Service Canada Handles CPP. The Territory Handles the Pioneer Utility Grant. The WSCB Handles Workplace Deaths. Indigenous Services Handles Burial Assistance. And You Are Supposed to Figure Out Which Forms to File With Which Agency, in Which Order, Before the Deadlines You Were Never Told About Expire.

Someone you depended on has died in the Yukon, and now your household income has changed overnight. The CPP deposit that used to arrive on the third-last banking day of the month has stopped. The GIS and OAS that kept the bills manageable are still flowing into a bank account the branch just froze. The heating oil bill for a Whitehorse winter does not care that you are grieving. And the government websites that are supposed to help you replace the lost income are scattered across four separate agencies, each with its own forms, eligibility rules, and deadlines that nobody cross-references.

Here is what makes the Yukon different from every other jurisdiction in Canada. A surviving spouse in Ontario applies for CPP and moves on. A surviving spouse in the Yukon applies for CPP, then discovers the Pioneer Utility Grant has a strict July 1 to December 31 application window that closes whether you are ready or not. Then discovers that the Yukon Seniors Income Supplement pays up to $323.26 per month but is administered separately from the federal Allowance for the Survivor. Then discovers that Section 2(4) of the Home Owners Grant Act lets you claim the $500 senior property tax reduction rate even if you are under 65 -- but only if your deceased spouse previously qualified, and only if you know the rule exists. Then discovers that if the death was work-related, the Workers' Safety and Compensation Board provides a $15,000 tax-free lump sum, funeral costs up to $10,000, and a lifetime spousal pension -- but the claim expires 12 months from the date of death, and late applications are rejected outright.

Miss one deadline, apply to the wrong agency first, or fail to notify Service Canada before the next payment cycle, and the CRA claws back every overpayment from whatever is left of the estate.

The Yukon Survivor Benefits Navigator is a Benefit Recovery Roadmap -- built to replace the dozens of government tabs open on your browser with a single, chronological action plan that maps every federal pension, territorial grant, property tax break, health coverage continuation rule, and emergency funeral funding source available to surviving families in the Yukon Territory. Not a generic Canadian survivor benefits overview with "Yukon" pasted into the header. A day-by-day operational guide covering the specific forms, dollar amounts, eligibility thresholds, and agency contacts that apply to this territory and no other.

What's Inside the Benefit Recovery Roadmap

A complete 12-chapter guide and a Survivor Benefits Quick-Start Checklist -- covering every federal and territorial benefit available to surviving spouses, dependent children, and estate administrators in the Yukon:

The First 10 Days -- Immediate Actions That Prevent Financial Damage

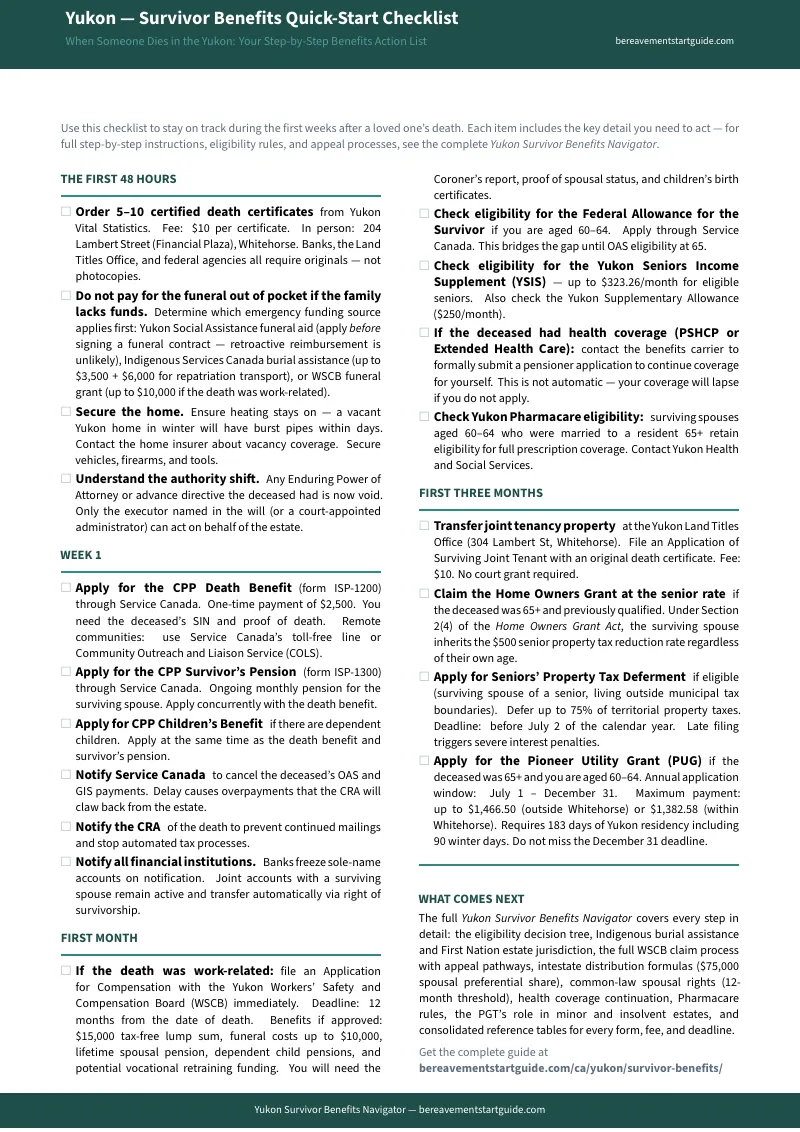

The moment someone dies in the Yukon, every Enduring Power of Attorney they granted is void. Joint bank accounts remain accessible, but sole-name accounts are frozen the instant you notify the bank. The guide maps the exact sequence for the first critical days: ordering five to ten certified death certificates from Yukon Vital Statistics at 204 Lambert Street ($10 each), notifying Service Canada to stop OAS and GIS before the CRA claws back overpayments, securing the home so a vacant property in a -40C winter does not end up with burst pipes and an insurance claim, and assembling the core documents -- SIN, marriage certificate, Notice of Assessment showing Line 23600 net income -- that every subsequent application demands.

The Eligibility Decision Tree

Not every surviving family qualifies for every program. The benefits available depend on who died, how they died, what they contributed to during their working life, and what territorial programs they were already enrolled in. Chapter 2 is a structured decision tree that tells you exactly which benefits apply to your situation -- workplace fatality (WSCB), senior spouse (PUG, YSIS, Pharmacare), Indigenous survivor (ISC burial assistance, self-governing First Nation programs), low-income family (Social Assistance funeral aid), veteran (Last Post Fund), or general (CPP and OAS). You stop reading about programs you do not qualify for and focus on the ones that put money back in your household.

Emergency Funeral Funding Sources

The funeral hits before any benefit has been applied for, often before the surviving family has legal access to the deceased's bank accounts. The guide maps every source available in the territory: Yukon Social Assistance funeral aid (but you must apply and receive approval before signing a contract with the funeral director -- apply afterward and the department will reject the claim), Indigenous Services Canada burial assistance (up to $3,500 plus up to $6,000 for repatriation transport to remote First Nation communities), WSCB funeral costs (up to $10,000 for workplace deaths), the Last Post Fund for veterans, and the bank Bond of Indemnity option that can release estate funds without a court order.

Federal Benefits -- CPP, OAS, and the Allowance for the Survivor

The largest ongoing income replacement most surviving spouses will receive comes through Service Canada. The CPP Death Benefit (form ISP-1200) pays a flat $2,500 to the estate. The CPP Survivor's Pension (form ISP-1300) provides an ongoing monthly payment for life. The Federal Allowance for the Survivor bridges the gap for spouses aged 60 to 64 who are not yet eligible for OAS. The GIS must be recalculated because the household shifted from couple to single status. Remote Yukon communities -- Faro, Haines Junction, Old Crow, Watson Lake -- have no Service Canada office, but the Community Outreach and Liaison Service (COLS) means you do not have to travel to Whitehorse. The guide covers every form, every eligibility rule, and the processing timeline so you know when to expect the first deposit.

Keeping the House Affordable -- Territorial Grants and Tax Deferrals

Heating a home through a Yukon winter costs thousands of dollars. The territory provides programs specifically designed to keep surviving spouses in their homes, but none are automatic. The Pioneer Utility Grant subsidizes home heating -- up to $1,382.58 within Whitehorse, up to $1,466.50 outside Whitehorse -- but the application window is July 1 to December 31. Miss December 31 and you forfeit the entire winter's subsidy. The Seniors' Property Tax Deferment lets you defer up to 75% of territorial property taxes, but you must file before July 2 or face severe interest penalties. And the Home Owners Grant spousal continuity rule under Section 2(4) lets a surviving spouse under 65 claim the $500 senior property tax reduction rate -- a provision so obscure that most people never learn it exists.

Health Insurance and Pharmacare Continuation

If you were covered as a dependent on the deceased's health plan, your coverage does not continue automatically. The Public Service Health Care Plan requires a formal pensioner application to the benefits carrier. Yukon Extended Health Care requires a coverage transfer. And the territorial Pharmacare program -- which covers the full cost of prescription medications -- has a spousal eligibility rule that lets surviving spouses aged 60 to 64 retain coverage even though they are years away from qualifying on their own. If you do not know to apply, your prescriptions stop being covered.

Workplace Fatality -- The Full WSCB Claim Process

If the death resulted from a workplace incident, the WSCB provides the most substantial survivor benefit package in the territory: the $15,000 tax-free lump sum, funeral costs up to $10,000, transport of remains within Canada, a lifetime spousal pension, dependent child pensions until age 19 (or 21 if in full-time education), and potential vocational retraining funding. The guide covers the complete claim process -- what documents to bring, the 12-month filing deadline, what happens if the claim is denied, and how to escalate to the independent Workers' Compensation Appeal Tribunal.

Indigenous Survivors -- First Nation Governance and Burial Assistance

Eleven of the fourteen Yukon First Nations are self-governing. This means the federal Indian Act does not automatically apply, and some First Nations have enacted their own estate and inheritance laws that may override the territorial Estate Administration Act. The guide covers the ISC burial assistance application, the self-governing First Nation contact process, the Supreme Court's mandatory First Nation Status Affidavit, and what happens when community laws supersede territorial statute.

Who This Guide Is For

- The surviving spouse whose household income just dropped -- who needs to transition from joint pension deposits to individual survivor benefits without missing the Pioneer Utility Grant window, the Federal Allowance application, or the Pharmacare coverage transfer that nobody told them was not automatic

- The adult child managing a parent's affairs from outside the territory -- living in Vancouver, Calgary, or Toronto with a few days of bereavement leave to figure out which agencies to call, which forms to file, and which deadlines cannot be missed before flying home

- The family with no money for the funeral -- who needs to know within 48 hours whether to apply to Yukon Social Assistance, Indigenous Services Canada, or the WSCB, and in what order, before the funeral director asks for a deposit

- The executor or power of attorney who was planning ahead -- managing a terminal diagnosis or cognitive decline, mapping out every benefit the surviving family will need to claim so nothing falls through the cracks when the death occurs

- The social worker or family helper coordinating benefits for a vulnerable client -- who needs a single reference document that consolidates every federal and territorial program instead of tracking information across a dozen agency websites

Why Free Resources Will Not Get You Through This

The information you need exists. It is scattered across Service Canada, the Yukon Department of Health and Social Services, the Workers' Safety and Compensation Board, Indigenous Services Canada, Veterans Affairs, the Yukon Public Legal Education Association, and eleven self-governing First Nation governments. Here is what you encounter when you try to claim every benefit using free sources alone:

- Service Canada operates in a strict federal silo. The Benefits Wayfinder tool mentions the Yukon Seniors Income Supplement but entirely fails to integrate the Pioneer Utility Grant, property tax deferrals, Pharmacare spousal eligibility, or the Home Owners Grant continuity rule. It covers federal programs and points vaguely at the territory for everything else.

- Yukon Health and Social Services publishes program pages, not project plans. The PUG page describes the grant. The Social Assistance page describes the funeral aid. Neither tells you how they interact with CPP timing, when to apply for one before the other, or what happens to your eligibility if you apply in the wrong sequence.

- The WSCB website covers workplace deaths only. It clearly states the $15,000 lump sum and the $10,000 funeral grant. But a surviving spouse whose partner died at work also qualifies for CPP, potentially for YSIS, and possibly for the PUG -- and the WSCB site does not cross-reference any of those. You would never know to apply.

- YPLEA publishes education, not execution. The Yukon Public Legal Education Association offers excellent overview PDFs about estates and wills. They explain concepts. They do not provide day-by-day checklists, tracking sheets, or chronological action plans for claiming benefits in the right order.

- National benefit calculators pretend the Yukon is Ontario. Willful and EstateExec reference CPP survivor pensions and national programs. They miss the Pioneer Utility Grant entirely, do not mention the $323.26 YSIS supplement, and have no idea that Section 2(4) of the Home Owners Grant Act exists. They are template products with "YT" dynamically inserted.

Free resources give you fragments from a dozen agencies that never reference each other, and not one of them connects the CPP timeline to the PUG deadline to the Pharmacare transfer to the WSCB claim window in the same document. The Benefit Recovery Roadmap puts every federal pension, territorial grant, emergency funding source, health coverage rule, and property tax break into one guide -- in the order your household actually needs them.

-- Less Than 15 Minutes of a Whitehorse Lawyer's Time

A single consultation with a Whitehorse estate or benefits lawyer costs $350 or more per hour -- and that consultation will not come with a chronological checklist of every deadline, a decision tree for determining which programs apply to your situation, or a consolidated reference table with every form number and agency contact in the territory. National benefit advisory services charge $150 to $200 per session. This guide costs less than fifteen minutes of professional time and gives you the complete Yukon-specific benefit recovery system for every federal pension, every territorial grant, every emergency funding source, and every health coverage continuation rule.

Your download includes the complete guide, the Yukon -- Survivor Benefits Quick-Start Checklist, and five standalone printable tools: an Eligibility Decision Tree covering all six benefit scenarios, an Emergency Funeral Funding reference with every source and contact, a Territorial Grants Deadline Tracker for the PUG window and property tax dates, a WSCB Workplace Claim Guide for workplace fatality benefits, and Quick Reference Tables with every form, fee, deadline, and agency contact in the territory. Plus a 30-day money-back guarantee. If the guide does not give you clarity on which benefits to claim and confidence that you are claiming them in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Yukon -- Survivor Benefits Checklist covering the most critical actions for the first 48 hours, the first week, the first month, and the first three months -- enough to get oriented and make sure you do not miss the deadlines that cost families the most money.

You did not ask for this responsibility. But the money your family is entitled to is real, the deadlines are fixed, and the forms are finite. The guide shows you which ones to file, in which order, with which agency -- so nothing expires while you are still figuring out where to start.