You're dealing with the Probate Registry, HMRC, HM Land Registry, and every bank's bereavement team — all at once, while grieving

After a death in England, the administrative machinery starts immediately. Bank accounts freeze. Direct debits cancel. HMRC's clock starts running from the date of death — not from when you feel ready. And buried inside the English system are procedural traps that catch even careful executors: a probate application fee jumping 75% to £526 in July 2026, bank thresholds that range from £5,000 to £50,000 with no single published list, and an HM Land Registry form system where choosing the wrong form triggers a 15-working-day requisition that can cancel your entire application.

The free government pages tell you each step exists. They don't tell you what order to do things in, which deadlines run concurrently, or where the traps are hiding. GOV.UK fragments the process across dozens of nested pages. HM Land Registry's Practice Guides are written for conveyancing solicitors. And the law firm blogs that rank on Google? They deliberately withhold the final procedural steps to push you toward £2,000–£6,000 retainers.

The Executor's Settlement Sequencer — every form, every deadline, every trap, in the order they actually happen

The Estate Settlement Guide for England turns fragmented government websites into a single chronological roadmap. It walks you through every step — from the first 48 hours through to final distribution — with the specific forms, fees, phone numbers, and deadlines that apply in England and Wales.

This isn't a list of links. It's what we call the Executor's Settlement Sequencer — a chronological administrative playbook that maps the Medical Examiner system, the Probate Registry, HMRC reporting routes, HM Land Registry forms, and bank bereavement teams into the exact order you need to deal with them. Generic UK guides skip the operational detail. This guide was built around it.

What's inside

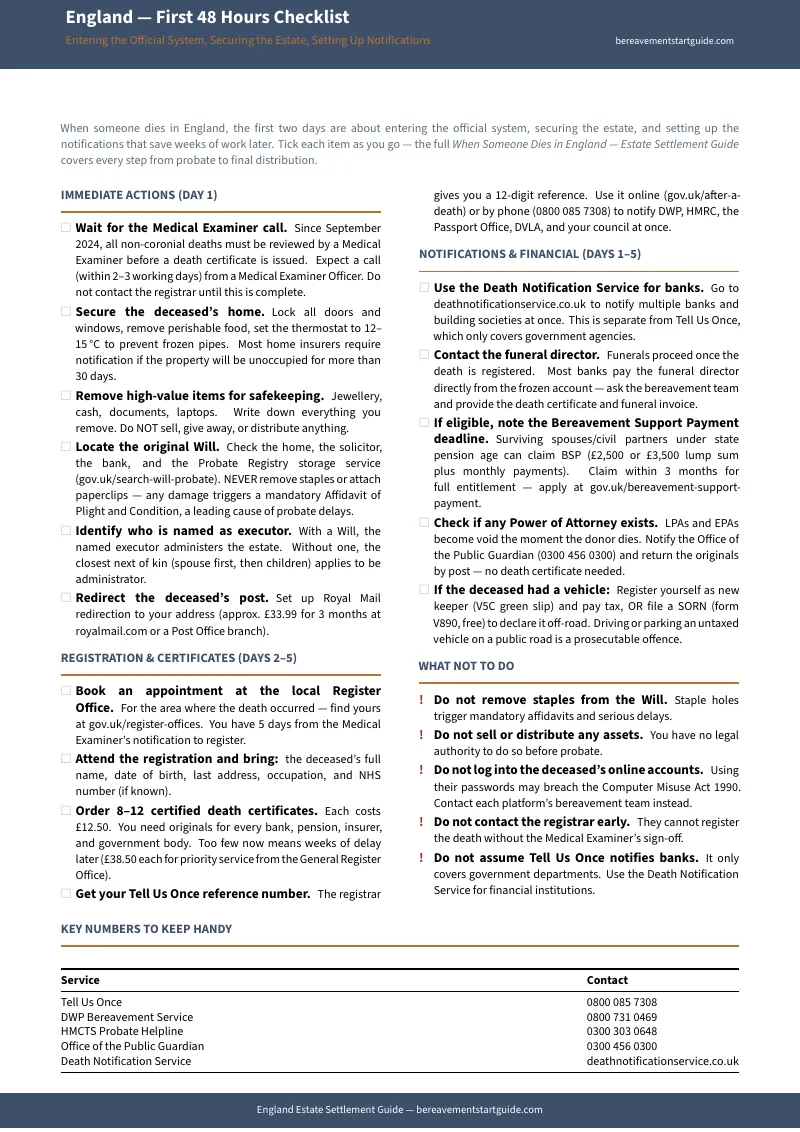

- The 48-hour triage checklist — what must happen before the registrar appointment (Medical Examiner call, securing the property, locating the Will), what can wait, and the critical home insurance notification if the property will be unoccupied for more than 30 days

- Death certificate ordering strategy — why you need 8–12 copies at £12.50 each, how under-ordering creates weeks of delays via the GRO, and why the £38.50 priority service exists for executors who got it wrong

- Tell Us Once vs. Death Notification Service — the exact boundary between government agencies (DWP, HMRC, DVLA, Passport Office) and commercial entities (banks, insurers, utilities), because assuming Tell Us Once covers banks is the most common and most expensive mistake families make

- The 2026 bank threshold matrix — every major UK bank's internal probate limit in one table: Barclays, NatWest, Santander, and Lloyds at £50,000; Yorkshire and Skipton at £30,000; Principality at £15,000; NS&I and Revolut as low as £5,000 — plus the mechanism for releasing funeral funds directly to the funeral director before probate is granted

- Probate application walkthrough — PA1P (with Will) and PA1A (without Will) form-by-form instructions, the IHT421 timing trap (submit too early and your application gets stopped for 15–20 weeks), and the £526 fee effective July 2026

- Inheritance tax reporting routes — the excepted estate shortcut, the £325,000 nil-rate band, the residence nil-rate band, the spouse exemption, and the IHT400 long-form process for estates above the threshold

- HM Land Registry form decision tree — Joint Tenants use DJP (free, 2–4 weeks). Tenants in Common or sole name use AP1 + AS1 (transfer to beneficiary) or AP1 + TR1 (sale to third party). Get this wrong and you face a formal requisition with a 15-working-day deadline before the application is cancelled

- Executor personal liability shield — Section 27 Trustee Act 1925 Gazette notices, beneficiary bankruptcy searches, and the two-month creditor window that protects you from personal financial liability when unknown creditors emerge after distribution

- Intestacy calculator — the £322,000 statutory legacy for the surviving spouse, the division formula for the remainder among children, and the complete beneficiary hierarchy when there is no Will

- Digital assets protocol — email accounts, social media memorialisation, cryptocurrency, and subscription cancellation — with the legal constraints on accessing password-protected accounts

- Benefits and financial support — Bereavement Support Payment (£3,500 lump sum + up to 18 monthly payments), Funeral Expenses Payment eligibility, and the DWP notification timeline to prevent overpayment clawbacks

- Agency Notification Tracker — a printable master list of every organisation you need to contact, with reference numbers, contact details, and completion checkboxes

- Key forms reference — every form mentioned in the guide with its purpose, where to get it, and filing deadlines in one reference table

Plus 10 standalone printable worksheets and reference cards — each designed to be printed separately and used at your desk, at the bank, or at the Probate Registry: Agency Notification Tracker, Bank Threshold Matrix, Probate Pre-Submission Checklist, Asset and Liability Inventory, Beneficiary Communication Log, Land Registry Decision Tree, Intestacy Calculator, Executor Liability Shield, Estate Settlement Timeline, and Executor's Decision Flowchart.

Who this is for

- Adult children named as executor who have limited bereavement leave, no legal training, and need to know exactly what to do and in what order — without spending weeks deciphering GOV.UK

- Surviving spouses who need to access joint accounts, transfer the property via right of survivorship, and secure household finances within days of the death

- Budget-conscious executors who want to handle probate themselves rather than pay a solicitor 1–3% of the estate value (often thousands of pounds) — and need a guaranteed DIY pathway that won't get rejected

- Remote or overseas family members managing an English estate from another city or country — who need to understand digital applications, postal processes, and remote oath-swearing

- Anticipatory caregivers preparing now for an elderly parent's eventual death — building the asset inventory, understanding property ownership structures, and setting up Lasting Powers of Attorney while there's still time

Why not just use the free government pages?

The government pages are accurate — they're just scattered across dozens of disconnected agencies, each written in clinical language, and none of them warn you about the traps.

GOV.UK explains that you need to apply for probate but doesn't tell you that submitting before HMRC processes the IHT421 will stop your application for 15–20 weeks. HM Land Registry publishes the forms but assumes you already know whether the property is Joint Tenants or Tenants in Common — and getting this wrong triggers a formal requisition. Citizens Advice and Age UK provide empathetic overviews but redirect you to a solicitor for anything beyond the basics. And law firms like Farewill and Co-op Legal Services publish just enough free content to create anxiety before funnelling you toward packages starting at £1,679.

This guide connects the dots. It's the difference between reading a map of each individual street and having turn-by-turn directions for the whole journey.

The cost of not knowing

The financial traps in English estate administration are substantial:

- Ordering too few death certificates and paying £38.50 per priority reorder — when ordering the right number upfront costs £12.50 each

- Having a probate application stopped for a preventable error and waiting 15–20 additional weeks while assets remain frozen

- Distributing the estate without Section 27 Gazette notices and becoming personally liable when an unknown creditor surfaces

- Paying a solicitor £2,000–£6,000 for straightforward probate work that most executors can complete themselves with the right instructions

- Using the wrong Land Registry form and having your property transfer application cancelled after 15 working days

- Missing the boundary between Tell Us Once and commercial notifications — and discovering months later that the deceased's bank accounts were still accruing charges

The guide costs a fraction of any single one of these mistakes.

— less than a single hour of a probate solicitor's time

Every probate solicitor in England charges more per hour than the entire cost of this guide. The Executor's Settlement Sequencer gives you the administrative playbook to handle the estate yourself — and tells you exactly when a solicitor is genuinely needed, so you only pay for the moments that require one.