Your Partner's Income Stopped the Day They Died — but the Bills Did Not. Centrelink Will Pay a Surviving Spouse a Bereavement Lump Sum Worth Thousands, Except the Window Closes Quietly. The Tax Office Can Take 17% of the Superannuation if It Lands in the Wrong Hands. And One Missed 30 June Deadline Triggers a Backdated Land Tax Bill on the Home You Just Inherited.

Nobody hands you a manual for this. One week you are sitting beside a hospital bed; the next you are on hold to Services Australia, then Titles Queensland, then the deceased's super fund, then the bank — and not one of them tells you what the other three need, or which deadline is already running against you. The household income has halved overnight, but the mortgage, the rates, and the funeral invoice have not moved. And somewhere underneath the grief is a quieter fear: that you are leaving money on the table — entitlements you are owed but cannot find — while accidentally triggering a tax bill or a penalty you never saw coming.

Here is what the grief brochures will not tell you. The bereavement payments, the superannuation, the property transfers, and the workplace-death compensation in Queensland are governed by different agencies, under different laws, on different clocks — and almost every one of them rewards the family that acts fast and punishes the family that does not. Centrelink pays a surviving partner a lump sum bereavement payment, and the Pension Bonus Bereavement Payment can be worth up to $55,411.60 — but only if you claim within 14 weeks. The Australian Taxation Office treats a super death benefit paid to a spouse as tax-free, yet taxes the same benefit at 15% to 17% when it flows to a non-dependent adult child. WorkCover Queensland pays a dependent family a lump sum that now exceeds $896,000 after a workplace death — but the claim is barred after six months. And if you fail to lodge a simple Form 4 with Titles Queensland before the next 30 June, the Queensland Revenue Office can issue a retrospective land tax assessment on a home you already own outright.

None of this is written down in one place. The information is real, it is public, and it is scattered across eight government departments that do not talk to each other — which is exactly why grieving families miss entitlements worth more than a year's pension while paying the Queensland Public Trustee administration fees that start at $3,822.

The Queensland Survivor Benefits Navigator is a Financial Protection Roadmap — a single chronological, cross-departmental map that walks a surviving spouse, executor, or dependent through every benefit you can claim and every trap you must avoid, in the order the deadlines actually fall. Not a welfare pamphlet. Not a generic Australian explainer that treats Queensland the same as New South Wales. A jurisdiction-specific operating manual built around the exact federal payments, state forms, tax rules, and statutory deadlines that decide whether your family keeps what it is owed.

What's Inside the Financial Protection Roadmap

A 13-chapter guide with a 20-item Quick-Start Checklist — covering the first 48 hours through final distribution, built specifically for Queensland's agencies, the Succession Act 1981, the Duties Act 2001, and the federal benefit system that surviving families depend on:

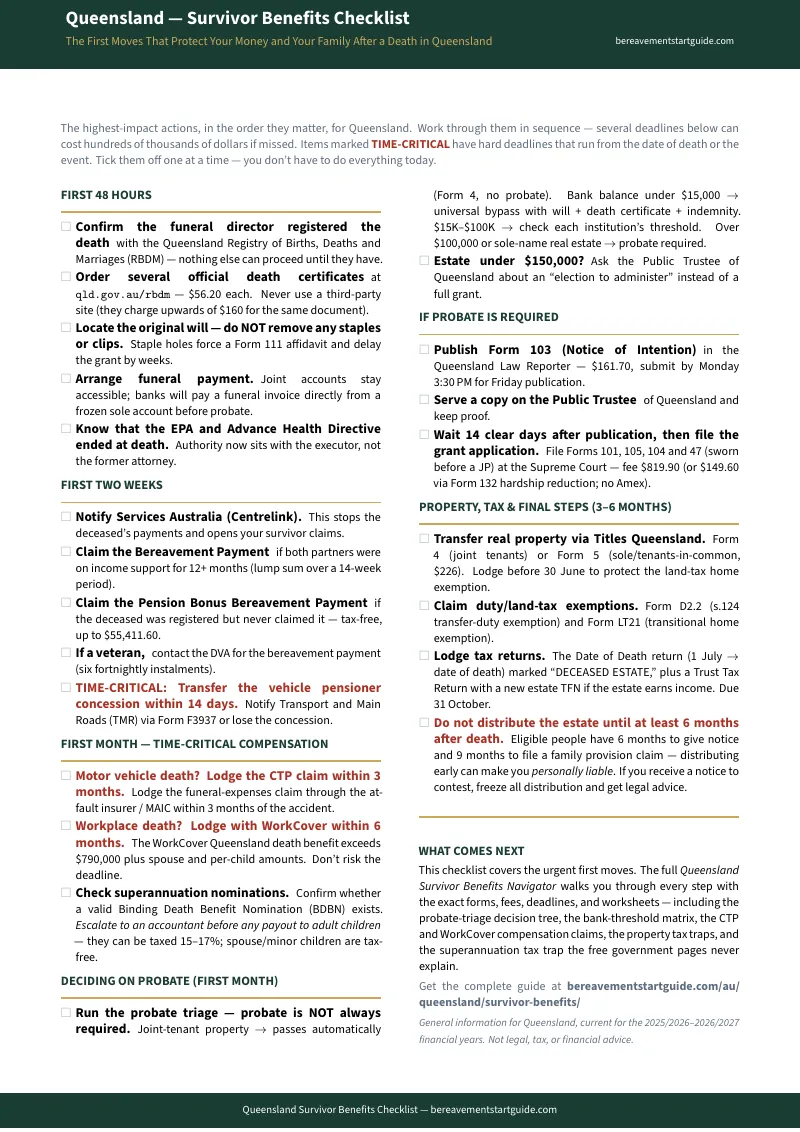

The First 48 Hours — and the $160 Death Certificate Scam

The death certificate is the master key: Centrelink, the super fund, the ATO, Titles Queensland, and the bank all demand a certified original before they will move. Queensland's Registry of Births, Deaths and Marriages charges $56.20 and takes up to 10 business days. Yet panicked families searching online routinely land on unauthorised lead-generation sites that charge upward of $160 for the identical document while harvesting the deceased's identity details. The guide tells you exactly where to order, how many certified copies to request up front, why an Enduring Power of Attorney ends the instant a person dies, and how to protect the original will from the damage that derails everything downstream.

Funeral Funding When the Accounts Are Frozen

The bank freezes the accounts the day it learns of the death — but it will usually release funds directly to a funeral director against the invoice, and most families never ask. This chapter maps every immediate cash source: direct bank release, the Centrelink bereavement lump sum, the Burials Assistance Act 1965 pathway for families who genuinely cannot pay, and Victim Assist Queensland's funeral grant of up to $6,000 where the death was a homicide or violent crime.

Centrelink Survivor Benefits — The 14-Week Window

This is the chapter that pays for the guide many times over. The standard bereavement payment, the Pension Bonus Bereavement Payment worth up to $55,411.60, the carer payment bereavement transition, and the move from a couples pension rate to the single rate are all governed by hard deadlines and reassessment rules that quietly reduce what you receive if you act late. The guide walks the Services Australia process step by step, in plain English, so a distressed spouse does not forfeit thousands by missing a form.

The Superannuation Tax Trap — Where Families Lose the Most

Superannuation is often the largest single asset, and it is the one most often handled wrong. A valid Binding Death Benefit Nomination controls where it goes; the difference between a "tax dependant" and a "non-tax dependant" controls how much the ATO takes. Paid to a spouse, a super death benefit is tax-free. Paid to a financially independent adult child, the taxable component is taxed at 15% to 17%. The guide explains the proportioning rules, the tax-free versus taxable components, and the decisions that can legally protect tens of thousands of dollars from erosion.

WorkCover, CTP, and Victim Assist — Compensation With Six-Month Clocks

When the death was a workplace incident, a road crash, or a violent crime, an entirely separate stream of statutory compensation opens — and it is bound by strict limitation periods. WorkCover Queensland lump sums for a dependent family now exceed $896,000, plus weekly payments for dependent children, under the Workers' Compensation and Rehabilitation Act 2003 — but the claim is barred after six months. CTP insurers cover funeral and dependency costs after a fatal road accident. Victim Assist Queensland funds funerals for homicide victims. The guide keeps these specialised frameworks clearly separate from ordinary estate administration so a traumatised family does not forfeit life-changing support through sheer administrative ignorance.

Property, Vehicles, Tax, and Safe Distribution

The remaining chapters carry you through every asset transfer and obligation: Titles Queensland property transfers (Form 4 Record of Death for joint tenancy survivorship versus Form 5 Transmission Application for sole ownership, the s.124 Duties Act duty exemption, and the 30 June land tax deadline); vehicle transfers through Transport and Main Roads (Form F5296 within the 14-day window, plus the pensioner concession transfer); banks, insurance, and share registries; the date-of-death tax return and the estate trust return; and safe distribution — the six-month family provision notice and nine-month filing window under the Succession Act 1981 that can leave an executor personally liable if assets are paid out too early. A final chapter covers the edge cases: insolvent estates, intestacy with no will, Indigenous and Torres Strait Islander estates, and interstate or overseas assets.

Who This Guide Is For

- The financially vulnerable surviving spouse whose household income halved the day their partner died — who needs the Centrelink bereavement payments secured inside the 14-week window, plain-English reassurance that joint tenancy survivorship protects the family home, and a calm path through the agencies that does not depend on already knowing the system

- The nominated executor or adult child acting as personal representative — who is treating this as a project, fears personal liability for getting it wrong, and needs the Titles Queensland forms, the super tax rules, and the six-month distribution window mapped precisely so the estate is protected and nothing is forfeited

- The pre-emptive caregiver anticipating a parent's death — who wants the operating checklist ready in advance, the Binding Death Benefit Nomination validated now, and the super tax position arranged before the crisis rather than during it

- The low-income or regional family facing a funeral deposit they cannot cover with the accounts frozen — who needs every immediate cash pathway in one place, from bank release to state burial assistance, and a warning about the $160 death-certificate trap before they fall into it

- The sudden-trauma survivor after a workplace, road, or violent death — who needs the WorkCover, CTP, and Victim Assist claims explained as their own urgent track, with the six-month deadlines flagged before they quietly expire

Why Free Resources Won't Get You Through

The information exists. It is spread across Services Australia, the ATO, Titles Queensland, the Queensland Revenue Office, Transport and Main Roads, WorkCover, and the funnels of a dozen law firms. Here is what you actually meet when you try to assemble it yourself:

- The federal agencies ignore the state, and the state ignores the federal. Services Australia is authoritative on bereavement payments and pension transitions — and silent on Queensland property law, super tax, and vehicle transfers. Titles Queensland assumes you are a licensed conveyancer. Nobody publishes the single chronological timeline that merges federal welfare with state asset transfer, which is exactly the document a grieving family needs and cannot find.

- The Queensland Public Trustee markets simplicity and charges dearly. The QPT advertises "free wills" that quietly name the QPT as executor, locking estates into administration fees that start at $3,239.60 for a grant of probate and $3,822.07 for a grant of administration — plus percentage cuts of asset management. It has faced a Four Corners investigation and a Public Advocate report over excessive fees levied on vulnerable, asset-rich pensioners. Knowing how to administer an estate independently, and how to extract one from the QPT's grip, is a primary reason families buy real guidance.

- Law firms publish the problem and withhold the solution. Estate law firms post excellent breakdowns of executor liability and property pitfalls — every one engineered to convince you the process is too dangerous to handle alone and to funnel you toward a retainer starting north of $3,000. For genuinely contested estates that is fair. For a straightforward estate with a clear will, you are paying thousands for templates and steps this guide simply gives you.

- The deadlines are invisible until you have already missed them. The 14-week Centrelink window, the 14-day TMR vehicle transfer, the six-month WorkCover and family-provision clocks, and the 30 June land tax cut-off are buried in separate portals in legislative language. No free page assembles them into a single date-triggered calendar — so families discover them only when the entitlement is gone or the penalty has landed.

Free resources give you federal payments from one website, property forms from another, super tax rules from a third, and compensation deadlines from a fourth — with no connecting thread. The Financial Protection Roadmap puts every Queensland-specific benefit, form, tax rule, and deadline into one document, in the order the clocks actually run.

— Less Than a Tenth of One Centrelink Bereavement Payment

A single hour with a Queensland estate solicitor costs $300 to $600. The Queensland Public Trustee charges from $3,239.60 to administer a simple estate. A single missed Centrelink window, or 17% tax on a super death benefit that should have gone tax-free, can cost a family tens of thousands. This guide costs less than a tenth of one bereavement payment — and shows you how to claim every entitlement you are owed and sidestep every trap that quietly drains an estate.

Your download includes the complete 13-chapter guide, the Queensland Survivor Benefits Quick-Start Checklist (20 actionable items from the first 48 hours through final distribution), and 4 standalone print-ready reference cards: the Super Death Benefit Tax Decision Matrix (work out the tax before the fund pays out), the Survivor Benefits Deadline Calendar (every date-triggered deadline on one page), the Property & Vehicle Transfer Reference (Form 4 vs Form 5, the s.124 exemption, the TMR 14-day window), and the Fee, Payment & Contacts Quick Reference (benefit amounts and every agency number — pin it to the fridge). Plus a 30-day money-back guarantee. If the guide does not give you clarity on what to claim, when to claim it, and how to protect what your family is owed, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Queensland — Survivor Benefits Checklist — 20 items in the sequence the deadlines demand, from ordering death certificates through final distribution. It tells you what to do and when. The full guide tells you how.

You did not choose to be the one who sorts this out. But you can do it — and you can do it without leaving money your family is owed on the table. The guide shows you exactly how.