The Bank Froze the Account. CPF Won't Respond to the Will. HDB Says the Heir Doesn't Qualify. IRAS Wants a Tax Return for a Dead Person. And Nobody Told You That Inheriting a Flat Could Trigger a Six-Figure Stamp Duty Bill on Your Next Property Purchase.

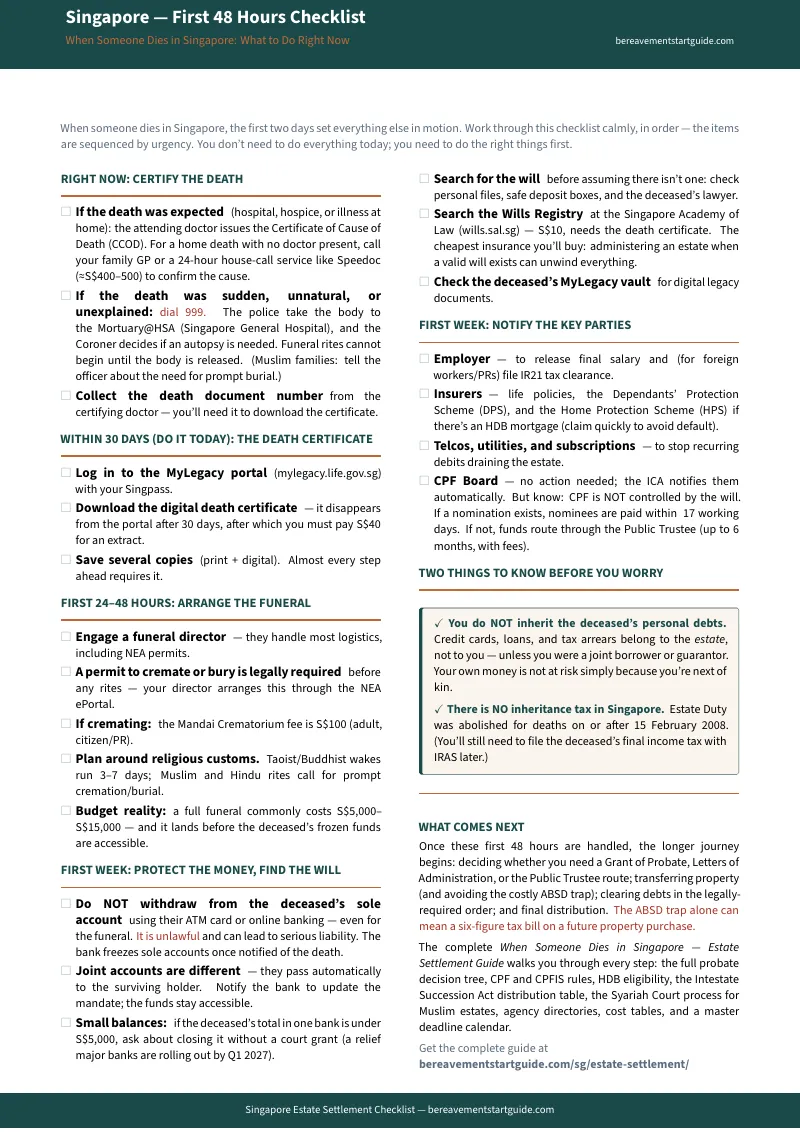

Someone you love has died in Singapore. By day two you are being asked to download a digital death certificate from a government portal that disappears after 30 days, choose between cremation at Mandai and burial at Choa Chu Kang, and somehow pay for a funeral that costs S$5,000 to S$15,000 — using money you cannot access because the bank froze the account the moment they heard.

You searched the MyLegacy portal. It covered the death certificate and funeral booking. Then it stopped. For the next six months — the bank accounts, the property transfer, the CPF money, the court applications, the creditors, the taxes — you are on your own. No single government agency covers the full sequence. No single website gives you the filing order. The CPF Board website tells you that CPF is not part of the will, but does not tell you what to do next. The Family Justice Courts website has forms, but the staff are legally prohibited from telling you which ones to file, or in what order.

The Singapore Estate Settlement Roadmap is a complete Agency Sequencing System built for the reality of Singapore's estate administration — where twelve different agencies each own one piece of the puzzle, and the order you contact them determines whether the process takes three months or eighteen. It maps every agency, every form, every threshold, and every deadline into one chronological sequence: from the death certificate on Day 1 through the final distribution of assets.

What's Inside the Agency Sequencing System

An 11-chapter guide with 3 appendices, a printable 18-item action checklist, and standalone reference sheets — covering every probate pathway, CPF rule, property trap, and agency procedure specific to Singapore law:

Chapters 1–2: Understanding the Landscape and the First 72 Hours

The complete map of Singapore's estate settlement system before you make a single phone call. The three roles you might be playing (executor, administrator, or beneficiary) and what authority each one carries. The two death certification pathways: the digital route through the attending doctor and MyLegacy portal, or the Coroner route through Mortuary@HSA when the death is sudden or unexplained. The critical 30-day window for downloading the digital death certificate — after which it disappears and you pay S$40 for a death extract from ICA. House-call doctor fees for home deaths (S$400–S$500 via services like Speedoc). How many certified copies to order and why four is not enough.

Chapter 3: Funeral Permits, Costs, and Cultural Rites

The NEA ePortal permit requirement — no cremation or burial proceeds without it. Mandai Crematorium fees (S$100 for citizens/PR). Ash storage and sea burial options. The cultural timing realities that affect every other deadline: Taoist/Buddhist wakes run 3–7 days, Muslim rites require prompt burial, Hindu customs expect cremation within 24 hours. How your funeral director handles most logistics, and what they cannot handle for you.

Chapter 4: Securing the Estate — Banks, Notifications, and the Will

Why you must never withdraw from the deceased's sole bank account — even for the funeral — and the legal liability that follows if you do. How joint accounts pass automatically to the surviving holder. The S$5,000 threshold where banks may close a sole account without a court grant. The complete notification sequence: employer (including IR21 tax clearance for foreign workers and PRs), insurers (life policies, DPS, and the Home Protection Scheme to prevent mortgage default), telcos, utilities, and subscriptions. The S$10 Wills Registry search at the Singapore Academy of Law — the cheapest insurance you can buy before assuming intestacy.

Chapter 5: CPF — The Asset That Plays by Its Own Rules

The single most misunderstood asset in every Singaporean estate. CPF is not part of the will and does not form part of the legal estate. If a valid CPF nomination exists, nominees are paid directly — typically within 17 working days, no court required. If no nomination exists (or if it was automatically revoked by a subsequent marriage), the entire CPF balance is swept into the Public Trustee's Office, where distribution takes up to 6 months and comes with tiered administration fees. The CPFIS trap: investments made under the CPF Investment Scheme are not covered by the CPF nomination — they go through probate like any other estate asset. The Dependants' Protection Scheme and Home Protection Scheme claims that must be filed promptly.

Chapter 6: Getting Legal Authority — Probate, Letters of Administration, or the Public Trustee

The decision tree that determines your entire legal pathway. Three options: the Public Trustee (estates under S$50,000 with no real property — cheaper than a lawyer, but not free: administration fees range from 2.25% to 6.50% on a tiered schedule). Grant of Probate (when a valid will exists — court confirms the executor's authority). Letters of Administration (when there is no will — the court appoints an administrator, and you will need two sureties to guarantee the estate's proper handling). Typical timelines: 2–6 months for an uncontested grant. Filing fees: S$74 originating application, plus affidavit fees and disbursements. The complete Intestate Succession Act distribution table — the exact fractions every family fights about — so you can point to the statute instead of arguing.

Chapter 7: Muslim Estates — The Syariah Court and Faraid

The mandatory first step that no other guide sequences correctly. Before you can apply to the Family Justice Courts for a grant, Muslim estates must first obtain an Inheritance Certificate from the Syariah Court — available online through the Syariah Court portal. The Wasiat (Muslim will) is limited to one-third of the estate and cannot benefit anyone already entitled under Faraid. The remaining two-thirds follows Quranic fractional distribution. Respectful, plain-language explanations of the Faraid shares so families can plan without paying a lawyer to read them a table.

Chapter 8: Property — HDB Flats, Private Homes, and the ABSD Trap

The chapter that can save or cost you a six-figure sum. Joint tenancy passes automatically to the survivor — lodge a Notice of Death with SLA and HDB; no court grant needed. Tenancy-in-common and sole ownership go through probate. But inheritance does not guarantee you can keep the HDB flat: the eligibility gauntlet requires Singapore citizenship or PR status, a qualifying family nucleus, and age requirements (single owners must be 35 or older). If you do not qualify, you must sell. The ABSD trap: if a beneficiary already owns private property and inherits an HDB flat, HDB forces a choice — sell the private property or the HDB flat within 6 months. And the inherited property counts toward your total property tally, meaning your next purchase could trigger 20% to 30% ABSD. The CPF refund shock: when an inherited property is sold, the CPF principal used to buy it — plus accrued interest at 2.5% per annum — must be refunded to the deceased's CPF account from the sale proceeds, drastically reducing the cash the beneficiaries actually receive.

Chapters 9–10: Debts, Taxes, Vehicles, and the Final Handover

The strict order of payment that executors must follow before distributing a single dollar — funeral expenses first, then administration costs, then secured debts, then unsecured. Why you do not inherit the deceased's personal debts (unless you were a joint borrower or guarantor). When the estate cannot cover its debts: how insolvent estates work and what beneficiaries actually receive. Filing the deceased's final income tax with IRAS — including the Form T for trust income if the estate generates investment returns during administration. Vehicle transfer and deregistration with LTA. Cross-border asset coordination for overseas relatives. The final handover: distributing assets and closing the estate.

Chapter 11 and Appendices

The decision framework for when you genuinely need a lawyer — contested wills, complex business assets, cross-border estates, insolvent estates — and how to walk in organised so you pay for an hour, not ten. Appendix A: the complete agency directory with phone numbers, addresses, and operating hours for every agency referenced in the guide. Appendix B: the cost reference table — every fee, filing cost, and threshold in one place. Appendix C: the master deadline table so you never discover a deadline after it has passed.

Who This Guide Is For

- The surviving spouse whose joint account still works but whose partner's sole account just vanished — and who needs to understand which assets pass automatically, which require a court grant, and whether the CPF nomination exists or whether six months of Public Trustee processing is about to begin.

- The adult child who just discovered that CPF is not covered by the will — and that the deceased's marriage automatically revoked an old nomination nobody remembered to update, routing hundreds of thousands of dollars to the Public Trustee instead of the people they expected.

- The executor who was named in the will and has no idea what that means — who needs to know the exact forms, the exact court, the exact fees, and the exact order of operations before paying a probate lawyer S$300 to S$700 an hour to explain what this guide covers in plain English.

- Families inheriting an HDB flat who also own private property — and who need to understand the ABSD trap, the 6-month forced sale window, and the option to formally renounce the inheritance to preserve first-time buyer status before a six-figure tax mistake becomes irreversible.

- Muslim families navigating the dual-track system — Syariah Court for the Inheritance Certificate, then the Family Justice Courts for the grant — who want clear, respectful explanations of Faraid distribution without paying a lawyer to translate a table.

Why Free Government Websites Do Not Replace a Sequenced Estate Guide

Every agency referenced in this guide has a public website. The CPF Board explains nominations. The Family Justice Courts list their forms. HDB has a page on property transmission. MyLegacy covers the death certificate. Here is why the websites alone are not enough:

- No government website covers the full sequence. MyLegacy handles the death certificate and stops. CPF handles nominations and stops. HDB handles flat eligibility and stops. SLA handles private property title and stops. IRAS handles taxes and stops. Nobody connects them. An executor who follows one agency's instructions to completion before starting the next can waste months because the agencies need to be contacted in a specific, overlapping order.

- Law firm websites explain the problem and withhold the solution. Singapore probate firms publish detailed articles about inheritance complexity. The content is accurate. It is also deliberately incomplete — designed to trigger a consultation call at S$300 to S$700 an hour, not to empower you to organise the estate yourself. The question is not "how complicated is this?" but "does my estate actually require a lawyer?" For many Singapore estates, the answer is no.

- Forum advice is legally dangerous. HardwareZone threads and Reddit posts advise families to quietly withdraw cash from the deceased's ATM before the bank finds out. This is unlawful. The guide gives you legal pathways to access funds — including the S$5,000 bank threshold and insurance claims — without creating liability.

- Singapore has estate hazards that no generic guide covers. The CPF-will disconnect. The CPFIS exception to CPF nominations. The ABSD trap on inherited HDB flats. The automatic revocation of CPF nominations by marriage. The Syariah Court prerequisite for Muslim estates. The Public Trustee fee tiers. These are not footnotes — they are the issues that cost Singapore families thousands of dollars when they follow national templates or overseas guides.

Free resources give you one agency at a time, with no sequencing, no cross-referencing, and no way to know what you are missing. The Agency Sequencing System maps every agency, every form, and every deadline into one chronological roadmap — so you claim everything, avoid every common trap, and know whether you actually need a lawyer before spending a dollar on one.

— Less Than Fifteen Minutes of a Probate Lawyer's Time

Singapore families lose weeks and thousands of dollars every year — not because the estate was complicated, but because nobody told them the order. An executor distributes assets before clearing debts with IRAS and faces personal liability. A family assumes the will controls CPF and discovers six months later that the money went to the Public Trustee. An heir inherits an HDB flat without understanding the ABSD implications and triggers a 20% stamp duty bill on their next property purchase. A Muslim family applies to the Family Justice Courts before obtaining the Syariah Court Inheritance Certificate and has the application rejected. This guide costs less than any of those mistakes.

Your download includes the complete 11-chapter guide with 3 appendices, the Singapore — First 48 Hours Checklist, and standalone printable reference sheets — covering every time-sensitive step from downloading the death certificate on Day 1 through the court application, the property transfer, the creditor sequence, and the final distribution.

30-day money-back guarantee. If the guide does not give you a clear map of every probate pathway available for your Singapore estate, every agency you need to contact, and every deadline you need to meet — email us for a full refund. No questions asked.

Not ready for the full guide? Download the free Singapore — First 48 Hours Checklist — a summary of the most urgent actions, agency contacts, and financial traps that most families do not discover until it is too late. Enough to protect the estate on day one.

You did not plan for this. But you can plan what happens next. The guide gives you the agencies, the deadlines, the legal pathways, and the filing sequence — so the next six months are spent settling the estate correctly, not discovering what you missed.