"Zero Estate Tax" Is the Most Expensive Misunderstanding in New Mexico

You read it everywhere, and it's true: New Mexico has no estate tax and no inheritance tax. So you breathe out. You assume the tax part of settling your mother's estate — or your late husband's — is handled the moment you file the final 1040.

And then, months later, a letter arrives from the New Mexico Taxation and Revenue Department. Failure-to-file penalties. Interest. On a return you didn't know existed, for income the estate earned after the death — rent on the house waiting to sell, dividends, a few months of interest in the estate account. The money to pay it comes out of what your family was supposed to inherit.

That's the trap. New Mexico's tax bureaucracy doesn't punish you for owing money. It punishes you for not knowing which form to file — and "no estate tax" is precisely the phrase that lulls grieving executors into missing the one return that actually applies.

The Problem Isn't That the Forms Are Hidden. It's That Nobody Will Tell You the Order.

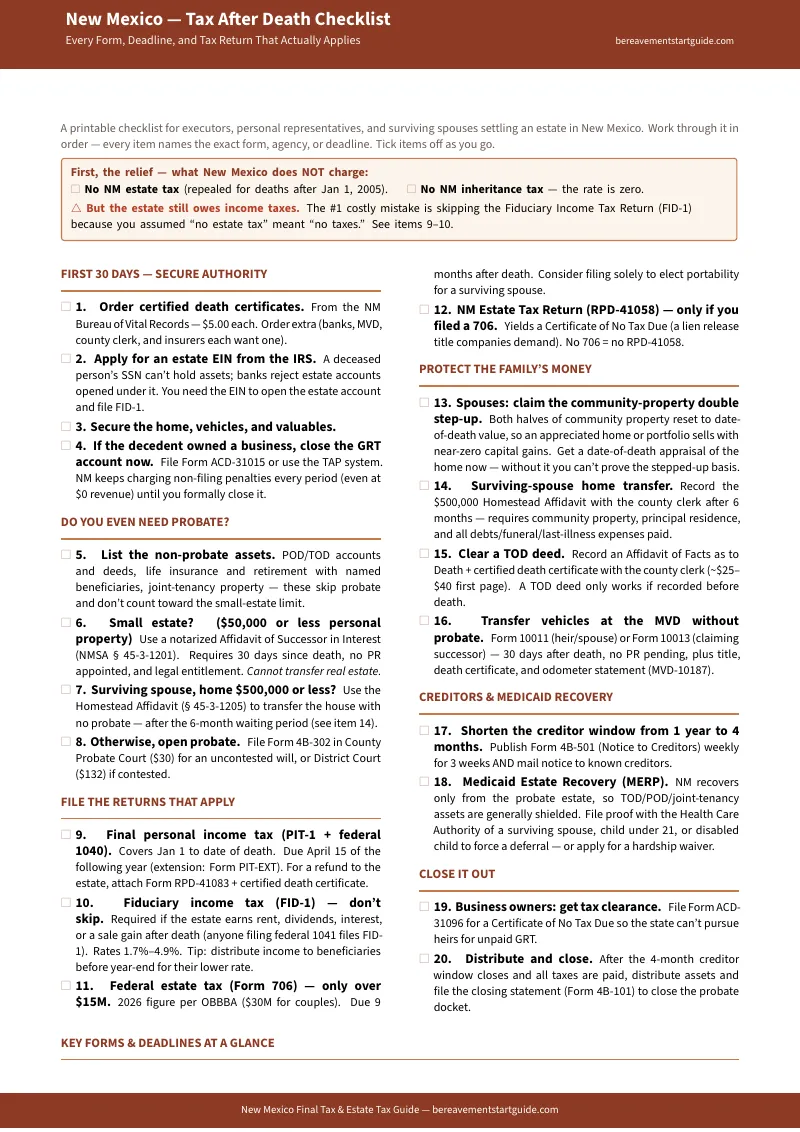

The FID-1, the RPD-41058, the PIT-1, the small-estate affidavit — all of it is free to download from nmcourts.gov and tax.newmexico.gov. The state hands you the blank forms and, by law, refuses to tell you anything else. The county clerk will say it out loud: "We can't give legal advice."

So you're left between two bad options. On one side, free government PDFs written in statutory jargon, with no sequence and no strategy — file the wrong one first and the clerk rejects it, costing you weeks. On the other, an Albuquerque or Santa Fe probate attorney whose retainer runs into the thousands, billing by the hour to organize paperwork you could have organized yourself.

The government gives you the forms but refuses to give you the roadmap. National sites like Nolo and TurboTax give you a roadmap built for a state that isn't New Mexico — they miss the FID-1, the community-property double step-up, and the tribal-land overlap entirely. You're stuck paying for accuracy or paying for affordability, never both.

The New Mexico FID-1 Compliance Roadmap

This guide is the missing roadmap. It walks the exact path you actually have to walk — from the first 30 days, through deciding whether you even need probate, into the specific returns New Mexico requires, and out the other side with the estate closed. Every chapter names the precise form, agency, deadline, and fee. Where New Mexico law hands you an advantage — and it hands you several large ones — the guide leads with it instead of burying it.

It is built for the three people who actually need it: the surviving spouse untangling decades of joint finances, the out-of-state adult child suddenly named executor for a parent who died here, and the person planning ahead for their own family. It is not legal advice for a contested or litigated estate — and Chapter 13 tells you plainly, in writing, exactly when your situation crosses the line into "call a lawyer or CPA."

What's Inside — and the Exact Fear Each Part Removes

The Fiduciary Tax Trap, defused (Chapter 6)

The chapter that pays for the guide. You'll learn the one-line rule for when the FID-1 is required, what counts as "income during administration," the 1.7%–4.9% brackets that hit the top rate almost immediately — and the legal move that pushes that income onto beneficiaries' lower personal rates instead. This is the penalty letter that never arrives.

The Community Property Double Step-Up (Chapter 8)

The most financially valuable concept in the book, and the one national tax software gets wrong for New Mexicans. Because New Mexico is a community property state, when the first spouse dies both halves of the home and portfolio reset to date-of-death value. A surviving spouse can sell a long-held, highly appreciated home and owe essentially zero capital gains — but only if you get the date-of-death appraisal. The guide tells you to do it now, before the value is impossible to prove.

The $500,000 Homestead Bypass (Chapters 3 & 9)

If you're a surviving spouse with a principal residence valued at $500,000 or less held as community property, you may be able to transfer the home with no probate at all — using the §45-3-1205 Homestead Affidavit. The guide gives you every condition, the six-month clock, and the exact documents to record with the county clerk.

Medicaid Recovery defense, in plain English (Chapter 10)

The deepest fear for many families — that the state will seize the home to recoup nursing-care costs. New Mexico recovers only from the probate estate, which is exactly why a TOD deed shields the home. The guide lays out the mandatory deferrals (surviving spouse, minor child, disabled child) and the hardship-waiver criteria, so you assert the protections instead of freezing in fear of them.

The probate decision tree and creditor shortcut (Chapters 3 & 4)

Many New Mexico estates skip probate entirely. You'll work through non-probate transfers, the $50,000 small-estate affidavit, and the homestead affidavit before ever paying a filing fee — and learn how publishing the 4B-501 Notice to Creditors cuts the claim window from a full year to four months.

Business closure, vehicles, tribal land, and a complete form index

How to close a decedent's Gross Receipts Tax account before non-filing penalties pile up (they accrue even at $0 revenue), transfer vehicles at the MVD without probate, handle Native American trust-land jurisdiction, and an appendix mapping every form — PIT-1, FID-1, RPD-41058, the MVD and 4B series — to its agency and purpose.

Who This Is For

- The surviving spouse afraid that selling or retitling the family home will trigger a devastating tax bill — when New Mexico law may erase it entirely.

- The out-of-state executor who flew home after the funeral with a box of documents and a parent's estate in a state whose tax rules they've never seen.

- The person planning ahead who wants their affairs in order so none of this lands on their family — including TOD deeds that must be recorded before death to work at all.

Why Not Just Use the Free Forms?

Because free forms come with no instructions and no sequence. The State of New Mexico will hand you a blank FID-1 and a blank Affidavit of Surviving Spouse, then leave you to guess which to file first — and a procedural rejection at the county clerk's window costs you weeks you don't have. This guide translates the statutory jargon into plain English and tells you the order.

And even if you ultimately hire a professional, handing a CPA or attorney a shoebox of unsorted documents costs the estate thousands in billable hours. Organize it yourself with this guide first, hand them a clean portfolio, and you can save the estate many times the cost of the guide. The free PDFs can't do that. The national software gets New Mexico wrong. The local attorney charges by the hour for what's in these pages.

Our Promise

This is a complete, New Mexico-specific roadmap for the ordinary estate, current to 2026 federal figures and New Mexico statute. If it doesn't give you a clearer path through New Mexico's tax and probate maze than the free forms ever could, we'll refund you — no questions, no friction. You're grieving; the last thing you need is a fight over .

Educational guide reflecting New Mexico law and 2026 federal figures — not legal or tax advice for a specific estate. Verify current fees and exemptions, and consult a licensed New Mexico attorney or CPA for contested, business, or large estates.

Settle the estate confidently, legally, and affordably.

Stop guessing with generic national forms that ignore New Mexico law.

Get the Guide