Your Spouse Died in Canberra. Centrelink Owes You a 14-Week Lump Sum You Have 26 Weeks to Claim. The Banks Will Release Up to $15,000 From the Frozen Account If You Ask Correctly. The Public Trustee Will Charge 1.1% of Everything If You Don't.

Someone has died and the financial machinery has already started moving against you. The joint bank account froze the moment the bank received notification. Centrelink is about to claw back the next pension payment — and if the deceased was registered for the Pension Bonus Scheme but never claimed, there is a tax-free 14-week lump sum sitting uncollected at Services Australia with a 26-week deadline that nobody tells you about. Meanwhile the funeral director wants a deposit by Friday, the superannuation fund says the death benefit could take months to process, and you are trying to work out whether you even need probate or whether the ACT's $50,000 threshold means you can skip it entirely.

You are not a financial planner. You are not an estate lawyer. You are a grieving family member in the Australian Capital Territory trying to hold your household together while navigating a system that splits critical information across Services Australia, the ACT Revenue Office, Access Canberra, the ACT Supreme Court, and WorkSafe ACT — none of which know what the others require, and none of which tell you what to do first.

That is the problem this guide solves. The Australian Capital Territory Survivor Benefits Navigator is a Benefits Sequencing System — a single chronological roadmap that tells you which payments to claim, which agencies to notify, which forms to lodge, and in what order, from the day of death through final estate distribution. Not a government brochure that covers one benefit and assumes you will find the other nine yourself. Not a funeral director's aftercare sheet. A structured benefits recovery plan built for the person who needs to keep the household solvent while the legal process runs.

What's Inside the Benefits Sequencing System

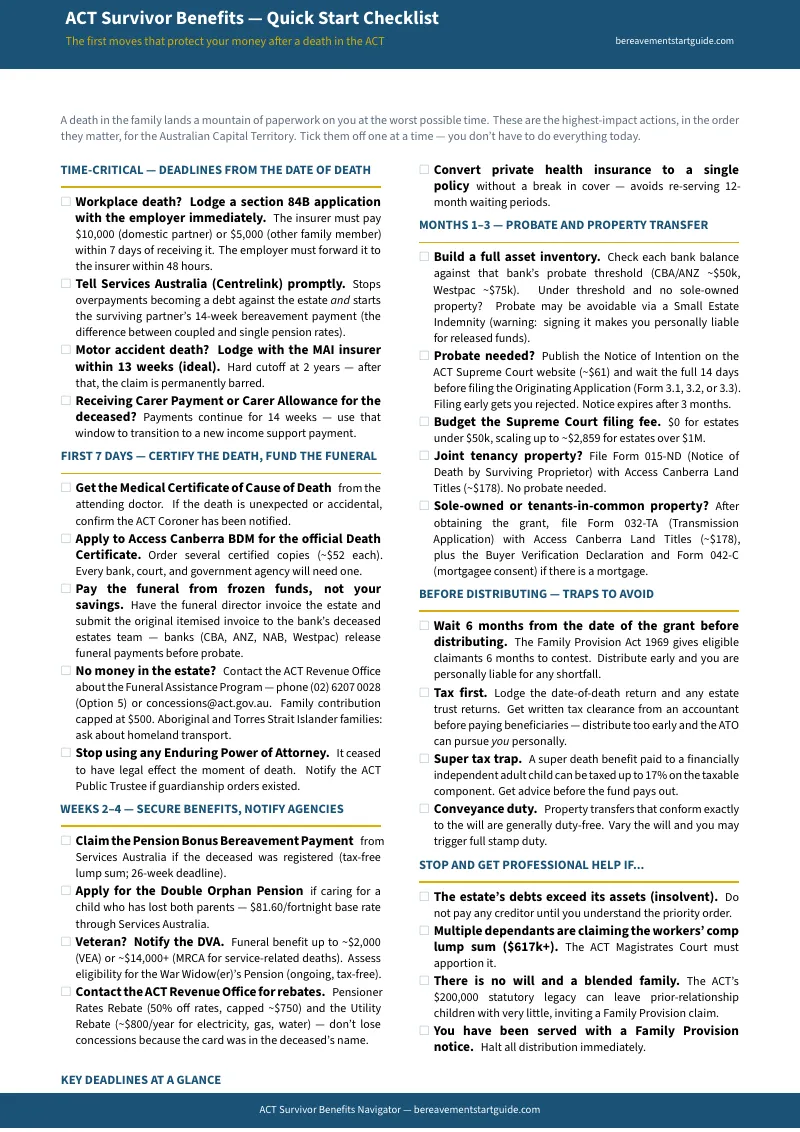

A 9-chapter guide plus the ACT Survivor Benefits Quick-Start Checklist — covering every financial entitlement, deadline, and administrative step from Day 1 through Month 24, built specifically for the ACT regulatory environment:

The First 7 Days: Cash Access, Funeral Funding, and Stopping the Bleeding

The funeral director needs a deposit and your bank accounts are frozen. Most families do not know that major Australian banks — NAB, CommBank, BankSA — will release up to $15,000 directly from the deceased's account to pay a funeral invoice, without waiting for probate. This chapter walks you through the exact mechanism: present the funeral invoice at the branch with the death certificate and your identification. It also covers the ACT Funeral Assistance Program for hardship cases (family contribution capped at $500), and the workers' compensation immediate death benefit if the death was workplace-related.

Weeks 2 to 4: Federal Income Support and Benefit Claims

Once the death certificate arrives from Access Canberra, everything unlocks. This chapter covers every Federal payment you may be entitled to: the Pension Bonus Bereavement Payment (a tax-free 14-week lump sum available only if the deceased was registered for the scheme but died before claiming — with a strict 26-week deadline), the Double Orphan Pension ($81.60 per fortnight for qualifying children), and JobSeeker bereavement extensions. It also maps the ACT Revenue Office concessions you need to claim immediately: the 50% pensioner rates rebate (capped at $750), the $800 electricity, gas, and water rebate for 2025-2026, and rates deferral for surviving spouses over 65.

Months 1 to 3: Probate, Property Transfers, and the PTG Trap

The ACT Supreme Court requires you to publish a Notice of Intention to apply for probate — not less than 14 days, not more than 3 months before filing your application. Miss this window and your timeline resets. File the probate application with a name spelled differently from the death certificate and the Registrar rejects it immediately with no refund on your filing fee (up to $2,859 for estates over $1 million). This chapter explains when to use Form 015-ND ($178) for joint tenancy property versus a Transmission Application for tenants in common, and exactly how to settle the estate yourself so you avoid the Public Trustee and Guardian's 1.1% capital commission — which amounts to $11,000 on a $1 million estate.

Specialist Claims: Workers' Comp, MAI, and Victims of Crime

If the death was caused by a motor vehicle accident, a workplace incident, or a criminal act, you may be entitled to additional compensation that operates entirely outside the normal estate process. The Workplace Legislation Amendment Act 2025 streamlined death benefit payouts under the Workers Compensation Act 1951 — the current statutory lump sum is $617,131, plus weekly payments for dependent children. The MAI (Motor Accident Injuries) scheme runs through the ACT Civil and Administrative Tribunal. The Victims of Crime Financial Assistance Scheme provides up to $19,627 for funeral-related expenses. This chapter maps which scheme applies when, because the answer is not always obvious and claiming from the wrong scheme first can complicate later applications.

The Superannuation Tax Trap

Most Australians assume superannuation death benefits are tax-free. They are — but only if paid to a "death benefit dependant" as defined by the Tax Act, which does not match the superannuation law definition. An adult child who is financially independent is a dependant under super law (and can receive the payout) but is not a tax dependant — meaning they may face a 15-17% tax bill on the taxable component that nobody warned them about. This chapter explains the distinction, the binding death benefit nomination that prevents the fund trustee from making the decision for you, and the strategies for minimising the tax hit before the payout is processed.

The ACT Crown Leasehold System

Property in the ACT is not freehold — it is Crown leasehold. This means property transfers after death work differently from every other Australian jurisdiction. Conveyance duty is not payable if the transfer conforms exactly to the Will, but if someone buys out a share not specified in the Will, duty applies to that portion. The guide explains how the Crown lease affects your specific situation, including the duty exemption rules that the ACT Revenue Office does not publicise in plain English.

Who This Guide Is For

- The surviving spouse whose partner died in the ACT and who needs to know which benefits are available, which deadlines are running, and how to keep the household financially stable during the most difficult months — without surrendering control to the Public Trustee

- The adult child named as executor who is navigating the ACT Supreme Court probate process for the first time and cannot afford a clerical error that freezes the estate for months

- The financially distressed dependent who cannot pay for the funeral and needs to access the ACT Funeral Assistance Program, bank release mechanisms, and emergency Federal payments before the next bill arrives

- The interstate family member handling an ACT estate from NSW or elsewhere — who needs to know which steps require physical presence, which can be handled by post, and how the ACT's Crown leasehold system differs from the freehold property they know

- The guardian taking custody of children who needs to claim the Double Orphan Pension, secure Centrelink extensions, and understand how superannuation nominations affect who receives the death benefit

Why Free Resources Leave You Exposed

The information exists. It is scattered across at least eight government agencies and financial institutions, each covering their own piece and none connecting the dots:

- Services Australia explains Centrelink payments but not ACT concessions. They cover the Pension Bonus Bereavement Payment and the Double Orphan Pension. They say nothing about the ACT Revenue Office rates rebate, the utility concessions, or the property transfer duty exemptions you are simultaneously entitled to.

- The ACT Revenue Office explains concessions but not the order. They publish the pensioner rates rebate and the utility rebate. They do not explain that you need the death certificate first, that Access Canberra takes weeks to issue it, or that you should be claiming Federal payments in parallel.

- Banks explain their release policy but not the alternatives. NAB and CommBank each publish their bereavement procedures. Neither mentions the ACT Funeral Assistance Program, the workers' compensation death benefit, or the superannuation payout timeline that determines whether you need the bank release mechanism at all.

- The ACT Supreme Court explains probate rules but assumes legal literacy. Their "Common Errors to Avoid" page lists the exact things that cause rejection — but it is written for solicitors, not for a grieving spouse trying to file without one. A name variance between the Will and the death certificate requires a sworn affidavit. Missing annexure clauses cause outright rejection. The guide translates these rules into a pre-submission checklist.

- Superannuation funds explain the payout but not the tax. They process the claim. They do not warn you that paying a death benefit to a non-tax-dependant adult child can trigger a 15-17% tax bill that a binding nomination and pre-distribution planning could have avoided.

Free resources give you fragments from agencies that do not communicate with each other. The Benefits Sequencing System puts every benefit, deadline, form, and fee into chronological order — so you know what to claim first, what triggers what, and what traps to avoid before you walk into them.

— Less Than One Hour With an Estate Solicitor

A single consultation with an estate solicitor in Canberra costs $350 to $500 per hour. The ACT Public Trustee and Guardian charges a 1.1% capital commission on the estate they administer — $11,000 on a $1 million estate. This guide costs a fraction of either, and it equips you to handle the process yourself or to walk into a solicitor's office knowing exactly which questions to ask, rather than paying them $400 to explain the basics.

Your download includes the complete 9-chapter guide, the quick-start checklist, and 8 standalone printable tools:

- ACT Survivor Benefits Quick-Start Checklist — time-critical deadlines, first-7-day actions, weeks 2-4 benefit claims, months 1-3 property and probate steps, distribution traps, and escalation triggers on a printable action list you can work through sequentially

- Bank Threshold & Indemnity Worksheet — list every account against each bank's probate threshold to determine whether you can skip probate entirely

- Benefit Sequencing Plan — every ACT and Federal benefit mapped side by side with a decision-tree eligibility map so you claim from all sources

- Superannuation Tax Trap Guide — the dependant-vs-tax-dependant distinction that determines whether your family pays 0% or 17% on the death benefit

- Property Transfer Concessions — Crown lease transfer forms, conveyance duty exemptions, and the Form 015-ND trap explained on one printable sheet

- Probate Fees & Forms Reference — every ACT Supreme Court filing fee, form number, and common rejection reason in one place

- Executor Compliance Timeline — every deadline that can cost you money or personal liability, from 7 days through end of financial year

- Intestacy Calculator — the ACT statutory distribution formula with a fillable worksheet and the blended-family trap worked example

- Escalation Triggers Reference — the 13 situations where you must stop and call a professional, with who to call for each

Plus a 30-day money-back guarantee. If the guide does not give you clarity on your entitlements and confidence that you are not leaving money unclaimed, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Australian Capital Territory — Survivor Benefits Checklist — the most urgent deadlines, first-week actions, and key benefit claims on a printable action list. It is enough to stop the immediate financial bleeding and ensure you do not miss the critical early deadlines.

You should not have to become a benefits expert to survive the financial aftermath of losing someone you love. But the system does not connect the dots for you — and every missed deadline is money your family will never recover. This guide makes sure you miss nothing.