Wyoming Has No Estate Tax, No Inheritance Tax, and No Income Tax. So Why Is the IRS Sending You a Penalty Notice?

Everyone told you Wyoming was the easy one. No state estate tax. No state inheritance tax. No state income tax. You assumed you could distribute the assets, close the accounts, and move on. Then the IRS sent a notice: the estate earned $4,200 in oil royalties during the six months it took to settle, and nobody filed a fiduciary income tax return. The penalty is $435 per month for every month the Form 1041 was late. That is not a Wyoming tax. It is a federal tax that exists regardless of which state has zero taxes on its books.

Then the Wyoming Department of Health sent a letter. Your father received Medicaid-funded nursing home care for two years. The state is filing a Chapter 35 estate recovery claim against the house. The house that passed by joint tenancy. The house you thought bypassed probate entirely. Wyoming's Medicaid Estate Recovery Program does not care how the property was titled. It is authorized to place a TEFRA lien on real property before death and file a recovery claim after death. You cannot sell the house for less than eighty percent of its fair market value without written approval from the Department. And you already listed it at seventy-five percent because you wanted a quick sale.

And then the mineral rights problem surfaced. Your father owned a quarter-section of mineral rights in Campbell County. The oil and gas operator suspended royalty payments the week he died and will not release another check until you provide a recorded probate document or a new division order. You assumed the small estate affidavit would cover it. But mineral rights count toward Wyoming's $400,000 summary distribution threshold, and the minerals alone appraise at $280,000. Combined with the house and the bank accounts, you are over the threshold. The summary procedure is not available. You need formal probate, a non-resident co-representative if you live out of state, and a chain-of-title filing with the county clerk before any royalties flow again.

A Wyoming estate attorney charges statutory fees based on the estate's gross value: ten percent on the first $1,000, five percent on the next $4,000, three percent on the next $15,000, and two percent on everything over $20,000. For a $400,000 estate, that is over $8,000 in attorney fees alone. A CPA filing the federal fiduciary return charges another $500 to $1,500. Neither one will explain the Medicaid lien, the mineral rights transfer process, and the federal filing deadlines in one conversation because each problem belongs to a different professional silo. You need one document that connects all of it. You need the Federal Compliance Sequence.

Introducing the Wyoming Final Tax & Estate Tax Guide

This is the guide built around the one thing no free resource, government website, or law firm blog provides: the Federal Compliance Sequence -- a strict chronological workflow that tells you which federal form to file, which Wyoming procedure to complete, which agency to notify, and in which order, so that a state with zero state taxes does not cost your family thousands in federal penalties, lost royalty income, and Medicaid recovery claims you never saw coming.

Free articles say Wyoming has no estate tax and stop there. Government websites scatter the requirements across the IRS, the Wyoming Judicial Branch, the Department of Health, county clerks, and oil and gas operators -- each knowing its own paperwork and nothing about the others. Law firm blogs describe the complexity with just enough detail to make you call for a consultation. None of them answer the question you are asking at midnight: "If Wyoming has no death taxes, what exactly do I still have to file, and what happens if I get the order wrong?"

The Federal Compliance Sequence gives you the answer. It maps the final federal Form 1040, the fiduciary Form 1041, the federal Form 706 portability election, the Medicaid Chapter 35 response, the mineral rights transfer procedure, and the small estate affidavit into a single timeline -- with the dependencies between them made explicit, so you never file out of order and never discover a requirement after the deadline has passed.

What's Inside -- and the Exact Problem Each Part Solves

The "Zero State Tax" Reality Check

A plain-English explanation of what Wyoming's triple absence actually means: no state estate tax, no state inheritance tax, no state income tax. And then the obligations that remain anyway: the final federal Form 1040, the estate's fiduciary Form 1041, the federal estate tax Form 706, Wyoming Medicaid estate recovery under Chapter 35, and the probate procedures that control when and how assets can be distributed. Solves: the dangerous assumption that "no state tax" means "no filings" -- the mistake that leads to federal penalties, frozen royalty payments, and personal liability for the executor.

The Step-Up in Basis Documentation Strategy

When someone dies owning Wyoming real estate, ranch land, or mineral rights, the federal step-up in basis resets the property's tax value to its fair market value at the date of death. All appreciation during the decedent's lifetime is eliminated for capital gains purposes. A ranch purchased for $200,000 that is worth $900,000 at death gets a $900,000 basis. An immediate sale generates zero capital gains. But the step-up only works if you document the fair market value with a certified appraisal immediately after death. And in Wyoming, agricultural land has two different valuations: the county's agricultural productivity assessment used for property taxes and the fair market value the IRS requires for the step-up. Use the wrong number, and the IRS will challenge the basis. Solves: the family that sells inherited ranch land and pays capital gains tax on appreciation that should have been eliminated -- because nobody told them to get a fair-market-value appraisal separate from the county's agricultural assessment.

The Mineral Rights Transfer Procedure

Wyoming mineral rights cannot be transferred by simply filing a small estate affidavit and mailing it to the operator. Mineral interests count toward the $400,000 summary distribution threshold. Oil and gas operators will suspend royalty payments upon learning of the owner's death and will not release them until they receive a recorded probate document, a certified death certificate, and a new division order. If the minerals push the estate over $400,000, you are in formal probate territory. If you live out of state, you need a Wyoming resident co-representative or a local bank acting as agent. Solves: the out-of-state heir whose monthly royalty checks stopped without warning and who has no idea what paperwork the operator needs or how long it takes to restore the payment stream.

The Medicaid Chapter 35 Estate Recovery Defense

The Wyoming Department of Health operates an aggressive Medicaid Estate Recovery Program under Chapter 35. The state can place pre-death TEFRA liens on real property and file post-death claims against the estate to recover the full cost of nursing home care. Properties subject to a TEFRA lien cannot be sold for less than eighty percent of fair market value without written Department approval. If the executor distributes assets before satisfying the lien, they face personal liability. Solves: the family that assumes joint tenancy or a Transfer on Death deed bypasses Medicaid recovery -- then receives a claim letter for assets they already distributed or a sale that the Department blocks because the listing price was too low.

The $400,000 Small Estate Threshold

Effective July 1, 2025, Wyoming doubled its small estate threshold from $200,000 to $400,000. Estates below this amount can use summary distribution procedures or a small estate affidavit instead of formal probate. But the affidavit cannot be executed until thirty days after the date of death. And the threshold calculation includes mineral rights, which many executors forget to count. Going through the affidavit process when the estate actually exceeds the threshold wastes time and may create liability. Solves: the executor who does not know the threshold just changed, does not know mineral rights count toward it, and either files unnecessarily in formal probate or files a small estate affidavit that is invalid because the estate exceeds the limit.

Federal Form 706 and Portability

The federal estate tax threshold is $15,000,000 per individual for 2026 deaths, made permanent by the One Big Beautiful Bill Act. Most Wyoming estates fall well below this. But filing Form 706 voluntarily to elect portability transfers the deceased spouse's unused exemption to the survivor, effectively doubling the shield to $30,000,000. For families with appreciating ranch land, mineral rights, or investment portfolios, this election can save millions in taxes decades from now. The nine-month filing deadline is absolute. Solves: the surviving spouse whose combined estate may grow past the exemption in ten or twenty years -- who does not realize the portability election window closes nine months after death and never reopens.

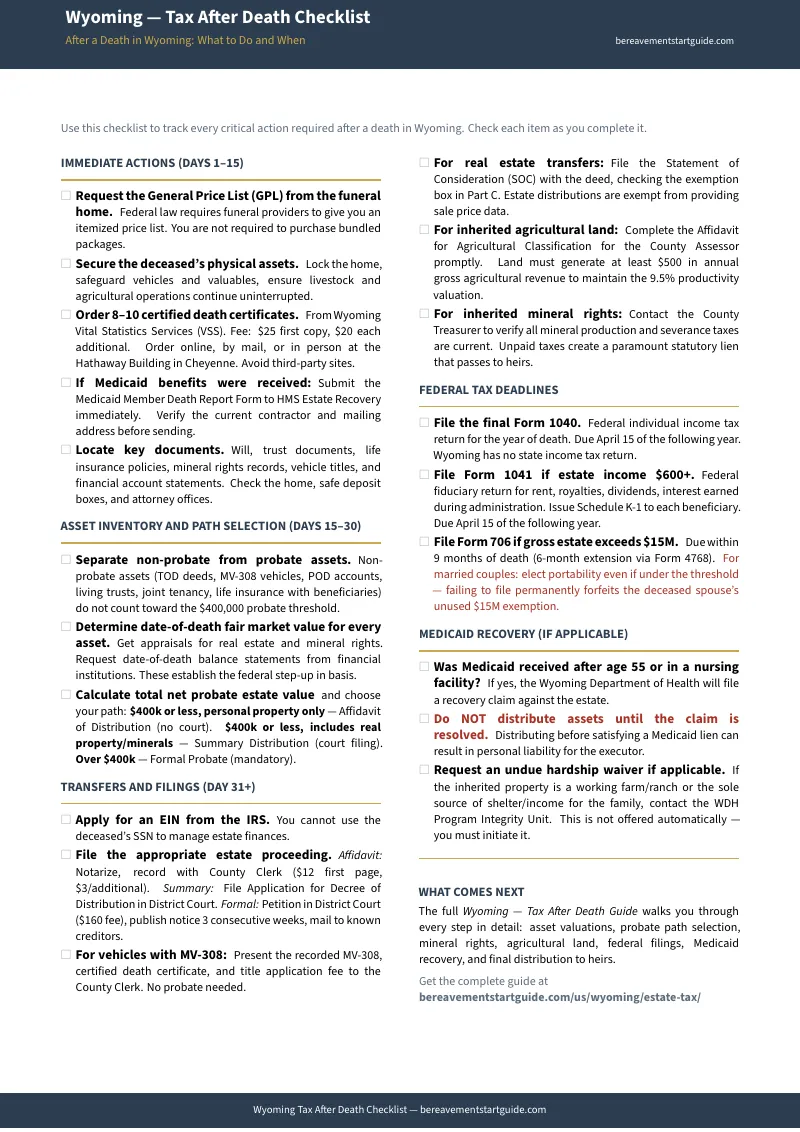

The First 10 Days -- Urgent Steps

A sequenced list of actions that directly affect the estate's tax position and legal standing: ordering certified death certificates, locating and filing the will, applying for the estate's EIN, notifying oil and gas operators to prevent unauthorized royalty distributions, ordering appraisals for the step-up in basis using fair market value (not the county's agricultural assessment), and understanding that any Power of Attorney expired at the moment of death. Solves: the family that waits weeks to start, then discovers the royalty checks were mailed to a closed account, the step-up documentation window is narrowing, and the legal authority they thought they had through a Power of Attorney no longer exists.

Who This Is For

- Executors and personal representatives who need to know exactly which federal returns to file and which Wyoming procedures to complete, in which order, by which deadlines -- before the IRS assesses penalties or the court rejects a petition.

- Surviving spouses who need to understand the step-up in basis before selling any inherited property -- because the appraisal must happen now, not when the property is listed.

- Out-of-state beneficiaries who inherited Wyoming mineral rights and need to understand why royalty payments stopped, what the operator requires, and whether the estate qualifies for summary distribution or needs formal probate.

- Families facing a Chapter 35 Medicaid estate recovery claim who need to understand the scope of the TEFRA lien, the eighty-percent sale restriction, and the exemptions that may apply.

- Anyone who was told Wyoming has "no death taxes" and wants to know what that actually means for the federal filings, Medicaid obligations, and probate procedures that still apply.

- Beneficiaries who plan to sell inherited ranch land, residential property, or mineral rights and need to document the step-up in basis correctly to avoid paying capital gains tax they do not owe.

Why Free Government Websites Won't Get You Through This

The information exists. The IRS publishes Form 1041 instructions, the Wyoming Judicial Branch publishes probate forms, the Department of Health publishes Medicaid recovery rules, and the county clerks maintain mineral rights records. Here is what you actually encounter when you try to use them:

- The Wyoming Judicial Branch publishes probate forms with no instructions. The blank PDFs are available. The courts are legally prohibited from telling you how to fill them out, which ones apply to your estate, or how they interact with federal tax filings. The forms assume you already know whether you qualify for summary distribution or need formal probate. They do not mention the thirty-day waiting period, the mineral rights threshold calculation, or the non-resident co-representative requirement.

- The IRS publishes Form 1041 and Form 706 instructions for tax professionals. The instructions explain every line of the return. They do not explain which Wyoming estates need to file, how estate income from mineral royalties is reported differently from ranch rental income, or that the Ogden, Utah processing center handles Wyoming filings. They assume you already have an EIN, already know the estate's fiscal year, and already understand the difference between the decedent's final 1040 and the estate's 1041.

- The Department of Health sends Medicaid recovery letters with no context. The letter states the amount owed. It does not explain the surviving spouse exemption, the hardship waiver process, the eighty-percent sale floor, or what happens if you already distributed the asset. It tells you what the state wants. It does not tell you what your defenses are.

- National estate tax websites say "Wyoming has no estate tax" and move on. SmartAsset, Nolo, FindLaw, and every state tax guide correctly reports that Wyoming levies no estate or inheritance tax. None of them mention the federal fiduciary return, the Chapter 35 Medicaid recovery program, the mineral rights transfer procedure, the new $400,000 small estate threshold, or the step-up in basis documentation that prevents unnecessary capital gains tax.

- Law firm blogs explain the complexity and end with a phone number. Every asset protection and estate planning firm in Cheyenne, Casper, and Jackson publishes content about executor liability, Medicaid recovery, and mineral rights transfers. The posts explain just enough to create urgency. They never explain enough to act. Every post ends with a consultation invitation backed by statutory fees that start at $350 and scale with the estate's gross value.

Free resources give you IRS instructions written for CPAs, probate forms with no guidance, Medicaid letters with no defense strategy, and law firm blogs that end with a billable-hour phone number. The Federal Compliance Sequence puts every federal return, state procedure, agency notice, and deadline into one document, in the order you actually need them.

-- Less Than Fifteen Minutes With a Wyoming Estate Attorney

A consultation with a Wyoming probate or estate attorney costs statutory fees that can exceed $8,000 for a $400,000 estate. A CPA preparing the federal fiduciary return charges $500 to $1,500 depending on complexity. A single phone call to an oil and gas operator to ask about the division order process will keep you on hold longer than it takes to read the chapter that explains the entire procedure. This guide costs less than fifteen minutes of professional legal time and gives you the complete Federal Compliance Sequence -- every federal return, every state procedure, every agency notice, and the chronological order that determines whether the estate closes cleanly or stalls with penalties and frozen royalty payments.

Your download includes 6 printable PDFs: the complete guide covering every federal and state obligation, the standalone Wyoming -- Tax After Death Checklist across chronological timeline sections, a Key Forms Reference card listing every form with where to get it and where to file it, a Key Contacts directory of every agency you will deal with, a Mineral Rights Transfer Checklist covering the operator notification, division order, and recording process, and a Probate Path Decision Tree that tells you whether your estate qualifies for summary distribution or needs formal probate. Instant download, no account required.

If this guide doesn't give you a clearer path through Wyoming's federal tax and estate filing requirements than anything you found for free, reply to your receipt within 30 days and we'll refund every cent. No forms, no questions.

Two Ways to Start

Start free: Download the Wyoming -- Tax After Death Checklist. It covers the key deadlines, the critical forms, and the most common mistakes -- enough to understand which filings apply to your estate and whether you need the full guide.

Go deeper: The full Wyoming Final Tax & Estate Tax Guide () walks you through every filing in the Federal Compliance Sequence -- the step-up in basis documentation strategy, the mineral rights transfer procedure, the Medicaid Chapter 35 defense, the $400,000 small estate threshold calculation, the federal portability election, and the complete probate-to-closing roadmap. Plus 4 standalone reference cards you can print and bring to meetings.