You Filed the Probate Application Before the 20-Working-Day Window Closed. HMCTS Stopped It. Now You're in the 15-Week Paper Queue Instead of the 4-Week Digital One.

You thought you were being efficient. You valued the estate, filled in the IHT400 with its schedules, paid the Inheritance Tax using the IHT423 Direct Payment Scheme, and submitted the probate application online the same week. Four to five weeks, the government website said. Then nothing happened. After three weeks of silence you called HMCTS and learned the application had been automatically stopped — because HMRC and the Probate Registry need exactly 20 working days to synchronise their systems after an IHT400 is filed, and you applied too early. Your application is now in the "stopped" pile, where processing times run 15 to 16 weeks instead of 4. The bank accounts stay frozen. The house can't be sold. The beneficiaries are asking why nothing is moving.

That one sequencing error — applying before the 20-working-day sync window closed — just added three months to the process. And the worst part is that no page on GOV.UK tells you this clearly enough to prevent it. The information exists, buried across multiple guidance pages, but the critical dependency between the HMRC submission date and the HMCTS application date is never laid out as what it actually is: a hard countdown you must diarise and respect.

The England Probate Process Guide is an Estate Settlement Roadmap for every filing, fee, deadline, and decision in an English probate case — from the Medical Examiner's call through final distribution and estate closing. Not a generic UK overview that conflates England with Scotland's Confirmation system. Not a blog post written by a solicitor's marketing team to convince you that self-representation is irresponsible. A plain-English, England-specific manual that tells you exactly what GOV.UK does not: which steps depend on which, which forms trigger which processes, which traps cause stops, and which estates do not need probate at all.

What's Inside the Estate Settlement Roadmap

A 12-chapter step-by-step guide and a quick-start checklist — covering every phase of probate in England from the first phone call through final distribution, built on the current HMCTS procedures, HMRC requirements, and the 2026 fee changes:

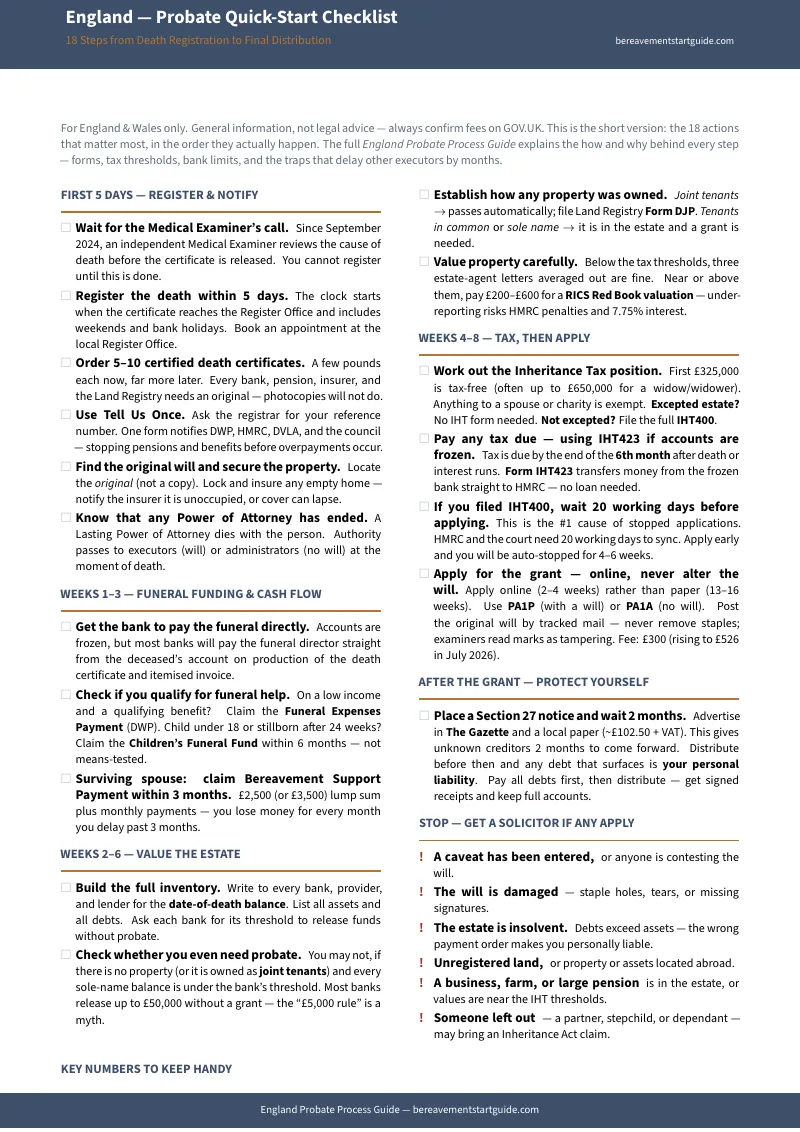

Before You Apply: Does the Estate Actually Need Probate?

This is the question that determines whether you spend months in the court system or weeks completing a simpler process. England does not have a single probate threshold — the requirement depends on which institutions hold the deceased's assets, how much each one holds, and how the property was owned. Barclays, Santander, NatWest, and Nationwide all release sole-name balances up to £50,000 on a signed indemnity without a grant. NS&I triggers at £5,000 to £15,000 depending on the circumstances. If the deceased's only significant asset is a jointly held property, you may not need probate at all — a Land Registry Form DJP transfers the title on a death certificate alone. The guide includes the bank-by-bank threshold matrix and a three-check decision tree that maps every scenario, so you do not file a £300 probate application (rising to £526 in July 2026) for an estate that could have been settled with phone calls and indemnity forms.

The Medical Examiner System and the 5-Day Registration Deadline

Since September 2024, the process of registering a death in England changed fundamentally — and most online guides have not caught up. An independent Medical Examiner now reviews every death before the certificate is released, and the Medical Examiner's office phones the family as part of the process. You cannot register the death until this step completes. The 5-day registration deadline includes weekends and bank holidays. The guide walks you through the new sequence, explains what the Medical Examiner call covers, and tells you exactly how many certified death certificates to order (5 to 10 — a few pounds each now, far more later, and every bank, insurer, pension provider, and the Land Registry needs an original).

The Cash-Flow Crisis: Frozen Accounts, Funeral Bills, and the IHT423

The deceased's sole-name bank accounts freeze the moment the bank learns of the death. The funeral bill arrives weeks before you have a grant. Then the Inheritance Tax is due — and you cannot access the money to pay it without the grant you cannot get until the tax is paid. This is the catch-22 that blindsides every first-time executor. The guide covers all three solutions: how to get the bank to pay the funeral director directly from the frozen account, how Form IHT423 (the Direct Payment Scheme) transfers money straight from the frozen bank to HMRC to pay the tax, and which DWP benefits — Funeral Expenses Payment, Children's Funeral Fund, Bereavement Support Payment — provide immediate cash-flow support. The IHT423 alone saves families from taking out bridging loans against the estate.

The Valuation Trap: RICS Reports, Estate-Agent Letters, and the 7.75% Interest Risk

Property valuation is the single biggest financial risk for a lay executor. Get it wrong in either direction and you pay for the mistake. Under-report and HMRC's District Valuer Service challenges the figure — the estate faces penalties and interest at 7.75% on the underpaid tax. Over-value and you drag the estate into a 40% tax charge on the excess. The guide explains when three estate-agent letters (free) are defensible and when you must pay £200 to £600 for a RICS "Red Book" valuation, how to claim the tenants-in-common discount that HMRC accepts but does not advertise (typically 10–15%, which on a £300,000 half-share saves thousands), and how the gross-value calculation works for fee purposes — mortgages and debts are ignored, so the court fee is based on the full property value, not the equity.

Inheritance Tax: Excepted Estates vs. the IHT400

Since January 2022, the old IHT205 short form has been abolished. Estates now fall into exactly two categories: excepted (the simpler route, where you report values inside the probate application itself) and non-excepted (where you must complete the full IHT400 and its supplementary schedules — IHT405 for property, IHT406 for bank accounts, IHT409 for pensions, and others). Roughly one in three IHT400 applications are queried or rejected for errors. The guide explains the excepted-estate rules (including the foreign-asset and trust-asset triggers that disqualify you even when no tax is due), walks through the nil-rate band, the residence nil-rate band, the transferred allowances for widows and widowers, and the spouse and charity exemptions — and tells you exactly which schedules to complete for your estate's specific asset mix.

The 20-Working-Day Rule and the "Stop" Pile

This is the single most important sequencing rule in English probate, and the one most frequently violated by executors who think they are being efficient. If you filed an IHT400, you must wait exactly 20 working days after HMRC confirms receipt before submitting your probate application to HMCTS. Apply a day early and the systems find no matching tax record — your application is automatically stopped and joins a queue where processing times run 15 to 16 weeks instead of 4 to 5. There is no shortcut and no appeal. The guide makes this dependency unmissable: diarise the HMRC confirmation date, count 20 working days, and only then apply.

The Probate Application: Online vs. Paper, PA1P vs. PA1A, and the Staple Trap

Online applications clear in 4 to 5 weeks. Paper applications take 13 to 16 weeks. The choice is not always yours — certain complex estates (applying through an attorney, resealing a foreign grant) are paper-only — but for most estates, the digital route is dramatically faster. The guide covers both pathways: PA1P (with a will) and PA1A (no will), the documents you must post with the application, the fee (£300, rising to £526 in July 2026), the Help with Fees scheme for low-income applicants, and the forensic handling of the original will. HMCTS examiners are trained to spot indentations, rust marks, and pinholes as signs of tampering. A will that arrives with unexplained staple holes gets stopped, and you will be asked for an Affidavit of Plight and Condition — a sworn legal statement explaining the damage. The guide tells you how to handle, store, and copy the will without triggering this.

Renunciation vs. Power Reserved: The Decision That Cannot Be Undone

When a named executor does not want to act, there are two options — and choosing the wrong one is permanent. Form PA15 (renunciation) permanently gives up the role and cannot be reversed. Power Reserved lets an executor step aside temporarily while keeping the right to step back in later. The guide explains the critical difference, the "intermeddling" rule that locks you in if you have already started acting, and why renunciation by mistake costs the estate flexibility it can never get back.

After the Grant: Section 27, Creditor Protection, and Safe Distribution

The sealed grant gives you legal authority, but this final stretch is where executors most often expose themselves to personal financial liability. The guide covers the Section 27 Gazette notice (~£102.50 + VAT) that gives unknown creditors 2 months to come forward, why distributing before the 2-month window closes means you pay unexpected debts out of your own pocket, the intestacy distribution rules (the surviving spouse takes the first £322,000 plus half the remainder — unmarried partners and stepchildren inherit nothing automatically), and the final accounts and clearance receipts that formally end your personal liability as executor.

Who This Guide Is For

- The executor who just learned the accounts are frozen — who needs to understand that a will is legally inert until the court validates it, and that the process between "holding the will" and "having legal authority" involves tax forms, a mandatory waiting period, and court fees that nobody mentioned at the funeral

- The surviving spouse whose only concern is keeping the family home — who may not need probate at all if the property is held as joint tenants, and needs to know the exact difference between a free Land Registry Form DJP and a £300+ probate application before making the wrong choice

- The family managing an estate near the IHT thresholds — who needs to understand the valuation trap, the District Valuer risk, the tenants-in-common discount, and the difference between excepted and non-excepted estates before filing anything with HMRC

- The executor who assumed everything was digital now — who applied online, then discovered the original will must still be posted by tracked mail to the Probate Registry, that staple holes trigger sworn affidavits, and that the court fee is about to jump 75% to £526

- The adult child managing a parent's estate with siblings demanding updates — who needs an authoritative timeline to communicate to the family: how long each stage takes, what causes delays, when distribution can legally begin, and why jumping the 20-working-day window turns a 4-week process into a 4-month one

- The reluctant executor trying to decide whether to renounce — who needs to understand the permanent consequences of Form PA15 versus the flexibility of Power Reserved before signing anything, and the intermeddling rule that can trap them in the role

Why Free Resources Will Not Get You Through This

English probate information exists. It is scattered across GOV.UK, HMCTS guidance pages, HMRC forms and instructions, HM Land Registry practice guides, bank bereavement portals, and dozens of law firm blogs. Here is what you actually encounter when you try to navigate probate using free sources:

- GOV.UK is authoritative, fragmented, and deliberately neutral to the point of unhelpfulness. The application portal is there. The IHT400 schedules are there. The fee table is there. But the critical dependencies — the 20-working-day sync rule, the interaction between HMRC submission and HMCTS application, the fact that excepted-estate reporting happens inside the probate form rather than on a separate tax return — are spread across dozens of disconnected guidance pages. GOV.UK explicitly states it cannot provide advice on individual circumstances, which in practice means it will not tell you which path applies to your estate or what sequence to follow.

- Law firm blogs are accurate, detailed, and engineered to sell you representation. Farewill, Co-op Legal Services, and every high-street solicitor publish guides that correctly identify the IHT400, the PA1P, and the staple trap. Every one of them stops short of execution details. They explain the 20-working-day rule — then end with "our probate team can handle this for you." They explain the valuation risk — then end with "contact us for a fixed-fee quote." The goal is to make the process look dangerous enough that you pay £1,000 to £5,000 for representation, or accept a percentage-of-estate fee that can reach £20,000 on a typical property.

- Citizens Advice covers the basics — and only the basics. Their probate pages explain what a grant is, what an executor does, and that you should apply online. They do not cover the IHT400 schedules, the excepted-estate classification, the 20-working-day sync, the bank threshold matrix, or any of the sequencing dependencies that determine whether your application takes 4 weeks or 16. Useful for the first ten minutes of research; insufficient for actually doing the job.

- Solicitors charge 1% to 5% of the gross estate plus VAT. On a house and savings worth £400,000, that is £4,000 to £20,000 — for following the same steps this guide teaches you. Percentage-based fees are calculated on gross value (not equity), so the mortgage is irrelevant. Some firms offer fixed fees of £1,000 to £3,000 for straightforward estates, but "straightforward" is defined by the solicitor after you have paid the initial consultation.

Free resources give you fragments from a dozen government websites that do not reference each other, do not sequence the steps, and do not warn you about the dependencies that cause stops. The Estate Settlement Roadmap puts every HMCTS requirement, HMRC form, fee schedule, and bank threshold into one document, in the order you actually need them.

— Less Than Thirty Minutes With a Probate Solicitor

A consultation with a probate solicitor in England runs £200 to £400 per hour. Full probate representation on a percentage basis costs £4,000 to £20,000 on a typical estate. Even a "fixed fee" service starts at £1,000 for a straightforward case. This guide costs less than thirty minutes of professional legal time and gives you the complete England-specific probate roadmap — every form, every filing requirement, every fee, the bank threshold matrix, the IHT classification decision tree, the 20-working-day countdown, and the property transfer instructions that tell you whether you need the court at all.

Your download includes 7 printable PDFs: the complete 12-chapter step-by-step guide, the standalone England Probate Quick-Start Checklist with 18 action items across five stages, plus five standalone tools — the Bank Threshold Matrix, the IHT Classification Decision Tree, the Probate Pre-Submission Checklist, the Forms & Fees Quick Reference, and the 20-Day Countdown Tracker. Instant download, no account required.

30-day money-back guarantee. If the guide does not give you clarity on what to file, when to file it, and what sequence to follow so your application clears in weeks rather than months — email us for a full refund. No questions asked.

Not ready for the full guide? Download the free England Probate Quick-Start Checklist — an overview of the probate process, the key deadlines, the critical sequencing warnings, and the three-check decision tree for determining whether you need probate at all. Enough to understand what you are facing and whether you need the full guide.

Probate is not something you were trained for. But it is something you can get through with the right instructions — and without handing a percentage of the estate to someone who will follow the same steps this guide teaches you.