Someone You Love Just Died in Utah. You Googled "Utah Estate Tax" and Got Twelve Different Answers. Five of Them Were Wrong. The Right Answer Involves Three Separate Tax Returns You Didn't Know Existed.

You are sitting at the kitchen table with the death certificate, a stack of unopened tax notices, and a browser full of tabs that contradict each other. One website says Utah has no estate tax. Another says you owe inheritance tax on the house. A third mentions something called a "fiduciary income tax return" and assumes you know what that means. The funeral was last week, the Relief Society meals are winding down, and the administrative reality is just now settling in: you are personally responsible for filing taxes on behalf of someone who died, and the wrong filing — or the missed filing — creates penalties that come out of your pocket, not the estate's.

Here is the short version: Utah has no estate tax. Utah has no inheritance tax. The state's pick-up tax was eliminated on December 31, 2004, and it has not come back. The vast majority of Utah estates owe zero dollars in state death taxes. But that does not mean the tax work is done. It means the tax work is different — and more confusing — than what you expected.

The deceased owes a final individual income tax return to both the IRS and the Utah State Tax Commission. If the estate earns any income after the date of death — rental payments, stock dividends, interest on bank accounts, a final paycheck — it owes a separate fiduciary income tax return. If the estate is large enough to cross the federal threshold (currently $15 million per individual), a federal estate tax return is required even though Utah imposes nothing at the state level. If you are inheriting property and plan to sell it, the step-up in basis rules determine whether you owe capital gains tax or nothing at all — and one common family mistake (adding a child's name to a deed during a parent's lifetime) can destroy a tax benefit worth tens of thousands of dollars.

The Utah Final Tax & Estate Tax Guide is a Tax Map System for every filing, every form, every deadline, and every trap between the date of death and the final distribution of assets. Not a generic national overview. Not a blog post that says "consult your CPA." A Utah-specific manual that separates the taxes you actually owe from the taxes you are afraid of owing — and walks you through both categories step by step, form by form, deadline by deadline.

What's Inside the Tax Map System

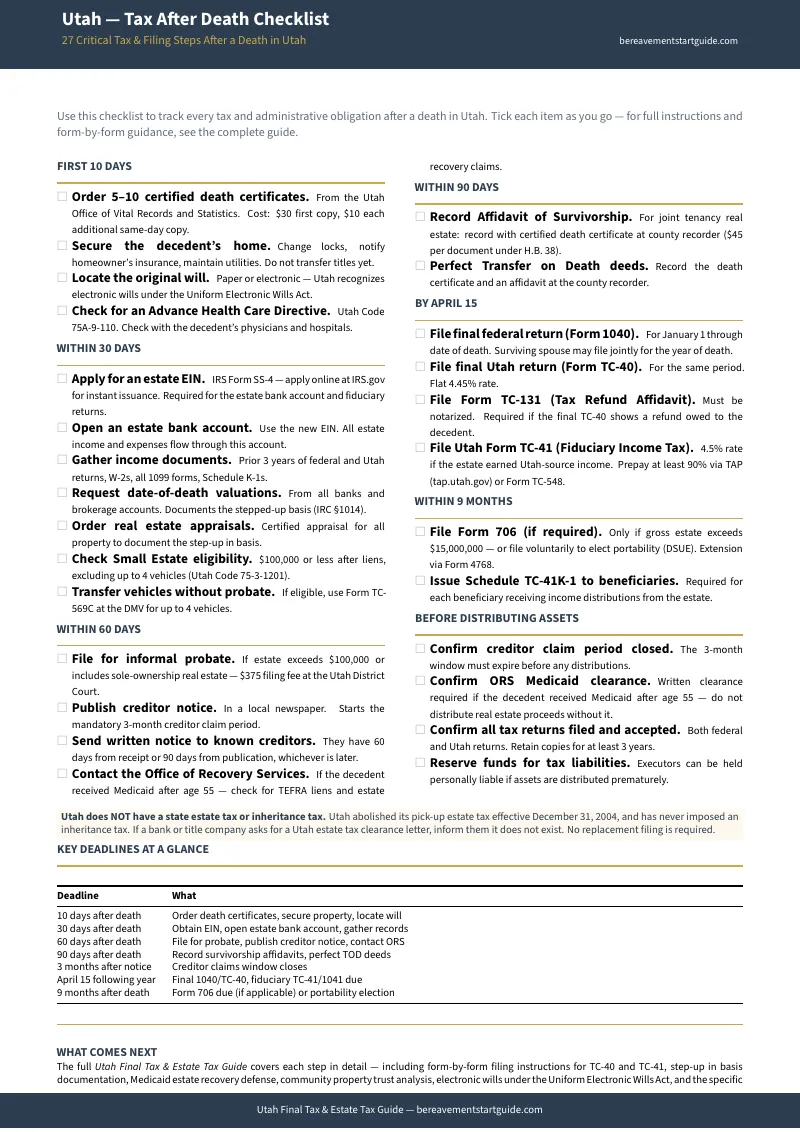

An 18-chapter guide, the Tax Obligations Checklist, and 8 standalone printable tools — covering every tax responsibility from the date of death through final distribution, built specifically for Utah statutes, Utah State Tax Commission forms, and the federal-state intersection that makes filing taxes for a deceased person different from filing your own. Includes a tax deadline calendar, document collection checklist, forms reference card, step-up in basis worksheet, probate route decision tree, creditor claim tracker, Medicaid recovery checklist, and executor mistakes fridge sheet — all designed to print and bring to meetings or pin to your wall:

The Final Individual Income Tax Return (Form TC-40)

The deceased earned income from January 1 through the date of death. That income must be reported on a final Utah Form TC-40. You need to check the "Deceased" box on page three of the return, enter the exact date of death, and file by April 15 of the year following the death. If you miss the deadline, you file for an extension using Form TC-546. If the deceased is owed a state refund, you cannot simply deposit the check — you must file a separate TC-131 Tax Refund Affidavit, have it notarized, and submit it to the Utah State Tax Commission before they will release the money. The guide walks through every field, every box, every signature requirement — because a rejection on the TC-131 means the refund sits in state hands for months while you figure out what went wrong.

The Fiduciary Income Tax Return (Form TC-41)

If the estate generates any income after the date of death — rental income from the deceased's property, dividends from stocks held during probate, interest from bank accounts that have not been distributed — the estate itself becomes a taxpayer. It needs its own Employer Identification Number from the IRS. It files its own return: Utah Form TC-41. The numbers from the federal Form 1041 flow directly down to the TC-41, but filing the federal form does not exempt you from filing the state form. Both are required. The guide explains when the TC-41 is triggered, how to choose between a calendar year and a fiscal year, and how income distributed to beneficiaries gets reported on their individual returns through Schedule K-1.

The Federal Estate Tax Return (IRS Form 706)

Utah does not have its own estate tax. But the federal estate tax still applies to estates exceeding the exemption threshold — $15 million per individual in 2026. Most Utah families will never need to file this return. But even if the estate is well below the threshold, there is one strategic reason to file: portability. Filing Form 706 allows a surviving spouse to claim the deceased spouse's unused federal exemption, effectively doubling their own protection to $30 million. If the surviving spouse has significant assets or expects to inherit more, the portability election is worth thousands in future tax savings — and it requires a timely filing that many families miss because nobody told them it existed.

Step-Up in Basis: The Tax Benefit Worth More Than This Guide

When someone dies, the IRS resets the taxable value of their assets to the fair market value on the date of death. A house purchased in 1985 for $60,000 that is worth $450,000 today does not carry $390,000 in built-in capital gains for the person who inherits it. The heir's tax basis starts at $450,000. If they sell the house next month for $455,000, the capital gains tax applies to $5,000, not $390,000. This single rule can save an inheriting family tens of thousands of dollars. But it only works if the property transfers at death. When families try to avoid probate by adding a child's name to the deed during the parent's lifetime, they destroy the step-up entirely. The child inherits the parent's original $60,000 basis and owes capital gains on the full appreciation when they sell. The guide explains exactly how the step-up works, how Transfer on Death deeds preserve it, and the specific lifetime transfers that eliminate it.

Medicaid Estate Recovery and the Tax Intersection

If the deceased received Medicaid benefits after age 55 — nursing home care, home health services, long-term care — Utah's Office of Recovery Services can pursue reimbursement from the estate. Utah operates under an expanded recovery model. Under Utah Code Section 75-2-205, the state can reach into non-probate assets: Transfer on Death deeds, joint tenancy property, payable-on-death accounts, and living trust assets. Before you calculate what taxes are owed on distributed assets, you need to know whether the state has a prior claim. The guide maps the recovery hierarchy, the protected categories (surviving spouse, minor children, blind or permanently disabled dependents), and the hardship exemptions that may reduce or eliminate the state's claim.

Selling Inherited Property: Capital Gains in Practice

You inherited a house. You want to sell it. The date of death establishes your new tax basis. If the property appraises at $400,000 on the date of death and you sell it three months later for $405,000, the taxable capital gain is $5,000. If you hold the property for two years and it appreciates to $460,000, the gain is $60,000. The timing of the sale, the accuracy of the date-of-death appraisal, and whether you used the property as a primary residence all affect the tax outcome. The guide covers the calculation, the appraisal requirements, the documentation you need to support your basis if the IRS audits the return, and the specific Utah property tax implications of a title transfer.

Tax Deadlines After Death: The Calendar You Need

From the date of death through the final distribution, every tax obligation runs on its own clock. The final TC-40 is due April 15 of the year after death. The TC-41 deadline depends on whether you elected a calendar year or fiscal year. Federal estimated payments may be due quarterly. The TC-131 refund affidavit has no statutory deadline but delays mean the state holds your money indefinitely. The guide consolidates every deadline into one sequential calendar — so you stop discovering deadlines after you have already missed them.

The EIN Application and Estate Bank Account

The deceased's Social Security number dies with them for tax purposes. Any income the estate earns after death must be reported under a new Employer Identification Number. You apply online through the IRS — it takes ten minutes. Then you open a dedicated estate bank account at any bank, using the EIN, the Letters Testamentary or Letters of Administration from the court, and the death certificate. Every dollar of estate income flows through this account. Every expense is documented. The guide walks through the application, the account setup, and the record-keeping requirements that protect you from personal liability when the court reviews your administration.

Funeral Expense Deductions: What Actually Works and What Does Not

Executors frequently assume funeral costs are tax-deductible. They are — but only on IRS Form 706, the federal estate tax return. Since the vast majority of Utah estates fall below the $15 million federal threshold and do not file a 706, the deduction is functionally unavailable. Funeral expenses are absolutely not deductible on the final individual income tax return (Form 1040 or TC-40). They are not deductible on the fiduciary income tax return (Form 1041 or TC-41). Attempting to claim them on the wrong return triggers audit flags. The guide clears up this misconception and explains where funeral costs do legitimately reduce the estate's exposure — so you stop chasing a deduction that does not exist for your situation.

Who This Guide Is For

- The executor who just learned there are three separate tax returns to file — the final individual return (TC-40), the fiduciary return (TC-41), and potentially the federal estate return (706) — and needs to know which ones apply, which forms to use, and when each one is due

- The surviving spouse wondering about portability — who has heard the term but does not know whether filing a federal Form 706 for a modest estate is worth the effort, or what they lose by skipping it

- The beneficiary inheriting real estate — who needs to understand the step-up in basis before listing the house, and who needs to know whether a lifetime deed transfer already destroyed the tax benefit they were counting on

- The family facing a Medicaid recovery claim — who needs to understand what assets the state can reach, what is protected, and how to resolve the recovery claim before calculating distributable assets and their tax consequences

- The adult child managing a parent's estate from out of state — who needs every Utah-specific tax form, deadline, and filing requirement in one document, because their home-state CPA does not know what a TC-131 is

- The person whose CPA handles their personal taxes but has never filed for a decedent — who needs the Utah-specific supplement to hand their accountant alongside the federal requirements

Why Free Resources Will Not Get You Through This

The information is technically available. It is scattered across the Utah State Tax Commission website, the IRS publications, the Utah Courts portal, and attorney blogs that want you to book a consultation. Here is what you actually encounter when you try to do this on your own:

- The Utah State Tax Commission website gives you forms, not instructions. You can download the TC-40, the TC-41, and the TC-131. The forms come with line-by-line worksheets written for CPAs, not for a grieving executor filing for the first time. There is no guidance on which forms apply to your situation, what order to file them in, or what happens if you file the wrong one. The form instructions assume you already understand the fiduciary tax system — the guide assumes you do not.

- National aggregators miss Utah-specific details. SmartAsset, Nolo, and FindLaw will tell you Utah has no estate tax. They will not tell you about the TC-131 refund affidavit and its notarization requirement. They will not explain how the TC-41 interacts with the federal 1041. They will not warn you about Utah's expanded Medicaid recovery rules reaching into assets you thought were protected. Their content is programmatic — one page for each state, assembled from a template that treats Utah the same as any other state.

- Attorney blogs highlight complexity to justify consultation fees. Local probate attorneys charge $250 to $450 per hour. Their blog posts explain just enough about the tax system to make you feel overwhelmed, then conclude with a phone number. For contested estates and complex trust structures, professional counsel is essential. For the executor of a straightforward estate who needs to file three forms correctly and on time, thousands in legal fees for what is fundamentally an administrative task does not make sense.

- Tax software handles the living, not the dead. TurboTax and H&R Block handle standard individual returns. They do not walk you through the deceased checkbox, the TC-131 refund process, or the fiduciary return. If you try to file a decedent return through consumer tax software without understanding the Utah-specific requirements, you will make errors the software cannot catch.

Our Guarantee

If this guide does not give you a clearer understanding of Utah's tax obligations after death than anything you found for free, reply to your receipt within 30 days and we will refund every cent. No forms, no questions.

Two Ways to Start

Start free: Download the Utah — Tax After Death Checklist. It covers every tax obligation at a glance — which returns are required, which deadlines apply, and the one-page action plan for the first 30 days after death.

Go deeper: The full Utah Final Tax & Estate Tax Guide () walks you through the complete Tax Map System — the final income tax return, fiduciary return, federal estate tax, step-up in basis, capital gains on inherited property, Medicaid recovery, funeral expense deductions, EIN setup, and every deadline from the date of death through final distribution — organized so you always know what to file next and why.