Someone You Depended On Just Died in the Northwest Territories. Federal Benefits, Territorial Programs, Indigenous Grants, and Workplace Compensation All Exist, but Nobody Will Tell You Which Ones Apply to You or in What Order to Claim Them.

You are sitting in a house that just lost its primary income. The heating bill is due. The bank account with the paycheques is frozen. And you have just discovered that the Northwest Territories operates a benefit system unlike anywhere else in Canada, where funeral funding requires pre-approval before you sign any contract, death certificates come exclusively from an office in Inuvik, and sworn documents cannot be witnessed over video because the territory does not recognize remote commissioning.

Here is what is actually happening. Service Canada controls the CPP survivor's pension and the $2,500 death benefit, but their website says nothing about the territorial programs that offset against federal payments. The Department of Health and Social Services runs a Funeral, Burial and Cremation Program, but it operates as the "payer of last resort," meaning if you apply in the wrong sequence, your family pays for the funeral out of pocket permanently. The Workers' Safety and Compensation Commission calculates survivor pensions against something called the Year's Maximum Insurable Remuneration, which is set at $116,000 for the NWT in 2026 and is a completely different figure from Nunavut's $117,300. The Gwich'in Tribal Council offers up to $2,500 in bereavement assistance and the Inuvialuit Regional Corporation runs its own funeral program, but neither portal explains how their grants interact with federal CPP benefits or territorial income assistance. The Extended Health Benefits program requires your CRA Line 23600 to prove your new income level, but nobody tells you that your single-income status likely qualifies you for coverage you never had before. And the Senior Home Heating Subsidy, the Property Tax Relief program, and the Housing NWT grants all require separate annual applications that are not retroactive if you miss them.

You are supposed to figure all of this out while grieving, while the furnace runs on the last tank of fuel, while the bank refuses to release a single dollar until someone files the right form with the right court in the right jurisdiction.

The Northwest Territories Survivor Benefits Navigator is a Benefit Claims System that covers every federal, territorial, municipal, and Indigenous program available to surviving families in the NWT. Not a collection of links to government PDFs. Not a generic Canadian survivor benefits overview with "Northwest Territories" pasted into the headings. A chronological, plain-language execution plan that tells you which benefits exist, which ones you qualify for, what documents each agency demands, and exactly what order to file in so that one application does not disqualify you from another.

What's Inside the Benefit Claims System

A complete guide, a Survivor Benefits Quick-Start Checklist, and standalone reference documents covering every stage from the first 72 hours through long-term income protection and estate resolution, built specifically for NWT legislation, agencies, and the realities of northern living:

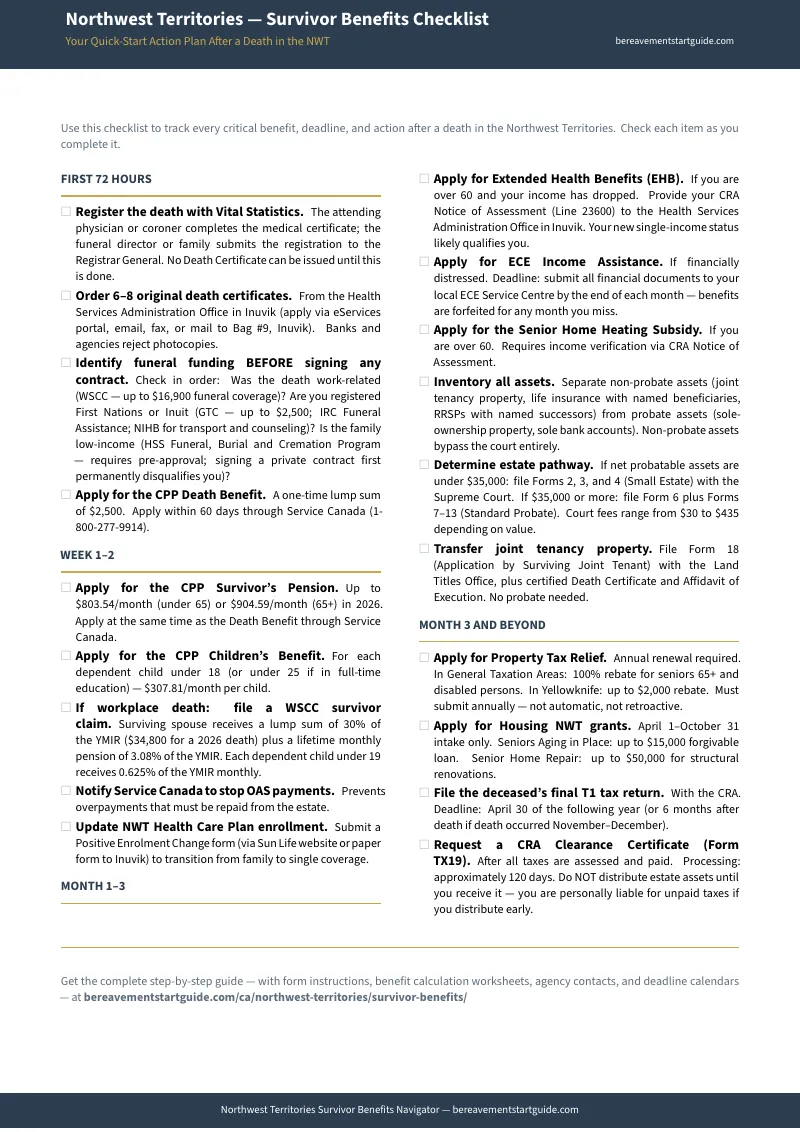

First 72 Hours: Death Certificates and Funeral Funding Sequencing

Every benefit application in this guide requires an official death certificate, and those certificates come from exactly one place: the Health Services Administration Office in Inuvik. Standard processing costs $26 per certificate; expedited costs $38. The guide tells you to order 6 to 8 copies immediately because banks, the Supreme Court, the WSCC, and insurance companies all reject photocopies. More critically, this chapter walks you through the funeral funding sequence that most families get catastrophically wrong. The HSS Funeral, Burial and Cremation Program requires a Benefits Administrator to approve costs before you sign any contract with a funeral director. Sign first, and your application is permanently denied. The guide lays out the exact order: WSCC first if the death was work-related (up to $16,900 in funeral coverage), Indigenous programs second (GTC up to $2,500, IRC assistance), CPP death benefit third ($2,500 lump sum), and territorial payer-of-last-resort programs last.

Survivor Income: CPP, WSCC, and the YMIR Calculation Worksheet

The CPP survivor's pension pays up to $904.59 per month if you are 65 or older, or $803.54 if you are under 65. But if the death was work-related, the WSCC provides an entirely separate layer of compensation calculated against the Year's Maximum Insurable Remuneration. For a 2026 NWT workplace death, that means a one-time lump sum of $34,800 (30% of the $116,000 YMIR), a lifetime monthly pension of $297.73 (3.08% of YMIR), and a dependent child pension of $60.42 per month per child (0.625% of YMIR). The guide includes a fill-in calculation worksheet so you can compute your exact WSCC entitlements without decoding the Workers' Compensation General Regulations yourself. It also covers the CPP Children's Benefit ($307.81 per month per eligible child) and the ECE Income Assistance program for households facing immediate destitution.

Health Coverage Continuity: EHB, NWT Health Care Plan, and NIHB

When your spouse dies, your health coverage does not automatically continue. You must submit a Positive Enrolment Change form to transition from family to single coverage on the NWT Health Care Plan. If you are over 60, you likely now qualify for the Extended Health Benefits program because your household income has dropped to single-earner levels. The guide explains exactly how to use your CRA Notice of Assessment (Line 23600) to prove eligibility. For registered First Nations and recognized Inuit, the federal Non-Insured Health Benefits program provides medical transportation, prescription drug coverage, and grief counseling alongside territorial coverage. The guide maps which programs stack and which require separate applications.

Property Protection: Tax Relief, Housing Grants, and Annual Renewal Traps

Losing a spouse's income can threaten your ability to keep your home. The NWT offers a Senior Citizens and Disabled Persons Property Tax Relief program that provides a 100% rebate in General Taxation Areas and up to $2,000 annually in Yellowknife. Housing NWT provides forgivable loans of up to $15,000 through the Seniors Aging in Place program and up to $50,000 through the Senior Home Repair program. But every one of these benefits requires a proactive annual application. Property Tax Relief is not automatic and not retroactive. Housing NWT applications are accepted only from April 1 to October 31. Miss the window, and you pay the full tax bill or wait until next year for home repairs in a climate that does not wait. This chapter gives you the exact application timeline and tells you to put renewal dates on your calendar as recurring annual tasks.

Estate Pathway: Small Estate, Standard Probate, and the Public Trustee Decision

Before you file anything with the Supreme Court, you need to separate non-probate assets (joint tenancy property, life insurance with named beneficiaries, RRSPs with named successors) from probate assets. The NWT's small estate threshold is $35,000, which is extraordinarily low. A single vehicle can push you past it. The guide includes an estate value worksheet that walks you through the calculation and tells you which court process applies. It also explains the Public Trustee's strict eligibility criteria: minors as sole beneficiaries, incapacitated beneficiaries, senior spouses over 65, or no next of kin. If you do not meet those criteria, the Public Trustee will decline involvement, and you must handle administration yourself. The guide covers both paths so you are not left stranded.

The Intestacy Trap: The NWT's $50,000 Preferential Share

If the deceased died without a will, the Intestate Succession Act gives the surviving spouse a preferential share of only $50,000 before the remainder is divided with children. Compare that to Ontario's $350,000 or Alberta's $150,000. For a family with a home worth $250,000 and $50,000 in savings, the surviving spouse ends up with $133,333 out of a $300,000 estate and may be forced to sell the home. The guide explains exactly when to stop and consult an estate lawyer before filing any court documents.

Indigenous-Specific Programs: GTC, IRC, and NIHB Integration

Indigenous funeral assistance programs do not automatically disqualify you from other benefits, but the sequencing matters. Receiving a GTC or IRC grant does not prevent you from claiming the CPP death benefit. But if you are also applying for HSS funeral funding, you must disclose all other funding because HSS calculates its payment as the gap between your other funding and the total cost. The guide maps the exact interaction between Indigenous, federal, and territorial programs so you claim everything you are entitled to without accidentally triggering an offset that reduces your total.

Tax, CRA Clearance, and the Personal Liability Trap

The executor must file a final T1 return for the deceased and request a CRA Clearance Certificate (Form TX19) before distributing any estate assets. Processing takes approximately 120 days. If you distribute assets before receiving the certificate and the estate later owes taxes, you are personally liable for the unpaid amount. The guide covers the filing deadline (April 30 of the following year, or 6 months after death if the death occurred in November or December), the immediate step of stopping OAS payments to prevent clawbacks, and how the surviving spouse's own tax situation changes in ways that affect eligibility for GST/HST credits, the Canada Child Benefit, and territorial income-tested programs.

Key Contacts Directory and Timeline Tracker

A complete directory of every federal, territorial, regional, and Indigenous agency you will interact with, organized by function rather than bureaucratic hierarchy. Plus a chronological timeline tracker from Day 1 through final estate distribution, with checkboxes for every major milestone and the agency responsible for each one. No more guessing what comes next or which office to call.

Who This Guide Is For

- The surviving spouse whose household income just disappeared and who needs to secure CPP survivor payments, Extended Health Benefits, and property tax relief before the next heating bill arrives, but has no idea which of the twelve agencies listed in the guide controls which benefit

- The Family Coordinator in a remote Indigenous community who has been designated to manage funeral logistics and benefit claims on behalf of the extended family, and needs to navigate GTC bereavement grants, IRC funeral assistance, NIHB transportation coverage, and federal CPP benefits without accidentally disqualifying the family from territorial payer-of-last-resort funding

- The adult child acting as executor who may live outside the NWT and must coordinate with Vital Statistics in Inuvik, the Supreme Court in Yellowknife, and multiple benefit agencies, all while unable to swear affidavits over video because the territory does not allow remote commissioning

- The surviving family of a workplace fatality who needs to file a WSCC claim immediately and calculate the lump sum, monthly pension, and dependent child pensions against the $116,000 YMIR, but cannot parse the Workers' Compensation General Regulations without a plain-language worksheet

- Government Service Officers, band administrators, and community health nurses who need a single reference manual they can hand to a grieving family or use as a desk guide when someone walks in asking for help with paperwork they have never seen before

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across Service Canada, the WSCC, the NWT Department of Health and Social Services, the Department of Education Culture and Employment, the Public Trustee's office, the Gwich'in Tribal Council, the Inuvialuit Regional Corporation, and a dozen municipal agencies. Here is what you actually encounter when you try to claim survivor benefits using free sources alone:

- Service Canada covers federal benefits accurately but ignores territorial programs entirely. Their CPP pages explain the $2,500 death benefit and the monthly survivor's pension. They say nothing about how receiving the CPP death benefit interacts with the NWT's payer-of-last-resort funeral programs, how WSCC pensions stack on top of CPP, or that your new single-income status probably qualifies you for territorial Extended Health Benefits you never had before. If you rely on Service Canada alone, you will miss every territorial dollar.

- Territorial agencies publish bureaucratic policy manuals, not guides. The HSS Funeral, Burial and Cremation Program guidelines state that the department is the "payer of last resort." That is a legal definition. It does not tell a grieving spouse how to practically prove indigent status, what documents to bring, or that signing a funeral contract before getting HSS approval permanently disqualifies you from funding. The ECE Income Assistance pages assume you understand government procurement terminology and CRA line items.

- The WSCC website is written for employers, not surviving families. The YMIR documentation explains how employers calculate assessable payroll. Finding the survivor pension formula (3.08% of YMIR) requires reading the Workers' Compensation General Regulations. A traumatized spouse trying to figure out their monthly income should not have to parse regulatory math to learn they are entitled to $297.73 per month.

- Indigenous governance portals cover their own programs but do not integrate with federal or territorial systems. The GTC provides application forms and lists of local grave diggers and casket makers in Gwich'in communities. The IRC details its Funeral Assistance Program. Neither explains how receiving a tribal grant affects an application for the HSS funeral program or whether it offsets the CPP death benefit. The Family Coordinator is left to guess how the systems interact.

- SEO aggregators miss the reality of remote northern living. EstateExec and similar platforms correctly list the NWT's $35,000 small estate threshold and probate fee schedule. They completely miss the Government Service Officers who can commission oaths in fly-in communities, the centralized vital statistics office in Inuvik, the absence of a crematorium in the entire territory, and the fact that mail delays can add weeks to every step. Their content is built for urban Canada with a territorial label pasted on.

- Financial advisors and wealth planners target high-net-worth estate optimization. TD, Edward Jones, and similar firms publish probate fee comparisons across Canadian jurisdictions. They have no content addressing the Senior Home Heating Subsidy, ECE Income Assistance for destitute families, Indigenous funeral grants, or the WSCC survivor pension. If the estate is modest or the family is low-income, these resources are irrelevant.

Free resources give you fragments from a dozen agencies that do not reference each other and assume you already understand which program belongs to which level of government. The Benefit Claims System puts every NWT-specific benefit, form, deadline, funding source, and agency contact into one document, in the order a surviving family actually needs them, with plain-language explanations that turn bureaucratic policy manuals into a claims checklist you can follow without a government service officer sitting next to you.

— Less Than One Hour With a Yellowknife Lawyer

A single consultation with an estate lawyer in the NWT costs $300 or more per hour, if you can get an appointment in a territory with fewer than thirty lawyers. A fee-based financial planner charges $150 to $250 per hour to review your benefit options. This guide costs less than one hour of professional time and gives you the complete NWT-specific benefit claims system: every federal, territorial, and Indigenous program, every application sequence, every deadline, every agency contact, and the WSCC calculation worksheets that turn impenetrable regulations into fill-in-the-blank arithmetic.

Your download includes the complete guide with the Survivor Benefits Quick-Start Checklist, the WSCC Survivor Benefit Calculation Worksheet, the Estate Value Worksheet, the Document Gathering Master Checklist, the Survivor Eligibility Quick-Reference, the Key Contacts Directory, and the Timeline Tracker. Plus a 30-day money-back guarantee. If the guide does not give you clarity on which benefits apply to your family and confidence that you are claiming them in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Northwest Territories Survivor Benefits Checklist covering the most critical actions for the first 72 hours, the first month, and the months ahead: which death certificates to order, how to sequence funeral funding without disqualifying yourself, where to apply for CPP and WSCC benefits, and when to file for property tax relief and housing grants. It is enough to get oriented and stop the financial bleeding.

You did not choose this. But the benefits exist, and they are yours to claim. The guide shows you exactly how, one agency at a time.