Your Partner Just Died in New Zealand. ACC Offers $8,566 for Accidental Deaths but WINZ Caps the Funeral Grant at $2,697 for Everyone Else. Nobody Told You These Are Completely Different Agencies With Completely Different Rules. And If You Apply to the Wrong One First, You May Lose Thousands.

You are standing in a place nobody prepared you for. The funeral director is waiting for a decision about the service while you try to figure out whether ACC or Work and Income handles your situation. The bank just froze the accounts. NZ Super payments will stop in 28 days whether you have arranged alternative income or not. And somewhere in the back of your mind, a question keeps circling: am I going to lose the house?

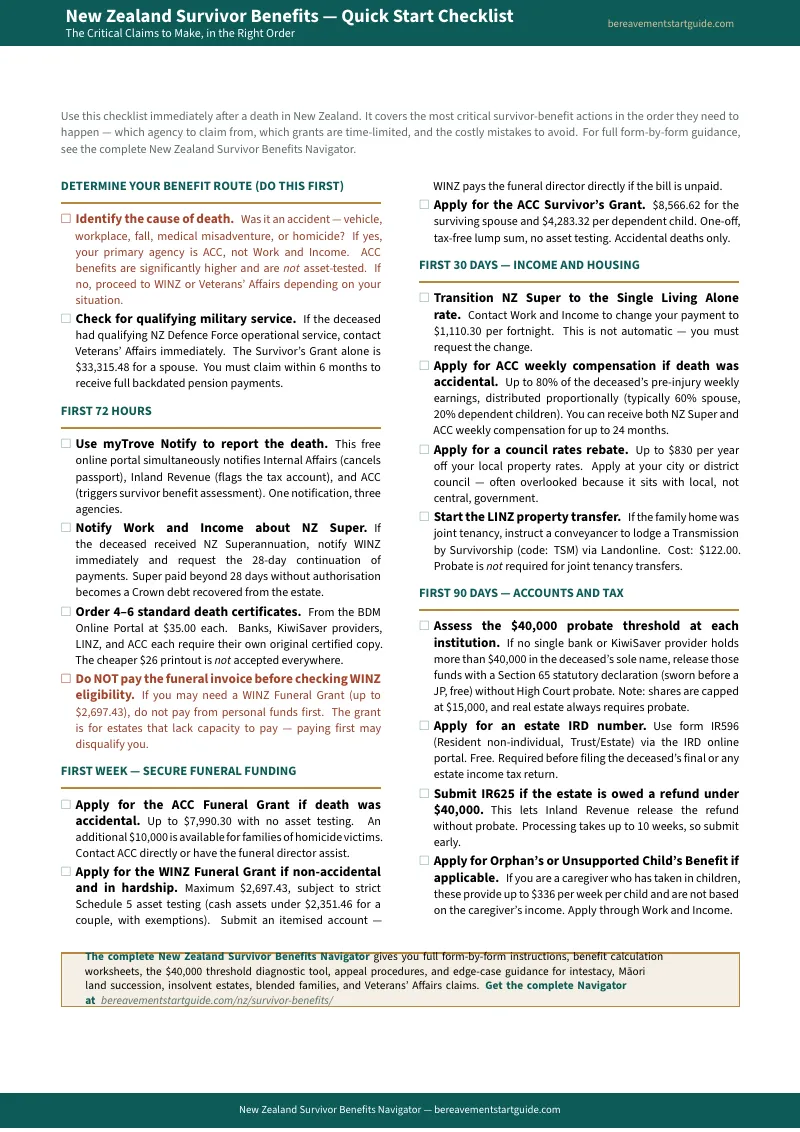

The answer depends entirely on which agency you contact first, which forms you file, and whether you understand the rules that five different government departments assume you already know. ACC provides a funeral grant of up to $7,990.30 with no asset testing whatsoever — but only if the death was caused by an accident. WINZ provides a maximum of $2,697.43, but only if your cash assets fall below $2,351.46 under Schedule 5 of the Social Security Act. Veterans' Affairs offers a survivor's grant of $33,315.48 — but only if you claim within six months to receive the full backdated pension. And none of these agencies will tell you about the others.

The government pages are accurate. They are also scattered across ACC, Work and Income, Veterans' Affairs, LINZ, Inland Revenue, and Births Deaths and Marriages — six agencies that do not reference each other, do not share forms, and do not explain how their rules interact. You are grieving and sleep-deprived, and the system expects you to be a project manager.

The New Zealand Survivor Benefits Navigator is a Cross-Agency Integration Playbook for every benefit, entitlement, and financial transition available to surviving spouses and dependents in New Zealand. Not a list of links. Not a generic checklist that cannot tell ACC from WINZ. A structured, NZ-specific manual that routes you to the right agency based on how the person died, walks you through every form and deadline in the order they actually happen, and flags the moments where applying to the wrong programme first costs your family real money.

What's Inside the Cross-Agency Integration Playbook

A 12-chapter guide and the Survivor Benefits Quick Start Checklist — covering every entitlement from the first 72 hours through estate tax closure, built specifically for New Zealand statutes and the agencies that administer them:

The Benefit Routing Decision Tree

The single most important decision you will make is which agency to contact first. If the death was caused by an accident — motor vehicle crash, workplace incident, fall, medical misadventure, drowning, or homicide — ACC becomes your primary agency, not Work and Income. The ACC funeral grant is up to $7,990.30 with no asset testing. The WINZ funeral grant is capped at $2,697.43 with strict means testing. That difference of over $5,000 depends entirely on routing your claim correctly in the first 48 hours. If the deceased had qualifying military service, Veterans' Affairs offers a survivor's grant of $33,315.48 for a spouse and $13,326.20 per child — but the pension must be claimed within six months of death to receive full backdated payments. The guide's decision tree maps every scenario so you never apply to the wrong agency first.

The $40,000 Probate Threshold Diagnostic

Since September 2025, the threshold for releasing funds without High Court probate has been $40,000 per institution — not per estate. An estate worth $110,000 spread across three providers might not need the High Court at all. But the exceptions are critical: company shares and government bonds remain capped at the legacy $15,000 limit, and real estate held in sole name always requires a formal grant regardless of value. The guide maps the exact scenarios where you can use a Section 65 statutory declaration to bypass the $269 filing fee and the six-to-eight-week court processing time — and where you cannot.

KiwiSaver Death Claim Templates

KiwiSaver balances do not automatically transfer to the surviving spouse. For balances under $40,000, providers require a statutory declaration sworn before a Justice of the Peace — a document that indemnifies the provider and confirms you will distribute the funds in the due course of administration. For balances over $40,000, the provider will demand the High Court probate grant before releasing a dollar. The guide includes line-by-line guidance for the statutory declaration and explains exactly what evidence each provider requires.

LINZ Property Transfer Guide

If the family home was held as joint tenancy, the surviving owner automatically assumes full ownership by the legal principle of survivorship — but the title does not update itself. A conveyancer must lodge a Transmission by Survivorship instrument (code TSM) via Landonline, at a cost of $122. No probate is required for joint tenancy transfers. For sole ownership or tenants in common, the deceased's share falls into the estate and the executor must present the High Court grant before LINZ will process the transmission. The guide explains both pathways in plain English, so you know whether you need a $122 title update or a $269 court application before you call a lawyer.

NZ Super Transition Checklist

When a partner dies, their NZ Super payments stop within 28 days. Any payments made beyond that window become a Crown debt recovered from the estate. The surviving spouse must actively request the transition to the Single Living Alone rate of $1,110.30 per fortnight — it is not automatic. The guide also covers the council rates rebate of up to $830 per year, which most surviving spouses never claim because it sits with local government rather than central government. And if the death was accidental, recent legislative changes allow a surviving spouse to receive both NZ Super and ACC weekly compensation simultaneously for up to 24 months.

Child and Dependent Benefits

If dependent children survive, the entitlements depend on the cause of death. For accidental deaths, ACC provides childcare payments of $182.17 per week for one child, $218.60 for two, and $255.03 for three or more — payable for five years or until the child turns 14. For non-accidental deaths, the Orphan's Benefit provides up to $336 per week per child, and it is not based on the caregiver's income. Grandparents, aunts, and uncles who suddenly take in children are often eligible but do not know these benefits exist. The guide covers both pathways, including how to prepare for a Family Group Conference without triggering an Oranga Tamariki investigation.

Schedule 5 Asset Test Worksheets

Work and Income's funeral grant application demands that you declare all cash and non-cash assets under Schedule 5 of the Social Security Act 2018. The form language is intimidating enough to stop families from applying for benefits they are entitled to receive. The guide translates the asset test into plain English: what counts as a cash asset, whether a small life insurance policy disqualifies you, whether a shared family vehicle is counted, and exactly how to calculate whether your family falls under the $2,351.46 couple threshold.

Veterans' Affairs Pathway

Dependents of qualifying veterans receive a survivor's grant of $33,315.48 for a spouse and $13,326.20 per child, plus a surviving spouse pension of $216.02 per week. But the pension must be claimed within six months of death to be backdated to the day after death — claim later, and entitlement begins only on the date the application is received. The guide maps the complete Veterans' Affairs pathway, including the critical detail that the pension permanently ceases if the surviving spouse enters a new marriage or de facto relationship.

Estate Tax Obligations

The executor must apply for a separate IRD number for the estate using form IR596. Two tax returns are required: the final personal return (IR3) covering April 1 to the date of death, and the estate trust return (IR6) for income earned after death. If the estate is owed a tax refund under $40,000, form IR625 allows Inland Revenue to release the refund without probate — but processing takes up to 10 weeks, so submitting early prevents delays in closing the estate. The guide also covers the student loan write-off that most families do not know about.

Who This Guide Is For

- The surviving spouse whose partner just died — who needs to know whether to contact ACC or WINZ first, how to keep NZ Super payments flowing during the transition, and whether the family home can be transferred for $122 without probate or requires the $269 High Court process

- The adult child managing a parent's affairs — who has been named executor and needs to understand the $40,000 threshold, the KiwiSaver statutory declaration process, and when they can handle things themselves versus when a solicitor is genuinely worth paying for

- The sole parent with dependent children after an accidental death — who needs to claim the ACC survivor's grant ($8,566.62), secure weekly compensation (up to 80% of the deceased's earnings), and apply for childcare payments before the household runs out of money

- The grandparent or relative who has suddenly taken in children — who needs to know that Orphan's Benefit provides up to $336 per week per child regardless of the caregiver's income, and how to apply without fear of triggering an Oranga Tamariki investigation

- The low-income family who cannot afford the funeral — who needs to navigate Schedule 5 asset testing for the WINZ funeral grant without being paralysed by the legal language on the application form

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across six government agencies that do not reference each other. Here is what you actually encounter when you try to navigate survivor benefits using free sources alone:

- Government pages are siloed by agency. ACC explains accidental death benefits but does not mention WINZ. Work and Income explains funeral grants but does not mention ACC. Veterans' Affairs has its own portal entirely. No government website maps the interaction between agencies or explains that ACC benefits supersede WINZ benefits when both could theoretically apply. Applying to WINZ when ACC should have covered the death can result in a denied or later recalled grant.

- The $40,000 probate threshold is widely misunderstood. Media coverage of the September 2025 change led thousands of families to believe any estate under $40,000 avoids probate entirely. The legislation applies per institution for cash and KiwiSaver — company shares remain capped at $15,000, and real estate always requires a court grant. An executor relying on news headlines will attempt to transfer a $20,000 share portfolio using informal administration, only to have the share registry reject the application weeks later.

- LINZ guidance is written for lawyers. The official property transfer documentation uses terms like "Authority and Instruction form," "Landonline pre-validation," and "statutory declaration from the remainderman." Because the language assumes legal training, surviving spouses are pushed toward property lawyers charging $1,000 or more for what is essentially a title update on a house they already own.

- Law firm blogs highlight complexity to justify retainer fees. Firms like Simply Probate, Jackson Russell, and Collins and May publish excellent technical breakdowns. All of their content is designed to convince you the process is too dangerous to handle alone — and that you need a retainer starting at $2,000. For contested estates and complex situations, that is true. For the majority of straightforward cases, the answer costs a fraction of a solicitor's hourly rate.

- Schedule 5 asset testing stops eligible families from applying. The WINZ funeral grant form demands declarations about "cash assets and non-cash assets" using language from the Social Security Act 2018. Families who qualify under the thresholds abandon the application because they cannot parse the legal terminology and fear that a mistake will create a debt to the Crown.

Free resources give you fragments from six agencies that do not talk to each other. The Cross-Agency Integration Playbook connects every entitlement, form, deadline, and agency into one document, in the order you actually need them.

— Less Than Thirty Minutes With a New Zealand Family Lawyer

A single consultation with a New Zealand family lawyer costs $250 to $450 per hour. Standard estate administration retainers start at $2,000 and can reach $5,000 for anything beyond basic probate. The Public Trust charges an hourly rate exceeding $307 before setup fees. This guide costs less than thirty minutes of professional legal time and gives you the complete New Zealand-specific roadmap — the benefit routing decision tree, every form and deadline, the $40,000 threshold diagnostic, the KiwiSaver claim templates, the LINZ property transfer walkthrough, the Schedule 5 asset test worksheets, and the Veterans' Affairs pathway that nobody explains in plain language.

Your download includes 10 PDFs: the complete 12-chapter guide, the Survivor Benefits Quick Start Checklist, plus 8 standalone printable tools — the Benefit Routing Decision Tree, the $40,000 Threshold Diagnostic, the KiwiSaver Claim Worksheet, the LINZ Property Transfer Walkthrough, the NZ Super Transition Checklist, the Schedule 5 Asset Test Worksheet, the Child Benefits Eligibility Guide, and the Forms Portals Fees and Deadlines Reference. Plus a 30-day money-back guarantee. If the guide does not give you clarity on which agency to contact, which forms to file, and what you are entitled to receive, email us for a full refund. No questions asked.

Not ready for the full guide? Download the free New Zealand — Survivor Benefits Checklist — the most critical actions covering everything that must happen in the first 72 hours and first 90 days after a death in New Zealand: benefit routing, funeral grants, NZ Super transitions, property transfers, and the $40,000 threshold assessment. It is enough to get through tonight and tomorrow.

You did not ask for this. But you can navigate it. The guide shows you how, one agency at a time.