Someone You Love Just Died in New South Wales. The Bank Froze Their Accounts. The Supreme Court Requires an Online Probate Application You Have Never Seen Before. And Nobody Told You About the Mandatory 14-Day Waiting Period That Delays Everything If You Miss It.

You are standing in a place nobody prepared you for. Maybe you were named executor in a will you barely remember reading, and now the funeral director is waiting for a decision about cremation paperwork while you try to figure out how many certified death certificates to order from the NSW Registry of Births, Deaths and Marriages. Maybe there was no will at all, and because you are the eldest child or the surviving spouse, everyone is looking at you for answers about a legal process governed by the Succession Act 2006 that you have never heard of. Maybe the Commonwealth Bank just told you the accounts are frozen and you cannot access a single dollar to pay the electricity bill, the water rates, or the funeral deposit that ranges from $8,000 to $12,000 depending on which funeral director you called.

You are grieving and sleep-deprived, but the paperwork does not wait. The funeral director needs you to understand the difference between the Medical Certificate of Cause of Death and the official death certificate. Services Australia needs notification within days or the estate will owe back overpayments on the pension. Siblings are already asking about the house. The ATO will eventually demand two separate tax returns: one for income earned up to the date of death and another for the estate trust. And somewhere in the back of your mind, a terrifying question keeps circling: if I miss a deadline I do not even know about, or distribute assets before the Family Provision claim window closes, or accidentally void the Section 63 stamp duty concession by letting beneficiaries swap assets informally — am I personally liable?

The short answer: the estate pays its debts, not you. But the long answer — the one that involves a Supreme Court that mandated online probate filing in August 2023 but still requires you to physically mail the original will to the registry, bank account thresholds that vary wildly between institutions (CBA at $100,000, ANZ at $50,000 to $100,000 depending on risk assessment, credit unions as low as $15,000), a CPI-indexed statutory legacy for intestate estates that now exceeds $611,000 but requires working with ABS data that was re-referenced in 2025, and regulated solicitor fees under Schedule 3 that only cover obtaining the grant while the actual estate administration is billed at unregulated hourly rates — that answer is what separates families who settle an estate in months from families who spend years and thousands of dollars untangling mistakes they did not know they were making.

The When Someone Dies in New South Wales — Estate Settlement Guide is a Settlement Blueprint for every legal, financial, and administrative step between the funeral home and final distribution. Not a law textbook. Not a generic Australian checklist that does not know NSW from Victoria. A structured, NSW-specific manual that separates what must be done in the first 48 hours from what legally cannot happen until the Family Provision claim window closes at 12 months — so you stop guessing, stop panicking, and start working through this in the right order.

What's Inside the Settlement Blueprint

A 14-chapter guide and the First 48 Hours Checklist — covering every stage from the moment of death through final asset distribution, built specifically for NSW statutes, the Supreme Court of NSW, and the state-specific rules that make settling an estate here different from anywhere else in Australia:

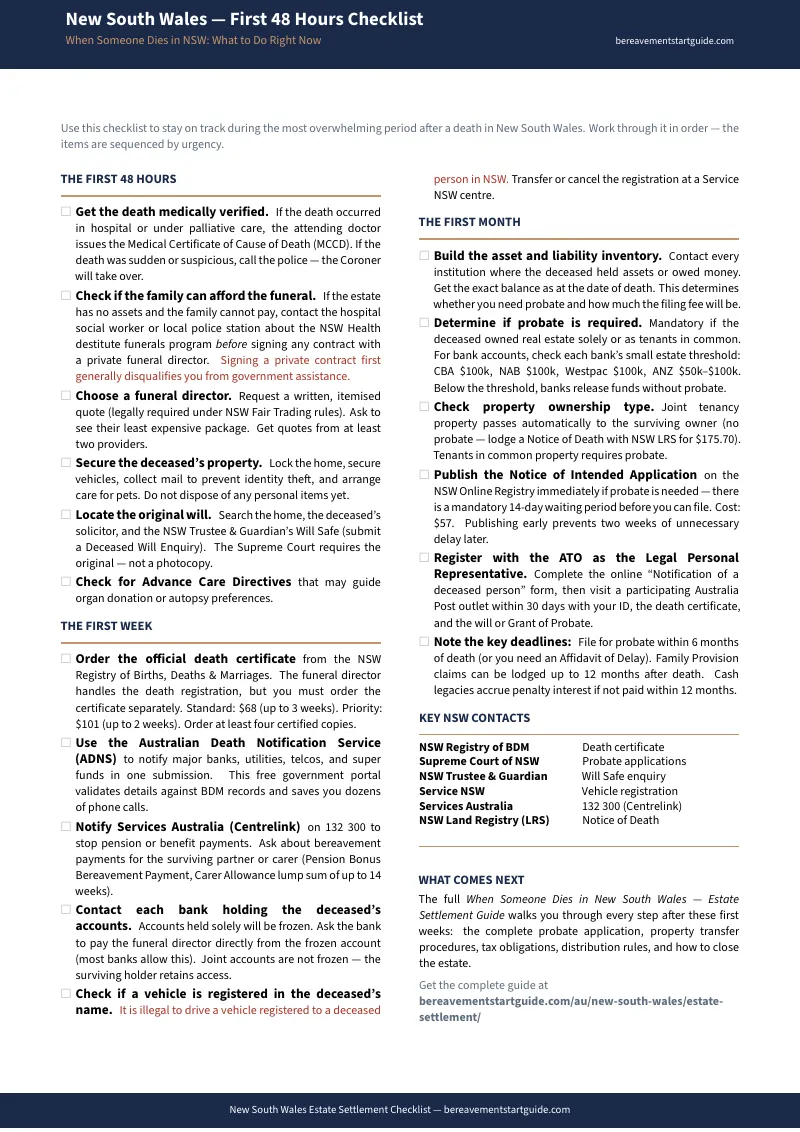

The First 48 Hours: Immediate Actions and Consumer Rights

The moment someone dies in New South Wales, every Enduring Power of Attorney and Enduring Guardian appointment is legally void. If you managed their finances under an EPA, you no longer have authority. This chapter covers getting the death medically verified, choosing a funeral director (and knowing your rights under the NSW Fair Trading Funeral Information Standard — they must show their cheapest package, provide an itemised quote before you sign anything, and disclose all commissions), securing the home and property, and the critical rule most people learn too late: if the family cannot afford a funeral, contact NSW Health about the destitute funerals program before signing any private contract, because signing first generally disqualifies you from government assistance.

Administrative Foundations: Death Certificates, Notifications, and the Asset Inventory

Death certificates cost $68 standard or $101 priority from the NSW BDM — and you need at least four certified originals because banks, the ATO, and the Supreme Court all demand them and will not accept photocopies. The guide gives you the calculation so you order the right number now instead of waiting three more weeks for extras later. It covers the Australian Death Notification Service (ADNS) — the free government portal that notifies major banks, utilities, and super funds in one submission — plus the tiered notification system (Services Australia, Medicare, Transport for NSW, utilities, digital accounts) and building the complete asset and liability inventory that determines whether probate is required.

The Probate Decision: When You Need It and When You Can Skip It

This is the most critical decision point in the entire process. Probate is mandatory if the deceased owned real estate solely or as tenants in common. For bank accounts, it depends on each institution's internal small estate threshold — and those thresholds are corporate policy, not law, meaning they can change without notice. The guide includes the current threshold for every major bank, explains the right of survivorship for joint accounts, covers Binding Death Benefit Nominations for superannuation (which bypass the estate entirely if valid), and maps the exact scenarios where you can settle without going to court.

Applying for Probate Through the NSW Online Registry

This is the chapter that does not exist in any free resource. Since August 2023, the Supreme Court of NSW mandated that most uncontested probate applications must be filed through the NSW Online Registry — a portal designed for legal professionals that forces grieving families to create digital accounts, navigate complex online forms, and generate UCPR Form 111 (Probate Summons), Form 118 (Affidavit of Executor), and Form 117 (Inventory of Property). The critical step most executors miss: you must publish a Notice of Intended Application on the registry and then wait a mandatory 14 clear days before filing. If you do not know about this requirement until you are ready to file, you have just added two weeks of unnecessary delay. The guide tells you to publish the notice the same week you receive the death certificate. It also covers the counterintuitive requirement that despite digital filing, you must still physically mail the original will to the Supreme Court registry — and the tiered filing fees from $921 to $7,099 depending on estate value.

Transferring Property in New South Wales

Real estate is typically the largest asset in a NSW estate, and the transfer rules are entirely different depending on how the property was owned. Joint tenancy: the surviving owner lodges a Notice of Death with NSW Land Registry Services for $175.70 — no probate needed. Sole ownership or tenants in common: the executor must obtain probate first, then lodge a Transmission Application through the PEXA electronic conveyancing platform. The guide covers both paths and explains the Section 63 stamp duty concession that saves families tens of thousands of dollars — and the trap that voids it. If beneficiaries informally agree to swap assets (one sibling takes the house, the other takes more cash), the transfer is no longer "in conformity with the will" and full ad valorem stamp duty applies. On a $1 million property, the difference between $100 nominal duty and full stamp duty is catastrophic.

Taxation: The ATO and Your Obligations as Executor

Tax is where many executors unknowingly expose themselves to personal liability. The ATO requires you to register as the Authorised Legal Personal Representative through a specific process involving the online notification form and a subsequent identity verification at a participating Australia Post outlet. Until you complete this, the ATO will not share any information about the deceased's tax history. The guide covers the two tax returns you may need to lodge (the "date of death" individual return and the estate trust return under a separate TFN), and the safe harbour under Practical Compliance Guideline 2018/4 that protects executors from personal liability — provided the estate meets specific conditions and you wait at least six months after lodging all outstanding returns before distributing.

Intestacy, Distribution, and the Public Trustee

The remaining chapters cover intestacy (including the CPI-indexed statutory legacy that now exceeds $611,000 for surviving spouses in blended families and the Indigenous kinship provisions under Part 4.4 of the Succession Act), the precise order of estate distribution (the Notice of Intended Distribution, the 30-day creditor notice period, the 12-month Family Provision claim window, and the penalty interest that accrues on unpaid legacies), avoiding the NSW Trustee and Guardian (whose capital commission alone reaches approximately $14,300 on a $500,000 estate), edge cases (insolvent estates, missing wills, superannuation death benefits, cross-border estates), pre-death planning (Advance Care Directives, Enduring Guardian, Enduring Power of Attorney), a consolidated deadline reference, and worksheets for tracking notifications, assets, the probate timeline, and beneficiary communications.

Who This Guide Is For

- The surviving spouse whose partner just died and whose bank accounts were frozen this morning — who needs to know which accounts stay accessible under right of survivorship, how to get the bank to pay the funeral director directly from the frozen account, and how to lodge a Notice of Death to transfer the family home without going through probate

- The adult child named as executor who has never navigated the Supreme Court of NSW and is terrified of making a mistake that triggers personal liability — who needs the complete NSW Online Registry walkthrough, every UCPR form explained, and a timeline that separates what is urgent from what must wait for the 14-day notice period

- The family with no will who just learned that the Succession Act 2006 dictates everything — who needs to understand who has priority to apply for Letters of Administration, how the CPI-indexed statutory legacy is calculated, and whether the NSW Trustee and Guardian will become involved

- The executor living interstate or overseas who cannot walk into a Service NSW centre or the Supreme Court registry — who needs to understand the digital filing process, electronic conveyancing through PEXA, and how to manage the ATO's identity verification requirements from afar

- The financially constrained family who cannot afford a funeral or a solicitor — who needs to know about the NSW Health destitute funerals program, the probate fee waiver for Healthcare Card holders, and the filing fee exemption for estates under $100,000

- The proactive planner organising affairs after a terminal diagnosis or aged care transition — who needs to assemble an Advance Care Directive, Enduring Guardian, and Enduring Power of Attorney before capacity is lost, and create a "death folder" so their family never has to scramble through this process blind

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across Service NSW, Legal Aid NSW, the Supreme Court of NSW, NSW Land Registry Services, Revenue NSW, the ATO, Services Australia, and a dozen institutional portals that do not talk to each other. Here is what you actually encounter when you try to settle an estate using free sources alone:

- Government pages tell you what to do but not how to do it. Service NSW and Legal Aid NSW publish checklists that establish broad obligations. They tell you that you need to register the death, apply for probate, and notify the ATO. They do not walk you through the NSW Online Registry step by step, explain how to generate UCPR Form 111, or warn you about the 14-day notice period that delays everything if you miss it. They assume baseline legal and financial literacy that most grieving families do not have.

- Law firm blogs highlight complexity to justify retainer fees. Fixed-fee disruptors like Bare Law advertise flat $1,999 probate applications. Traditional firms publish excellent technical breakdowns of Schedule 3 regulated fees and executor duties. All of their content is designed to convince you the process is too dangerous to handle alone — and that you need a retainer starting at $5,000. For contested estates, that is true. For the majority of straightforward estates, the answer costs a fraction of a solicitor's hourly rate.

- Bank estate pages protect the bank, not you. CBA, NAB, ANZ, and Westpac each publish deceased estate processes. Every one is focused on institutional liability protection. They explain why accounts are frozen. They do not explain how to negotiate early fund releases for funeral expenses, how the small estate indemnity process works, or why their thresholds differ from the bank across the street.

- Funeral home content stops after the ceremony. Funeral directors provide empathetic aftercare checklists covering the first 48 hours. They help you choose between burial and cremation, and remind you to order death certificates. Their advice ends where the hard questions begin: probate applications, property transfers, ATO obligations, and executor liability.

- The NSW Trustee and Guardian is universally feared. They publish transparent fee tables, but their capital commission structure means a $500,000 estate costs approximately $14,300 in administration fees alone — before income commission and annual account-keeping charges. Investigative journalism by the ABC has documented allegations of fee gouging and asset depletion. Families desperately want to keep estate administration private, but free resources do not show them how.

Free resources give you fragments from a dozen sources that do not reference each other. The Settlement Blueprint puts every NSW-specific statute, form, deadline, and procedure into one document, in the order you actually need them.

— Less Than Fifteen Minutes With a NSW Estate Solicitor

A single consultation with a NSW estate solicitor costs $350 to $500 per hour. Standard probate representation starts at $5,000 — and that only covers obtaining the grant. The actual estate administration (closing accounts, selling shares, organising tax returns) is billed separately at unregulated hourly rates. This guide costs less than fifteen minutes of professional legal time and gives you the complete NSW-specific roadmap — every statute, every UCPR form, every deadline, and the Online Registry process that the Supreme Court requires but nobody explains in plain language.

Your download includes the complete 14-chapter guide, the standalone First 48 Hours Checklist, and four print-ready worksheets — Agency Notification Tracker, Asset and Liability Summary, Probate Timeline Planner, and Beneficiary Communication Log. Six PDFs total. Plus a 30-day money-back guarantee. If the guide does not give you clarity on what to do next and confidence that you are doing it in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New South Wales — First 48 Hours Checklist — the most urgent actions covering everything that must happen in the first two days after a death in NSW: death certificates, securing property, funeral director rights, destitute funeral eligibility, bank notifications, and what not to pay. It is enough to get through tonight and tomorrow.

You did not ask for this job. But you can do it. The guide shows you how, one step at a time.