You Were Named Estate Trustee. The Ontario Superior Court Requires a Certificate of Appointment Before Any Institution Will Release a Dollar. The Ministry of Finance Requires a Separate Estate Information Return Filed via Gentax Within 180 Days — With Penalties Starting at $1,000 for Late Filing. And the Estate Administration Tax Calculation Has an Exemption Threshold, a Rounding Rule, and a Deduction Limit That Most Executors Get Wrong on Their First Filing.

Someone you loved has died, and you are now the person responsible for their entire financial life. The bank froze the accounts the day the death was registered — they will not release a cent without a Certificate of Appointment of Estate Trustee, even if you are named in the will and even if you held Power of Attorney the day before. That authority ended at death. The mortgage, property taxes, utilities, and insurance premiums on the house do not pause while you wait for the court to process your application — and in Toronto, that wait runs four to six months. You are carrying the estate's costs out of your own pocket, and the beneficiaries are asking when they will see their share.

You searched for help. The Ontario.ca website has the court forms — Form 74A for standard estates, Form 74.1A for small estates — but no instructions explaining the difference between a standard and small estate application, which supporting documents are required for each, or what causes the court to reject a package and send it back. The Justice Services Online portal accepts electronic filings but still requires the original will mailed to the courthouse separately. Law firm websites explain the complexity in careful detail, then quote $3,000 to $5,000 for standard probate representation. ClearEstate charges $4,648 or more. Reddit has answers, but the top comment applied Nova Scotia's tiered probate fee structure to an Ontario question — Ontario's Estate Administration Tax works completely differently.

Here is what nobody connects for you: Ontario uses its own terminology — "Estate Trustee" instead of executor, "Certificate of Appointment" instead of Grant of Probate — and every court form, every portal login, and every official letter uses the Ontario terms. The estate is overseen by two separate bodies operating on independent timelines: the Superior Court of Justice issues the Certificate, but the Ministry of Finance independently audits the estate's value through the mandatory Estate Information Return filed via the Gentax portal. Receiving the Certificate is not the finish line — the Ministry can audit your EIR for up to four years, and indefinitely if it suspects fraud. The Estate Administration Tax calculation has a $50,000 exemption, a rounding-up rule, and a deduction limit that allows only real estate encumbrances — not credit card debt, not funeral costs, not income tax owing. And since April 2021, estates valued at $150,000 or less qualify for the simplified Small Estate Certificate, but it has its own 30-day notice period that catches applicants off guard when they discover they cannot file until the waiting period expires.

The Ontario Probate Process Guide is a Court-Ready Filing System for the complete Ontario probate process — from the initial question of whether a Certificate of Appointment is even required through the CRA clearance certificate and final distribution. Not a generic Canadian probate overview that confuses Nova Scotia's tiered fee structure with Ontario's flat-rate tax. Not a law textbook. A 13-chapter, Ontario-specific manual built around the current Estates Act, the Estate Administration Tax Act, Rule 74 and Rule 74.1 of the Rules of Civil Procedure, the Succession Law Reform Act, and the Trustee Act — so your application passes the court registry review the first time.

What's Inside the Court-Ready Filing System

A 13-chapter guide, a standalone Probate Quick-Start Checklist, and 7 printable reference tools — covering every stage from the probate decision through final distribution, built specifically for Ontario's Superior Court of Justice as the forms and rules exist right now:

Chapter 1: Understanding Ontario's Probate System

Ontario does not use the word "probate" in its court system — the formal process is applying for a Certificate of Appointment of Estate Trustee. This chapter explains the terminology, the critical distinction between the Superior Court of Justice (issues the Certificate) and the Ministry of Finance (audits the Estate Information Return), and why Power of Attorney authority ended the instant the person died — even if you are also named Estate Trustee in the will. The key legislation: the Estates Act, the Succession Law Reform Act, the Estate Administration Tax Act, Rules 74 and 74.1, and the Trustee Act.

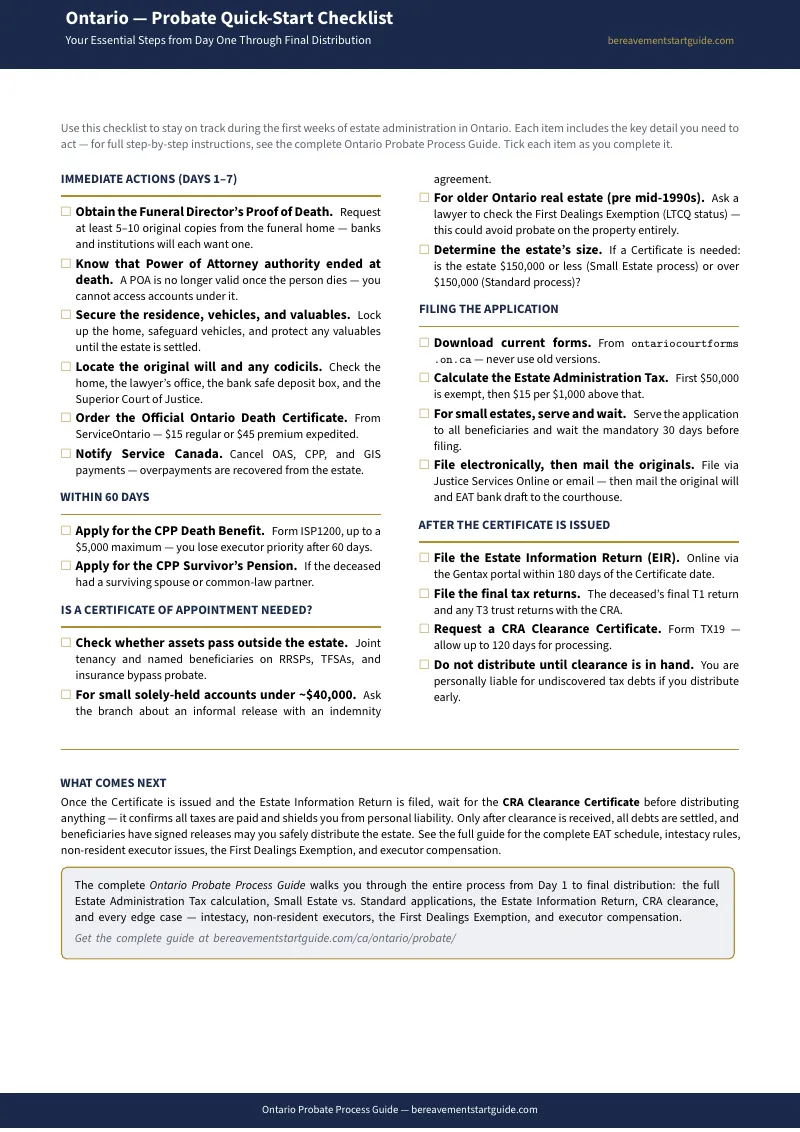

Chapter 2: Immediate Actions — Days 1 to 7

The Funeral Director's Proof of Death versus the Official Ontario Death Certificate from ServiceOntario ($15 regular, $45 premium expedited — regular processing runs up to 16 weeks). Securing the property, redirecting mail, locating the original will (check the home, the lawyer's office, the bank safe deposit box, and the Superior Court of Justice). Notifying Service Canada to cancel OAS and CPP payments before overpayments accumulate. The CPP Death Benefit application — up to $5,000, but the estate trustee loses priority if the application is not filed within 60 days.

Chapter 3: Do You Actually Need a Certificate of Appointment?

Not every Ontario estate needs a trip to court — and the Estate Administration Tax alone can run into thousands of dollars for larger estates. The decision framework: joint tenancy property passes automatically with just a death certificate; RRSPs, TFSAs, and life insurance with named beneficiaries bypass the estate entirely; banks will often release solely-held accounts under approximately $40,000 with a personal indemnity agreement signed by all beneficiaries. The First Dealings Exemption for real estate purchased before Land Titles Conversion Qualified (LTCQ) status — this can bypass the Certificate entirely for the property. The decision checklist that tells you definitively whether you need to apply.

Chapter 4: Standard vs. Small Estate — Which Process Applies?

Since April 1, 2021, estates valued at $150,000 or less can use the simplified Small Estate Certificate under Rule 74.1 — a simpler form (74.1A), no administration bond usually required, and faster processing. But it has a mandatory 30-day notice period: you must serve a copy of the application to all beneficiaries and wait 30 days before filing. Estates over $150,000 use the standard application under Rule 74 (Form 74A), which has different notice requirements and may require an administration bond. The side-by-side comparison so you choose the correct track before preparing a single form.

Chapter 5: Calculating the Estate Administration Tax

The exact math that determines whether your application is accepted. First $50,000 of estate value: $0. Every $1,000 above $50,000 (rounded up): $15. Estates at $50,000 or less pay nothing. The critical deduction rule: you can subtract real estate encumbrances (mortgages, registered liens) from the property value, but you cannot deduct credit card balances, personal loans, funeral costs, or income tax owing. A worked example showing how the calculation works for a $300,000 home with a $100,000 mortgage plus $39,250 in bank accounts. The EAT quick reference table from $50,000 to $1,000,000. And the rounding-up rule that catches people who calculate to the exact dollar.

Chapter 6: Preparing Your Court Application

The chapter that does not exist in any free resource. Which forms you need depends on whether there is a will, whether the estate qualifies as small or standard, whether the deceased was an Ontario resident, and whether any beneficiary is a minor or incapable person. Form 74A versus Form 74.1A versus Form 74D (with will annexed) versus Form 74H (no will) — plus the supporting affidavits, renunciations, draft Certificate, and administration bond where applicable. What the court checks on every page, the name-matching requirement between the death certificate and the will, and the errors that cause the registry to reject the entire package.

Chapter 7: Filing Your Application

Ontario's hybrid electronic filing system through Justice Services Online (JSO). The application is submitted electronically, but the original will and the EAT bank draft must be physically mailed to the courthouse. Which court location to file with, what to include in the mailing package, the processing timeline (Toronto: 4-6 months; smaller courthouses: 6-8 weeks), and what to do when you receive the Certificate — including how many certified copies to request and why you need more than you think.

Chapter 8: After the Certificate — Post-Grant Duties

The Certificate is in your hands, but the most consequential deadlines are just starting. The Estate Information Return (EIR) must be filed via the Ministry of Finance's Gentax portal within 180 days of the Certificate date — penalties for late filing start at $1,000 and can escalate to twice the estate tax owing plus potential imprisonment. This chapter covers the Gentax registration process, what the Ministry requires in the EIR, how the Ministry's independent valuation audit works (up to four years, indefinitely for suspected fraud), and the estate-closing obligations: creditor notices, debt settlement priority, the terminal T1 tax return, deemed disposition rules, and the CRA Clearance Certificate (Form TX19).

Chapter 9: Edge Cases and Special Situations

The First Dealings Exemption explained in full — how LTCQ real estate status bypasses the Certificate requirement for property transfers. Administration bonds for intestate estates and non-resident Estate Trustees (two times the estate value, with sureties). Multiple wills strategy for Ontario private company shares. Lost or destroyed wills and the separate court process required. Foreign assets and multi-jurisdictional estates. Minor and incapable beneficiaries — when you must involve the Office of the Children's Lawyer or the Public Guardian and Trustee.

Chapter 10: Executor Compensation

Ontario's unofficial 5% tariff — the longstanding convention that Estate Trustees may claim approximately 2.5% on capital receipts and 2.5% on capital disbursements. When compensation requires a passing of accounts versus a consent from all beneficiaries. How to calculate and document fair compensation that will withstand scrutiny if any beneficiary objects.

Chapters 11-13: Distribution, Timeline, and Key Contacts

The final distribution process — why you must hold the CRA Clearance Certificate (Form TX19) before distributing a single dollar, because personal liability for the estate's undiscovered tax debt falls on you if you distribute early. The complete timeline from death through estate closing on one page. And every contact: the Superior Court of Justice, ServiceOntario, the Ministry of Finance, the CRA, Service Canada, the Office of the Children's Lawyer, and the Public Guardian and Trustee.

Who This Guide Is For

- The newly named Estate Trustee who has never filed a court document and needs Ontario's unique forms and terminology — Certificate of Appointment, Estate Trustee, Form 74A versus 74.1A — translated into plain language with the filing requirements, the form selection logic, and the common rejection triggers explained step by step

- The surviving spouse who needs to know whether joint tenancy, named beneficiaries, and the bank's indemnity agreement threshold mean the estate can be settled without a Certificate — and what still must be done even if the court process is not required

- The DIY executor on a budget who knows that law firms charge $3,000 to $5,000 for standard probate and ClearEstate charges $4,648 or more — and needs a guide that replaces hourly consultations for routine procedural questions, while clearly identifying the complications that genuinely require professional help

- The out-of-province Estate Trustee managing an Ontario estate from British Columbia, Alberta, or another province — who needs to know which steps can be handled remotely through Justice Services Online and which require physical documents mailed to the courthouse, plus the administration bond requirement for non-resident applicants

- The executor under family pressure who needs an authoritative, standardized timeline to show impatient beneficiaries that the 4-to-6-month processing wait in Toronto, the 180-day EIR filing deadline, and the CRA clearance processing time are legal requirements — not evidence of delay or negligence

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across Ontario.ca, the Superior Court of Justice, the Ministry of Finance, Justice Services Online, ServiceOntario, Service Canada, and the CRA. Here is what you encounter when you try to assemble the process from free sources alone:

- Ontario.ca publishes the forms but not the filing instructions. Forms 74A, 74.1A, 74D, and 74H are downloadable from ontariocourtforms.on.ca. What is not published: the exact circumstances that determine which form set you need, which supporting documents are required for each application type, the hybrid JSO filing process (electronic submission plus physical mailing of the original will), or the common errors — name mismatches, incorrect EAT calculations, missing affidavits — that cause the court to reject the entire package. The forms are there. The instructions to use them correctly are not.

- The Ministry of Finance explains the EIR requirement but not the Gentax process. You will learn that you must file the Estate Information Return within 180 days of the Certificate date. You will not find a step-by-step walkthrough of the Gentax portal registration, the valuation methods the Ministry expects for each asset class, or the audit triggers that flag returns for review. The requirement is documented. The execution path is not.

- Law firm blogs explain the complexity to justify retainer fees. Probate lawyers publish clear, helpful articles answering specific questions — the EAT formula, the small estate threshold, the First Dealings Exemption. Each article concludes with a call to book a consultation at $300 to $500 per hour, with full representation running $3,000 to $5,000 or more. For contested estates, that advice is appropriate. For uncontested estates with a clear will and cooperative beneficiaries, the same answers cost a fraction of a legal retainer.

- Reddit applies the wrong province's rules. The most common error on Canadian personal finance forums is applying another province's probate fee structure to an Ontario question. Nova Scotia uses a tiered structure with a base-plus-overage calculation. British Columbia charges a flat percentage above a different threshold. Ontario has a $50,000 exemption and a $15-per-$1,000 flat rate above that — plus the unique deduction rule that allows real estate encumbrances but nothing else. Wrong-province advice applied to an Ontario estate means either overpaying for unnecessary legal help, or missing Ontario-specific requirements like the 180-day EIR, the Gentax portal, and the Small Estate Certificate's 30-day notice period.

- National estate platforms lack Ontario-specific depth. ClearEstate, Willful, and Epilogue provide modern workflows for executors across Canada. They are helpful for general orientation. But they gloss over the specific intersection of Ontario's dual oversight structure (court plus Ministry of Finance), the First Dealings Exemption for LTCQ real estate, the hybrid JSO electronic filing process, the administration bond requirement for intestate estates and non-resident applicants (two times the estate value), and the unofficial 5% executor compensation tariff. An Ontario executor following national-level guidance risks filing an application that the local court returns for province-specific errors.

Free resources give you forms without filing instructions, a tax requirement without the Gentax walkthrough, and advice from the wrong province. The Court-Ready Filing System puts every Ontario-specific form, fee, deadline, and filing step into one document, in the order the Superior Court of Justice actually requires them.

— Less Than Thirty Minutes With an Ontario Probate Lawyer

A single consultation with an Ontario probate lawyer costs $300 to $500 per hour. Standard probate representation runs $3,000 to $5,000 for routine estates — and significantly more if complications arise. ClearEstate's assisted service starts at $4,648. For a modest estate, those fees represent a significant portion of what is being passed to the family. This guide costs less than thirty minutes of professional legal time and gives you the complete Ontario-specific filing system — every form mapped to its circumstance, the Estate Administration Tax calculated with worked examples, every statutory deadline flagged, the Gentax EIR walkthrough, and every common rejection trigger identified.

Your download includes the complete 13-chapter guide, the standalone Probate Quick-Start Checklist, and 7 printable standalone tools: the Certificate Decision Tree, the Standard vs. Small Estate comparison, the EAT Calculation Worksheet, the Form Selector Matrix, the Executor Compensation Worksheet, Beneficiary Letter Templates, and an Asset Inventory Worksheet. Plus a 30-day money-back guarantee. If the guide does not give you clarity on what to do next and confidence that your application will pass the court registry review, email us for a full refund.

Not ready for the full guide? Download the free Ontario — Probate Quick-Start Checklist — covering the first actions from securing the estate and ordering death certificates through calculating your EAT, choosing between standard and small estate tracks, and meeting the post-Certificate deadlines. It is enough to see the full picture and start gathering what you need.

You did not choose to be the Estate Trustee. But the court does not wait, the 180-day EIR deadline does not pause, and the carrying costs on an empty house do not stop. The guide makes sure you do not miss any of it.