Virginia Has No Estate Tax and No Inheritance Tax. But the Commissioner of Accounts Is Auditing Every Dollar You Touch --- And the Deadlines Started Running the Day You Qualified.

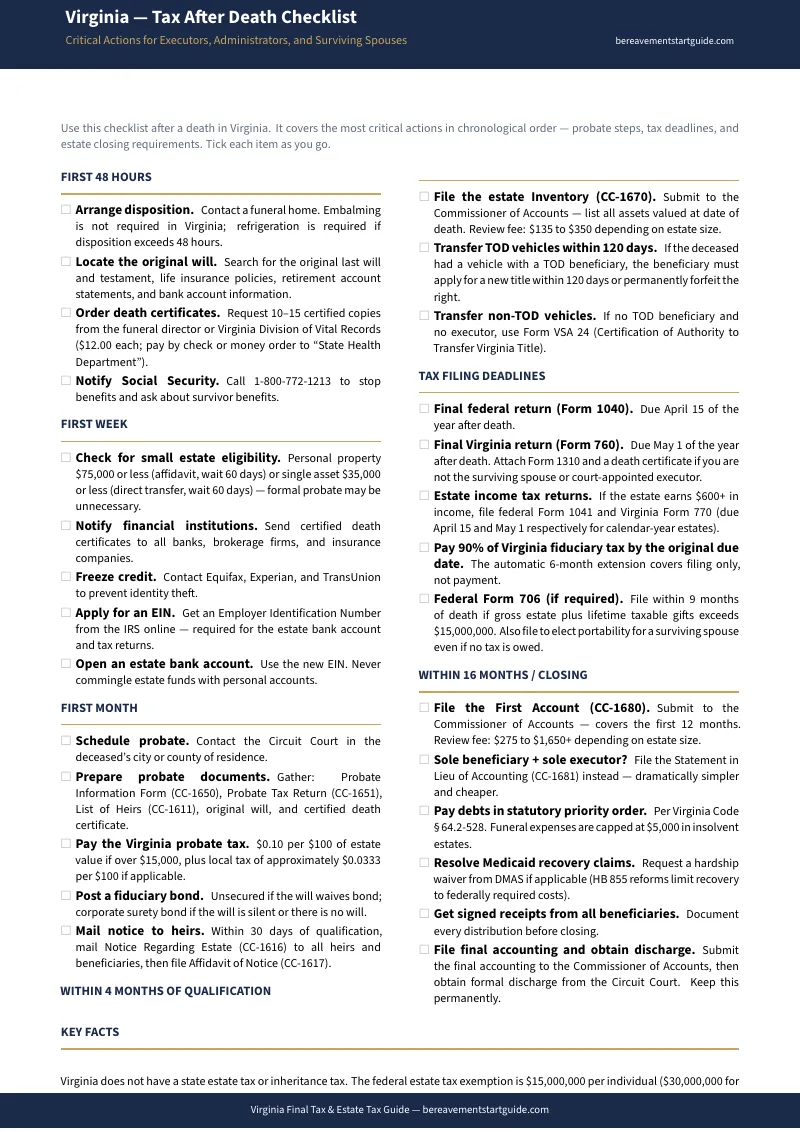

Someone has died, and you have been appointed to settle the estate in Virginia. You went to the Circuit Court, took the oath, paid the probate tax, and received your Certificate of Qualification. What you were not told is that a court-appointed attorney called the Commissioner of Accounts is now monitoring your every financial move. You have four months to file a detailed inventory of every asset. You have sixteen months to file a line-item accounting of every dollar that entered or left the estate --- with cancelled checks and signed receipts as proof. The Commissioner's audit fees start at $275 and climb past $1,650. Miss a deadline and you face personal delinquency fees. Get the accounting wrong and you face personal liability.

Meanwhile, the tax obligations are piling up. The decedent's final Virginia Form 760 is due by May 1. The estate's own fiduciary return --- Form 770 --- has a separate deadline, a separate set of rules, and a 90% payment trap that triggers escalating penalties if you underpay by even a few hundred dollars. The federal Form 1041 runs on yet another timeline. And you just learned that the real estate you thought you controlled "dropped like a stone" directly to the heirs the moment the decedent died --- meaning you cannot sell it, rent it, or manage it unless the will explicitly gave you that power. You are grieving, you are overwhelmed, and the clock is running on at least four different deadlines at once.

The Virginia Final Tax & Estate Tax Guide is a Commissioner Defense System built specifically for the Virginia fiduciary oversight model that no national guide covers. Not a generic probate checklist. Not a funeral home pamphlet. A plain-English, Virginia-specific tax and accounting reference that tells you which taxes apply, which do not, what forms to file, what deadlines to meet, how to structure the inventory and accounting to pass the Commissioner's audit, and how to protect yourself from personal liability at every step.

What's Inside the Commissioner Defense System

A comprehensive guide and a quick-start tax checklist --- covering every tax obligation, Commissioner filing, asset transfer strategy, and statutory deadline that Virginia executors and beneficiaries face after a death:

The Tax Landscape: What You Owe and What You Don't

The chapter that stops the panic. Virginia repealed its estate tax effective July 1, 2007. The state does not impose an inheritance tax. Beneficiaries owe nothing to Virginia on the assets they receive. But four tax obligations do apply: the decedent's final individual return (Virginia Form 760), the estate's fiduciary income tax return (Form 770), the state and local probate tax assessed at qualification, and --- for estates exceeding $15 million --- the federal estate tax (Form 706). The guide maps every tax to its form, its deadline, and its filing sequence so you stop searching for obligations that do not exist and start addressing the ones that do.

The 90% Payment Rule and Form 770 Penalties

The trap that catches most executors. Virginia grants an automatic six-month extension to file Form 770. But the extension applies only to the paperwork --- not the payment. If you fail to pay at least 90% of the final tax liability by the original due date, Virginia imposes a 2% per month extension penalty capped at 12%. Miss the extended deadline entirely and the penalty jumps to 6% per month, capped at 30%. A separate 6% late payment penalty runs concurrently. The guide explains exactly how to calculate the 90% threshold, which electronic payment forms to use (770-PMT, 770ES, 770IP), and why international ACH transactions are automatically rejected.

Commissioner of Accounts: Inventory, Accounting, and Audit Fees

The system that makes Virginia different from every other state. Within four months of qualification, you must file Form CC-1670 --- a five-part inventory categorizing personal property, multi-party bank accounts, and real estate into separate classifications based on whether you have the power to sell. Sixteen months after qualification, you must file Form CC-1680 --- a line-item accounting where beginning assets plus all receipts must exactly equal all disbursements plus assets on hand. Every single payment requires physical proof. The Commissioner charges $135 to $350 for the inventory review and $275 to $1,650-plus for the accounting audit. The guide walks you through both filings step by step, with the exact format the Commissioner expects.

The "Drops Like a Stone" Doctrine

The Virginia rule that shocks every out-of-state executor. In Virginia, real property vests immediately in the heirs or devisees at the exact moment of death. The executor has zero authority over the real estate unless the will explicitly grants a power of sale or the court issues a specific order. This means you cannot list, sell, or manage inherited property without express legal authority. But it also means heirs who take possession and sell the property can be sued directly by the decedent's creditors for debts up to the value of the real estate --- even if probate was never opened. The guide explains how to file the Real Estate Affidavit (Form CC-1612) to establish chain of title, when to petition the court for a power of sale, and how to use the step-up in basis to eliminate capital gains tax on inherited property.

Step-Up in Basis and Selling Inherited Property

The most valuable tax benefit available to heirs. When you inherit property, the IRS resets the cost basis to the fair market value on the date of death. A house purchased for $180,000 that is worth $450,000 at the date of death gets a new basis of $450,000. Sell it the next month and the capital gains tax is zero. But the benefit requires documentation --- a date-of-death appraisal, proper title transfer, and correct reporting on the final returns. The guide explains exactly how to secure the step-up, how alternate valuation dates work for federal estate tax purposes, and why selling before documenting the basis can cost heirs tens of thousands of dollars.

Small Estate Alternatives: $75,000 and $35,000 Thresholds

The escape routes that bypass the Commissioner entirely. If the total personal probate estate is $75,000 or less, designated successors can claim assets through a Small Asset Affidavit under Virginia Code Section 64.2-601 --- no court qualification, no Commissioner oversight, no accounting fees. For assets under $35,000, a single heir can collect directly from a financial institution without even an affidavit. The guide covers the 60-day waiting period, the notarization requirements, and what to do when a bank refuses to honor the statute because their staff has never heard of it.

The Debts and Demands Hearing

The liability shield most executors never learn about. For approximately $350 paid to the Commissioner, the executor can force every creditor to present their claims by a fixed deadline. Creditors who fail to appear forfeit their claims permanently. This single procedural step can eliminate thousands of dollars in disputed debts and protect the executor from personal liability for claims that surface after distribution. The guide explains when this hearing is worth the cost, how to petition for it, and what happens to creditors who miss the deadline.

Medicaid Estate Recovery and HB 855

The chapter that provides the most relief for families who fear losing the home. If the decedent received Medicaid long-term care after age 55, the Department of Medical Assistance Services is mandated to seek reimbursement from the estate. But the 2026 House Bill 855 reforms significantly constrain DMAS recovery --- limiting it strictly to federally required costs, capping managed care recovery at the lesser of the capitated rate or the recoverable portion, and making hardship waivers for low-income heirs permanent. The guide details every exemption (surviving spouse, minor children, disabled dependents), every waiver criterion, and every procedural step to respond to a DMAS claim.

Surviving Spouse Protections and the Elective Share

Virginia treats marriage as an economic partnership and prohibits complete disinheritance. A surviving spouse can claim up to 50% of the marital property portion of the augmented estate --- with the marital property percentage scaling from 3% for marriages under one year to 100% for marriages of fifteen years or more. In addition, the surviving spouse is entitled to up to $25,000 in homestead allowance, $25,000 in exempt property, and $30,000 in family allowance --- all of which take priority over nearly every other estate obligation. The guide explains the augmented estate calculation, the marriage-length scale, and the specific allowances available.

Probate Tax, Federal Portability, Vehicle Transfers, and Closing

The state probate tax assessed at 10 cents per $100 of estate value (plus a local surcharge of one-third the state rate). The federal portability election that lets a surviving spouse capture the deceased spouse's unused $15 million exemption by filing Form 706 --- even when the estate owes zero federal tax. Vehicle title transfers through the DMV using Forms VSA 18 and VSA 24, including the strict 120-day window that permanently forfeits Transfer on Death rights if missed. And the complete estate-closing procedure: final accountings, tax clearances, the Statement in Lieu of Settlement (Form CC-1681) shortcut for sole-beneficiary executors, and final distribution to heirs.

Who This Guide Is For

- The executor facing the Commissioner for the first time --- who just qualified at the Circuit Court, received the four-month inventory deadline, and realized that a court-appointed auditor is now reviewing every financial decision they make. The guide walks through the exact format, the exact forms, and the exact fee schedule the Commissioner expects --- so the inventory and accounting pass on the first submission.

- The out-of-state adult child managing a Virginia estate remotely --- who was named executor but lives in a state where the probate court handles everything. In Virginia, the Commissioner of Accounts is a separate office with separate fees, and real estate does not flow through probate at all. The guide explains every Virginia-specific procedural difference in the order you encounter them.

- The surviving spouse trying to avoid unnecessary costs --- who needs to determine whether the estate qualifies for the Small Asset Affidavit, how joint accounts and beneficiary designations bypass probate entirely, and whether the probate tax applies to non-probate assets. The guide separates what requires formal administration from what does not.

- The heir about to sell inherited real estate --- who needs to understand the step-up in basis, the Real Estate Affidavit, and the "drops like a stone" doctrine before listing the property. The guide explains how to document the fair market value, establish chain of title, and avoid capital gains tax on appreciation that occurred during the decedent's lifetime.

- The executor confused by four overlapping tax deadlines --- who cannot tell the difference between Form 760, Form 770, Form 1041, and Form 706, and needs a clear map showing which forms apply, when each is due, how the numbers flow between returns, and what happens if the 90% payment threshold is missed. The guide sequences every filing by deadline.

- The family worried about Medicaid taking the house --- who received a recovery notice from DMAS and does not know about the surviving spouse exemption, the HB 855 reforms, or the permanent hardship waiver for low-income heirs. The guide details every defense available under current law.

Why Free Resources Get Virginia Wrong

Every form you need is available for free. The Virginia Department of Taxation provides Form 760 and Form 770. The Supreme Court of Virginia publishes every CC-series probate form. The IRS posts Form 1041 and Form 706 with instructions. Here is what happens when you try to navigate all of this yourself:

- The Department of Taxation provides Form 770 instructions. They do not explain how Form 770 interacts with the federal Form 1041. The Virginia fiduciary return uses the federal modified taxable income as its starting point. File one without understanding the other and you will either double-count income or miss deductions entirely.

- TurboTax handles the federal 1040 and 1041. It does not mention Virginia Form 760 or Form 770. National tax software operates in a federal-only silo. It will not tell you about Virginia's May 1 filing deadline, the 90% payment rule, or the electronic filing mandate for professional preparers.

- National estate guides explain probate. They do not explain the Commissioner of Accounts. Virginia's fiduciary oversight system --- with its four-month inventory, sixteen-month accounting, and escalating audit fees --- exists in no other state. Every national probate guide skips it entirely because it does not apply to the other 49 states.

- Nolo and FindLaw explain the step-up in basis. They do not explain the "drops like a stone" doctrine. In Virginia, real estate vests in the heirs immediately at death and never enters the executor's control. National guides assume the executor manages the sale. In Virginia, you may not have the legal authority to sell the property at all without a court order.

- Local attorneys provide accurate advice. They charge $250 to $400 per hour. For an estate that owes no estate tax, no inheritance tax, and needs the correct forms filed in the correct order, a $5,000 retainer is a disproportionate expense for what is fundamentally an organizational and sequencing problem.

- Competitors have not updated for HB 855 or the $15 million federal exemption. Pages still reference the old Medicaid recovery rules, outdated exemption thresholds, and pre-reform hardship waiver procedures. Following outdated instructions creates unnecessary complications with DMAS and the Department of Taxation.

Free resources give you one form at a time, with no sequencing, no cross-referencing, and no warning about how Virginia's Commissioner of Accounts system changes every assumption you brought from a national guide. The Commissioner Defense System maps every tax obligation to your estate's specific situation, organizes every form by deadline, structures your inventory and accounting to pass the Commissioner's audit, and tells you exactly which returns to file in which order --- so you pay what you owe, capture every deduction and exemption available, and do not discover a missed filing or a penalty notice six months after the deadline has passed.

--- Less Than One Hour of a CPA's Time

Virginia executors overpay on taxes and underprepare for the Commissioner's audit every year --- not because they are careless, but because no single resource connects Virginia's unique fiduciary oversight system to the federal and state tax code in plain English. An executor misses the 90% payment threshold on Form 770 because no one explained the extension trap. An heir sells inherited property without documenting the step-up in basis because no one mentioned the date-of-death appraisal requirement. A family pays a $5,000 attorney retainer for a $60,000 estate that could have been settled with a Small Asset Affidavit. This guide costs less than any of those mistakes and shows you how to avoid every one of them.

Your download includes the complete guide, the Virginia Tax After Death Checklist, and standalone reference sheets: the Commissioner Filing Timeline, Step-Up in Basis Documentation Worksheet, Form 770 Penalty Calculator, Small Estate Eligibility Flowchart, Medicaid Recovery Defense Reference, Federal Portability Election Planner, Critical Deadlines Calendar, and Forms and Fees Reference Card. Print the checklist first. Start at the top. Work down.

30-day money-back guarantee. If the guide does not give you a clear map of every tax obligation, every Commissioner filing requirement, every form you need, every deduction you can claim, and every deadline you need to meet --- email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Virginia Tax After Death Checklist --- a summary of the most critical tax actions, Commissioner deadlines, and filing sequences that most executors do not discover until a penalty notice arrives. Enough to start organizing the estate's obligations in the right order.

You did not plan for this. But you can plan how the taxes and the Commissioner's audit get handled. The guide gives you the forms, the deadlines, the filing sequence, and the Virginia-specific strategies --- so the next sixteen months are spent settling the estate efficiently, not discovering what you missed.