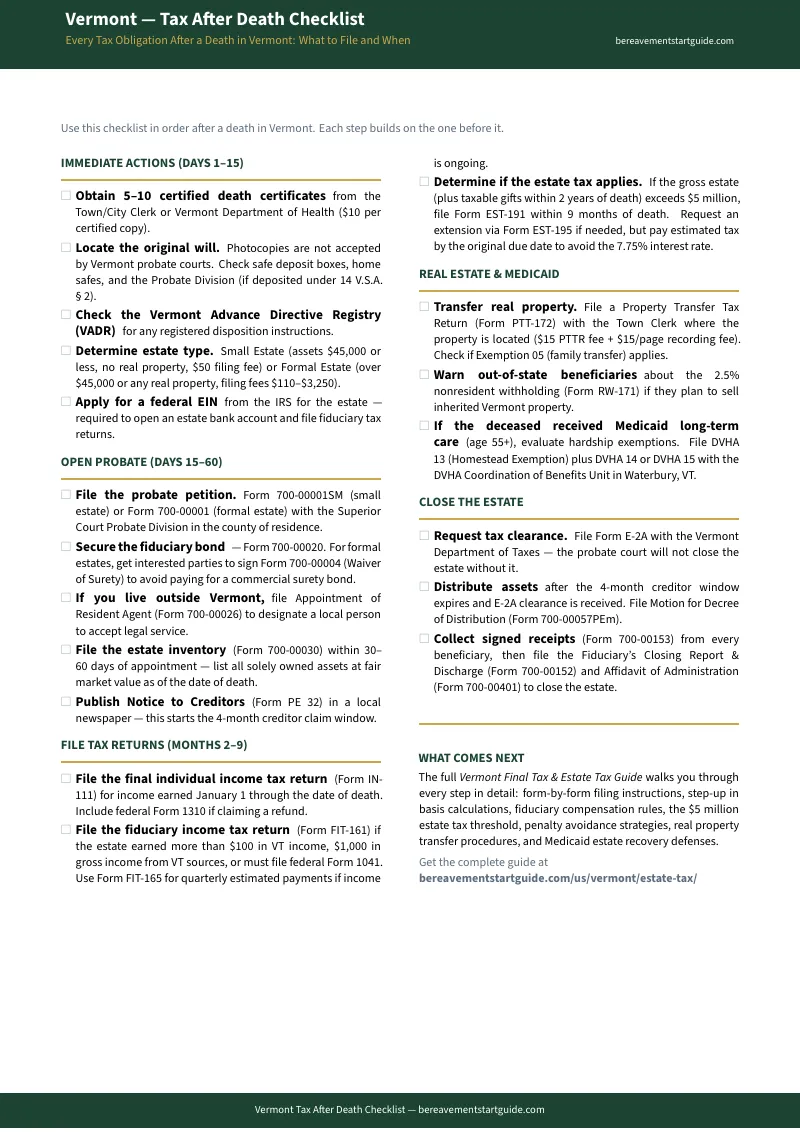

Someone You Love Just Died in Vermont. The Probate Court Will Not Close the Estate Until the Commissioner of Taxes Signs Off. You Have Never Heard of Form E-2A.

You are sitting at the kitchen table with a stack of papers from the probate court, a browser full of tabs from five different Vermont government websites, and a growing realization that nothing closes until the state says the taxes are paid. One site explains the estate tax. Another mentions a fiduciary income tax return triggered by just $100 of estate income. A third references something called a "tax clearance" without explaining how to get one. The funeral was last week. The family is asking when they will receive their inheritance. And you are personally responsible for filing every return correctly, because under Vermont law, an executor cannot be discharged until the Commissioner of Taxes issues a receipt proving all taxes are settled.

Here is what makes Vermont different: Vermont is one of a handful of states that levies its own estate tax — a flat 16% on estates exceeding $5 million, with no inflation indexing and no portability between spouses. Most Vermont estates fall below that threshold. But that does not mean the tax work is done. The estate still owes a final individual income tax return. If the estate earns more than $100 in Vermont income after the date of death — interest from a bank account, a final paycheck, rental income from the house — a separate fiduciary return is required. If the estate includes real property and an out-of-state beneficiary wants to sell it, the buyer is legally required to withhold 2.5% of the sale price and send it directly to the Vermont Department of Taxes. And when you go to record a deed, you will not find a county recorder's office — because Vermont does not have them. All 246 towns maintain their own land records independently.

The Vermont Final Tax & Estate Tax Guide is a Clearance Sequence System — a plain-English manual built around the one document that unlocks the end of probate: Form E-2A, the Vermont Tax Clearance. Every chapter, every checklist, every form walkthrough feeds into a single goal: getting the Commissioner of Taxes to confirm that all obligations are satisfied so the probate court will discharge you and release the estate to the people waiting for it.

What's Inside the Clearance Sequence System

A comprehensive guide, the Tax Obligations Checklist, and standalone printable tools — covering every tax responsibility from the date of death through the Form E-2A clearance and final distribution, built specifically for Vermont statutes, Vermont Department of Taxes forms, and the decentralized town clerk system that makes this state unlike any other:

The Final Individual Income Tax Return (Form IN-111)

The deceased earned income from January 1 through the date of death. That income must be reported on a final Vermont Form IN-111. You need to mark the return as a final filing, enter the exact date of death, and file by April 15 of the year following the death. If the deceased is owed a state refund, you must establish legal authority to claim it — and a rejected claim means the refund sits with the Department of Taxes while you sort out the paperwork. The guide walks through every field, every signature requirement, and the specific documentation Vermont requires before releasing money owed to a deceased taxpayer.

The Fiduciary Return of Income (Form FIT-161)

This is the form that catches executors off guard. If the estate generates more than $100 in Vermont income after the date of death — not $600, not $1,000, but $100 — the estate itself becomes a Vermont taxpayer. You need a federal Employer Identification Number from the IRS. You file the federal Form 1041 first, then the Vermont FIT-161. Estimated payments may be required using Form FIT-165. And if the IRS later adjusts the federal 1041, you are legally required to file an amended Vermont return within 60 days of notification — regardless of the standard three-year statute of limitations. The guide explains the triggers, the payment vouchers, the fiscal year election, and the Schedule K-1 distribution reporting that determines what beneficiaries owe on their own returns.

The Vermont Estate Tax Return (Form EST-191)

Vermont imposes a flat 16% estate tax on the taxable estate exceeding $5 million. The return is due within nine months of death, with a six-month extension available via Form EST-195. Unlike the federal system, Vermont does not index the exemption for inflation and does not recognize portability between spouses. That means a surviving spouse cannot claim any unused portion of the deceased spouse's exemption — and moderately wealthy families are exposed in ways the federal code does not create. The guide explains the threshold calculation, the extension process, and the strategic considerations for married couples whose combined estates approach the line.

The Form E-2A Tax Clearance: The Finish Line

Nothing closes without this document. Under 32 V.S.A. Section 7454, an executor cannot be discharged, a final accounting cannot be waived, and assets cannot be distributed to beneficiaries until the Commissioner of Taxes issues a clearance confirming all state taxes are settled. The E-2A is the final step in a sequence — and every other chapter in this guide feeds into it. Filing the IN-111, the FIT-161, and (if applicable) the EST-191 are all prerequisites. The guide maps the exact sequence: which forms to file, in what order, and what documentation to submit with the E-2A application so the clearance is issued without delays or rejections.

The Real Estate Trap: Property Transfer Tax and Nonresident Withholding

Selling or transferring inherited property in Vermont triggers two taxes that routinely blindside executors. The Property Transfer Tax (PTT-172) applies to deed transfers at 1.25% plus a 0.22% Clean Water Surcharge — but specific exemptions exist for family transfers without consideration. The town clerk will not record the deed without a properly completed PTT-172. Separately, when real estate is sold by a nonresident — which includes many out-of-state beneficiaries — the buyer must withhold 2.5% of the sale price and remit it to the state using Form RW-171. The guide details both taxes, both sets of exemptions, and the election procedures that can prevent an out-of-state beneficiary from losing thousands to a withholding they did not know existed.

Step-Up in Basis: The Tax Benefit You Cannot Afford to Lose

When someone dies, the IRS resets the taxable value of their assets to the fair market value on the date of death. A house purchased in 1972 for $35,000 that is worth $380,000 today does not carry $345,000 in built-in capital gains for the person who inherits it. The heir's basis starts at $380,000. If they sell next month for $385,000, capital gains apply to $5,000, not $345,000. But this benefit only works if the property transfers at death. When families add a child's name to the deed during the parent's lifetime to "avoid probate," they destroy the step-up entirely. The guide explains how the step-up works in Vermont, how Transfer on Death deeds preserve it, and the specific lifetime transfers that eliminate it.

Medicaid Estate Recovery (DVHA Forms 13/14/15)

If the deceased received Medicaid-funded long-term care after age 55, the Department of Vermont Health Access will file a claim against the probate estate. The family home may be at risk — but statutory protections exist. The state will not pursue recovery if a surviving spouse, a disabled child, or a caregiving child who lived in the home for two continuous years before the decedent's admission to care still resides there. Estates valued under $2,000 are also exempt. The guide maps the DVHA claim process, the hardship waiver procedures, and the intersection between Medicaid recovery and tax obligations — because the recovery amount must be resolved before you can calculate what is distributable and what taxes apply to distributions.

The 246 Town Clerks: Vermont's Decentralized Record System

In most states, you visit the county recorder to file deeds, obtain vital records, and research property titles. Vermont does not have county recorders. All land records, vital statistics, and deed recordings are maintained at the municipal level — across 246 separate town clerk offices. Each charges its own fees (typically $15 per page for deeds, $10 for certified vital records). Town clerks do not perform title research for the public. The guide explains which town clerk offices you need, what documents to bring, and how to navigate a system designed for people who grew up in Vermont and already know where to go.

Standalone Printable Tools (5 Reference Sheets)

Print these and keep them with your paperwork:

- E-2A Clearance Sequence Checklist — Every prerequisite and closing step in order, with checkboxes and date fields

- Estate Tax Deadline Tracker — Fill in the date of death and calculate every filing deadline on one page

- Real Estate Transfer Checklist — Everything you need for the town clerk visit: forms, fees, documents, and the nonresident withholding trap

- Vermont Tax Forms Reference — Every court, tax department, DVHA, and IRS form number with its title

- Key Thresholds Quick Reference — Exemption amounts, tax rates, deadlines, fees, and penalty rates at a glance

Who This Guide Is For

- The executor who just discovered there is no discharge without a tax clearance — who needs to understand the E-2A requirement and every filing that must be completed before applying for it

- The surviving spouse navigating an estate without portability — who cannot carry over the deceased spouse's $5 million Vermont exemption and needs to understand what that means for their own estate planning

- The out-of-state executor managing a Vermont estate remotely — who has never heard of town clerks, cannot find a county recorder, and just learned about the 2.5% nonresident withholding on the house sale they were counting on

- The beneficiary inheriting real estate in Vermont — who needs to understand the step-up in basis before listing the house and needs to know what the Property Transfer Tax and Clean Water Surcharge will cost at closing

- The family facing a Medicaid estate recovery claim from DVHA — who needs to understand what is protected, what is exposed, and how to resolve the claim before calculating distributable assets

- The person whose CPA handles their personal taxes but has never filed for a decedent in Vermont — who needs to hand their accountant every Vermont-specific form, threshold, and deadline in one document

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across the Vermont Department of Taxes, the Vermont Judiciary, 246 town clerk websites, and attorney blogs that want you to book a $350/hour consultation. Here is what you encounter when you try to piece it together yourself:

- The Vermont Department of Taxes gives you forms, not a sequence. You can download the FIT-161, the EST-191, and the E-2A. Each form comes with instructions written for tax professionals. There is no guidance connecting the fiduciary return to the estate tax return to the tax clearance application. The Department publishes each form in isolation — the guide puts them in order.

- National aggregators miss the details that matter here. SmartAsset, Nolo, and FindLaw will tell you Vermont has a $5 million estate tax exemption. They will not mention the $100 fiduciary filing threshold. They will not explain the 2.5% nonresident withholding on Form RW-171. They will not warn you that Vermont has 246 town clerks instead of county recorders. Their content runs from a template that treats Vermont the same as every other state — and Vermont is not the same as every other state.

- Local attorney blogs diagnose the problem and sell you the solution. Vermont probate attorneys charge $300 to $400 per hour. Their blog posts explain just enough to make you anxious, then offer a phone number. For contested estates and complex trusts, professional counsel is essential. For the executor who needs to file the right forms in the right order and get the E-2A clearance, paying $350/hour for what is fundamentally an administrative sequence does not make sense.

- The Vermont Judiciary website explains probate rules but not tax rules. The court tells you that a tax clearance is required to close the estate. The court does not tell you how to get one. You need to cross over to the Department of Taxes site to find the E-2A, then figure out on your own that every preceding return must be filed and settled first. The guide bridges the gap between the court requirements and the tax filings that satisfy them.

Our Guarantee

If this guide does not give you a clearer understanding of Vermont's tax obligations after death than anything you found for free, reply to your receipt within 30 days and we will refund every cent. No forms, no questions.

Two Ways to Start

Start free: Download the Vermont — Tax After Death Checklist. It covers every tax obligation at a glance — which returns are required, which deadlines apply, and the one-page action plan for the first 30 days after death.

Go deeper: The full Vermont Final Tax & Estate Tax Guide () includes 7 PDFs — the complete guide, the checklist, and 5 standalone printable tools — walking you through the complete Clearance Sequence System from the final income tax return through the fiduciary return, estate tax return, real estate withholding, step-up in basis, Medicaid recovery, and the Form E-2A tax clearance.