Someone You Love Just Died in New Zealand. The Bank Froze Their Accounts This Morning. The High Court Requires Physical Forms You Have Never Seen Before. And Nobody Told You About the Six-Month Waiting Period That Makes You Personally Liable If You Distribute Too Early.

You are standing in a place nobody prepared you for. Maybe you were named executor in a will you barely remember reading, and now the funeral director is waiting for a decision about the service while you try to figure out how many death certificates to order from Births, Deaths and Marriages at $35 each. Maybe there was no will at all, and because you are the surviving spouse or the eldest child, everyone is looking at you for answers about a legal process governed by the Administration Act 1969 that you have never heard of. Maybe ANZ or Westpac just told you the accounts are frozen and you cannot access a single dollar to pay the power bill, the mortgage, or the funeral deposit — and funerals in New Zealand cost $8,000 to $15,000 depending on which funeral director you called.

You are grieving and sleep-deprived, but the paperwork does not wait. The funeral director needs you to understand the difference between the Medical Certificate of Cause of Death and the official death certificate from BDM. Inland Revenue needs notification through myTrove before penalties start accruing. The family is asking about the house. Work and Income needs to know about the pension before overpayments create a debt against the estate. And somewhere in the back of your mind, a terrifying question keeps circling: if I distribute the estate before the six-month window closes, or accidentally trigger a bank freeze by notifying myTrove before I have arranged alternative finances, or make a formatting error on the High Court PR1 form that gets the whole application rejected — am I personally liable?

The short answer: the estate pays its debts, not you. But the long answer — the one that involves a $40,000 probate threshold that applies per institution not per estate (meaning three accounts of $38,000 each might not need the High Court at all), a Family Protection Act that gives estranged relatives up to twelve months to contest the will, a KiwiSaver balance that does not automatically transfer to the spouse, IRD requiring two completely different tax returns for the same person, and a High Court that still demands wet-ink sworn affidavits physically couriered to the Wellington Probate Unit despite having an online payment portal — that answer is what separates families who settle an estate in months from families who spend years and thousands of dollars untangling mistakes they did not know they were making.

The When Someone Dies in New Zealand — Estate Settlement Guide is a Calm Sequencing System for every legal, financial, and administrative step between the funeral home and final distribution. Not a law textbook. Not a generic checklist that does not know New Zealand from Australia. A structured, NZ-specific manual that separates what must be done in the first 48 hours from what legally cannot happen until the six-month protection period expires — so you stop guessing, stop panicking, and start working through this in the right order.

What's Inside the Calm Sequencing System

An 11-chapter guide and the First 48 Hours Checklist — covering every stage from the moment of death through final asset distribution, built specifically for New Zealand statutes, the High Court of New Zealand, and the country-specific rules that make settling an estate here different from anywhere else:

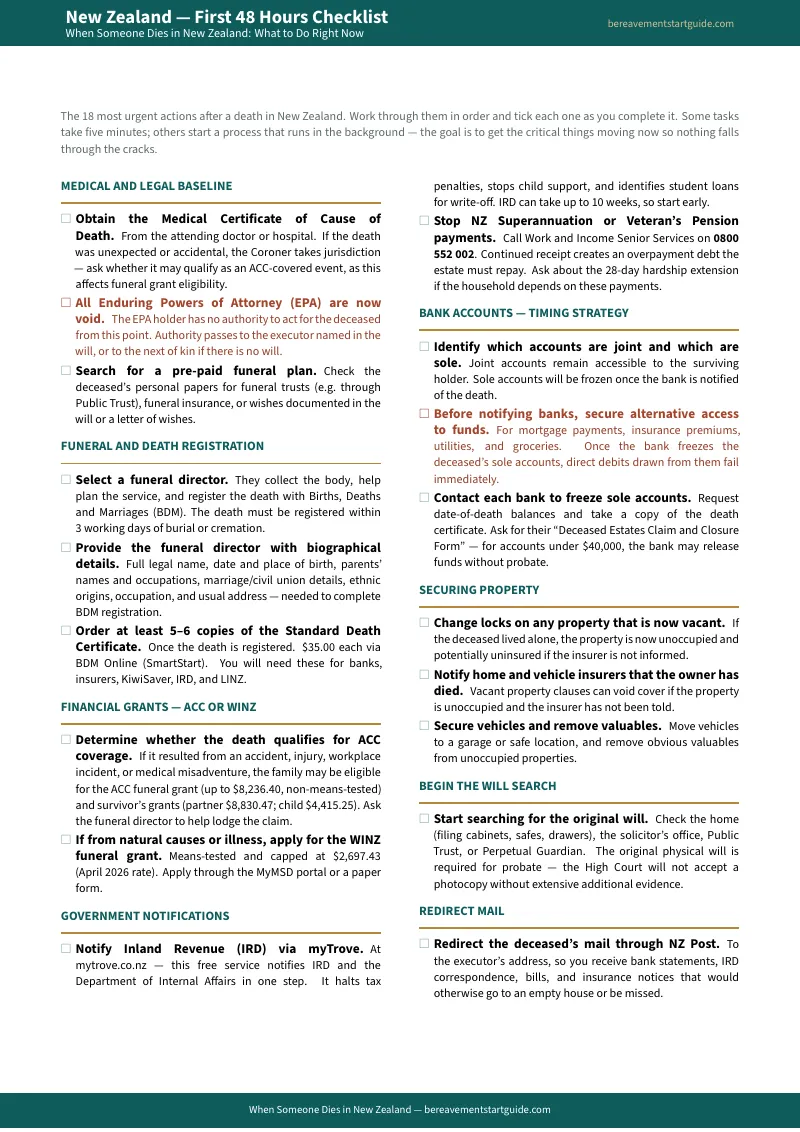

The First 48 Hours: Immediate Actions and Death Registration

The moment someone dies in New Zealand, every Enduring Power of Attorney issued under the Protection of Personal and Property Rights Act 1988 is legally void. If you managed their finances under an EPA, you no longer have authority. This chapter covers getting the death medically verified, choosing a funeral director, registering the death with BDM within the mandatory three working days, and the critical distinction most families learn too late: if the death was caused by an accident, the family qualifies for the ACC funeral grant of up to $8,236.40 (non-means-tested) instead of the WINZ funeral grant capped at $2,697.43 (strictly means-tested). That difference of over $5,500 depends entirely on understanding the cause of death and flagging it with the funeral director in the first 24 hours.

The First Month: Discovery, Asset Inventory, and the $40,000 Threshold Decision

This is the most critical decision point in the entire process. You must locate the original will (the High Court will not accept a photocopy without complex affidavits), secure the property, and inventory every asset. Then comes the question that determines whether you face a rapid administrative closure or a months-long court process: does any single institution hold more than $40,000 in the deceased's sole name? This threshold — raised from $15,000 to $40,000 in September 2025 — applies per institution, not per estate. An estate worth $110,000 spread across three providers might not need the High Court at all. The guide maps the exact scenarios where you can settle without court authority and where you cannot.

The High Court: Probate and Letters of Administration

If the estate requires formal authority, you must file with the High Court of New Zealand. This chapter walks through every step: Form PR1AA (the simplified application introduced for straightforward estates), the traditional PR1 and PR7 forms, the affidavit requirements, the $269 filing fee paid through the Ministry of Justice File and Pay portal, the requirement to physically courier the original will and wet-ink sworn affidavits to the Wellington Probate Unit despite digital payment, and the typical six-to-eight-week processing time. It covers the reality that the High Court routinely rejects applications for minor formatting errors — and what to do when it happens.

Administration, Tax, and Closing the Estate

Once the High Court issues the sealed grant, the real work begins. This chapter covers opening a dedicated estate bank account, directing banks and KiwiSaver providers to liquidate accounts, the LINZ Landonline property transmission process (Transmission Instrument code TSM, $180 plus lawyer fees), and the two tax returns that confuse every executor: the final individual return (IR3) covering April 1 to the date of death, and the estate trust return (IR6) for income earned after death. It explains when you need a separate IRD number for the estate and how to get one.

The Six-Month Protection Rule and Beneficiary Management

This is the chapter that saves executors from personal financial liability. Under the Family Protection Act 1955, spouses, children, and grandchildren have a statutory window to contest the will. If you distribute the estate before the six-month period following the grant expires and a successful claim is filed, you are personally liable to repay those funds out of your own pocket. The guide provides the precise timeline, explains the difference between the six-month safe distribution window and the twelve-month claim filing deadline, and gives you the framework for communicating with impatient beneficiaries who want their inheritance now — without destroying family relationships during bereavement.

Intestacy, Edge Cases, and Institutional Fees

The remaining chapters cover intestacy under Section 77 of the Administration Act (including the $155,000 prescribed amount for surviving spouses — a figure that shocks families who assumed the spouse gets everything), insolvent estates (strict priority rules under the Insolvency Act 2006), Māori Land Court succession for Māori freehold land (including whāngai provisions), foreign assets and cross-border resealing, disputes and missing documents, a consolidated reference of every form, portal, fee and deadline, and a transparent comparison of Public Trust fees ($6,355 setup plus $307/hour) versus private solicitors ($700 to $1,500 for standard probate) so you can make an informed decision about what help to hire and what to handle yourself.

Who This Guide Is For

- The surviving spouse whose partner just died and whose bank accounts were frozen this morning — who needs to know which accounts stay accessible under joint tenancy, how to get the bank to pay the funeral director directly from the frozen account, and whether the $40,000 threshold means you can skip the High Court entirely

- The adult child named as executor who has never filed anything with the High Court and is terrified of making a mistake on the PR1 form that gets the application rejected — who needs the complete filing walkthrough, every affidavit requirement explained, and a timeline that separates what is urgent from what must wait for the six-month protection period

- The family with no will who just learned that Section 77 of the Administration Act dictates everything — who needs to understand that the surviving spouse only receives $155,000 plus one-third of the residue if children exist, and who has priority to apply for Letters of Administration

- The executor living in Australia or overseas who cannot walk into an ANZ branch in Auckland to present the original death certificate — who needs to understand which processes can be managed digitally through myTrove and the File and Pay portal, and which absolutely require physical documents couriered to Wellington

- The financially constrained family who cannot afford a $10,000 funeral or a solicitor — who needs to know about the ACC funeral grant ($8,236.40 if accident-related), the WINZ funeral grant ($2,697.43 means-tested), the High Court filing fee waiver for financial hardship, and how to use the $40,000 threshold to avoid court costs entirely

- The proactive planner organising affairs after a terminal diagnosis or rest home transition — who needs to structure accounts, update Enduring Powers of Attorney, and create a "death folder" so their family never has to scramble through this process blind

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across govt.nz, the Ministry of Justice, Inland Revenue, LINZ, Work and Income, ACC, BDM, and a dozen institutional portals that do not talk to each other. Here is what you actually encounter when you try to settle an estate using free sources alone:

- Government pages tell you what to do but not when or how. The govt.nz "End of Life" hub and Te Hokinga ā Wairua cover death registration, funeral grants, and broad obligations. They do not sequence the steps chronologically, do not warn you about the strategic timing of myTrove notifications (triggering it before you have arranged alternative finances cascades into frozen direct debits and voided insurance), and do not explain how the $40,000 per-institution threshold actually works in practice.

- The Ministry of Justice discourages self-filing. The High Court forms (PR1AA, PR1, PR7) are legislative instruments designed for lawyers. The Ministry publishes them as PDFs with minimal guidance. Over 99% of probate applications are drafted by lawyers or specialist probate services — not because the process is impossible, but because the free resources make it feel impossible.

- Law firm blogs highlight complexity to justify retainer fees. Firms like Smith Partners, DK Legal, and Pier Law publish excellent technical breakdowns of executor liability and the Family Protection Act. All of their content is designed to convince you the process is too dangerous to handle alone — and that you need a retainer starting at $2,000. For contested estates, that is true. For the majority of straightforward estates, the answer costs a fraction of a solicitor's hourly rate.

- Public Trust charges institutional rates for institutional service. Public Trust has massive market share because they draft many of the wills that name them as executor. Their setup fee of $6,355 plus an hourly rate exceeding $307 plus 5% of gross estate income can consume a significant portion of a modest estate. Families want to avoid this but free resources do not show them how.

- myTrove is powerful but misunderstood. The centralized notification system saves an estimated 50 hours of administration time. But no free resource warns you about the consequences of triggering notifications too early — frozen accounts, cancelled insurance policies, halted direct debits — or explains the optimal sequence for using it.

- Bank estate pages protect the bank, not you. ANZ, BNZ, ASB, and Westpac each publish deceased estate processes focused on institutional liability protection. They do not explain how the $40,000 threshold works across institutions, how to negotiate early fund releases for funeral expenses, or why their processes differ from each other.

Free resources give you fragments from a dozen sources that do not reference each other. The Calm Sequencing System puts every New Zealand statute, form, deadline, and procedure into one document, in the order you actually need them.

— Less Than Fifteen Minutes With a New Zealand Estate Solicitor

A single consultation with a New Zealand estate solicitor costs $250 to $450 per hour. Standard estate administration retainers start at $2,000 and can reach $5,000 for anything beyond basic probate. Public Trust charges a setup fee of $6,355 before the hourly billing begins. Boutique probate services like Kiwilaw charge $759 just for the High Court application — and that covers nothing beyond obtaining the grant. This guide costs less than fifteen minutes of professional legal time and gives you the complete New Zealand-specific roadmap — every statute, every High Court form, every deadline, the $40,000 threshold strategy, the myTrove sequencing, the six-month protection rule, and the IRD tax transition that nobody explains in plain language.

Your download includes 10 PDFs: the complete 11-chapter guide, the First 48 Hours Checklist, plus 8 standalone printable tools — the $40,000 Threshold Decision Guide, the High Court Probate Walkthrough, the Six-Month Protection Rule reference card, the IRD Tax Transition Guide, the Intestacy and Fee Reference, the Forms/Portals/Fees/Deadlines fridge sheet, the Asset and Liability Inventory Worksheet, and the Beneficiary Communication Log. Plus a 30-day money-back guarantee. If the guide does not give you clarity on what to do next and confidence that you are doing it in the right order, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New Zealand — First 48 Hours Checklist — the 18 most urgent actions covering everything that must happen in the first two days after a death in New Zealand: death certificates, securing property, ACC versus WINZ funeral grants, myTrove notifications, pension cessation, and the asset inventory that determines whether you need the High Court. It is enough to get through tonight and tomorrow.

You did not ask for this job. But you can do it. The guide shows you how, one step at a time.