Your Spouse Died in a Fly-In Community. Service Canada Said to Mail the Forms. The WSCC Sent a Policy Manual Written for Actuaries. The Public Trustee Said to Wait Three Years. And Nobody Told You That Common-Law Partners Get Nothing Under Nunavut Intestacy Law.

You called Service Canada to apply for the CPP Survivor's Pension. They said to fill out the application and mail it from your community. You asked which form. They transferred you. You were on hold for forty minutes before the line dropped. You called back the next day and reached someone who explained the $2,500 Death Benefit and the monthly Survivor's Pension, but could not tell you whether your common-law partner status qualifies under territorial law or only under federal rules. They suggested you contact a lawyer.

You searched for the WSCC death benefits because the death was work-related. You found a policy manual that referenced the Year's Maximum Insurable Remuneration, a 3.08% spousal pension rate, a 0.625% dependent child rate, and an upcoming legislative transition from lifetime pensions to lump-sum payments. You do not know what the 2026 Nunavut YMIR is, how to calculate your actual monthly payment, or whether accepting WSCC benefits will reduce your CPP pension. Nobody explained the 50% offset rule.

You contacted NTI about bereavement travel. They said the Compassionate and Bereavement Travel Program covers flights for three family members, but only for enrolled NLCA beneficiaries, and only if the application is submitted within one week of the funeral. The funeral was four days ago. You have three days left. You do not know where to find your Community Liaison Officer or what documentation they need.

You discovered that the deceased had no will. You searched "Nunavut intestacy" and found a Legal Aid PDF that explained the Intestate Succession Act in general terms. It said the surviving spouse receives a $50,000 preferential share. In Ontario, that number is $350,000. In British Columbia, $300,000. In Nunavut, an estate with a snowmobile, hunting equipment, and a modest dwelling can exceed $50,000, forcing you to split everything above that threshold with the deceased's children. Nobody told you this before the estate was frozen.

The Nunavut Survivor Benefits Navigator is the Northern Benefits Recovery System for families who need to claim every federal, territorial, and Inuit-specific benefit they are owed after a death in Nunavut -- without waiting three years for the Public Trustee, without hiring a lawyer in Iqaluit, and without trying to decode actuarial policy manuals written for employers. Not a repurposed southern Canadian benefits guide. Not a Service Canada FAQ that ends with "contact your local office" when the nearest office is a $1,200 flight away. A plain-language, Nunavut-specific system that sequences every benefit, every form, every deadline, and every agency contact in the order you actually need them.

What's Inside the Northern Benefits Recovery System

A step-by-step guide, a survivor benefits checklist, and standalone reference tools covering every benefit, pension, and financial entitlement available to surviving families in Nunavut, built on the CPP Act, the WSCC Workers' Compensation Act, the Intestate Succession Act, the NTI Compassionate and Bereavement Travel Policy, and the territorial programs that make benefits recovery in the North fundamentally different from anywhere else in Canada:

The Funeral Funding Sequencer: Five Agencies in the Right Order

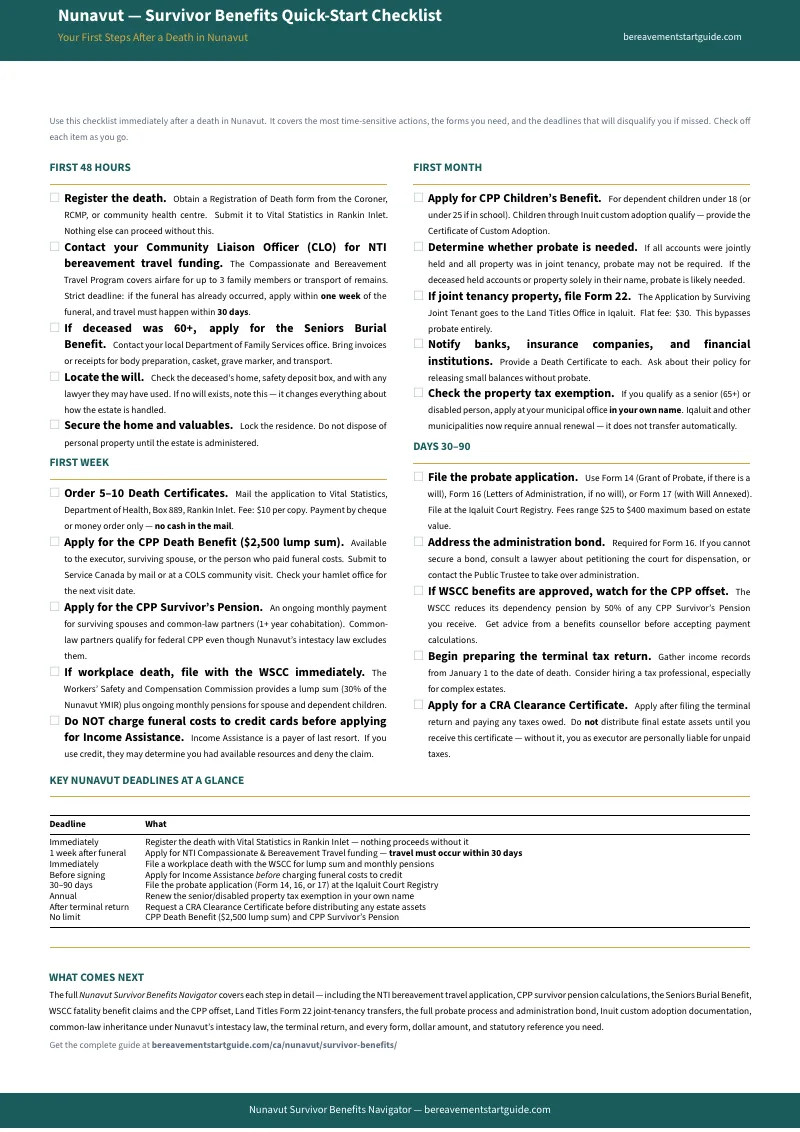

Funeral costs in Nunavut routinely exceed $6,000 because caskets must be flown in by air cargo and graves must be opened in permafrost. Five separate agencies can help pay -- NTI bereavement travel, the Seniors Burial Benefit, the CPP Death Benefit, WSCC fatality payments, and GN Income Assistance -- but they must be approached in a specific order because Income Assistance is explicitly a "payer of last resort" and will deny your claim if you have not exhausted the others first. The guide maps the exact sequence, eligibility criteria, and documentation required for each source so you do not get disqualified by applying in the wrong order or charging funeral costs to a credit card before applying.

CPP Survivor Benefits: Common-Law Partners Qualify Federally Even When Nunavut Law Excludes Them

This is the chapter that prevents the most expensive misunderstanding in Nunavut bereavement. The territorial Intestate Succession Act excludes common-law partners from automatic inheritance. But the federal Canada Pension Plan recognizes common-law relationships after just one year of cohabitation. You can claim the $2,500 CPP Death Benefit and the ongoing monthly Survivor's Pension even if Nunavut law treats you as a legal stranger to the estate. The guide walks through the federal definition, the documentation that proves cohabitation, and the separate application process for the Death Benefit, the Survivor's Pension, and the Children's Benefit -- including children through Inuit custom adoption.

WSCC Death Benefits: Plain-Language Calculations Using the 2026 Nunavut YMIR

The Workers' Safety and Compensation Commission publishes death benefit formulas in policy manuals designed for employers and actuaries. The guide translates them for families. The 2026 Nunavut YMIR is $117,300. Your spousal pension is 3.08% of YMIR per month. Each dependent child receives 0.625% per month. The lump-sum fatality payment is 30% of YMIR. The guide provides pre-calculated payment tables, explains the upcoming legislative transition from lifetime pensions to lump-sum compensation, and identifies the critical 50% offset: the WSCC reduces its dependency pension by half of any CPP Survivor's Pension you receive. Without understanding this offset, you will accept a lower combined payment than you are entitled to.

NTI Bereavement Travel: Claiming Flights, Hotel Reimbursements, and Remains Transport

The NTI Compassionate and Bereavement Travel Program covers airfare for up to three NLCA beneficiaries and the cost of shipping remains to the burial community. Hotel reimbursements are capped at $1,000 total (four nights) for weather delays. But the strict one-week post-funeral application deadline and the requirement to route everything through a Community Liaison Officer means families regularly miss the window or submit incomplete applications. The guide provides the step-by-step CLO contact process, the documentation checklist, the eligibility rules for Regional Inuit Associations (QIA, KIA, Kitikmeot), and the exact distinction between NTI travel funding and the separate GN funeral cost programs.

The Common-Law Intestacy Trap: What Unmarried Partners Must Do Immediately

Nunavut's Family Law Act recognizes common-law partners for property division. The Intestate Succession Act does not. If your partner dies without a will, you are legally excluded from the $50,000 preferential spousal share and from automatic inheritance. Your only recourse is a Dependants Relief Act claim -- and the application window is limited. The guide explains the exact steps to file a dependant's maintenance claim, how to document the relationship for court, and which assets (joint accounts, named beneficiary designations) bypass the estate entirely so you can access funds without waiting for probate.

Custom Adoption and Survivor Benefits: Proving Eligibility for CPP Children's Benefits

Children adopted through Inuit custom adoption have identical legal standing to biological children under Nunavut law, but federal agencies do not always recognize the Certificate of Custom Adoption without additional documentation. The guide explains how to obtain or retroactively register a custom adoption certificate through the Aboriginal Custom Adoption Commissioner, which documents to submit alongside CPP Children's Benefit applications, and how to handle federal agents who are unfamiliar with Nunavut's custom adoption framework.

The 90-Day Benefits Timeline: Every Deadline, Form, and Agency Contact in Sequence

Days 1-3 focus strictly on funeral funding and NTI travel. Days 4-14 cover agency notifications, CPP applications, and WSCC claims. Days 15-30 address probate decisions, bank notifications, and property tax transfers. Days 30-90 cover probate filing, the administration bond, the CPP-WSCC offset calculation, the terminal tax return, and the CRA Clearance Certificate. The guide sequences every task chronologically so you never miss a deadline and never tackle a complex form before you have the prerequisite documents in hand.

Who This Guide Is For

- The common-law partner who just discovered they inherit nothing under Nunavut intestacy law -- who needs to understand immediately that CPP Survivor's Pension qualifies on the federal definition of common-law (one year of cohabitation), and that a Dependants Relief Act claim can protect their housing and assets before the estate is distributed to other heirs.

- The adult child executor trying to avoid the Public Trustee's two-to-three-year timeline -- who needs to know that Nunavut probate fees cap at $400, that DIY administration is straightforward with the right forms, and that every month spent waiting for the Public Trustee is a month that bills, taxes, and housing issues compound without resolution.

- The family in a fly-in community trying to pay for a funeral -- who needs the Funeral Funding Sequencer to access NTI travel, the Seniors Burial Benefit, and CPP in the correct order before Income Assistance will even consider their application.

- The surviving spouse of a worker killed on the job -- who needs plain-language WSCC pension calculations, the current YMIR figures, and an explanation of the 50% CPP offset that the WSCC policy manual buries in actuarial language.

- The community health worker, CLO, or social worker -- who assists grieving families regularly and needs a reliable, printable desk reference covering every benefit program, every deadline, and every form, organized into a reproducible checklist they can hand directly to families.

Why Free Resources Will Not Get You Through This

Survivor benefits information for Nunavut exists. Service Canada publishes CPP guides, the WSCC publishes policy manuals, NTI publishes travel policies, and national estate platforms produce content about every Canadian jurisdiction. Here is what you actually encounter when you try to claim Nunavut survivor benefits using free sources:

- Service Canada explains CPP nationally but cannot tell you how it interacts with Nunavut law. The CPP Survivor's Pension pages do not mention that Nunavut's Intestate Succession Act excludes common-law partners while the CPP recognizes them. They do not explain how to prove cohabitation from a remote community where you cannot visit a Service Canada office. They tell you to mail the forms and wait.

- The WSCC publishes benefit rates in actuarial language for employers. The policy manuals reference YMIR, 3.08%, and 0.625% without ever showing a family what their actual monthly payment will be. They do not explain the CPP offset in terms a grieving spouse can understand. They assume the reader is an HR professional or a benefits administrator.

- NTI publishes the travel policy but not the application walkthrough. The Compassionate and Bereavement Travel Policy states eligibility rules and coverage limits but does not provide a step-by-step application checklist, does not explain how to contact your CLO, and does not distinguish its coverage from the separate Regional Inuit Association programs or the GN funeral cost programs.

- National estate platforms give you southern Canadian advice with a Nunavut label. Willful and LegalWills discuss probate fees across Canada but say nothing about the Seniors Burial Benefit, NTI travel, WSCC death benefits, or the custom adoption framework. Their content is templated from Ontario and British Columbia with a Nunavut fee schedule appended.

- The Public Trustee explains how to surrender your benefits administration -- not how to manage it yourself. The Office of the Public Trustee provides materials for families who want to hand over the entire process. They do not provide guidance on claiming benefits independently, and their timeline of two to three years means your pension applications, tax obligations, and property transfers sit frozen while you wait.

Free resources give you CPP forms without Nunavut context, WSCC calculations in actuarial language, NTI policies without application checklists, national platforms that assume you live in Toronto, and a Public Trustee who wants to manage your benefits for three years. The Northern Benefits Recovery System puts every Nunavut-specific benefit, form, deadline, and calculation into one document, sequenced in the order you actually need them.

-- Less Than One Hour of a Benefits Counsellor's Time

A benefits counsellor or estate lawyer in Iqaluit charges $300 to $450 per hour. The Public Trustee charges a $400 file opening fee before any work begins, plus ongoing commissions on every dollar that flows through the estate. A missed CPP application costs you months of retroactive pension payments. A misunderstood WSCC offset means you accept thousands less than your entitlement. This guide costs less than a single consultation and gives you the complete Nunavut-specific benefits recovery system: every pension calculated, every deadline mapped, every form annotated, and every agency contact listed.

Your download includes 9 PDFs: the complete step-by-step guide, the standalone Nunavut Survivor Benefits Checklist, and seven printable reference tools: the Funeral Funding Sequencer, the CPP Application Walkthrough, the WSCC Payment Calculator, the NTI Travel Documentation Checklist, the Common-Law Partner Action Plan, the Custom Adoption Documentation Guide, and the 90-Day Benefits Timeline with every deadline and agency contact. Instant download, no account required.

30-day money-back guarantee. If this guide does not make every benefit you are owed immediately clear and save you hours of phone calls to agencies that cannot advise you on Nunavut-specific entitlements, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Nunavut -- Survivor Benefits Checklist -- a one-page overview of the most urgent benefits to claim, the critical deadlines, and the mistakes that cost families the most in the first two weeks. Enough to get organized and determine whether you need the full guide.

Nobody trained you for this. Service Canada assumes you can visit an office. The WSCC assumes you can read actuarial tables. NTI assumes you know your CLO. The court assumes you hired a lawyer. The national websites assume you live in the south. You have something none of them provide -- a benefits recovery system built entirely for the realities of Nunavut, by someone who calculated every pension, mapped every funding source, and sequenced every deadline that exists above the 60th parallel.