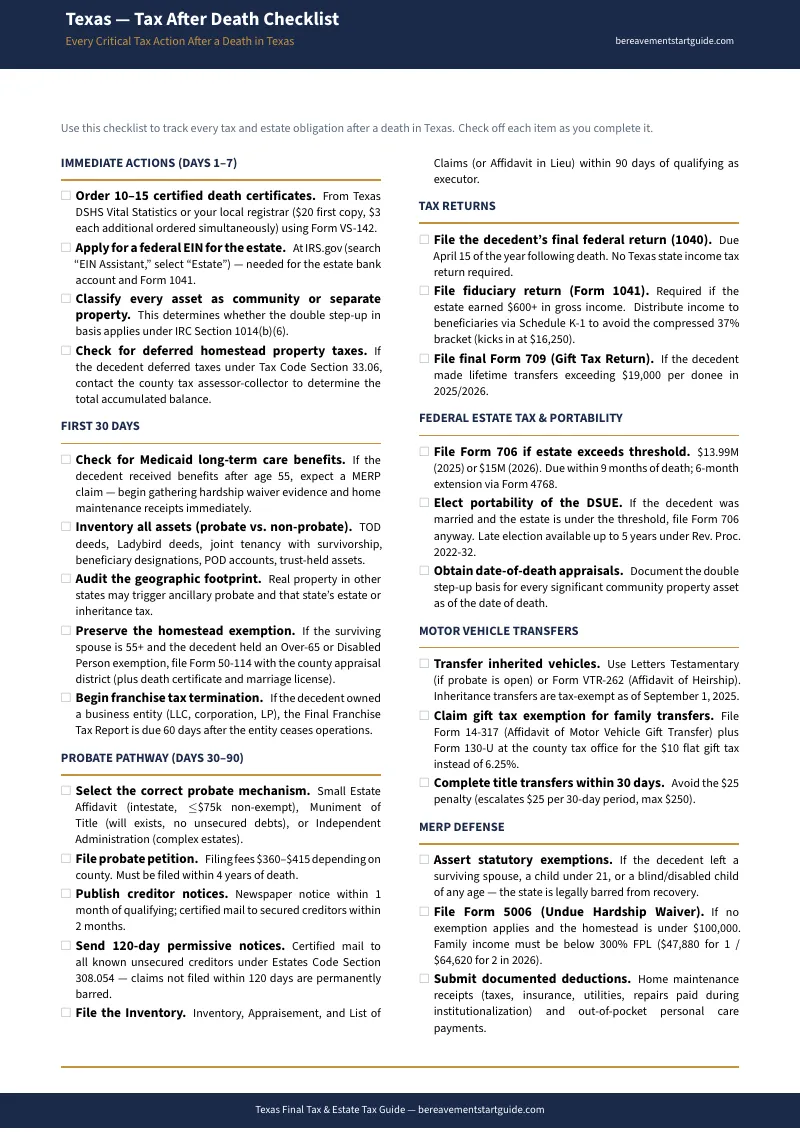

The Tax Filing Roadmap — Every Form, Deadline, and Trap Waiting for Texas Executors

Everyone told you Texas has no estate tax. No inheritance tax. "You're lucky," they said.

Then the IRS letter arrived. The county sent a property tax bill three times larger than last year's. The deceased's business partner called about a 60-day franchise tax deadline nobody mentioned. The CPA wants $2,500 to file returns you didn't know existed. And you're standing in the county tax office wondering why "no state tax" still means six federal and local tax obligations that each have their own forms, their own deadlines, and their own penalties for getting it wrong.

"No state estate tax" is the most dangerous half-truth in Texas probate. It makes families think the tax work is done. It isn't even close.

The Tax Filing Roadmap is a sequenced, executor-level manual that walks you through every tax obligation triggered by a death in Texas — in the order you need to file them. Not a blog post that says "consult your CPA." Not an IRS publication written in statutory language. A single document that tells you what to file, when to file it, which forms to use, and which costly mistakes to avoid at each step.

— Less Than 30 Minutes of CPA Time

Texas CPAs charge $150-$400 per hour for estate and fiduciary returns, with final tax filing packages routinely running $1,500-$3,000. This guide is your CPA Prep Kit: it identifies which returns actually apply to your estate, explains the elections that save money, and organizes your documents — so if you hire a professional, you spend their time on strategy, not on explaining what Form 1041 is or why you should care about portability.

What's Inside

The Final Form 1040 Walkthrough

The decedent's last income tax return covers January 1 through the date of death — but filing status, deductions, and income allocation depend on whether the marriage was community property or separate property, whether the surviving spouse remarries before year-end, and whether a personal representative or surviving spouse signs. Step-by-step instructions for each scenario, including the election to file jointly for the final year and why that decision can save thousands in tax.

The Form 1041 Decision Guide

If the estate earns $600 or more in income after the date of death — interest, dividends, rental income, asset sales — you owe a fiduciary income tax return. Most executors don't realize the estate is a separate taxpayer with its own EIN, its own brackets, and its own filing deadline. This chapter explains when Form 1041 is required, how to apply for an estate EIN, and when income should be distributed to beneficiaries (via Schedule K-1) to avoid the estate's compressed tax brackets that hit the top 37% rate at just $14,450.

The Portability Election — The $13.6 Million Decision Hiding in Form 706

Even when no federal estate tax is owed, filing Form 706 to elect portability transfers the deceased spouse's unused estate tax exemption to the survivor — up to $15 million in 2026. Skip this filing and the exemption vanishes forever. The deadline is 9 months from date of death (with a 6-month extension available), and the IRS offers a simplified procedure for estates that don't owe tax. This chapter walks you through the election, the simplified filing, and why this is the single most valuable form most Texas families never file.

The Community Property Double Step-Up

Under IRC Section 1014(b)(6), when one spouse dies in a community property state like Texas, both halves of community property receive a stepped-up basis to fair market value at date of death — not just the decedent's half. This means the surviving spouse can sell the family home, brokerage account, or rental property at today's value with zero capital gains tax on the appreciation. But you must document community property status correctly, and separate property only gets a step-up on the decedent's share. This chapter explains how to identify community vs. separate property and how to document the double step-up for every asset in the estate.

The Deferred Property Tax Trap

If the deceased had an Over-65 or Disabled homestead deferral, all deferred taxes plus 8% annual interest become due within 180 days of death. A homeowner who deferred $3,000 per year for 10 years could owe $30,000-$45,000 in back taxes and interest — and the county tax lien attaches to the property immediately. This chapter explains the deferral termination rules, how to calculate the payoff amount, the 180-day timeline, and the surviving spouse's options for assuming the deferral or paying from estate funds.

The Franchise Tax Final Report

If the deceased owned an LLC, corporation, or partnership registered in Texas, the entity's final franchise tax report and Public Information Report must be filed with the Comptroller within 60 days of termination. Miss this deadline and the Comptroller can forfeit the entity's right to do business, creating personal liability issues for the executor. This chapter covers the final report filing, the voluntary termination process, and the certificate of account status you'll need to close the entity cleanly.

Motor Vehicle Tax — $10 vs. 6.25%

Transferring a vehicle to a non-family member triggers the 6.25% Standard Presumptive Value tax — on a $30,000 truck, that's $1,875. But transfers between spouses, parents, children, and siblings qualify for the $10 gift tax rate using Form 14-317. This chapter explains who qualifies for the gift rate, the difference between Form VTR-262 (Affidavit of Heirship) and Form 130-U (Application for Title), and the 30-day transfer deadline before penalties begin.

The MERP Tax on Medicaid Recipients

If the deceased was 55 or older and received Medicaid-funded long-term care, the state may file a MERP claim against the probate estate to recover those costs. But MERP only reaches probate assets — life insurance, POD accounts, TOD deeds, and Ladybird deeds are exempt. And recovery is blocked entirely if the deceased is survived by a spouse, child under 21, or disabled child. This chapter explains the MERP claim process, the hardship waiver (Form 5006), and how to document exempt assets before the claim is filed.

Who This Guide Is For

- Executors and personal representatives who were told "Texas has no estate tax" and now face a stack of federal and local tax obligations they didn't expect

- Surviving spouses who need to understand the community property double step-up before selling any jointly held assets

- Adult children managing a parent's estate — especially when the parent had an Over-65 property tax deferral, a small business, or Medicaid coverage

- Families of business owners facing the 60-day franchise tax deadline and entity termination process

- Anyone who inherited property in Texas and needs to understand cost basis, capital gains, and whether to file Form 706 for portability

Why Not Just Use Free Resources?

You can. Every form, deadline, and rule in this guide exists somewhere across irs.gov, the Texas Comptroller's website, your county appraisal district, and IRS Publications 559 and 950. That's the problem — "somewhere" across dozens of dense pages written in statutory language, with no sequencing and no explanation of how the Form 1040 filing interacts with the Form 1041 requirement, how the portability election deadline overlaps with the property tax deferral timeline, or why the community property classification matters for every return you file.

National estate tax guides say "Texas has no state estate tax" and move on. CPA blogs explain Form 706 in isolation but don't tell you that the deferred property tax bill is due 180 days after death while your portability election deadline is 9 months out. IRS publications don't cover Texas-specific issues at all — no mention of the double step-up, franchise tax, or MERP. This guide connects everything in one filing sequence built specifically for Texas estates.

What You Get

- The Complete Tax Filing Roadmap — every federal and Texas-specific tax obligation in chronological filing order, from the final Form 1040 through entity termination and MERP defense

- Quick Start Checklist — the most critical tax actions and deadlines in the exact order you need to address them

- Tax Obligation Worksheet — fill-in tracker mapping every return, the form number, the filing deadline, and your estimated liability

- Key Contacts and Forms Reference — every IRS form, Comptroller filing, and county office on one printable sheet

Satisfaction Guarantee

If the Tax Filing Roadmap doesn't save you time, confusion, or money — email [email protected] and we'll make it right. No questions, no hassle.

Start Filing With Confidence

Download the free Texas Tax After Death Checklist for the most critical tax deadlines and actions — or get the complete Tax Filing Roadmap with full step-by-step instructions, the portability election walkthrough, community property double step-up documentation, deferred property tax trap analysis, and every form you'll need.