Someone You Love Died in Ontario. You Are Owed Benefits — Federal, Provincial, and Municipal — but Nobody Gave You the Sequence, the Deadlines, or the Traps That Void Your Eligibility If You Step Wrong.

The CPP Death Benefit has a 60-day priority window. The CPP Survivor's Pension caps retroactive payments at 12 months — every month you delay is money you never recover. Ontario Works funeral assistance is denied if you pay the funeral home before applying. The Estate Administration Tax is due as a deposit when you file for probate, and the Estate Information Return must follow within 180 days or you face personal liability. And somewhere in the middle of all this, you are grieving.

Service Canada covers the federal benefits. ServiceOntario covers the death certificate. The Bereavement Authority covers funeral rights. Your municipality covers funeral grants. The Ministry of Finance covers the estate tax return. The Superior Court covers probate. None of these agencies reference each other. None of them tell you the order. None of them warn you that paying for the funeral before applying for Ontario Works assistance can permanently disqualify you from $2,250 in coverage.

You are expected to be your own project manager across six separate government systems during the worst month of your life. And the cost of getting the sequence wrong is not confusion — it is lost benefits, overpayment clawbacks, and personal liability that follows the executor for years.

The Ontario Survivor Benefits Navigator is a Benefit Recovery System — every federal, provincial, and municipal benefit, entitlement, and tax obligation that follows a death in Ontario, organized into a single chronological timeline with exact forms, dollar amounts, deadlines, and the sequencing traps that cost families thousands of dollars when they act in the wrong order.

What's Inside the Benefit Recovery System

A 14-chapter guide with 3 appendices, a printable quick-start checklist, and 7 standalone worksheets and reference cards — covering every benefit claim, probate track, tax filing, and distribution rule specific to Ontario in 2026:

The Landscape Before You Start (Why Ontario Is Different)

"Spouse" means different things to different agencies — and this single inconsistency is the source of more financial pain than any other issue in Ontario estates. A common-law partner can claim the CPP Survivor's Pension federally, but inherits absolutely nothing under Ontario intestacy law. This chapter maps the four structural features of Ontario's survivor-benefit system that trip up nearly everyone: the common-law definition gap, the two-tier probate system ($150,000 threshold), the Estate Administration Tax plus the mandatory Estate Information Return, and the fact that every Power of Attorney terminated the instant the person died — even if you were paying their bills yesterday.

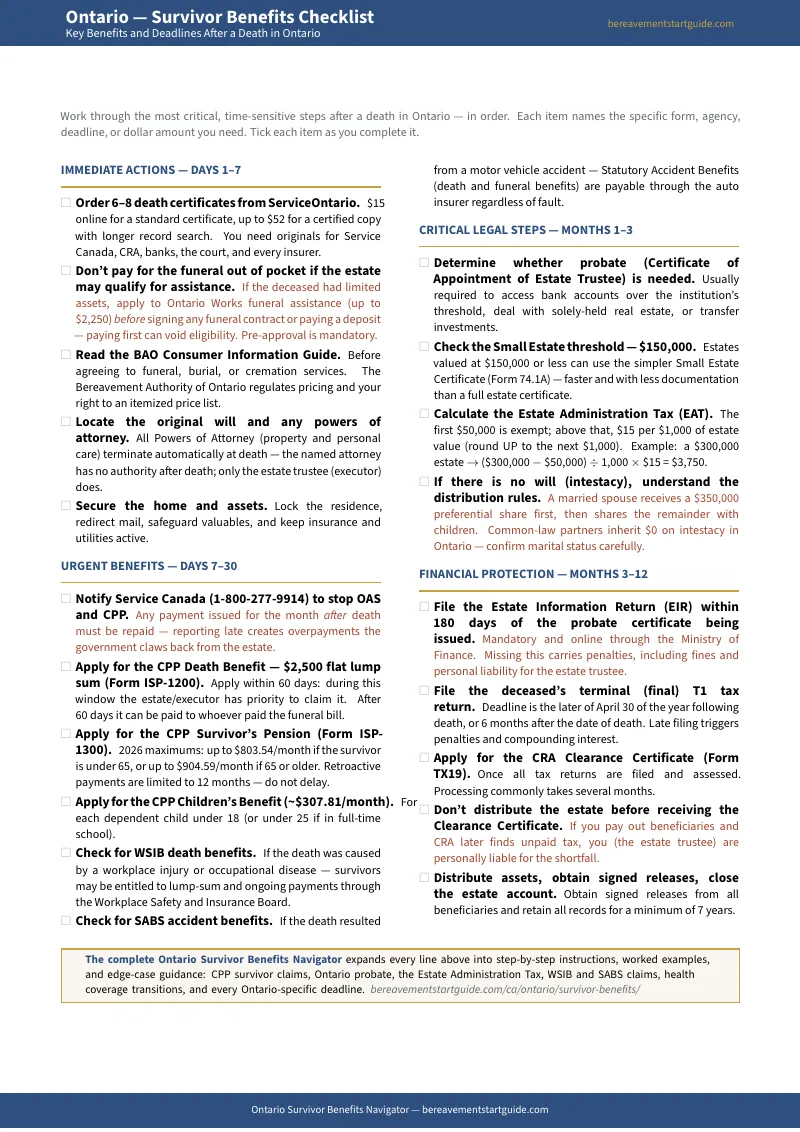

Phase 1: The First 14 Days — Funeral Funding Before You Pay

The single most expensive mistake in this entire process happens in the first week. Government funeral assistance programs — Ontario Works (up to $2,250), the Last Post Fund (up to $7,376 for veterans), Indigenous Services Canada (up to $5,000) — are all "payers of last resort." If you pay the funeral home first and apply afterward, you can be denied entirely. This chapter gives you the exact sequence: who to call, what to say, and how to secure approval before you sign any contract. Plus: how to order the right number of death certificates, the difference between the Funeral Director's Proof of Death and the official Death Certificate from ServiceOntario, and why trying to use a terminated Power of Attorney to access the deceased's accounts will get you nowhere.

Phase 2: Halt Payments and Triage Every Benefit You May Qualify For

Any CPP or OAS payment issued for the month after death must be repaid. The government will claw it back from the estate, and the executor is personally responsible for returning it. This chapter covers the urgent Service Canada notification (1-800-277-9914), the complete benefit triage — which benefits apply to your specific situation, which have hard deadlines, and which can wait — and the exact order to file so nothing falls through.

CPP Survivor Benefits — the Full Calculation, Not the Summary

The CPP Death Benefit is a $2,500 flat lump sum, but the 60-day priority window determines who gets to claim it and how cleanly it flows into the estate. The CPP Survivor's Pension pays up to $803.54/month (under 65) or $904.59/month (65+) — but the combined cap means a surviving spouse already receiving their own CPP retirement pension may receive far less than expected. The CPP Children's Benefit adds approximately $307.81/month per dependent child. This chapter walks through every calculation, form (ISP-1200, ISP-1300), retroactivity rule, and the common-law statutory declaration (ISP-3004CPP) that trips up unmarried partners.

Workplace Deaths, Accident Benefits, Health Coverage, Probate, Intestacy, Estate Taxes, and Distribution

The remaining chapters cover WSIB death benefits (lump sums up to $154,534.73 for workplace fatalities), Statutory Accident Benefits for motor vehicle deaths, Ontario Drug Benefit and property tax relief for surviving seniors, the authority gap between death and probate, both probate tracks (Small Estate Certificate at Form 74.1A vs. standard Form 74A), the intestacy distribution rules and the devastating common-law trap, the Estate Administration Tax calculation and the 180-day Estate Information Return deadline, the terminal tax return and CRA Clearance Certificate, and the closing sequence that protects the executor from personal liability.

Edge Cases, Worksheets, and Ready-Reference Appendices

A dedicated chapter on complications — insolvent estates, minor beneficiaries and the Office of the Public Guardian and Trustee, concurrent WSIB and SABS claims, digital assets, Indigenous and remote community considerations, and probate application rejections. Plus 7 standalone printable worksheets and reference cards: Command Centre setup worksheet, benefit claim sequencing tracker, EAT calculation worksheet, intestacy decision map, master deadline reference, master forms reference, and a key dollar figures card with every 2026 threshold in one place.

Who This Guide Is For

- The surviving spouse staring at a sudden income drop — whose household just lost a CPP retirement pension, an OAS payment, or both, and who needs to know exactly what the Survivor's Pension will actually pay after the combined cap, whether the Allowance for the Survivor applies (ages 60–64, up to $1,682.15/month), and which provincial programs offset the property tax and drug costs that now fall on one income

- The executor who inherited a filing cabinet, not a roadmap — who has been named estate trustee, is personally liable for every misstep, and needs the exact sequence of Service Canada notifications, CRA filings, probate applications, and distribution rules that prevents clawbacks, penalties, and personal exposure

- The family with no money for the funeral — who needs Ontario Works funeral assistance (up to $2,250) but will be denied if they pay the funeral home first, and who can also claim the $2,500 CPP Death Benefit without entering probate if no estate exists

- The common-law partner who assumed they would inherit — who qualifies for the CPP Survivor's Pension federally but inherits nothing under Ontario intestacy law, and who needs to understand the dependant's support claim and the proof-of-cohabitation requirements before a court deadline passes

- The adult child managing a parent's estate from another province — who needs to navigate Ontario's specific probate forms, EAT calculations, and ServiceOntario death certificate process without being physically present, and who needs to know which steps can be done remotely and which require a local agent

- The professional advising bereaved families — palliative social workers, end-of-life doulas, financial advisors, and junior paralegals who need a current, verified reference covering every 2026 threshold, form number, and dollar figure in one place

Why Free Resources Leave Money on the Table

The information exists. Service Canada publishes the CPP rules. ServiceOntario publishes the death certificate process. The Bereavement Authority publishes a 24-page consumer guide. Law firms publish articles on the Estate Administration Tax. None of them talk to each other, and none of them sequence the steps. Here is what that fragmentation actually costs you:

- Service Canada explains the CPP Survivor's Pension but never mentions the combined benefit cap clearly enough. Surviving spouses who are already receiving their own CPP retirement pension discover — weeks after filing — that the "survivor pension" they expected is reduced to almost nothing because the combined total cannot exceed the maximum single retirement pension. The Navigator shows you the exact math before you plan your budget around money that may not arrive.

- ServiceOntario explains the death certificate but never connects it to the 60-day CPP Death Benefit priority window. If you wait 8 weeks for the official provincial certificate before applying for the Death Benefit, the priority window has closed and the claim gets complicated. The Navigator tells you to use the Funeral Director's Proof of Death for CPP and order the official certificate in parallel.

- Municipal social services explain Ontario Works funeral assistance but never warn you about the pre-payment disqualification. The policy is clear in internal guidelines — if any money has been paid toward the funeral before the application is approved, the benefit can be denied on the grounds that the need has already been met. Families who put the funeral on a credit card expecting to be reimbursed discover this too late.

- Estate law firms explain the EAT but never connect it to the mandatory Estate Information Return. The tax is due as a deposit when you file for probate. The EIR is a separate filing, due within 180 days of the probate certificate being issued, to the Ministry of Finance. Missing either one creates penalties and personal liability for the estate trustee. The Navigator integrates both into one timeline.

Free resources give you pieces from agencies that operate in silos. The Benefit Recovery System connects every federal, provincial, and municipal step into one sequence — so you never miss a deadline, never trigger a clawback, and never leave money on the table because you didn't know it existed.

— Less Than a Single Death Certificate From ServiceOntario

The CPP Survivor's Pension alone can be worth over $10,000 per year. A missed 60-day Death Benefit window complicates a $2,500 claim. Filing for Ontario Works funeral assistance in the wrong order voids $2,250 in coverage. An unfiled Estate Information Return triggers penalties and personal liability for the executor. And a common-law partner who does not understand the Ontario intestacy gap can lose their entire claim to the estate.

Your download includes the complete 14-chapter guide covering every phase from the first 48 hours through estate distribution, three appendices (master deadline reference, master forms reference, key dollar figures), the printable Ontario Survivor Benefits Quick Start Checklist with 20 critical actions organized by urgency, and 7 standalone printable worksheets and reference cards — Command Centre setup, benefit claim sequencing tracker, EAT calculation worksheet, intestacy decision map, master deadline reference, master forms reference, and key dollar figures. Plus a 30-day money-back guarantee — if the Navigator does not give you clarity on what you are owed and confidence in the order of operations, email us for a full refund.

Not ready for the full guide? Download the free Ontario Survivor Benefits Checklist — covering the most time-sensitive actions across all four phases, the key dollar amounts, and the sequencing traps that cost the most when they catch you off guard. It is enough to know what to do first and what not to do yet.

The benefits do not arrive automatically. Nearly all of them must be claimed, most have deadlines, and several have traps. This Navigator makes sure you claim every one.