The benefits are there. The deadlines are running. And nobody hands you a single list of what to claim.

When your spouse or partner dies in England, the government doesn't send you a letter explaining what you're owed. Instead, it buries your entitlements across the DWP, HMRC, your local council, HM Land Registry, and dozens of private pension providers — each with its own forms, its own eligibility rules, and its own deadlines. Miss the Bereavement Support Payment window by a single day and you lose up to £9,800 in tax-free payments. Fail to apply for the Council Tax Class F exemption and your local authority charges you full rates on an empty property. Leave the State Pension inheritance question unanswered and you forfeit income for the rest of your life.

GOV.UK tells you each benefit exists — on separate pages, in separate departments, with no indication of which deadlines overlap or which claims unlock others. The charity guides provide emotional support and high-level summaries. The solicitors charge £2,000-£15,000 for estate administration and deliberately hold back the procedural detail that would let you do it yourself. And the DWP's own forms assume you already know the difference between a pre-2016 Additional State Pension and a post-2016 Protected Payment — which almost nobody does.

The Benefits Claim Sequencer — every entitlement, every deadline, every form, mapped to your timeline

The England Survivor Benefits Navigator pulls every financial entitlement available to bereaved families in England into a single chronological system. It covers the full landscape — DWP payments, pension inheritance, property tax relief, funeral funding, industrial death compensation, and the private-sector notifications that Tell Us Once leaves out — and organises them by the order you actually need to act.

We call it the Benefits Claim Sequencer. Instead of jumping between GOV.UK pages and hoping you haven't missed something, you work through one document that tells you what to claim, when to claim it, what forms to use, and what evidence each agency needs. Generic UK bereavement guides mention that benefits exist. This guide was built around the operational detail of actually claiming them.

What's inside

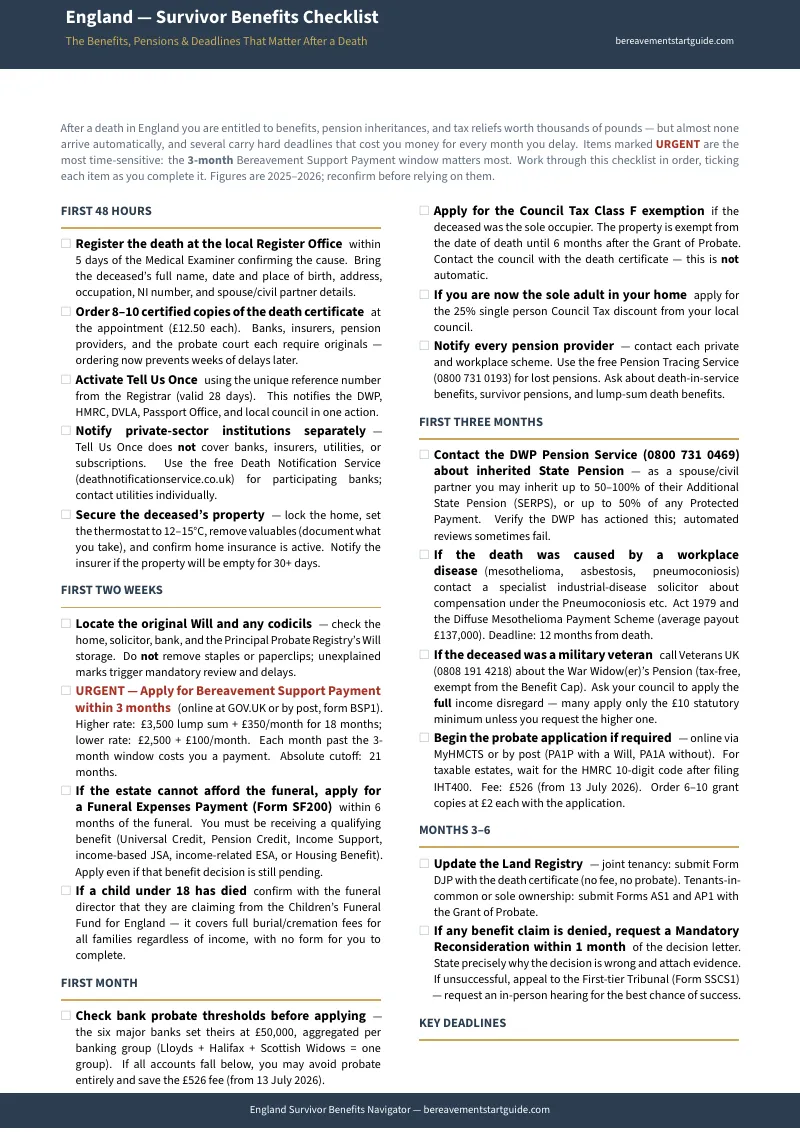

- Bereavement Support Payment claim guide with the 3/12/21-month deadline cliff — the full lump sum (£2,500 or £3,500 depending on dependent children) plus 18 monthly payments worth up to £9,800 total. Claims filed after 3 months receive reduced payments. Claims after 21 months are rejected entirely. The guide walks you through the SF200 form, the evidence requirements, and the cohabiting partner eligibility rules that changed in 2023

- Bank probate threshold directory with aggregation rules — every major UK bank's internal limit in one table (Barclays, NatWest, Santander at £50,000; Yorkshire and Skipton at £30,000; Principality at £15,000; NS&I as low as £5,000). Critically: the threshold applies per banking group, not per account. Halifax, Lloyds, and Scottish Widows aggregate against a single £50,000 limit. Understanding this can save you the £526 probate application fee entirely

- State Pension inheritance decision tree — the rules depend on whether the deceased reached pension age before or after 6 April 2016, and they are genuinely complex. Pre-2016 survivors may inherit up to 50% of the Additional State Pension, Graduated Retirement Benefits from 1961-1975, and Protected Payments. Post-2016 survivors inherit under different transitional rules. The guide replaces the DWP's scattered web pages with a single visual decision tree that tells you exactly what applies to your situation

- Council Tax Class F exemption walkthrough — when a sole occupant dies, the property qualifies for a full Council Tax exemption through probate and up to six months after the Grant is issued. This is not automatically applied. You must contact your local authority, submit the death certificate, and provide evidence of your executor status. The guide gives you the application steps and the follow-up protocol if the exemption is refused

- Land Registry Form DJP and AS1/AP1 walkthroughs — if the property was held as joint tenants, a single Form DJP with the death certificate removes the deceased from the title (no probate needed). If held as tenants in common or in the deceased's sole name, you need Form AS1 (assent to beneficiary) and Form AP1 (application to change the register). The guide includes a diagnostic to determine which forms apply and step-by-step completion instructions for each

- Private-sector notification checklist — Tell Us Once handles DWP, HMRC, DVLA, the Passport Office, and local councils. It does not touch banks, building societies, mortgage lenders, private pension providers, utility companies, broadband providers, or digital subscriptions. The guide provides a printable checklist of every private-sector organisation you need to notify separately, with contact details and the documents each one requires

- Funeral cost support — DWP Funeral Expenses Payment eligibility criteria and SF200 form instructions, the non-means-tested Children's Funeral Fund for under-18s, and the Universal Credit bereavement run-on that maintains your existing joint-claim benefit levels for three assessment periods after the death

- Industrial disease and workplace death compensation — the Diffuse Mesothelioma Payment Scheme (DMPS) pays lump sums to dependants of asbestos disease victims, with average payouts around £137,000. Claims must be filed within 12 months of the death. Industrial Injuries Disablement Benefit (IIDB) dependant claims also have strict deadlines. Awareness of these schemes is extremely low — the guide covers eligibility, forms, and timelines

- War Widow(er)'s Pension and Armed Forces compensation — eligibility rules, current payment rates, and application pathways for families of service personnel and veterans whose death was caused or hastened by military service

- Appeals and Mandatory Reconsideration pathway — if the DWP denies your claim, you have one month to request a Mandatory Reconsideration. If that fails, you can appeal to the Social Security Tribunal. The guide covers the process step by step, including what additional evidence strengthens your case and the realistic timelines for each stage

- Master deadline calendar — a single-page visual timeline showing every benefit deadline running from the date of death: 3 months (BSP maximum), 12 months (DMPS/IIDB dependant claims), 21 months (BSP absolute cutoff), and the ongoing windows for pension inheritance and Council Tax claims. Print it and pin it up

- Claim tracker worksheet — a printable tracking sheet for every benefit and notification, with columns for reference numbers, submission dates, expected processing times, and follow-up dates

Plus standalone printable worksheets and reference cards — each designed to be printed separately and used at your desk, on a call with the DWP, or at the bank: Benefits Deadline Calendar, BSP Eligibility Checklist, Bank Threshold Quick Reference, State Pension Decision Tree, Council Tax Exemption Application Checklist, Private-Sector Notification Tracker, and Claim Status Log.

Who this is for

- Surviving spouses and civil partners who need to replace lost household income, understand what benefits they're entitled to, and avoid permanently forfeiting payments by missing deadlines they didn't know existed

- Cohabiting partners who became eligible for Bereavement Support Payment under the 2023 rule change but aren't sure whether they qualify or how to prove the relationship to the DWP

- Adult children acting as executor who need to claim benefits on behalf of the estate, notify private institutions that Tell Us Once missed, and handle bank accounts that sit below probate thresholds

- Low-income families facing a funeral cost crisis — average funeral costs in England exceed £4,100, and the DWP's Funeral Expenses Payment has complex eligibility rules and estate deduction calculations that determine what you actually receive

- Dependants of workers who died from industrial disease or workplace injury — the DMPS and IIDB dependant schemes are high-value and have strict 12-month claim deadlines, yet awareness remains remarkably low

- Anticipatory carers preparing for a terminally ill partner's death — understanding what happens to Carer's Allowance (the 8-week run-on), how the LPA ceases to function at the moment of death, and which benefit claims can be prepared in advance

Why not just use the free government pages?

The government pages are accurate — they're scattered across the DWP, HMRC, local council websites, and HM Land Registry, with no cross-referencing and no indication of which deadlines run concurrently.

GOV.UK explains that Bereavement Support Payment exists but doesn't tell you that the 3-month deadline for maximum payments is measured from the date of death, not from when you register the death or feel ready to apply. The DWP's State Pension inheritance pages spread the pre-2016 and post-2016 rules across multiple interlinked pages that presume you already understand the pension tier structure. Citizens Advice and Age UK provide compassionate overviews but direct you to a solicitor or the DWP helpline for anything specific. And the solicitor blogs publish enough complexity to generate anxiety without ever providing the forms, checklists, or step-by-step instructions that would let you handle it yourself.

This guide connects the scattered pieces into a single sequence. It's the difference between knowing benefits exist and actually claiming them before the deadlines expire.

The cost of not knowing

The financial consequences of missing benefit deadlines in England are permanent:

- Filing for Bereavement Support Payment after 3 months reduces your payments — filing after 21 months means you get nothing from a benefit worth up to £9,800

- Paying the £526 probate application fee when the estate sits below bank thresholds that would have released the funds without probate

- Paying full Council Tax on a property that qualifies for a Class F exemption — because your council didn't tell you the exemption exists and won't apply it automatically

- Missing the 12-month DMPS deadline for an industrial disease claim that could be worth over £100,000 to the deceased's dependants

- Leaving State Pension inheritance unclaimed because the pre-2016 transitional rules were too confusing to navigate without guidance

- Discovering months later that the deceased's bank accounts, insurance policies, and subscriptions were still active — because Tell Us Once doesn't cover the private sector

The guide costs a fraction of any single one of these losses.

— less than a single death certificate

At £12.50 per certified death certificate copy, you'll spend more on the paperwork the banks require than on the guide that tells you how to claim everything your family is owed. The Benefits Claim Sequencer gives you the complete system — every entitlement, every form, every deadline — so nothing expires while you're still figuring out where to start.