Your Spouse Died Two Weeks Ago. The Bank Froze Every Account. The MPF Trustee Says You Cannot Claim His Pension Without a Grant. And Nobody — Not the Bank, Not the Government, Not the Funeral Director — Has Given You a Single Document That Lists Everything You Are Entitled to and the Order You Must Claim It In.

You walked out of HSBC with a death certificate and a frozen account. The teller said the money does not move until you produce a sealed Grant from the High Court. So you went home and searched "survivor benefits Hong Kong" — and found twelve government departments, each describing its own narrow slice of what is available, none of them referencing the others, none of them warning you which claims have deadlines and which ones you have to file before something else or lose the money permanently.

That is how families lose tens of thousands of dollars in Hong Kong. Not because the benefits do not exist — they do. The MPF death benefit. The employer's statutory compensation (up to HK$3.24 million for workplace fatalities). The Home Affairs Department's emergency funeral release. The Social Welfare Department burial grant. The life insurance payout. The property rates concession. The surviving spouse's Old Age Living Allowance. They are all real, they are all claimable, and they are scattered across so many agencies with so many preconditions that the average grieving family discovers half of them too late and claims the other half in the wrong order.

Here is the order problem that costs families money: you apply to the Home Affairs Department for the Certificate for Necessity of Release of Money to fund the funeral. But you apply after you have already paid the undertaker out of pocket. The HAD rejects you — they fund the undertaker directly, they do not reimburse. You are now permanently out up to HK$20,000. Or you file the MPF death claim, only to discover that the eMPF platform requires the personal representative's Grant of Representation first — and you have not even started probate. Or you miss the employer's obligation to reimburse funeral expenses up to HK$98,950 under the Employees' Compensation Ordinance because nobody told you it existed and the HR department did not volunteer the information. Every one of these is a sequencing error, not a knowledge gap. The information was available. The order was not.

The Hong Kong Survivor Benefits Navigator is built around what we call the Compliance Sequence Method — a structured, chronological system that maps every survivor benefit available in Hong Kong to the exact point in the bereavement timeline when you must claim it, which forms you need, which agency handles it, and which claims must be completed before the next one unlocks. Not a catalogue of benefits. Not a list you have to figure out how to sequence yourself. A step-by-step operational roadmap that tells you what to claim, when to claim it, and what happens if you get the order wrong.

What's Inside the Navigator

A 7-module guide, a standalone Benefits Entitlement Checklist, and two printable worksheets — covering every survivor benefit available in Hong Kong from the moment of death through the final financial settlement:

Module 1: The First 48 Hours — Emergency Benefits and Urgent Claims

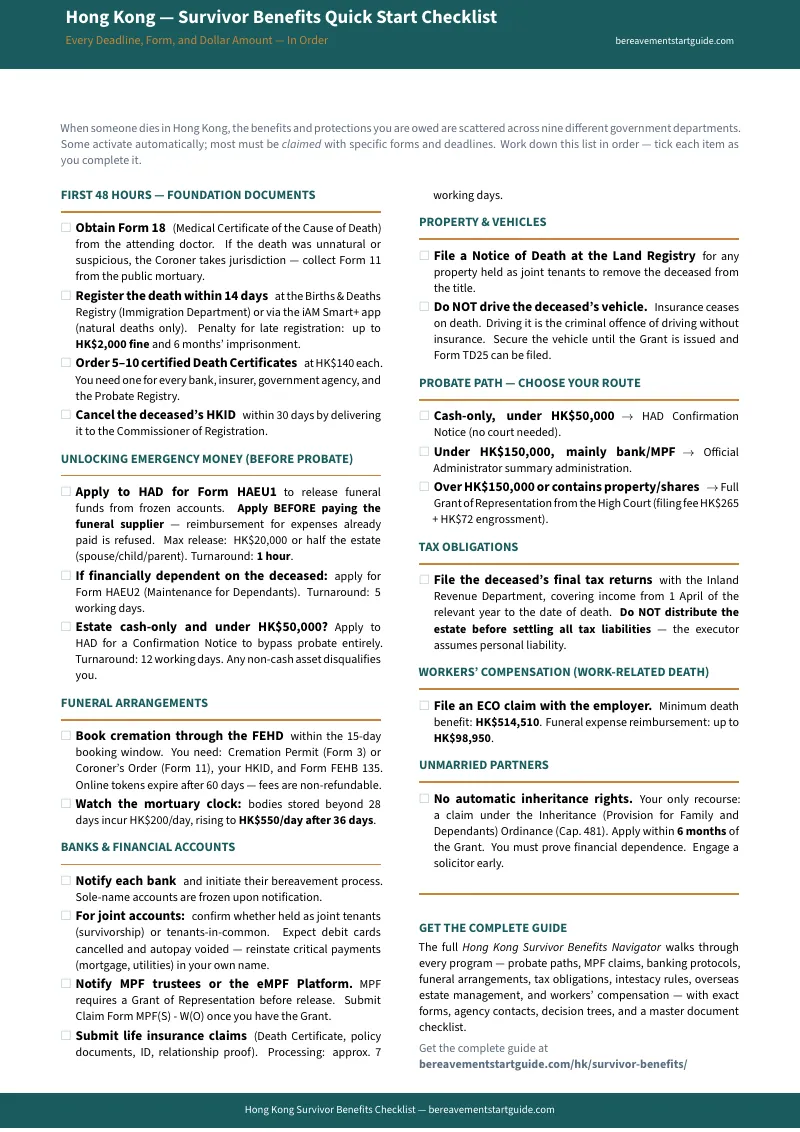

The benefits clock starts ticking immediately. This module covers the Hospital Authority's mortuary fee escalation (HK$200/day after 28 days, HK$550/day after 36 days) and how to avoid it, applying for the HAD's Certificate for Necessity of Release of Money before you pay the undertaker (up to HK$20,000 or half the estate, paid directly to the funeral provider within the hour), the HAD maintenance allowance for dependents who need immediate living expenses, and the critical timing rule that catches every family who pays first and applies second.

Module 2: Life Insurance and Commercial Claims

How to file death claims with every major Hong Kong insurer — AIA, Sun Life, Prudential, Manulife, Bowtie — the exact documents each requires (original death certificate, HKID copy, policy number, relationship proof), the typical 7-working-day processing timeline, and how to chase a stalled claim. Plus the critical distinction between named-beneficiary policies (which bypass probate entirely) and estate-payable policies (which require the Grant first), and the common trap of failing to claim group life cover through the deceased's employer.

Module 3: MPF, Pensions, and Retirement Benefits

The Mandatory Provident Fund is the benefit that shocks most surviving spouses. Unlike pension systems in other countries, Hong Kong's MPF does not allow beneficiary nominations — the funds form part of the estate and must pass through the personal representative. This module covers the eMPF platform death claim process step by step, which documents the trustee requires, why you need the Grant of Representation before the trustee will release a cent, the ORSO occupational scheme alternative for employers that still run one, and how to check whether the deceased was enrolled in more than one MPF scheme (common for employees who changed jobs without consolidating).

Module 4: Employer Benefits and Workplace Death Compensation

If the deceased was employed, the family is entitled to benefits that HR departments rarely volunteer. This module covers the final salary disbursement (including accrued leave, pro-rata bonus, and any outstanding reimbursements), the group life insurance claim through the employer's corporate policy, and — for deaths caused by workplace accidents or occupational diseases — the Employees' Compensation Ordinance calculation: 84 months' earnings for employees under 40, 60 months for ages 40 to 56, 36 months for 56 and above, subject to a maximum monthly earnings cap of HK$38,670, a minimum death compensation of HK$514,510, and a separate funeral reimbursement of up to HK$98,950. Plus how to file the claim with the Labour Department and what happens when the employer disputes it.

Module 5: Government Grants, Welfare, and Ongoing Allowances

The Social Welfare Department burial grant (up to HK$16,790 for CSSA recipients), the Old Age Living Allowance and how the surviving spouse qualifies after the death (the asset test that excludes the family home but includes cash investments), the CSSA continuation for dependent family members, and the disability allowance for survivors with long-term health conditions. Each grant has its own asset test, its own application form, and its own disqualifiers — this module walks through every one with a decision table so you can see at a glance which you qualify for.

Module 6: Property, Rates, and Tax Benefits

The property rates concession for an owner-occupied home the surviving spouse continues to live in, how to apply for the concession through the Rating and Valuation Department, the Inland Revenue Department's requirements for the deceased's final salaries and property tax returns (Section 54 of the IRD Ordinance), the Personal Assessment election that can offset business losses against rental income, and the timing trap — the executor must file and clear all outstanding tax before distributing the estate. Misstep here and the executor is personally liable for the shortfall.

Module 7: Unmarried Partners, Cohabitants, and Non-Traditional Families

Hong Kong intestacy law does not recognise unmarried partners. But the Inheritance (Provision for Family and Dependants) Ordinance (Cap. 481) allows a financially dependent cohabitant to claim reasonable maintenance from the estate — if they can prove they were being maintained immediately before the death. This module covers the evidentiary threshold, how to apply through the Home Affairs Department for interim maintenance before the estate is distributed, the recent court developments on same-sex spousal rights, and the practical steps for a partner who has no automatic legal standing but has legitimate financial needs.

Who This Guide Is For

- The surviving spouse who just lost a partner and discovered that the bank accounts are frozen, the MPF cannot be touched, and no single government office can explain what the family is entitled to or in what order to claim it — who needs one document that sequences every benefit from the emergency funeral release through the final tax clearance

- The adult child managing a parent's affairs from across Hong Kong or from overseas — who needs to know exactly which claims require the Grant of Representation, which bypass probate entirely, which have hard deadlines, and which HR and insurance benefits to demand before the employer quietly closes the file

- The executor or administrator who is terrified of personal liability — who needs to know that clearing the IRD's tax obligations comes before distributing any survivor benefits, that MPF claims require the Grant, and that the HAD funeral release must be applied for before the invoice is paid

- The family of someone who died at work — who needs the Employees' Compensation Ordinance calculation broken down plainly, the Labour Department claim process mapped, and the employer's separate obligation to reimburse funeral expenses up to HK$98,950 flagged before it slips through the cracks

- The unmarried or same-sex partner with no automatic inheritance rights — who needs absolute clarity on the Cap. 481 dependency claim, the evidence required, and how to secure interim maintenance before hostile family members distribute the estate

Why Free Resources Will Not Get You Through This

Every benefit in this guide is technically documented somewhere on a government website. Here is what happens when you try to assemble it yourself:

- Government portals describe their own department and nothing else. The Social Welfare Department explains the burial grant but says nothing about the HAD emergency release, the MPF claim, or the employer's compensation obligation. The eMPF platform explains how to file a death claim but does not mention that you need the Grant of Representation first — or how long the Grant takes. There is no central survivor benefits office in Hong Kong and no single portal that sequences everything.

- Law firms write about probate, not about benefits. Solicitors produce excellent content on the Grant of Representation process — because that is what generates HK$20,000 to HK$80,000 in retainers. They rarely cover the HAD emergency release, the employer's ECO obligations, the SWD burial grant, or the property rates concession, because those claims generate zero billable hours.

- Banks explain their own freeze and nothing beyond it. HSBC and Hang Seng each publish a bereavement leaflet that explains how to close accounts at their institution. They do not mention what you should claim elsewhere, when to claim it, or what depends on what.

- Forum advice is empathetic and dangerous. Reddit threads and diaspora WhatsApp groups are full of people sharing what worked for them — much of it anecdotal, some of it years out of date, and a portion of it advice that technically constitutes intermeddling. Following a stranger's suggestion to "just use the joint account for the funeral" can trigger the penalty under Section 60J of the Probate and Administration Ordinance.

- Generic bereavement guides are built for the wrong country. The digital market is dominated by American and British "survivor benefits" guides that cover Social Security, UK Bereavement Support Payment, and NHS Widowed Parent's Allowance. None of them have heard of the HAD, the eMPF platform, the ECO compensation formula, or Cap. 481. They cannot help you in Hong Kong.

Free sources give you fragments from a dozen departments. This guide puts every Hong Kong survivor benefit, every form, every agency, and every deadline into one document — in the exact order you must claim them.

— A Fraction of the Benefits You Will Claim

The HAD emergency funeral release alone can put up to HK$20,000 back in your hands within the hour — if you apply before you pay. The employer's ECO funeral reimbursement adds up to HK$98,950. The ECO death compensation can reach HK$3.24 million. Life insurance, MPF, the SWD burial grant, the property rates concession, the Old Age Living Allowance — every one of these is money your family is entitled to. Missing even one because you did not know the form, the deadline, or the sequence costs more than this guide ever will.

Your download includes the complete 7-module guide, the standalone Benefits Entitlement Checklist, and two printable worksheets: a Claim Tracking Matrix for logging every claim filed, its status, and its follow-up date across all agencies, and a Document Submission Log for tracking which certified copies of the death certificate, HKID, marriage certificate, and Grant have been submitted to which institution — so nothing gets lost in transit. Plus a 30-day money-back guarantee. If the guide does not give you clarity on what you are entitled to and the confidence to claim it in the right order, email us for a full refund.

Not ready for the full guide? Download the free Hong Kong — Survivor Benefits Checklist — a one-page overview of every benefit available, the agency that handles it, and the one timing rule that saves families thousands. It is enough to see what you are entitled to today.

You are carrying a weight nobody prepared you for. But the benefits exist, the claims are yours to make, and the order is right here. One step at a time.