— Less Than Half an Hour of a CPA's Time

Washington CPAs charge $700 to $2,500 to prepare a single fiduciary tax return. Probate attorneys bill $350 to $500 per hour. Meanwhile, you are staring at four separate tax returns that may need to be filed — the final Form 1040, the estate's Form 1041, the federal Form 706, and the Washington Estate and Transfer Tax Return — each with its own deadline, its own rules, and its own penalties for getting it wrong. No government website, no CPA intake form, and no attorney's retainer agreement will tell you which return to file first, which deductions appear on which form, or how a mistake on one return creates a cascading problem on the others.

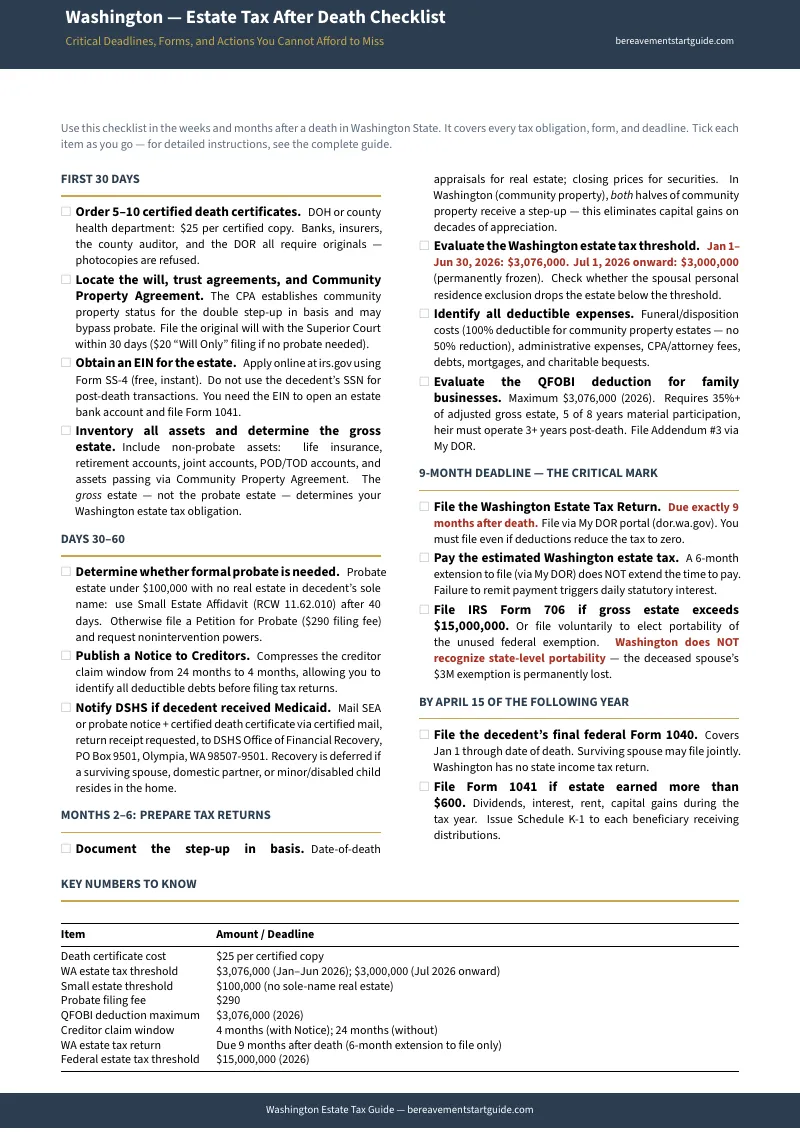

The Department of Revenue will tell you the estate tax threshold is $3,076,000 for deaths in the first half of 2026 and $3,000,000 for deaths after July 1. They will not tell you that community property math might keep your estate under that threshold entirely. They will not tell you that Washington rejects portability — meaning a married couple who fails to use both exemptions during the first spouse's death permanently forfeits roughly $390,000 in tax savings. And they will not tell you that funeral expenses on a community property estate are 100% deductible, not 50%, a distinction that out-of-state accountants routinely miss.

This guide exists because Washington's tax landscape is more volatile and more punishing than any other state's — and the people who need to navigate it are doing so for the first time, while grieving.

The Executor's Tax Sequence

The Washington Final Tax & Estate Tax Guide is built around what we call The Executor's Tax Sequence — a strict chronological workflow that tells you exactly which tax return to prepare first, which documents feed into the next return, and which deductions must be claimed on which form to avoid double-counting or forfeiture. Not a glossary of tax concepts. Not a form-by-form explainer that leaves you guessing at the order. A sequenced, deadline-driven system that mirrors the actual administrative timeline of a Washington estate, from the day of death through final distribution.

What's Inside

The Four Returns — In the Right Order

Washington estates can trigger up to four separate tax filings, and the sequencing matters. Income reported on the wrong return gets taxed twice. Deductions claimed on the wrong form get disallowed. The guide walks through each return in the order you should prepare them:

- The Final Form 1040 — the decedent's last personal income tax return. Washington has no state income tax, so this is federal only — but medical expenses paid in the final illness, state property taxes, and charitable contributions all have specific rules for the year of death. The guide covers the "deceased" checkbox, the surviving spouse joint-filing election, and the income cutoff date that trips up most filers.

- Form 1041 — Estate Fiduciary Income Tax — required when the estate earns more than $600 in gross income during administration. Dividends, rental income, and capital gains from selling inherited property all flow through this return. The guide explains how distributions to beneficiaries shift the tax burden via Schedule K-1, and why timing asset sales around the estate's fiscal year can save thousands.

- The Washington Estate and Transfer Tax Return — due exactly nine months after the date of death, with no automatic extension for payment. The guide covers the 2026 split-year exemption ($3,076,000 for January through June deaths, $3,000,000 for July onward), the graduated rate schedule that reaches 35% in the first half of the year and compresses to 20% after July, and every allowable deduction including the 100% community property funeral expense rule.

- Federal Form 706 — required only when the gross estate exceeds the federal exemption ($15,000,000 in 2026). Most Washington estates will not owe federal estate tax but may still need to file to elect portability of the unused exemption to the surviving spouse — except Washington rejects portability for state purposes, creating a planning trap the guide specifically addresses.

The Community Property Advantage Most Families Miss

Washington is one of nine community property states, and this classification creates two massive tax benefits that executors and surviving spouses routinely fail to claim because nobody explains them clearly:

- The double step-up in basis. When a spouse dies in a community property state, both halves of every community asset — the decedent's half and the surviving spouse's half — receive a step-up in cost basis to fair market value at the date of death. A home purchased for $200,000 that is now worth $1,000,000 gets a full $1,000,000 basis. If the surviving spouse sells it the next week, the capital gains tax is zero. Failing to document the date-of-death valuation — or failing to identify which assets qualify as community property — turns a tax-free transaction into a six-figure tax bill.

- The 100% funeral expense deduction. On the Washington Estate Tax Return, funeral expenses for community property estates are fully deductible. They are not subject to the 50% reduction that applies in separate-property states. Human composting, alkaline hydrolysis, traditional burial — all qualify. This deduction is frequently missed by CPAs who trained in common-law states.

The Portability Trap That Costs Washington Families $390,000

Federal estate tax law allows a surviving spouse to inherit the deceased spouse's unused federal exemption — a concept called "portability." Many estate plans rely on this mechanism. But Washington State explicitly rejects portability for state estate tax purposes. If the first spouse dies with a $6,000,000 estate and uses only $3,000,000 of exemption, the remaining $3,000,000 does not transfer to the survivor. When the second spouse dies, their estate gets one $3,000,000 exemption — not two. The result is roughly $390,000 in additional Washington estate tax that families assumed they had already planned around. The guide explains the A-B trust structure that captures both exemptions and the Community Property Agreement language that makes it work.

Real Estate, REET, and the Lack of Probate Affidavit

Selling inherited property in Washington involves two distinct tax questions that executors routinely confuse. First, capital gains tax — almost always eliminated by the step-up in basis, but only if you properly document the date-of-death fair market value with an appraisal. Second, the Real Estate Excise Tax (REET) — Washington's graduated tax on property transfers. Inheritance transfers are exempt from REET under WAC 458-61A-202, but claiming the exemption requires either Letters Testamentary from probate or a Lack of Probate Affidavit filed with the county. The guide walks through both scenarios: how to document the step-up, how to claim the REET exemption, and the exact affidavit process that title companies require before they will close.

The New Capital Gains and Income Taxes

Washington now imposes a 7% capital gains excise tax on long-term gains exceeding $262,000 (as of 2026), and a 9.9% tax on Washington taxable income above $1,000,000. Both apply to estates, trusts, and pass-through entities — not just individuals. If the estate sells a highly appreciated asset or distributes income from a non-grantor trust, these taxes can blindside executors who assume Washington has "no income tax." The guide covers the thresholds, the exemptions, and how to time distributions to minimize exposure.

Medicaid Estate Recovery and the Probate-Only Rule

Washington uses a "probate-only" recovery model for Medicaid. The state can only claim reimbursement from assets that pass through formal probate — not from joint accounts, life insurance, or Transfer on Death deeds. For families where the deceased received long-term Medicaid benefits, the guide explains which assets are exposed, which are protected, and how the $1,130,000 home equity exemption for Medicaid eligibility does not prevent recovery against the home after death unless specific protections apply.

Deadlines That Cannot Be Missed

Every deadline in one place, with the consequences for missing each one:

- 9 months after death — Washington Estate Tax Return and payment due. No automatic extension for payment. Interest accrues from day one of delinquency.

- April 15 of the following year — Final Form 1040 due.

- 15th day of the 4th month after fiscal year close — Form 1041 due (the estate can choose its own fiscal year, and the guide explains why this choice matters).

- 9 months after death — Form 706 due, if required, with a 6-month automatic extension available for filing (but not for payment).

- 40 days after death — earliest date to use the Small Estate Affidavit for assets under $100,000.

- 4 months after published Notice to Creditors — creditor claims bar date, which must be resolved before final tax returns can be filed accurately.

Who This Guide Is For

- The surviving spouse who just learned the family home is worth enough to trigger Washington estate tax — but who may be able to use community property math to stay under the threshold, and who needs to document the double step-up in basis before making any decisions about selling

- The adult child serving as executor from out of state who understands federal taxes but has never filed a Washington Estate Tax Return, does not know the 2026 split-year exemption rules, and cannot justify $2,500 for a CPA when the estate is straightforward

- The executor of a high-value estate who needs to understand the portability trap, calculate whether the estate crosses the $3,000,000 threshold after deductions, and determine whether an A-B trust restructure is still possible

- The family member selling inherited real estate who needs to claim the REET exemption, document the stepped-up basis, and understand whether the new capital gains excise tax applies to their specific transaction

- Anyone preparing to meet with a CPA or attorney who wants to walk in with organized records, identified deductions, and an understanding of which returns need to be filed — so they pay professional rates for professional analysis, not for sorting paperwork

Why Free Government Websites Will Not Get You Through This

The Department of Revenue publishes accurate estate tax thresholds, rate tables, and form instructions. The IRS publishes Form 1040, Form 1041, and Form 706 instructions. County assessors publish REET rates and exemptions. Here is what happens when you try to use these sources to actually administer an estate:

- The DOR explains the Washington estate tax in isolation. They will not tell you how the estate tax interacts with the federal Form 706, how to calculate community property deductions, or why filing in the wrong order creates deductions you cannot reclaim. Their forms assume you already know what you owe. If you knew that, you would not be reading their instructions.

- The IRS explains federal returns without state context. Form 1041 instructions do not mention that Washington's new capital gains excise tax may apply to the same income. Form 706 instructions do not warn you that electing portability federally does nothing for your Washington estate tax liability. You are reading two sets of instructions written by agencies that do not coordinate with each other.

- National publishers sell generic guides at $61 to $106 that treat Washington as an afterthought. Nolo's executor guides cover broad federal principles but miss the 2026 split-year exemption, the portability trap, the community property funeral deduction, and the REET exemption affidavit. You pay more and get less Washington-specific guidance than you need.

- WA-Probate.com has deep Washington knowledge buried in a 1990s user interface. The content is extensive but entirely unsequenced — an overwhelming wall of statutes and forms with no chronological workflow. Finding the right information at the right time, under deadline pressure, is functionally impossible.

Free resources give you raw data from agencies that do not talk to each other. The Executor's Tax Sequence integrates federal and state obligations into one chronological workflow — so you know what to file, when to file it, and which deduction goes on which return.

— What a CPA Charges for 20 Minutes of Consultation

Your download includes 10 PDFs — the complete guide plus 9 standalone printable tools you can use independently. Instant download, no account required.

- Washington Final Tax & Estate Tax Guide — the full Executor's Tax Sequence covering all four tax returns, the community property advantage, the portability trap, REET exemptions, the new capital gains and income taxes, Medicaid estate recovery, and every deadline with consequences for missing each one

- Washington Tax After Death Checklist — a printable checklist of every tax obligation, filing deadline, and document you need to collect, organized chronologically from the day of death through final distribution

- Community Property Classification Worksheet — classify each asset as community or separate property before filing any returns

- Gross Estate Valuation Worksheet — calculate whether the estate exceeds the Washington filing threshold

- Estate Tax Deadline Calendar — every deadline on one page with fill-in fields for actual dates

- Tax Returns Decision Guide — determine which of the four returns apply to your specific estate

- Rate Schedule Reference (Table W) — both 2026 rate schedules side by side with a worked example

- Forms and Filing Reference — every form, issuing agency, purpose, and where to get it

- Key Contacts Reference — phone numbers and websites for DOR, IRS, DSHS, DOH, and DOL

- CPA & Attorney Interview Checklist — when to hire, what to ask, and expected costs

Satisfaction guarantee: If the guide does not cover a Washington tax obligation relevant to your estate, email us and we will update it.

Not ready for the full guide? Download the free Washington Tax After Death Checklist — a printable summary of every tax return that may need to be filed, every deadline, and the documents required for each. Enough to see the full scope of what you are dealing with and start organizing immediately.

You should not have to become a tax specialist to settle an estate. But you do have to know the sequence — because the penalties for getting it wrong fall on you personally.