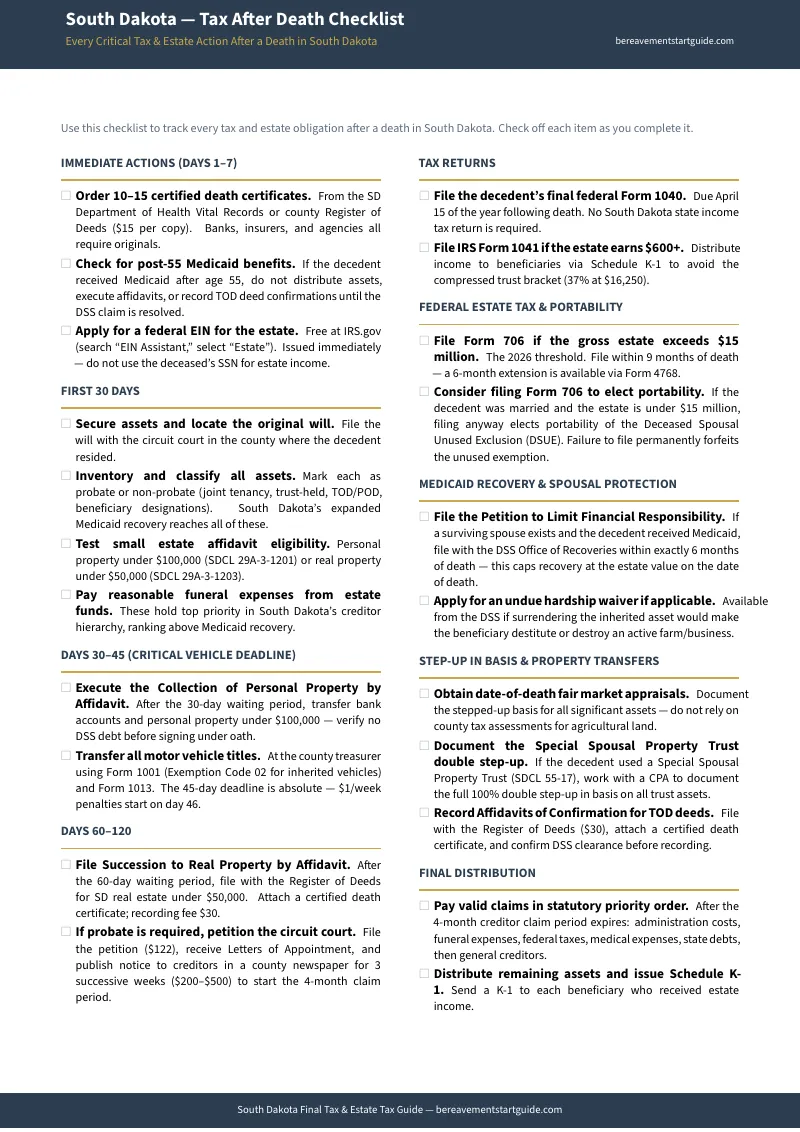

Order 10 to 15 certified death certificates at $15 each from the South Dakota Department of Health or the county Register of Deeds — coming back later means weeks of processing delays that freeze every bank, every insurance company, and every court filing. Determine immediately whether the decedent received Medicaid benefits after age 55, because if the answer is yes, you cannot distribute a single asset, execute a small estate affidavit, or record a TOD deed confirmation until the DSS claim is resolved. Apply for an EIN for the estate at IRS.gov — free, issued immediately, required before you can open an estate bank account or file a fiduciary return.

Chapter 3: Evaluating the Estate — Thresholds and Pathways

South Dakota provides two small estate affidavit paths that bypass probate entirely — one for personal property under $100,000 (30-day waiting period) and one for real property under $50,000 (60-day waiting period, agricultural land excluded). But both affidavits require the executor to swear under oath that the decedent owes no debt to the Department of Social Services. If a Medicaid debt surfaces after you sign, the affidavit is invalidated and you face personal liability. This chapter walks you through the exact valuation methodology, the agricultural land exclusion, and the decision tree that determines whether your estate qualifies for the affidavit path or requires the $122 formal probate filing.

Chapter 4: The Final Income Tax Return — Form 1040

South Dakota has no state income tax return. The IRS does not care. The executor is federally mandated to file the decedent's final Form 1040 covering January 1 through the date of death. Due by April 15 of the year following death. Surviving spouses may file jointly for the year of death if they have not remarried. This chapter covers what income to include, what deductions to claim, and the specific medical expense election that lets the executor deduct final medical costs on either the income tax return or the estate tax return — whichever produces the greater benefit.

Chapter 5: The Estate's Own Tax Return — Form 1041

The estate becomes a separate taxable entity the moment the decedent dies. If it earns more than $600 in gross income — rent from inherited property, dividends from a brokerage account, interest on bank balances — the executor must file Form 1041. The trap: trust and estate tax brackets are severely compressed. The top federal rate of 37% kicks in at just $16,250, compared to $609,350 for individuals. The guide explains how to use the income distribution deduction and Schedule K-1 to push income through to beneficiaries at their lower individual rates, avoiding thousands of dollars in unnecessary tax.

Chapter 6: Federal Estate Tax — The $15 Million Threshold and Portability

The 2026 federal estate tax exemption is $15 million per individual under the One Big Beautiful Bill Act. Married couples can shield up to $30 million through portability. But portability is not automatic — the executor must file Form 706 to elect it, even if the estate is far below the filing threshold. If you do not file, the surviving spouse permanently loses the deceased spouse's unused exemption. This chapter explains when Form 706 is required, when it is optional but strategically essential, and the nine-month filing deadline with the six-month extension available through Form 4768.

Chapter 7: Step-Up in Basis and the Special Spousal Property Trust

This is where South Dakota offers something almost no other common-law state provides. Under standard federal tax law, inherited assets receive a step-up in cost basis to fair market value at the date of death — eliminating capital gains on appreciation during the decedent's lifetime. In most common-law states, jointly owned marital property receives only a 50% partial step-up. But South Dakota enacted SDCL Chapter 55-17, creating the Special Spousal Property Trust. Couples who transfer appreciated assets into an SSPT can claim a full 100% double step-up in basis on the first spouse's death. For a family farm purchased forty years ago at $200,000 that is now worth $2 million, this eliminates up to $270,000 in federal capital gains tax. This chapter explains how the SSPT works, how to document the step-up for the IRS, and why every South Dakota farm family with appreciated land should know about it.

Chapter 8: Medicaid Estate Recovery — The Expanded Program

South Dakota uses expanded Medicaid estate recovery. The DSS does not limit itself to assets in the probate estate — it reaches joint bank accounts, life estate properties, revocable living trusts, and TOD/POD designations. If the decedent received Medicaid-funded nursing home care after age 55, the state will assert a claim. But protections exist. Recovery is barred while a surviving spouse, a child under 21, or a blind or disabled child survives. The surviving spouse can file a Petition to Limit Financial Responsibility within six months of the death to permanently cap the state's claim at the estate value on the date of death. The guide walks through every protection, every deadline, and the undue hardship waiver available when surrendering the asset would make the beneficiary destitute or destroy an active farm operation.

Chapters 9–12: Property Transfers, Vehicle Titles, Probate, and Nonresident Issues

Real estate transfers through executor deeds and TOD deed confirmations, with the $30 recording fee and the SDCL 43-4-22 transfer fee exemptions. Motor vehicle transfers through Form 1001 (Exemption Code 02 for inherited vehicles) and Form 1013, with the 45-day deadline that triggers $1-per-week penalties on day 46. The complete probate process from the $122 filing fee through the four-month creditor claim window to final distribution. And the ancillary probate requirements for out-of-state heirs who inherit South Dakota agricultural land or mineral rights.

Chapters 13–18: Trust Structures, Property Taxes, Distribution Strategies, and the Complete Timeline

South Dakota's Domestic Asset Protection Trusts and how they interact with estate administration. County property tax obligations during the administration period, including mineral rights and agricultural classifications. Tax-efficient distribution strategies using the income distribution deduction to keep estate income out of the compressed trust bracket. When to hire a CPA, when to hire an attorney, and when the guide handles the entire process. Every statutory deadline from Day 1 through Month 12 in one sequential reference. And the complete forms and contacts directory covering the IRS, the South Dakota Department of Health, the Department of Social Services, the Unified Judicial System, and every county office you will need.

Who This Guide Is For

- The executor who was told "South Dakota has no taxes" and is now discovering that the IRS still requires a final Form 1040, the estate needs its own EIN and a Form 1041 filing, and the compressed trust tax bracket will consume 37% of undistributed estate income at just $16,250 — who needs the complete federal filing sequence in one document, specific to South Dakota's exemptions

- The surviving spouse facing Medicaid estate recovery who just received a letter from the Department of Social Services demanding reimbursement for nursing home costs — who needs to understand expanded recovery, the assets that are vulnerable (including joint accounts and living trusts), the assets that are protected, and the six-month deadline to file the Petition to Limit Financial Responsibility that caps the state's claim permanently

- The farm family inheriting appreciated agricultural land who needs to understand the step-up in basis, the Special Spousal Property Trust that provides a 100% double step-up unavailable in most states, and the agricultural land exclusion that blocks the $50,000 real property affidavit — who needs to know whether selling the farm will trigger a capital gains bill or whether the step-up eliminates it entirely

- The out-of-state heir who inherited South Dakota property — a hunting lodge, mineral rights, or a quarter section of farmland — who just learned that their home state's probate court has no jurisdiction over South Dakota real estate and they need ancillary proceedings in a state they have never lived in

- The adult child managing a small estate under $100,000 who assumes the small estate affidavit handles everything — who needs to know that the affidavit requires swearing under oath that no DSS debt exists, and that signing it when a Medicaid claim is outstanding means personal liability and potential perjury

- The executor who wants to know whether they even need a lawyer — who needs the decision framework that separates straightforward estates (final Form 1040, small estate affidavit, no Medicaid debt) from estates that genuinely require professional representation (contested wills, SSPT documentation, complex mineral rights, significant Medicaid recovery claims)

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across IRS publications, the South Dakota Unified Judicial System forms portal, the Department of Social Services website, the Department of Revenue motor vehicle guides, and county Register of Deeds offices that each maintain their own procedures. Here is what you actually encounter when you try to handle post-death taxes using free sources alone:

- The IRS publishes forms and instructions that assume you already know what applies. Publication 559 ("Survivors, Executors, and Administrators") is 36 pages of federal rules with zero South Dakota context. It does not tell you which state returns are unnecessary. It does not tell you about the SSPT double step-up. It does not mention that South Dakota's expanded Medicaid recovery can reach assets that bypass federal estate tax entirely. It gives you the rules for all fifty states and expects you to figure out which ones matter.

- The South Dakota Unified Judicial System gives you court forms and tells you to hire a lawyer. The UJS provides the probate petition, the inventory form, and the fee schedule. Every page states it "cannot provide legal advice." It does not tell you how to determine which tax returns the estate needs to file, how to avoid the compressed trust bracket, or how the small estate affidavit interacts with Medicaid recovery. Paperwork without strategy.

- The Department of Social Services explains its recovery authority but not your defenses. The DSS website describes expanded estate recovery and the assets it can reach. It does not prominently feature the six-month spousal petition that caps its own claims, the hardship waiver for farm families, or the specific demographic exemptions that bar recovery entirely. The agency explains its power, not your protections.

- Local estate attorneys highlight complexity to justify retainer fees. Attorney blog posts about South Dakota estate taxes are accurate — and they are written to convince you that the process is too dangerous to handle without paying $300 or more per hour. For estates with contested wills, DAPT structures, or significant Medicaid claims, that is true. For the majority of straightforward estates, the information costs a fraction of one billable hour.

- National financial sites treat South Dakota as a footnote. Fidelity, SmartAsset, and NerdWallet publish estate tax overviews that mention South Dakota's lack of state taxes in one sentence and move on. They do not cover the SSPT, the agricultural land exclusion, the expanded Medicaid recovery program, or any of the state-specific deadlines that determine whether your family settles this estate in months or spends years untangling mistakes.

Free resources give you fragments from a dozen sources that do not reference each other. The Federal Filing Roadmap puts every South Dakota-specific tax obligation, federal filing requirement, capital gains strategy, and Medicaid defense into one document, in the order you actually need them.

— Less Than Ten Minutes With a South Dakota Estate Attorney

A consultation with a South Dakota estate attorney costs $300 or more per hour. A CPA who specializes in fiduciary returns charges similar rates. National estate software platforms charge $15 to $40 per month in recurring subscription fees that continue billing whether you need them or not. This guide costs less than ten minutes of professional time and gives you the complete South Dakota-specific tax roadmap — every federal form, every filing deadline, every capital gains strategy, every Medicaid defense, and the decision tree that tells you whether you even need professional help at all.

Your download includes the complete 18-chapter guide, the standalone South Dakota Tax After Death Checklist, and eight printable reference tools — an estate evaluation decision tree, a master deadline calendar, a step-up in basis worksheet with SSPT documentation, a small estates affidavit guide, a Medicaid recovery reference with spousal petition procedures, a vehicle title transfer card with the 45-day deadline, a creditor priority reference with payment tracker, and a forms and contacts directory. Ten PDFs, instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on what the estate owes, what it does not owe, and exactly how to handle both, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free South Dakota Tax After Death Checklist — a structured checklist covering every tax and estate obligation after a death in South Dakota: which federal returns to file, which state returns do not exist, the Medicaid recovery deadlines, the vehicle transfer window, and the small estate affidavit traps. It is enough to see what you are dealing with and start organizing.

You did not ask for this responsibility. But you can handle it. The guide shows you exactly what is owed, what is not, and how to get through it — one chapter at a time.